Автор: Andjela Radmilac

Перевод: Deep Tide TechFlow

Введение от Deep Tide: ETF решили только вопрос "как купить биткойн", но никто не заметил, что Уолл-стрит уже использует его для того же, для чего используют казначейские облигации и золото: для залоговых кредитов, страховых резервов, рейтинговых облигаций. Кризис ликвидации в феврале доказал, что эта система выдерживает давление, но также обнажил смертельный недостаток коллективного сброса в цепочке левериджа.

Все знают об ETF, но почти никто не знает, что в то время как ETF поглощают всё внимание, существует несколько десятков институциональных продуктов, построенных вокруг биткойна — от 40-миллионных страховых резервов на Барбадосе до выпуска рейтинговых облигаций от Standard & Poor's, продаваемых Jefferies инвесторам с Уолл-стрит.

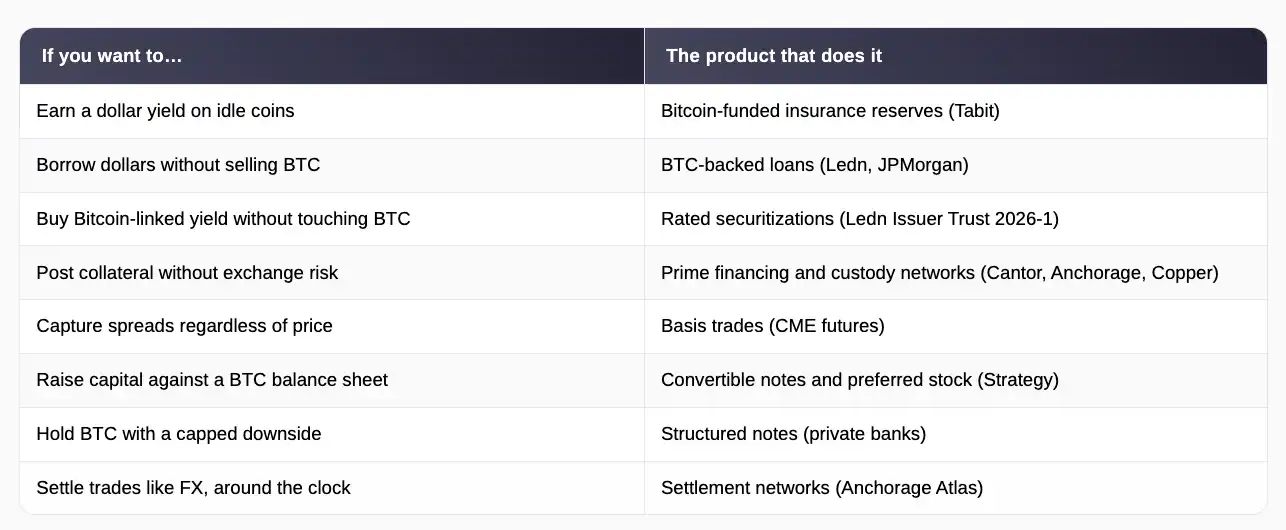

ETF ответили только на один вопрос: как обычные инвесторы и институты могут владеть биткойном в регулируемой упаковке. Продукты, описанные в этой статье, отвечают на другой, возможно, более важный вопрос: как только у вас есть биткойн, что вы можете с ним делать?

Ответ: то же самое, что финансовая индустрия всегда делала с казначейскими облигациями США и золотом. Вы можете заложить его, чтобы занять деньги, использовать его в качестве маржи для сделок, использовать как резерв для страхового полиса или строить на его основе корпоративные балансы.

Актив, способный на всё это одновременно, иногда называют финансовым примитивом — это модный способ сказать «строительный блок»: нечто, широко принимаемое и легко оцениваемое, на чём остальные части финансовой системы могут надстраивать кредиты, облигации и деривативы. Казначейские облигации получили этот статус, потому что все согласны с их стоимостью и с тем, как их арестовать, если сделка пойдёт не так.

Сейчас биткойн проходит тот же тест, и ранние результаты объясняют, почему некоторым крупнейшим участникам этого рынка абсолютно всё равно, растёт цена или падает.

Страховые резервы, потребительский кредит и первые рейтинговые биткойн-облигации

В марте 2025 года компания Tabit Insurance, основанная бывшими руководителями биржи Bittrex и лицензированная на Барбадосе, капитализировала агентство по страхованию имущества и несчастных случаев на сумму 40 миллионов долларов, полностью обеспеченную биткойном.

По сути, владельцы биткойна передают его для поддержки реальных страховых полисов, покрывающих ущерб от штормов и судебные иски против директоров компаний, а взамен получают доходность, близкую к 10% в долларах. Полисы и премии остаются в долларах, поэтому клиенты никогда не контактируют с криптовалютой, а биткойн служит резервом для выплат претензий в случае проблем.

Tabit имеет лицензию 2-го класса от Комиссии по финансовым услугам Барбадоса и учреждена как компания с раздельными счетами, что означает, что каждый пул средств инвесторов юридически изолирован от других, поэтому убытки по одному счету не истощают капитал другого.

Регуляторы и аудиторы также могут в реальном времени проверять резервы в блокчейне, обеспечивая большую прозрачность, чем та, которую традиционные страховщики предоставляют в своих квартальных отчётах. Генеральный директор Стивен Стоунберг заявляет, что вся глобальная индустрия перестрахования работает примерно на 800 миллиардах долларов капитала, в то время как биткойн — это класс активов стоимостью в триллионы, поэтому даже небольшая часть этого богатства, направленная в страховой бизнес, будет ощущаться во всей отрасли.

Хотя страховые резервы — действительно довольно неожиданный вариант использования биткойна, кредитование — это то место, где начинаются серьёзные деньги. Биткойн-залоговые кредиты работают просто: вы закладываете свои монеты кредитору, получаете доллары, а когда возвращаете долг — получаете монеты обратно.

Владельцы делают это, потому что продажа спровоцирует налогооблагаемую прибыль и лишит их возможности получить выгоду от будущего роста цены, в то время как кредит под залог монет даёт им наличные, не заставляя отказываться ни от одной из них.

Объёмы сделок на различных платформах в 2025 году достигли примерно 20 миллиардов долларов, а компания Ledn из Торонто сообщила, что с 2018 года выдала более 95 миллиардов долларов. JPMorgan и другие крупные банки теперь также предлагают аналогичные продукты своим клиентам.

В феврале 2026 года этот кредитный бизнес вышел на основной рынок облигаций. Ledn завершила секьюритизацию на сумму 1,88 миллиарда долларов. Это означает, что она объединила 5441 кредит в пул и продала облигации, процентные выплаты по которым происходят из платежей заёмщиков.

Облигации были разделены на два уровня: старшие ноты на 1,6 миллиарда долларов получают выплаты в первую очередь, рейтинг Standard & Poor's — BBB- (инвестиционный уровень, впервые присвоенный ценным бумагам, обеспеченным цифровыми активами), и младшие ноты на 2800 миллионов долларов с более высоким риском, рейтинг B-, которые принимают на себя первые убытки в обмен на более высокую доходность.

По криптостандартам, базовые цифры довольно консервативны. 2914 американских заёмщиков в пуле должны 199,1 миллиона долларов, но заложили примерно 4079 BTC стоимостью 356,9 миллиона долларов, что означает соотношение суммы кредита к стоимости залога (LTV) 55,8%. Это значит, что они заложили почти 2 доллара в биткойнах за каждый занятый 1 доллар.

Генеральный директор Ledn Адам Ридс заявляет, что такая структура создаёт «прямой канал» между держателями биткойнов, ищущими ликвидность, и самым глубоким в мире пулом институционального капитала. А европейский руководитель исследований Bitwise Андре Драгос говорит, что эта сделка доказывает, что традиционные финансы теперь рассматривают биткойн как законный и даже первоклассный залог.

Эта структура почти сразу подверглась стресс-тесту, выявив как силу, так и уязвимость всей модели. Цена биткойна упала примерно на 27% с середины января по февраль 2026 года, что повысило LTV всего пула и спровоцировало маржин-коллы — автоматические требования к заёмщикам либо увеличить залог, либо наблюдать, как кредитор его продаст.

В итоге Ledn ликвидировала около четверти кредитов, изначально предназначенных для этой сделки. Продажа всё равно состоялась, отчасти потому, что эти автоматические ликвидации сработали именно так, как были задуманы, и Ledn никогда не несла убытков при продаже залога из-за дефолта.

Обратную сторону следует запомнить: когда многие кредиторы применяют одинаковые триггеры к одному и тому же волатильному активу, резкое падение цены заставляет их продавать одновременно, и эти продажи ещё больше снижают цену, запуская новые продажи. Система прошла первый настоящий тест, но она также показала, где она рухнет при достаточном давлении.

Сети залога, керри-трейд и корпоративные балансы

Под этими продуктами базовые механизмы рынка перестраиваются, и они начинают больше походить на денежный рынок и рынок облигаций, где компания, хранящая ваши активы, платформа, на которой вы торгуете, и система, обрабатывающая сделки, — это три разные вещи.

Anchorage Digital, оператор единственного в США федерально зарегистрированного криптобанка, в апреле 2024 года запустила свою сеть расчётов Atlas, чтобы институты могли напрямую рассчитываться друг с другом, не размещая средства на счетах у кастодиана или не предварительно пополняя счета на биржах.

К марту 2026 года Atlas подключила почти 600 участников, что в четыре раза больше, чем годом ранее, обработала сотни миллиардов долларов расчётов и расширила функционал до управления залогом. Это означает, что банк теперь отслеживает кредитные позиции для кредиторов, отправляет маржин-коллы и обрабатывает ликвидации.

Cantor Fitzgerald в марте 2025 года выбрала Anchorage и Copper.co для этой роли в своём глобальном бизнесе по биткойн-финансированию. Система ClearLoop от Copper позволяет торговым компаниям блокировать монеты у кастодиана, при этом продолжая торговать на нескольких биржах, так что повторение краха FTX не унесёт активы клиентов.

Всё это делает использование биткойна в качестве маржи таким же рутинным и безопасным, как предоставление казначейских облигаций, и это предпосылка для расширения всего остального, упомянутого в этой статье.

Огромные объёмы институциональных средств, протекающие через эту инфраструктуру, не имеют никакого мнения о биткойне как таковом. Керри-трейд (торговля на разнице базиса) — одна из самых популярных институциональных стратегий с момента запуска ETF. Она использует тот факт, что фьючерсы на биткойн обычно стоят немного дороже спота: фонды покупают спотовый биткойн или доли ETF, одновременно продавая фьючерсный контракт по более высокой цене, и зарабатывают на разнице независимо от того, как изменится цена дальше, потому что прибыль по одной позиции компенсирует убыток по другой.

После того как ETF предоставили фондам простой способ держать спотовую часть, хедж-фонды нарастили рекордные короткие позиции в фьючерсах CME, где открытый интерес вырос примерно с 30 000 контрактов в начале 2024 года до пика около 45 000 в ноябре того же года.

Эта сделка стала настолько большой, что её закрытие теперь само по себе может двигать рынок. Открытый интерес CME в апреле 2026 года упал ниже 10 миллиардов долларов, поскольку эти парные позиции закрывались, и механические продажи давили на цену, независимо от настроений кого бы то ни было.

CME продолжает строить инфраструктуру для этой группы, введя в мае 2026 года круглосуточную торговлю, а в июне запустив фьючерсы на индекс волатильности биткойна, позволяя институтам делать ставки или хеджировать интенсивность ценовых колебаний, а не их направление.

Корпоративные казны доводят эту идею дальше всего. По состоянию на конец мая 2026 года MicroStrategy владеет 843 738 BTC. Компания выпустила конвертируемые облигации на 6,7 миллиарда долларов (это облигации, которые можно конвертировать в акции, если цена акций вырастет), плюс привилегированные акции на 15,5 миллиарда долларов, разделённые на пять различных инструментов — ценные бумаги с фиксированными дивидендами, находящиеся между долгом и обыкновенными акциями, чтобы финансировать свои безумные покупки BTC.

Только в 2025 году она привлекла 25,3 миллиарда долларов, став крупнейшим эмитентом акций в США в том году (около 8% от всех размещений). Она продавала привилегированные ценные бумаги как «цифровой кредит» — полноценную линейку продуктов с фиксированным доходом, дивиденды по которым в конечном счёте обслуживаются биткойн-балансом.

Акционеры через акции фактически получают левериджированный доступ к биткойну; инвесторы, ориентированные на дивиденды, получают двузначную доходность, обеспеченную монетами. От котирующейся в Токио Metaplanet до подражателей Semler Scientific — все копируют рискованную стратегию Майкла Сэйлора.

Частные банки запускают параллельные сборочные линии для состоятельных клиентов, упаковывая структурированные ноты, которые ограничивают риски снижения биткойн-экспозиции ценой отказа от части потенциального роста, позволяя консервативным портфелям держать актив, который иначе был бы для них слишком волатильным.

Это завершает круг парадокса, с которого начиналась статья.

ETF ответили на вопрос, как институтам владеть биткойном, а продукты, описанные в этой статье, отвечают на вопрос, для чего им владеть им. Актив, который одновременно капитализирует карибскую перестраховочную компанию, поддерживает инвестиционные облигации, обеспечивает маржу для деривативов CME и обслуживает дивиденды по привилегированным акциям, уже далеко ушёл от спекулятивного принятия и вошёл в рабочие механизмы финансов.

Будущие историки этого рынка, возможно, будут рассматривать ETF как видимый первый слой институционализации, в то время как устойчивые изменения происходят в системах финансирования и расчётов, где биткойн выполняет ту же работу, которую казначейские облигации и золото выполняли на протяжении поколений: служит залогом, на котором строится всё остальное.

Риски реальны, как доказал февральский кризис ликвидации, и они растут вместе с левериджем. Но направление, похоже, уже определено. Самая важная институциональная роль биткойна, возможно, никогда не появится на графиках потоков средств, потому что он становится частью самой машины.