Author:100y

Compiled by: Deep Tide TechFlow

Deep Tide Intro: While Saylor is shouting about increasing the BTC per share, he is issuing shares below the break-even point and only using half of the raised money to buy BTC—this is not bottom fishing, this is using MSTR shareholders' interests to subsidize STRC's sustainability. For investors holding MSTR, understanding the logic behind this trade is more important than focusing on how much BTC was bought.

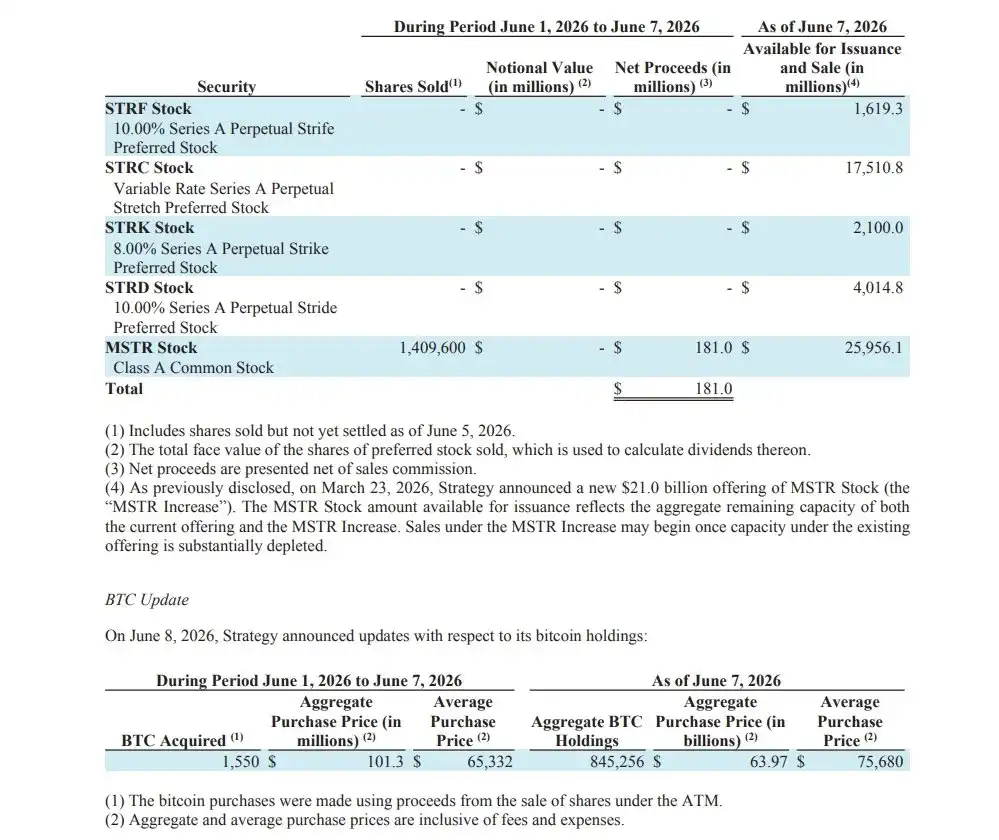

Saylor first sold 32 BTC, then turned around and bought 1,550 BTC today.

I don't want Strategy to fail. But some things must be made clear.

This is one of the worst trades.

On the surface, this trade looks beautiful. Strategy bought a large amount of BTC near recent lows and even increased its dollar reserve for preferred stock dividends from $900 million to $1 billion.

Is this Strategy's revival?

If you think this is positive, it means you don't fully understand Strategy yet.

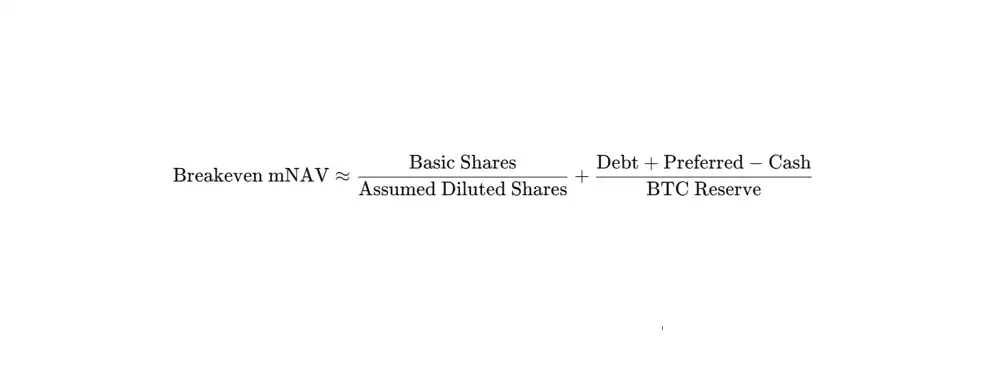

1. You Need to Understand the Break-Even mNAV

One of Strategy's core objectives is to increase the BTC per share (BPS) for MSTR shareholders.

The method to increase BPS is simple: issue common stock at a premium and use the raised funds to buy BTC.

So, how high a premium does MSTR need to issue shares via ATM offerings to truly increase BPS?

According to the 2026 Q1 earnings call, the mNAV needs to be above 1.22.

This is the so-called "break-even mNAV."

This concept comes from a simple condition: the amount of BTC that can be bought by selling 1 share of MSTR must be greater than the BTC amount corresponding to each existing MSTR share.

The complete derivation process can be referred to in my previous article.

In the end, the break-even mNAV is calculated as follows:

By the way, the current break-even mNAV is no longer 1.22.

Based on the data before this purchase of 1,550 BTC, my calculated result is 1.30.

2. The Worst Trade

Now back to Strategy's purchase of these 1,550 BTC.

Strategy raised $181 million through MSTR's ATM offering, of which $101.3 million was used to purchase 1,550 BTC.

There are two issues here:

First, MSTR's ATM offering seems to have been conducted at an mNAV below 1.30. Selling shares to buy BTC below the break-even mNAV is not increasing BPS; it's diluting it.

Second, and this is the key point: not all ATM-raised funds were used to buy BTC. The entire concept of break-even mNAV is based on the premise that 100% of the raised funds are used to buy BTC. Even if the mNAV is high enough, if only part of the funds flows into BTC, this trade can still lower BPS.

Strategy seems to have added the remaining unused funds to the dollar reserve.

In other words: Strategy sacrificed MSTR shareholders' shares and BPS to maintain STRC's sustainability.

In fact, after this trade, Strategy's BPS decreased by approximately 0.19% compared to before the trade.

What did they gain in return?

The available time for the dollar reserve was extended from about 6.3 months to 7 months.

3. Strategy's Bet

"Our goal is to drive the BTC per share up, and we are doing everything we can to drive the BTC per share up."

These are the words of Michael Saylor in the 2026 Q1 earnings call.

But in this trade, Strategy sacrificed MSTR's BPS for STRC.

Strategy has rolled the dice.

If sacrificing BPS can reverse market sentiment, restore STRC's price, and pull the mNAV back up, then Strategy can continue raising funds through MSTR and STRC's ATM offerings.

But what if sentiment doesn't improve?

Then Strategy may have no choice but to continue sacrificing MSTR.

In the worst-case scenario, either delaying STRC's dividend payments...

Or slowly bleeding out.

Pray for BTC, MSTR, and STRC to recover.

Amen.