Оригинал | Odaily Planet Daily(@OdailyChina)

Автор | Ляоляо

Криптовалютный рынок, особенно сектор децентрализованных финансов (DeFi), постоянно ищет базовые активы, сочетающие стабильность, высокую ликвидность и высокую доходность. По мере того, как доходность традиционных активов реального мира (RWA, таких как казначейские облигации США) постепенно стабилизируется, жажда DeFi-рынка к высокодоходным приносящим проценты активам породила новый парадигмальный сдвиг. На этом фоне проекты стейблкоинов на базе STRC набирают популярность с впечатляющей скоростью.

Стейблкоины, как краеугольный камень криптомира, прошли путь эволюции от ранних обеспеченных фиатом (таких как USDT, USDC), к обеспеченным с избыточным залогом криптоактивами (таким как USDS), затем к алгоритмическим (таким как обанкротившийся UST) и в последние годы — к основанным на арбитраже базисной разницы (таким как USDe).

Однако нынешняя рыночная проблема заключается в том, что доходность стейблкоинов ниже 10% или даже 5% уже не может удовлетворить потребность в премии за риск у средств в блокчейне, в то время как чрезмерно высокая алгоритмическая доходность часто сопровождается системными рисками, такими как «смертельная спираль».

Проекты стейблкоинов на базе STRC как раз вовремя заполняют этот пробел. Судя по темпам роста TVL, потокам средств в блокчейне и накалу дискуссий в сообществе, создание стейблкоинов на основе STRC стало одной из самых обсуждаемых ниш на текущем рынке DeFi.

Особенно при поддержке протоколов доходности, таких как Pendle и Morpho, эти продукты перестали быть просто «стейблкоинами» и начали эволюционировать в новую форму актива, сочетающую стабильность, доходность и финансовую композируемость.

Что такое STRC?

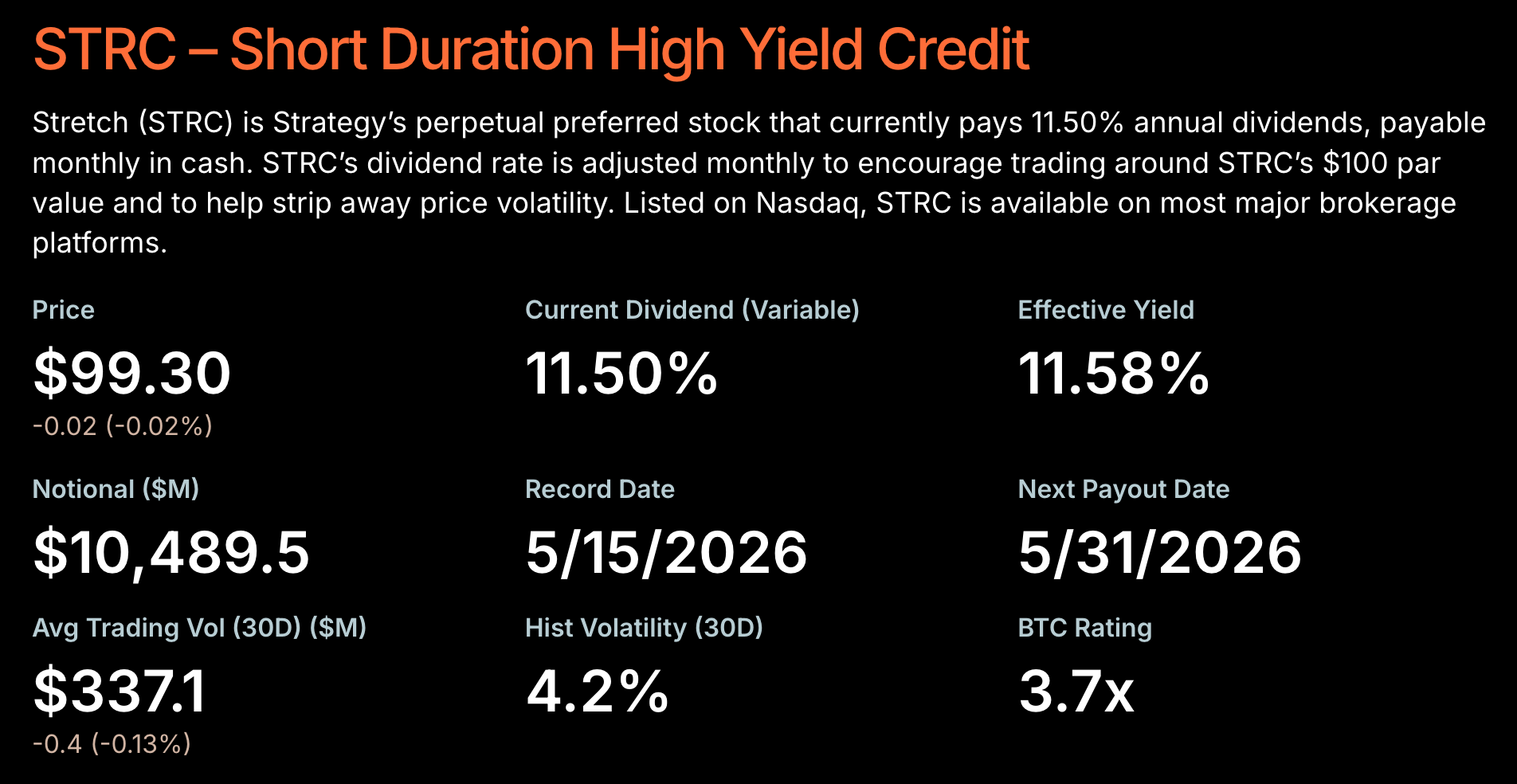

STRC означает «биткойн-кредитный инструмент», выпущенный казначейской компанией MicroStrategy.

Примечание Odaily: подробный разбор STRC см. в статье «Десять тысяч слов о STRC: новый фокус MicroStrategy по привлечению денег для покупки биткойнов».

Проще говоря, MicroStrategy привлекает финансирование на рынке, выпуская STRC, а затем на полученные средства непрерывно скупает биткойны. Держатели STRC, в свою очередь, получают плавающие процентные выплаты с доходностью более 12.3% ежемесячно. В отличие от традиционных облигаций, STRC является привилегированной акцией, а не долговым обязательством, поэтому не имеет фиксированной даты погашения; в то же время ее права на дивиденды выше, чем у обыкновенных акций (MSTR), что придает ей сильные свойства, схожие с инструментами с фиксированным доходом.

Самая особая черта STRC заключается в том, что она фактически превращает долгосрочные ожидания роста Биткойна в продукт «цифрового кредита» (Digital Credit), приемлемый для традиционного рынка капитала.

Чтобы STRC оставалась стабильной вблизи номинала в 100 долларов, MicroStrategy динамически корректирует свою дивидендную доходность — когда STRC падает ниже номинала, доходность повышается для привлечения средств; когда STRC выше номинала, премия подавляется за счет дополнительной эмиссии.

С момента запуска STRC компанией MicroStrategy, благодаря относительно стабильным характеристикам «привязки» (после нескольких кратковременных отклонений она успешно восстанавливалась) и относительно привлекательной доходности, рыночный отклик был весьма положительным.

На момент публикации общий объем выпуска STRC превысил 104 миллиарда долларов США, что составляет более 60% от общего объема выпуска привилегированных акций на всем рынке в 2026 году.

Ранее в этом месяце основатель MicroStrategy Майкл Сэйлор в интервью Дэвиду Лину прямо заявил — такие продукты цифрового кредита, как STRC, и есть «убийственное приложение» Биткойна (см. «Интервью с Майклом Сэйлором: я говорил, что продам, но точно не буду чистым продавцом»).

Однако традиционные доли STRC обычно обращаются только среди хедж-фондов Уолл-стрит, регулируемых институтов и состоятельных квалифицированных инвесторов. Пользователям DeFi в блокчейне из-за барьеров, регулирования и ограничений каналов капитала трудно напрямую получить доступ к этому высокодоходному продукту, который захватывает традиционные финансовые рынки.

Именно здесь начинает действовать наш главный герой, Apyx.

Apyx выступает в роли моста между инструментами цифрового кредита с Уолл-стрит и блокчейн-лего DeFi, то есть через инновационную финансовую архитектуру в блокчейне вводит возможности получения сверхдоходности от STRC в блокчейн, создавая следующее поколение процентных стейблкоинов с высокой ликвидностью, композируемостью и еще более высокой доходностью.

Деконструкция Apyx: возможно, самый доходный стейблкоин на рынке

В отличие от многих проектов стейблкоинов, которые полагаются на нарративы аирдропов и не имеют реальных источников дохода, основное конкурентное преимущество Apyx заключается не только в «более высокой APY», но и в сочетании способности привлекать капитал из традиционных финансов и композируемости протоколов в блокчейне.

Что касается предыстории, ключевой стороной, стоящей за Apyx, является публичная казначейская компания DeFi Development Corp, которая не только участвовала в инкубации и стратегических инвестициях в Apyx, но и предоставила ему ключевой мост, соединяющий традиционный рынок капитала с миром блокчейна.

В дизайне продукта Apyx использует модель из двух токенов: apxUSD + apyUSD.

apxUSD больше похож на традиционный стейблкоин, привязанный к 1 доллару США, и в основном выполняет функции средства обмена и обеспечения ликвидности в блокчейне. Сам apxUSD не накапливает доход автоматически, он больше похож на высоколиквидный «базовый долларовый актив», пригодный для торговли, платежей, кредитования и т.д.

Настоящую основную ценность Apyx воплощает apyUSD — пользователи могут заблокировать apxUSD, чтобы получить apyUSD (разблокировка занимает 20 дней), последний похож на wstETH от Lido, его цена постоянно растет по мере накопления дохода от базового актива. Другими словами, apyUSD сам является носителем дохода.

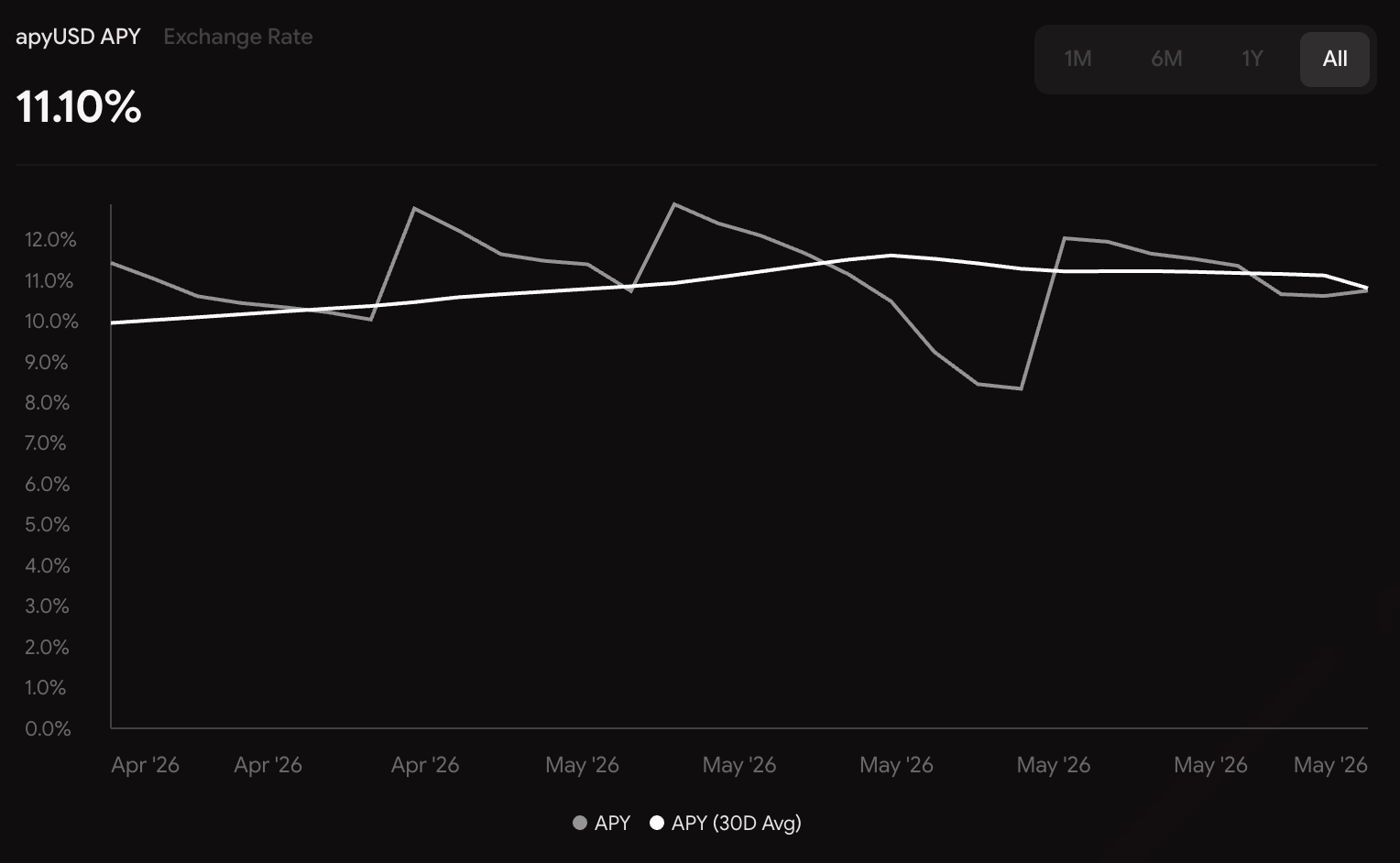

В настоящее время реальная годовая доходность apyUSD составляет около 11%, а ожидаемая годовая доходность превышает 13%. На фоне продолжающегося снижения общей доходности долларовых стейблкоинов, актив в виде стейблкоина, обладающий реальным источником дохода и двузначной доходностью, естественно, обладает особой привлекательностью.

Кроме того, важно подчеркнуть, что в отличие от многих проектов стейблкоинов, которые полагаются на субсидии токенов для достижения краткосрочной высокой доходности, основной доход Apyx поступает от дивидендных выплат STRC, что делает источник дохода более стабильным и устойчивым.

Данные Defillama показывают, что с момента запуска в конце февраля этого года эмиссия apxUSD менее чем за три месяца быстро достигла 502 миллионов монет, и Apyx стал 21-м по величине протоколом стейблкоинов в мире DeFi.

Конечно, одной только доходности недостаточно для поддержки экосистемы стейблкоина. То, что действительно определяет потенциал протокола, — это композируемость активов и эффективность ликвидности. И в этом аспекте Apyx явно проделал большую работу — в настоящее время Apyx уже глубоко интегрирован с несколькими основными протоколами, включая Morpho, Curve и Pendle.

На Morpho пользователи могут использовать apyUSD в качестве залога для заимствования других активов, реализуя операцию «получать доход и одновременно высвобождать ликвидность», а более агрессивные игроки могут даже использовать рекурсивное кредитование для увеличения экспозиции к доходу; Curve отвечает за решение проблемы ликвидности. Создавая торговые пулы между apxUSD и основными стейблкоинами, такими как USDC и USDT, Apyx обеспечивает низкий проскальзывание при крупных обменах, что критически важно для системы стейблкоинов.

Что касается Pendle, то это, возможно, самая взрывная часть всей экосистемы Apyx. Поскольку Pendle может разделять доходные активы на PT (основную сумму) и YT (права на доход), apyUSD перестает быть просто активом «держи и получай проценты», а превращается в доходный продукт, который можно торговать, использовать с кредитным плечом и спекулировать на нем — консервативные пользователи могут фиксировать фиксированный доход через PT; а более агрессивные пользователи могут увеличить ставку на будущую доходность, покупая YT.

Именно благодаря такой высокой степени композируемости, экосистема Apyx расширяется заметно быстрее, чем многие традиционные протоколы стейблкоинов.

В некотором смысле, Apyx делает не просто «выпуск высокодоходного стейблкоина», а скорее пытается создать целый рынок кредита в блокчейне, построенный вокруг STRC.

Программа очков и стратегии их получения

На нынешнем рынке DeFi «очки» давно перестали быть простым инструментом мотивации пользователей, а стали скорее способом предварительного определения будущих прав на токены. Особенно теперь, когда рынок снова вступает в фазу конкуренции за ликвидность, способность проекта постоянно привлекать средства часто зависит от двух вещей — достаточно ли высока доходность и достаточно ли определенны ожидания относительно токена.

И то, что Apyx смог быстро собрать значительный TVL за короткое время, во многом связано с его текущей системой очков. Согласно официальному плану, программа очков Apyx реализуется поэтапно:

- Season 1 завершилась 22 мая 2026 года, и официально подтверждено, что 5% от общего предложения токенов будет распределено среди ранних участников этого этапа;

- После окончания Season 1 сразу же начался Season 2, который продлится до 11 октября, с продолжением раздачи 6% токенов в качестве стимулов;

- После окончания Season 2, Apyx проведет TGE и аирдроп 13 октября.

Такой ритм очень умный. С одной стороны, сроки окончания каждого сезона создают естественные «окна для рывка», побуждая средства ускорить приток перед закрытием; с другой стороны, плавный переход к Season 2 позволяет избежать проблемы, характерной для многих проектов: «окончание первого сезона приводит к обвалу TVL»; самое главное, Apyx уже определил четкую дату TGE и аирдропа на следующий год, что дает пользователям более ясные ожидания от взаимодействия.

Для рынка это означает, что ожидания аирдропа Apyx — не краткосрочное событие, а скорее война за ликвидность, длящаяся несколько месяцев. С точки зрения пользователя, более важный вопрос — «как эффективнее получать очки».

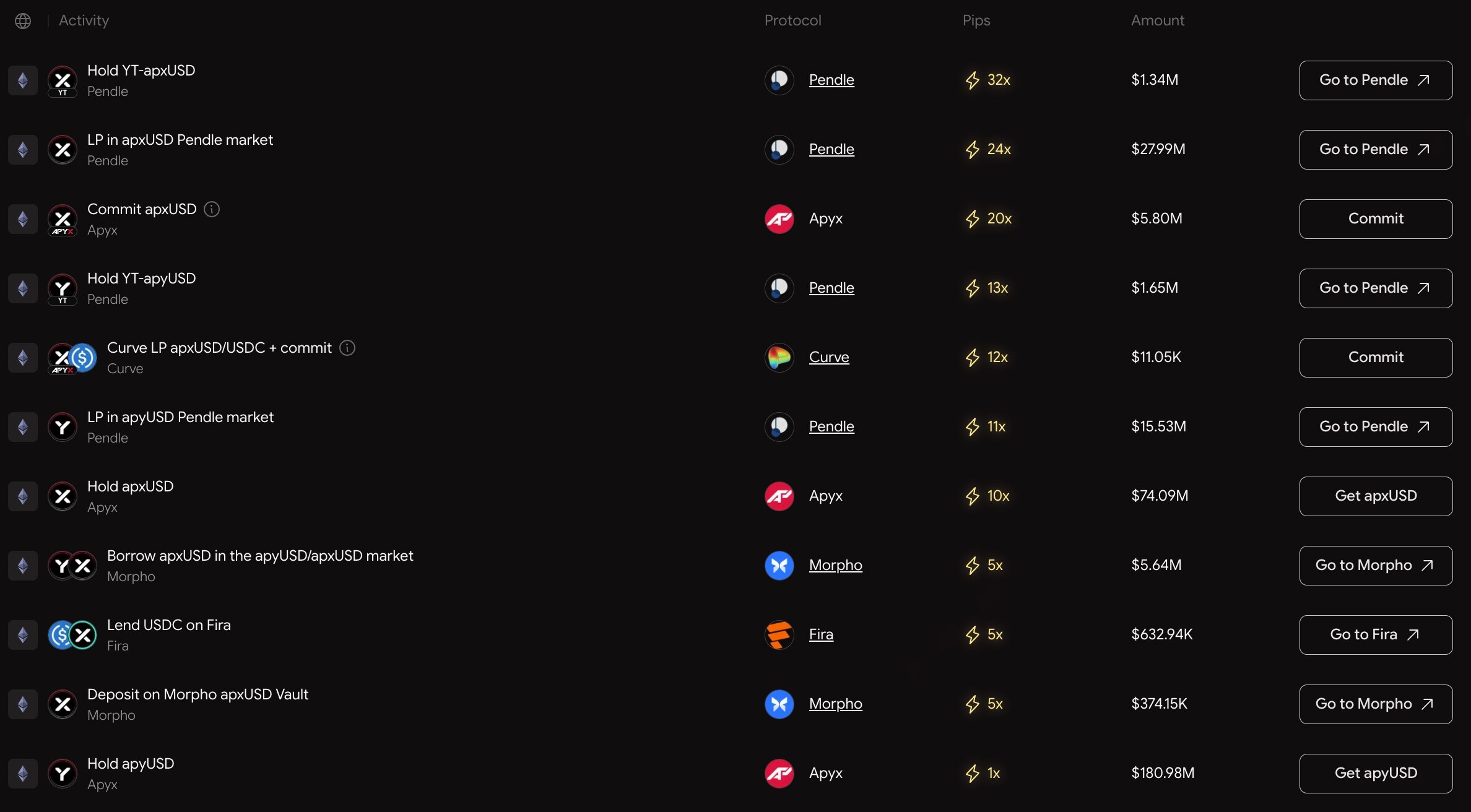

Apyx на своем официальном сайте указывает эффективность получения очков для различных операций, грубо говоря, их можно разделить на две категории: «базовый режим» и «продвинутый режим».

«Базовый режим» — это простое хранение apxUSD (10-кратные очки) или apyUSD (1-кратные очки); «Продвинутый режим» — гибкое использование вышеупомянутых интегрированных протоколов, например, заимствование или кредитование apxUSD на Morpho (5-кратные очки), или создание LP для apxUSD на Curve (12-кратные очки). Самая эффективная стратегия связана с Pendle: прямое хранение YT для apxUSD дает сразу 32-кратные очки, создание LP для apxUSD на Pendle также дает 24-кратный множитель очков.

Конкурентная ситуация в нише и преимущества Apyx

Как зарождающаяся ниша, находящаяся на очень ранней стадии, рынок стейблкоинов на базе STRC в настоящее время не имеет много по-настоящему значимых игроков. Судя по объему средств, вниманию рынка и скорости расширения экосистемы, проекты, оказавшие реальное влияние, в основном ограничиваются Apyx и Saturn. В некотором смысле, вся ниша «стейблкоинов цифрового кредита» постепенно приобретает структуру конкуренции двух лидеров.

Хотя Saturn запустился раньше, сейчас Apyx уже обогнал его по данным. В целом, конкурентные преимущества Apyx проявляются в следующих основных аспектах.

Во-первых, абсолютное преимущество по масштабу TVL и владению базовыми активами. Apyx уже в своем позиционировании проекта установил четкий стратегический план — стать крупнейшим институциональным держателем STRC в мире. По состоянию на конец апреля портфель уже достиг 125 миллионов долларов (у Saturn — всего 50 миллионов долларов). Как только Apyx достигнет своих стратегических целей, он будет монополизировать право на распределение доходов в блокчейне на основе цифрового кредита MicroStrategy. Кроме того, для стейблкоина преимущество Apyx в объеме TVL также означает более глубокие торговые пулы, меньшее проскальзывание при крупных обменах и более стабильную эффективность ликвидности, способную безопасно выдерживать вход и выход крупных средств.

Во-вторых, более высокая доходность и отсутствие риска приостановки начисления дохода. Для целевой аудитории Apyx и Saturn ключевым требованием является стабильный и предсказуемый доход. По сравнению с sUSDat от Saturn, apyUSD от Apyx в статическом режиме хранения долгое время сохраняет преимущество в годовой доходности примерно в 2%. Кроме того, очень важно, что дизайн sUSDat тесно связан с обменным курсом STRC. Когда цена STRC падает ниже «водяного знака» (Watermark) из-за даты отсечки дивидендов (ex-dividend) или по другим причинам, накопление дохода для YT-sUSDat полностью приостанавливается, в то время как у Apyx такой проблемы нет вообще.

В-третьих, более четкие ожидания TGE и отсутствие давления от продаж со стороны венчурных капиталистов. Пользователи криптоиндустрии больше всего не любят «неопределенные очки PUA». По сравнению с Saturn, Apyx четко раскрыл дату TGE, сроки и объемы вознаграждений в виде токенов для каждого Season очковых активностей, что с психологической точки зрения способствует удержанию пользователей. Кроме того, разработка Apyx не привлекала венчурный капитал, лишь очень небольшая часть — это ранние инвестиции, и часть из них — от самого основателя. Это означает отсутствие институциональных инвесторов раундов private sale, которые бы фиксировали прибыль, продавая токены до прихода рядовых инвесторов, что делает доход от токенов, соответствующих очкам, более идеальным.

Потенциальные риски и прогнозы на будущее

Важно четко подчеркнуть, что высокая доходность Apyx не означает «отсутствие риска». По своей сути Apyx по-прежнему является доходным продуктом, построенным на кредитной структуре Биткойна, а не традиционным безрисковым долларовым активом. Поэтому, обсуждая его потенциал роста, необходимо также признать источники риска, стоящие за ним.

Во-первых, это кредитный риск самого базового актива. Базовая логика STRC построена на MicroStrategy и его балансе биткойнов. Другими словами, готовность рынка принимать доходность STRC по сути основана на вере в то, что MicroStrategy сможет и дальше использовать активы в биткойнах для поддержания своей кредитной структуры и постоянно завершать финансирование, расширение баланса и выплату процентов.

И если на рынке биткойнов произойдут экстремальные колебания, например, резкое обвальное падение за короткое время, или если рыночные предпочтения к риску модели кредитного плеча MicroStrategy значительно снизятся, то рыночная оценка, ликвидность и структура доходов STRC могут пострадать. Хотя такой «системный риск» не означает немедленного краха протокола, он действительно означает, что источник дохода Apyx в определенной степени привязан к самому циклу биткойна.

Во-вторых, это типичный риск композиции DeFi. Поскольку Apyx глубоко интегрирован с протоколами Morpho, Curve и Pendle, его экосистема фактически построена на высоко сложной композируемости в блокчейне. Преимущество такой структуры — возможность значительно повысить эффективность использования средств; но расплатой является то, что риски всей системы становятся более связанными.

Например, если в каком-либо базовом протоколе обнаружатся уязвимости смарт-контракта, кризис ликвидности или аномалии механизма ликвидации, это может передать риски всей экосистеме через структуры LP, залога и разделения дохода. Особенно когда рекурсивное кредитование и игры с высоким кредитным плечом становятся все более распространенными, рыночные колебания часто усиливаются.

Поэтому Apyx лучше понимать как актив «средне-высокого риска, высокой доходности» в блокчейне, а не как замену традиционным стейблкоинам с избыточным залогом. Но именно это разделение рисков придает Apyx уникальную привлекательность в текущих рыночных условиях.

Нынешний рынок стейблкоинов сталкивается со все более очевидной проблемой — доходность быстро становится однородной. По мере снижения доходности казначейских облигаций США и сокращения традиционного арбитражного пространства, реальный доход, который могут предложить большинство протоколов стейблкоинов, становится все более ограниченным, рынку нужны новые источники дохода, и пользователи готовы брать на себя определенную степень риска ради более высокой доходности.

За последние несколько лет, от LSD и рестейкинга до торговли доходностью на Pendle, весь рынок DeFi фактически проверял одно и то же — пользователи никогда не избегают риска, чего они действительно избегают, так это активов без «соотношения риск/доходность». А появление STRC как раз дает рынку новый вариант соотношения «риск vs доходность».

И в течение последних нескольких месяцев постоянный рост TVL Apyx и всей ниши STRC показывает, что рынок голосует за этот нарратив реальными деньгами.