Автор: Oluwapelumi Adejumo

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: Объем торгов не рухнул, но количество активных адресов продолжает сокращаться в течение шести месяцев, достигнув пятилетнего минимума. Это расхождение между "внешним процветанием и внутренней пустотой" является противоположным сигналом структурного здоровья бычьего рынка.

В статье используются три набора данных от Glassnode, Santiment и CryptoQuant для перекрестной проверки, предлагаются три сценария будущего, подходящие в качестве справочной рамки для оценки текущей динамики BTC.

Полный текст ниже:

Активность сети Bitcoin неуклонно снижалась в течение последних шести месяцев, но эта тенденция не отражается в ключевых показателях, на которые трейдеры смотрят в первую очередь.

Более четкий сигнал — не объем торгов (который в основном стабилен), а широта участия. Даже если сеть продолжает обрабатывать схожее количество транзакций, количество активных адресов в сети продолжает снижаться.

На рынке, где обнаружение цен все чаще происходит через ETF и деривативы, это разделение имеет решающее значение. Оно означает: ончейн-присутствие Bitcoin сужается, в то время как рыночная экспозиция продолжает активно проявляться в других местах.

По мере продолжения медвежьего рынка эту тенденцию становится все труднее игнорировать.

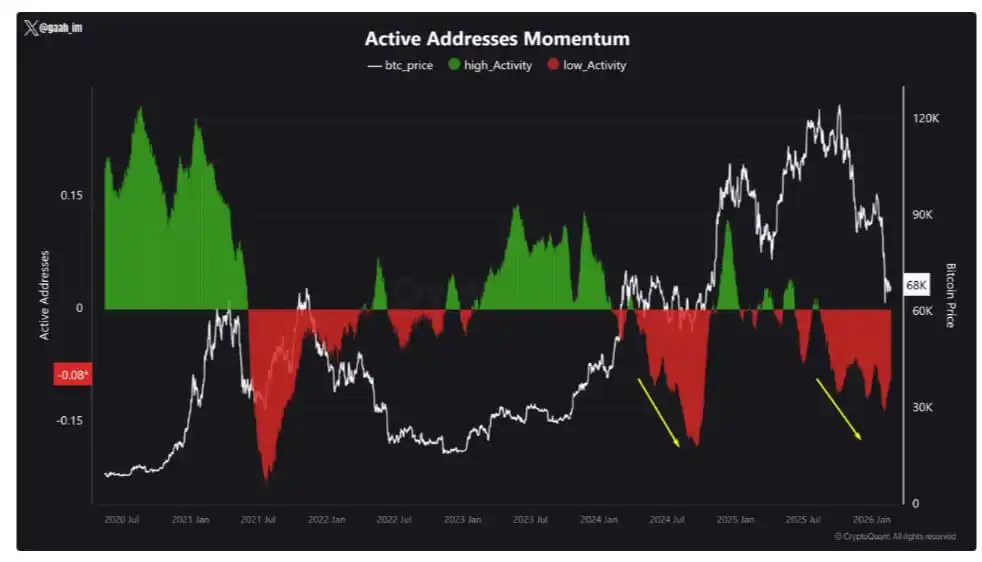

Данные Glassnode показывают, что в середине августа 2025 года 8-дневное скользящее среднее количество активных адресов Bitcoin составляло около 778 680. По состоянию на 23 февраля это число снизилось до примерно 535 942, что составляет падение на 31%.

CryptoQuant также в течение шести месяцев подряд отмечает низкую сетевую активность, описывая текущую фазу как период устойчивой слабости ончейн-участия.

Динамика активных адресов Bitcoin

Источник: CryptoQuant

В последний раз рынок демонстрировал подобную картину в 2024 году — после этого Bitcoin пережил коррекцию примерно на 30%.

Это не означает, что сейчас это обязательно повторится, но это усиливает историческую закономерность: длительная сетевая слабость часто совпадает с фазами ослабления рыночной уверенности.

Широта падает, но пропускная способность не рухнула

Количество транзакций Bitcoin не снизилось синхронно с количеством активных адресов.

В середине августа 2025 года среднесуточное количество транзакций составляло около 444 тысяч. Данные Blockchain.com показывают, что за последние 30 дней в среднем составляло около 439 тысяч.

Внутридневные данные все еще колеблются — от примерно 289 тысяч до 702 тысяч, — но общий тренд пропускной способности не обрушился.

Это расхождение является ключом к пониманию текущей ситуации.

Если объем транзакций остается стабильным, а активных адресов становится меньше, это означает, что меньшее количество субъектов осуществляет одинаковый объем ончейн-активности.

У этого есть несколько причин, и ни одна из них не требует притока розничных инвесторов. Биржи и кастодиальные услуги могут обрабатывать выводы партиями; крупные держатели могут консолидировать переводы; институциональные потоки могут обрабатываться через меньшее количество кошельков; операционная активность также может вызывать кратковременные всплески количества транзакций, не означая реального возврата пользователей.

Результат: сеть по-прежнему выглядит оживленной, но базовое количество участников сокращается.

Вот почему падение широты участия говорит о большем, чем просто сырая пропускная способность. Стабильное количество транзакций может маскировать рынок, где активность все больше концентрируется среди повторяющихся трейдеров, крупных институтов и операционных денежных потоков.

В такой конфигурации блокчейн Bitcoin по-прежнему функционирует нормально, но широта пользовательского участия, которую он представляет, становится менее реальной.

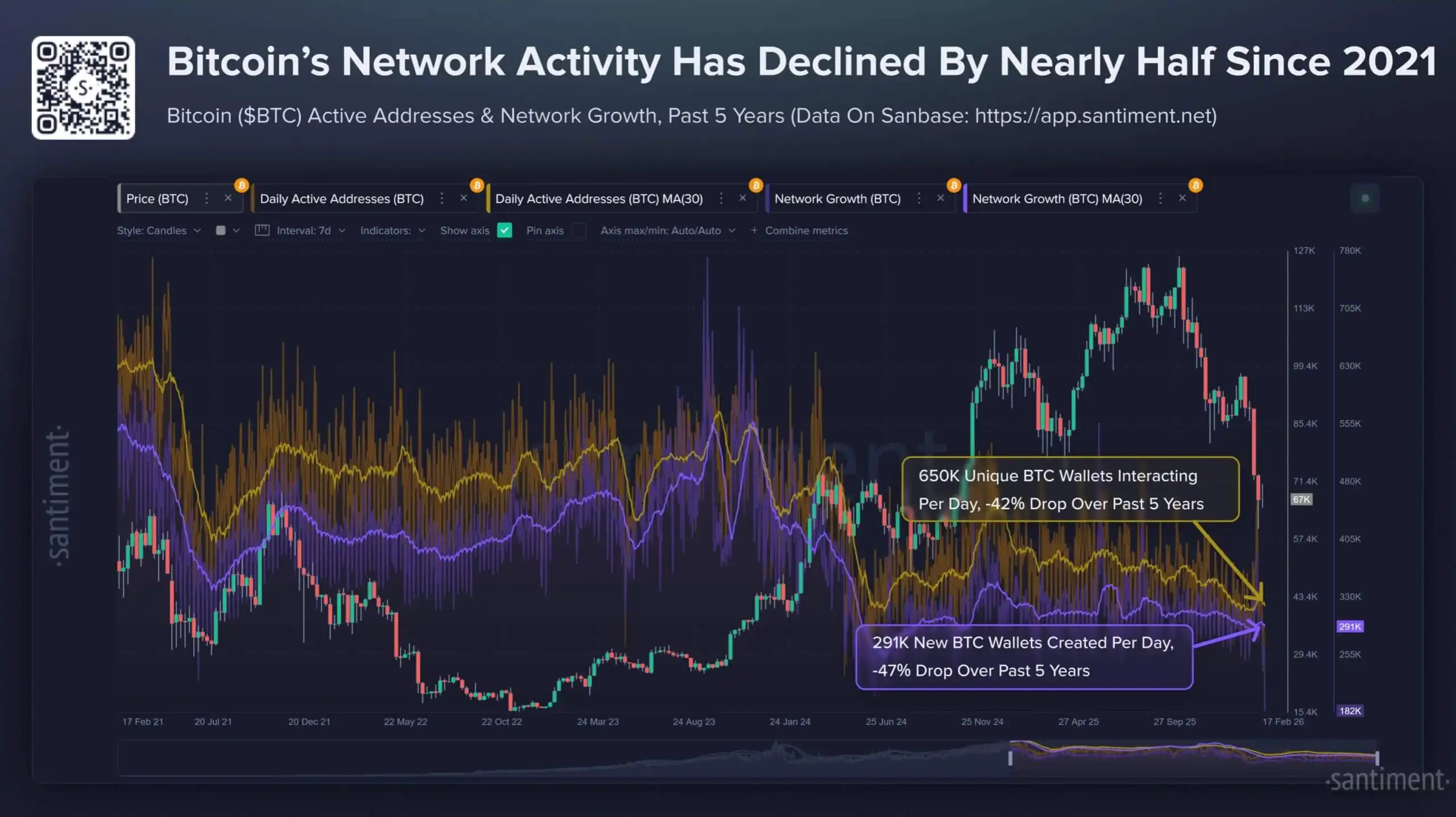

Аналитическая фирма Santiment дает более прямолинейное описание с более долгосрочной перспективы.

Организация сообщает, что с февраля 2021 года количество уникальных адресов, инициирующих транзакции Bitcoin, сократилось на 42%, а количество новых создаваемых адресов уменьшилось на 47%.

Santiment не характеризует это как доказательство смерти криптовалют или закрепления многолетнего медвежьего рынка, но это действительно описывает медвежье расхождение, сохранявшееся в течение 2025 года — рыночная капитализация росла, в то время как показатели полезности Bitcoin ослабевали.

Это напряжение теперь воплощается в шестимесячном тренде. Цена и рыночная нарратива могут продолжать поддерживаться, но сама цепь становится все тише.

Низкие комиссии указывают на сокращение спроса на блок-пространство

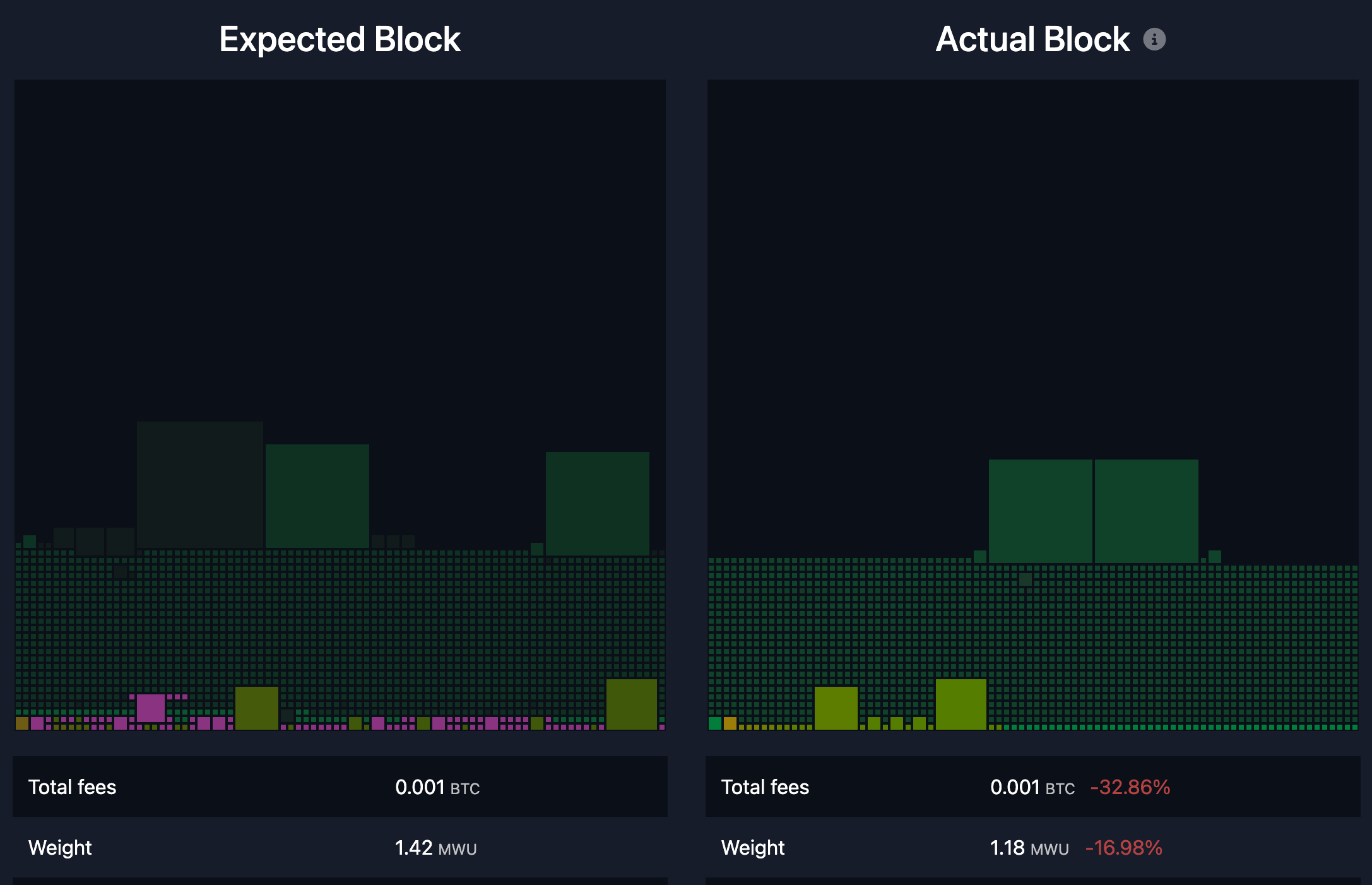

Данные о комиссиях дополнительно подтверждают, что Bitcoin Layer 1 находится в состоянии слабого спроса.

Данные mempool.space показывают, что недавняя средняя комиссия за транзакцию в сети составляет около $0,24, что эквивалентно примерно 1.8 sats/vB.

Для сети, которая в пиковые периоды прошлых циклов испытывала постоянную конкуренцию за блок-пространство, это низкий уровень. При текущем темпе транзакций этот уровень комиссий означает, что ежедневный доход от комиссий сети составляет менее $100 000.

Для сравнения, субсидия за блок все еще составляет около 450 BTC в день, при этом доля дохода от комиссий крайне мала.

Средние комиссии за блок Bitcoin

Источник: Mempool.space

Это не является непосредственной проблемой безопасности и не означает, что модель безопасности Bitcoin сталкивается с сиюминутным давлением.

Это связано с тем, что субсидия за блок по-прежнему доминирует в доходах майнеров. Но это действительно указывает на долгосрочную реальность, с которой Bitcoin на данном этапе цикла еще не был вынужден столкнуться.

Тема перехода к модели бюджета безопасности, основанной на комиссиях, возвращается каждый цикл, но в текущих условиях этот переход не испытывается — потому что сам спрос на комиссии слаб.

Практически, спокойный рынок комиссий позволяет отложить это обсуждение.

Сеть не сталкивается с постоянным давлением перегруженности, и пользователи не ведут острой конкуренции за место в блоке. Это может быстро измениться во время волатильных событий, спекулятивных волн или новых всплесков спроса, но пока этого не произошло.

В настоящее время использование блок-пространства явно низкое по сравнению с прошлыми бычьими фазами, что согласуется с общим фоном снижения широты участия.

Пустой мемпул Bitcoin

Источник: Mononaut

Вывод CryptoQuant также согласуется с этой средой комиссий — низкая сетевая активность обычно связана со снижением интереса рынка к активу и периодами повсеместных убытков.

Когда интерес ослабевает, новых участников становится меньше, самостоятельно инициируемых переводов меньше, давление на комиссии ослабевает.

Bitcoin как финансовый актив может продолжать активно торговаться, но сама цепь больше не отражает широкого пользовательского участия.

Макросреда и потоки ETF меняют способ торговли Bitcoin

Макроконтекст помогает объяснить, почему эта тенденция сохраняется.

Bitcoin все больше становится похожим на макрочувствительный актив с высокой бетой, особенно выделяясь в периоды избегания риска.

За последний год инфляция в США несколько снизилась, в январе 2026 года рост ИПЦ в годовом исчислении составил 2,4%; целевой диапазон процентных ставок ФРС на конец января указывался как 3,50%–3,75%.

В более простой рыночной среде охлаждение инфляции могло бы поддержать более четкий отскок рисковых активов.

Однако внимание рынка сосредоточено на нескольких катализаторах волатильности — включая неопределенность тарифной политики. Этот фактор спровоцировал резкие колебания процентных ставок и доллара, сохраняя общие аппетиты к риску нестабильными.

В такой среде и розничные, и институциональные инвесторы часто сокращают частоту операций. Участие розницы снижается, трейдеры реже совершают сделки. Институты могут сохранять экспозицию, но предпочитают корректировать позиции через продукты, не требующие ончейн-перемещения монет.

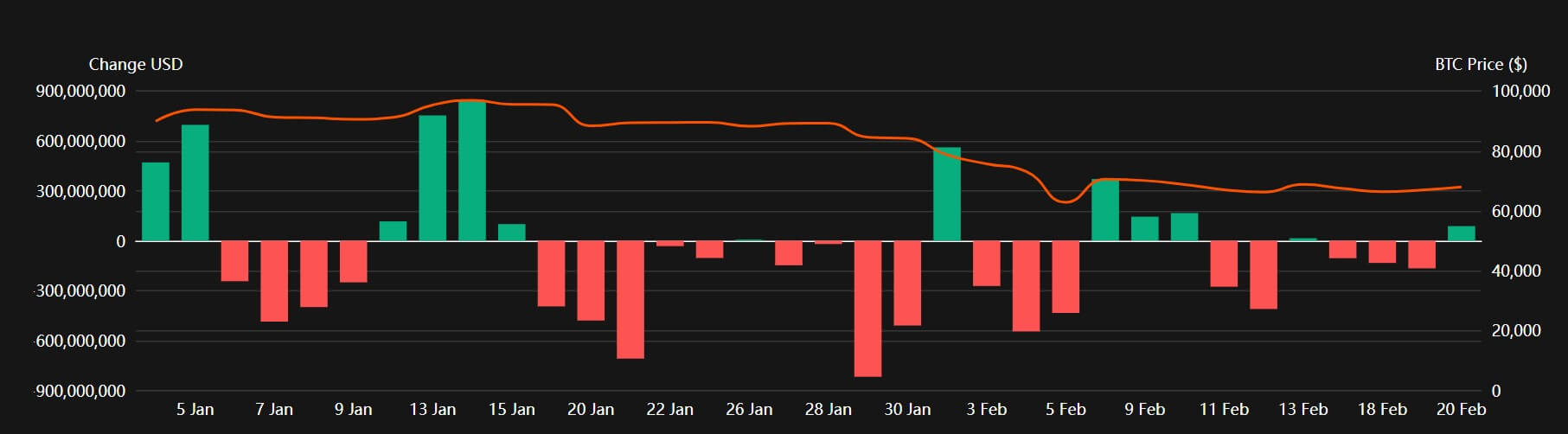

Именно поэтому спотовые Bitcoin ETF стали главными героями нарратива.

Данные Coinperps показывают, что американские Bitcoin ETF в течение нескольких недель подряд демонстрируют чистый отток, за последние пять недель累计ный отток составил около $3,8 млрд, с начала года — около $4,5 млрд.

Ежедневные потоки средств американских Bitcoin ETF в 2026 году

Источник: Coinperps

Это перемещает активность с кошельков самохранения на брокерские счета.

Это также объясняет, почему рынок может оставаться активным, в то время как сеть становится все тише. Экспозиция продолжает переходить из рук в руки, но большая часть этого оборота происходит вне цепи.

Это важное изменение роли Bitcoin. Он все больше становится похожим на финансовый продукт в институциональной оболочке, в то время как Layer 1 все более избирательно используется для расчетов, хранения и периодических переводов.

Между тем, повседневная торговая энергия в криптопространстве все больше концентрируется и направляется в другие места, особенно в стейблкоины.

Coin Metrics называет стейблкоины ключевым драйвером ончейн-активности, в настоящее время общий объем предложения стейблкоинов приближается к $3 трлн, а объем торгов продолжает расти.

Если стейблкоин-транзакции на других блокчейнах берут на себя больше повседневных расчетных потребностей, Bitcoin Layer 1 по своей функциональности естественным образом становится более специализированным.

Само по себе это не ослабляет инвестиционную логику Bitcoin, но确实 меняет его форму.

Три сценария на следующие три-шесть месяцев

Текущее шестимесячное снижение сетевой широты выстраивает три возможных пути для будущей динамики Bitcoin.

Первый — продолжение апатии, что выглядит как базовый сценарий в условиях избегания риска.

В этом сценарии активные адреса остаются на низком уровне (диапазон 450–600 тысяч), количество транзакций колеблется, но не обрушивается, комиссии остаются низкими, потоки ETF продолжают быть ровными или слегка отрицательными.

Здесь Bitcoin все еще может сильно колебаться из-за макрозаголовков, но ончейн-участие не подтверждает широкого восстановления. Логика торговли активом больше похожа на макроинструмент, а не на сеть, вступающую в новую фазу экспансии.

Второй — разморозка ликвидности, более оптимистичный путь.

Если инфляция продолжит снижаться, а ожидания смягчения политики стабилизируют аппетиты к риску, потоки ETF могут превратиться из чистого оттока в устойчивый чистый приток. В такой среде рост активных адресов станет ключевым сигналом подтверждения.

Восстановление до 650–800 тысяч активных адресов будет означать, что широта участия восстанавливается, а не просто возвращается ценовой импульс. Это будет больше похоже на классическое циклическое восстановление — рост цены, поддерживаемый ростом пользовательской вовлеченности в сети.

Третий — сценарий структурного замещения, возможно, самый值得关注.

В этом сценарии цена Bitcoin растет, но ончейн-широта продолжает оставаться вялой. ETF, деривативы и кастодиальные расчеты продолжают доминировать, а стейблкоины на других участках криптопространства берут на себя больше торговых потребностей.

Здесь Bitcoin все больше становится похожим на цифровой макроактив и расчетный слой, а не на блокчейн с широкой повседневной активностью розничных пользователей.

Этот сценарий ознаменует эволюцию роли Bitcoin, отражая глубокие изменения, которые произошли с ним по сравнению с тем, что было много лет назад.