Original Author: Protos

Original Translation: Chopper, Foresight News

Eleven months ago, French semiconductor company Sequans Communications launched a corporate bitcoin reserve plan to combat the risk of delisting from the New York Stock Exchange. Today, this trial has come to a quiet end.

The chipmaker confirmed that it has fully repaid its convertible bonds by selling its bitcoin holdings and also plans to gradually liquidate its remaining 658 bitcoins. The company's bitcoin holdings once peaked at 3,234 coins.

Sequans had previously declared its intention to accumulate and hold over 3,000 bitcoins as a long-term reserve asset. Yet this so-called "long-term" ultimately lasted less than a year.

The company's stock (ticker SQNS) has fallen 77% year-to-date, with a staggering 97% cumulative decline over the past five years.

Sequans' bitcoin reserve plan was launched on June 23, 2025, a time when Swan Bitcoin and its CEO Cory Klippsten were actively promoting the project (Note: Swan Bitcoin was the exclusive operator and advisor for Sequans' bitcoin reserve strategy). This launch came just 18 days after the NYSE issued a delisting warning to Sequans, stating the company's market capitalization and shareholder equity had both fallen below the exchange's $50 million minimum threshold.

Sequans' latest announcement confirms full repayment of its convertible bonds.

Klippsten stated at the time, "Sequans has the potential to become a leader in the corporate bitcoin treasury space." Back then, SQNS stock was trading at $23.40; today it opened at just $3.98.

Bitcoin Reserve Strategy Fails Shortly After Launch

Following the market bubble burst in early summer 2025, the stock prices of many public companies with digital asset treasury strategies collectively weakened, dashing the bright prospects Sequans had painted.

Sequans CEO Georges Karam had earlier expressed strong confidence, firmly believing bitcoin was a superior asset with extremely high long-term investment value.

The company had selected Swan Bitcoin as its execution partner and Coinbase Prime as the custodian. Simultaneously, Northland Capital Markets and B. Riley Securities acted as joint lead underwriters, assisting the company in completing a $384 million private placement.

Of this capital, only $195 million came from the sale of American Depositary Receipts at $1.40 per share; the remaining $189 million was in the form of secured convertible bonds using bitcoin as collateral. This means that from day one, the bitcoin Sequans held in reserve was essentially pledged to creditors.

As of October 3, 2025, Sequans held a total of 3,234 bitcoins, with an average acquisition cost of approximately $116,643 per coin. As of this writing, the bitcoin price has fallen to $73,000.

Just one month later, the company gained notoriety for a piece of negative news: to repay a portion of its debt, it sold 970 bitcoins.

This action completely violated the core principle of the corporate bitcoin accumulation model. Michael Saylor, a pioneer of this approach, famously stated, "Even if you are desperate, do not sell your bitcoin." But Sequans ultimately chose to sell its coins to pay debt.

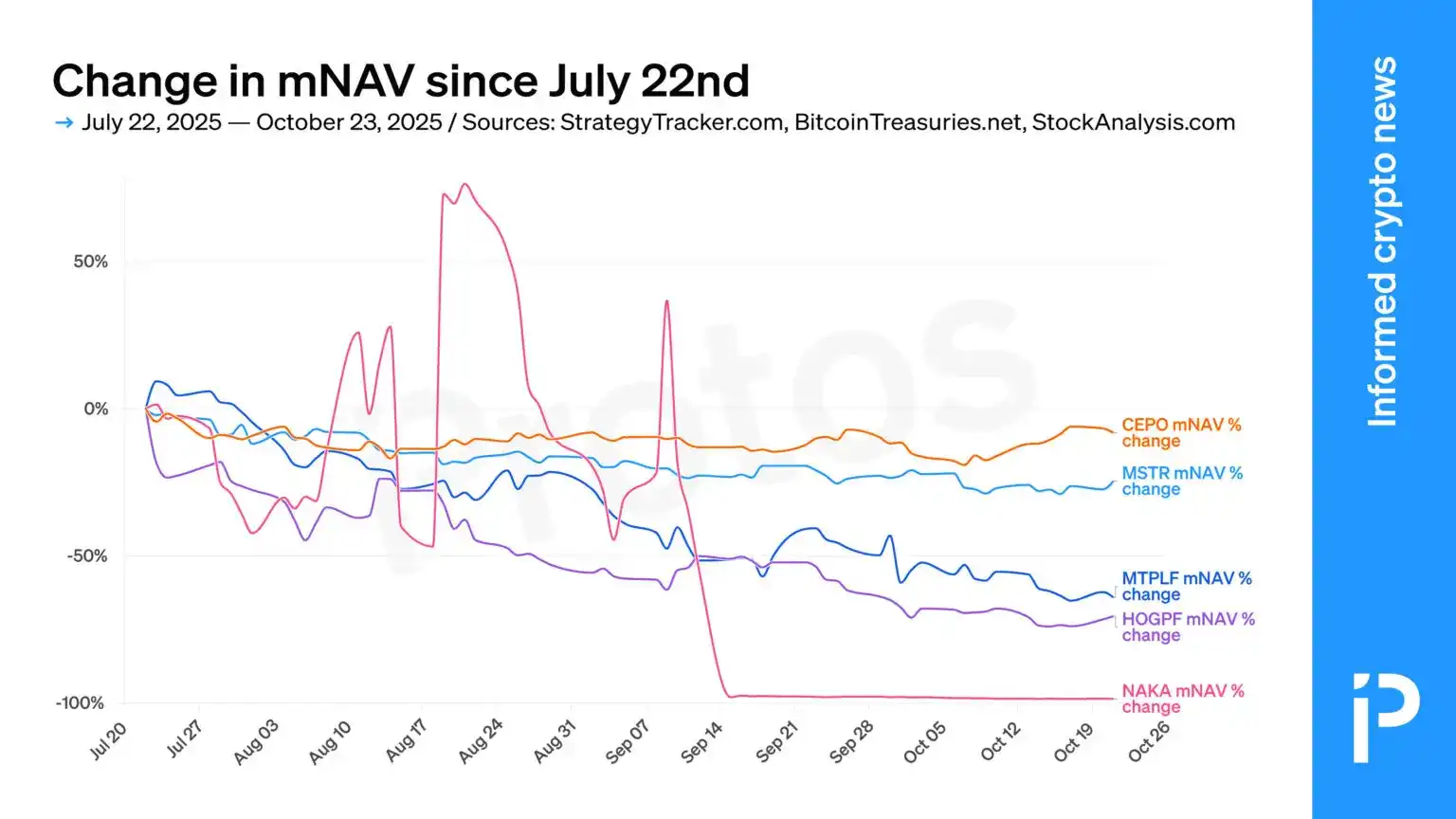

Percentage change in modified Net Asset Value per Share (mNAV) for several corporate bitcoin treasury companies since July 22, 2025.

"Bitcoin Reserve Strategy Officially Terminated"

Five more months passed, and Sequans completely halted the program. The company's announcement tersely stated: "The Bitcoin reserve strategy has been terminated."

Karam, the CEO who was once so bullish on bitcoin, now stated that this debt repayment is a significant turning point for the company, and Sequans will now fully focus on its core IoT semiconductor business to drive expansion.

All previous praise for bitcoin's value and promises to create long-term shareholder returns through crypto asset reserves have been abandoned. The current plan for the company is solely liquidation.

In fact, the exit signal was given three weeks earlier in the company's Q1 2026 earnings report. In the risk factors section, the company explicitly mentioned terminating its bitcoin reserve-related business. For that quarter, Sequans reported revenue of only $6.1 million and an operating loss of $50.5 million.

According to annual report data, Sequans posted a net loss of $109.3 million for the full year 2025. Within this, unrealized impairment losses on bitcoin assets alone amounted to $67.4 million, bringing the company's cumulative loss total to a staggering $145.1 million.

In summary, Sequans bought bitcoin high and sold low, ultimately generating tens of millions in losses.

The company had hoped to use its bitcoin reserves to strengthen its financial resilience and create long-term value for shareholders, but both goals have failed. Currently, SQNS stock is down over 80% from the day the bitcoin plan was launched and down 92% from its high over the past year.