Автор: Fidelity Digital Assets

Компиляция: Цзяхуань, ChainCatcher

Середина года — хороший момент для проверки, позволяющий инвесторам оценить, как изменилась рыночная динамика и остаются ли в силе суждения, сделанные в начале года.

В «Перспективах на 2026 год» команда исследователей Fidelity Digital Assets полагала, что ключевым моментом этого года является не немедленный рост цен, а более тонкая динамика — структурная «перестройка» всей экосистемы цифровых активов. Несмотря на временами вялые, а временами колебания цен в этом году, при более глубоком рассмотрении можно увидеть, что несколько фундаментальных тенденций продолжают развиваться.

В этой статье рассматривается прогресс ключевых тем из «Перспектив на 2026 год» на сегодняшний день, указывается, какие из наших суждений подтвердились, а какие разошлись, и что эти изменения могут означать для будущего.

1: Ускоренная интеграция цифровых активов и традиционных рынков капитала

Мы ожидали, что в 2026 году интеграция цифровых активов с традиционными рынками капитала продолжится. До сих пор эта тенденция действительно развивается, причем в некоторых областях даже быстрее, чем ожидалось.

Несмотря на волатильность общего рынка, спрос на доступ к цифровым активам через основные финансовые каналы остается устойчивым, а традиционные платформы продолжают расширять свой ассортимент продуктов.

Примечательно, что открытый интерес по опционам на спотовые ETP на биткоин (такие продукты впервые появились только в ноябре 2024 года) теперь может сравниться с опционами, рассчитываемыми непосредственно в биткоинах, что отражает продолжающийся рост принятия институциональными и мейнстримными инвесторами.

Токенизация также набирает обороты, и активность, по-видимому, превосходит ожидания. Традиционные финансовые учреждения все чаще выпускают блокчейн-ориентированные инвестиционные продукты, а крупные биржи сотрудничают с платформами цифровых активов или приобретают их доли, чтобы расширить каналы дистрибуции и подключиться к ончейн-инфраструктуре.

В то же время нормативно-правовая база становится более ясной. Комиссия по ценным бумагам и биржам (SEC) и Комиссия по торговле товарными фьючерсами (CFTC) совместно опубликовали руководство, устанавливающее классификацию цифровых активов, а прогресс в законодательстве, таком как «Закон CLARITY», означает, что участники рынка получат более четкие рамки.

В совокупности эти достижения свидетельствуют о том, что цифровые активы продолжают интегрироваться в более широкую финансовую систему, чему способствуют рыночный спрос и расширение инфраструктуры.

2: Права держателей токенов постепенно привлекают внимание, но остаются неопределенными

Мы ожидали, что в 2026 году интересы держателей токенов станут более тесно связанными, и больше ончейн-компаний будут уделять приоритетное внимание механизмам выкупа токенов, более четким правам собственности и т. д.

Пока что это направление, похоже, не изменилось, и эксперименты во всей экосистеме продолжаются: от динамики выкупа на основе резервов (например, альянс Hyperliquid/USDC) до обновлений в управлении и структуре, таких как реструктуризация Aave DAO/Labs.

Однако, хотя применение этих механизмов расширяется, явная «премия за права держателей токенов» еще не полностью отразилась в рыночных ценах. Эта тенденция развивается, но все еще находится на ранней стадии, и инвесторы все еще оценивают, какие модели действительно могут привести к устойчивому накоплению стоимости.

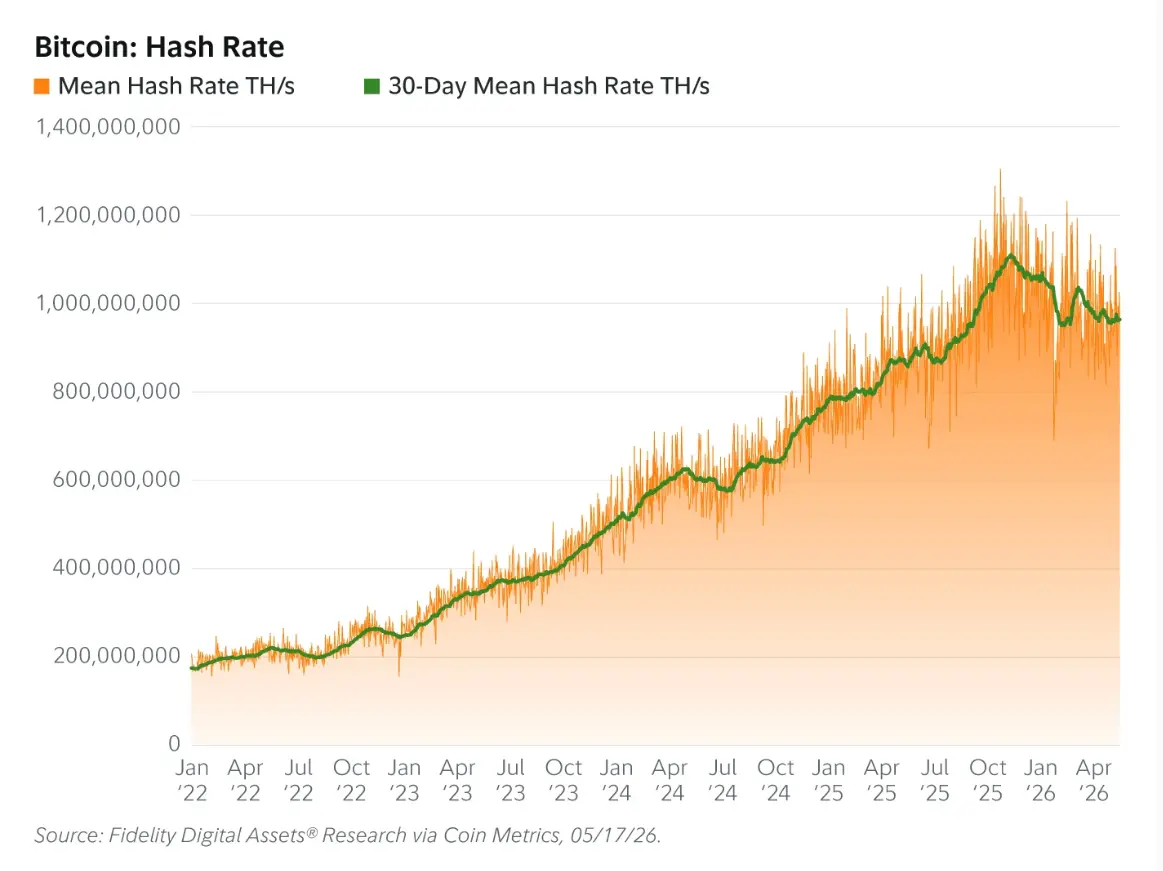

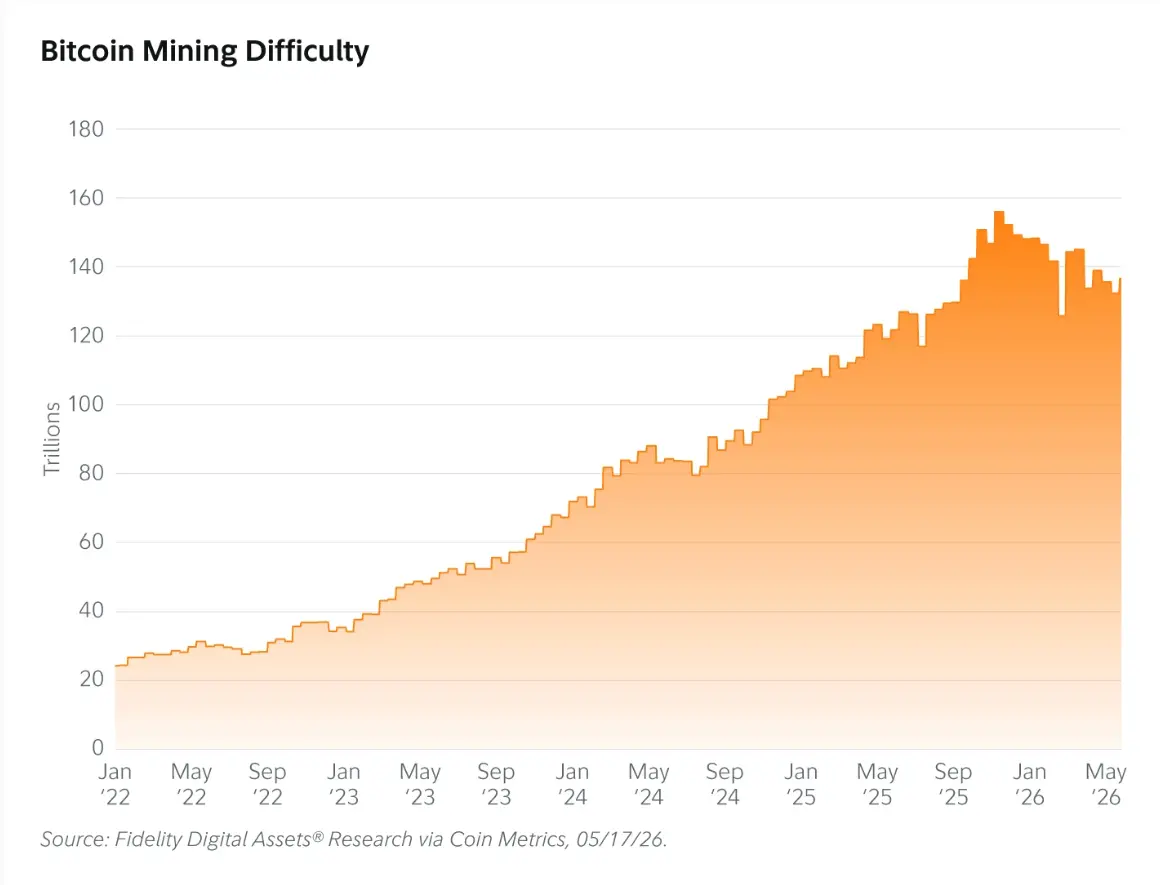

3: Потенциальный сдвиг: искусственный интеллект и майнинг

Мы предположили, что усиление конкуренции со стороны спроса на вычислительные мощности для ИИ может привести к стабилизации роста хешрейта биткоина, поскольку майнеры перенаправят энергию и инфраструктуру на потенциально более прибыльные направления. В этом году такая динамика, возможно, начинает проявляться: средний 30-дневный хешрейт и сложность майнинга снизились примерно на 8,8% и 7,8% соответственно.

Если смотреть на более длинную траекторию, темпы роста хешрейта по сравнению с предыдущими годами замедлились, что может быть ранним сигналом структурных изменений. Бизнес дата-центров для ИИ становится все более прибыльным, особенно для крупных операторов, которые могут получить доступ к энергетической инфраструктуре, и это, по-видимому, все чаще может быть движущей силой.

Несмотря на раннюю стадию, наблюдаемое замедление роста согласуется с первоначальной гипотезой и может отражать постепенный переход майнеров к другим источникам дохода.

4: Биткоин на новой точке перелома

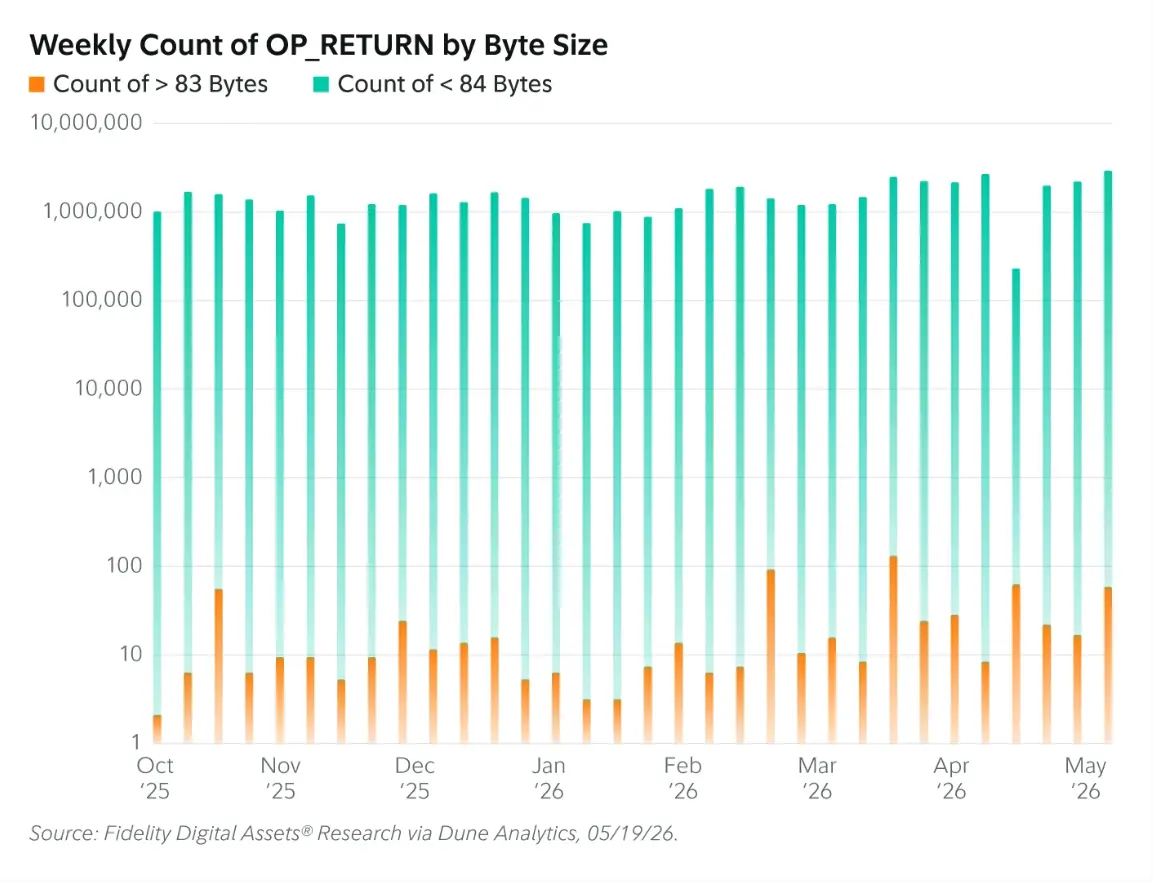

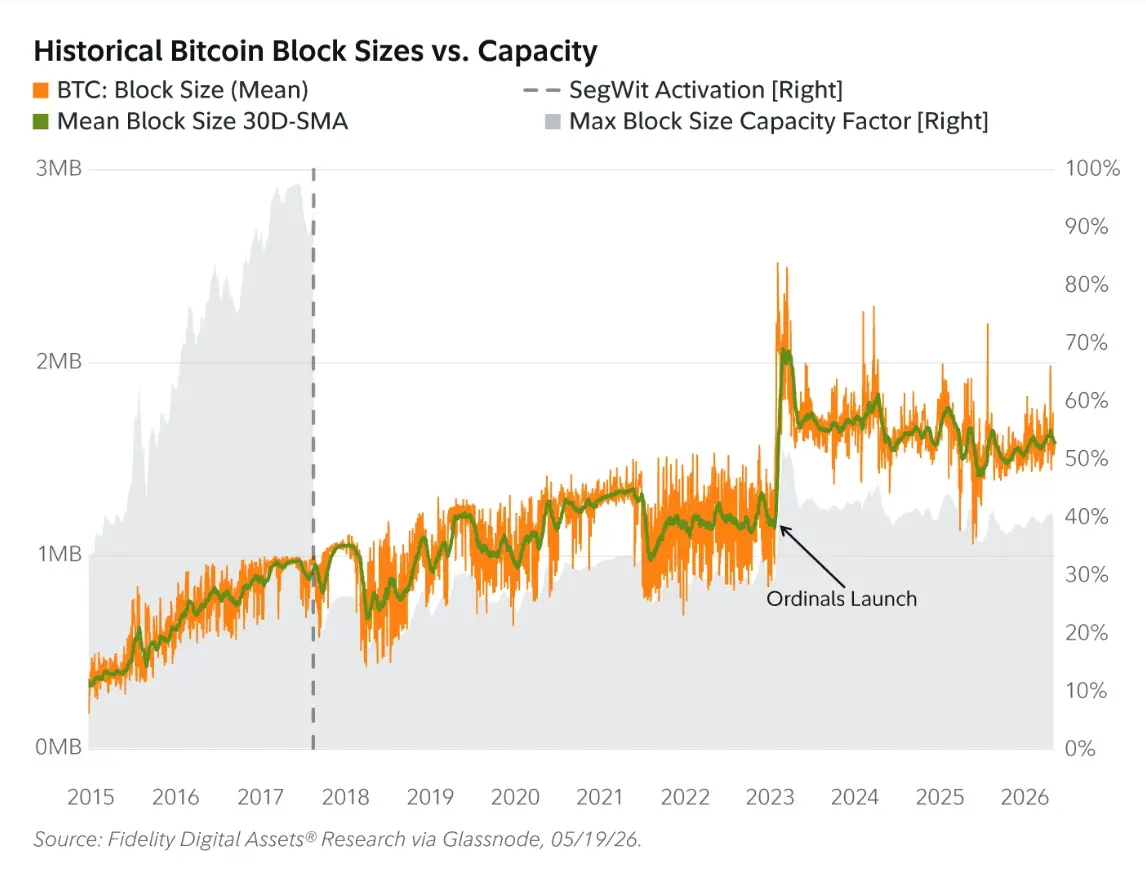

Мы ожидали, что увеличение объема данных, которые можно записать с помощью операционного кода OP_RETURN, не приведет к значительному раздуванию блокчейна (OP_RETURN используется для записи данных в блокчейн, и, поскольку требует оплаты комиссии, смягчение ограничений на объем данных не привело к злоупотреблениям или перегрузке сети). На сегодняшний день данные, похоже, подтверждают этот вывод.

Использование OP_RETURN с большим размером данных (≥84 байт) в основном не изменилось, а общий рост блокчейна по-прежнему остается в прогнозируемом диапазоне (около 1,35–2,5 МБ). Другие показатели использования блоков показывают, что емкость по-прежнему ниже 50%, что свидетельствует о том, что увеличение гибкости данных не оказало существенного давления на сеть.

В то же время внимание переключилось на более макроскопическую динамику сети. Узлы Bitcoin Knots демонстрировали значительные колебания, быстро росли и так же быстро снижались, что вызвало предположения о потенциальной сибил-подобной активности.

Согласно текущим данным, узлы Bitcoin Core по-прежнему составляют около 77% сети, а узлы Knots — около 17%. Несмотря на меньшинство, это создает риск неожиданного раскола — вероятность невысока, но не равна нулю: при определенных условиях узлы Knots могут отделиться в цепочку, которая остановится или будет менее безопасной; по текущим оценкам, такая ситуация может возникнуть примерно через 80 дней.

Тем не менее, доминирующая доля Core по-прежнему служит якорем для сетевого консенсуса. В то же время набирает обороты работа над долгосрочными обновлениями безопасности. BIP-360 был упрощен и ввел квантово-устойчивые типы выходов (Pay-to-Merkle-Root, P2MR); продолжающиеся исследования OP_CHECKSHRINCS отражают изучение схем постквантовой подписи на основе хэшей.

Хотя конкретные сроки появления квантовой угрозы не определены, эти достижения показывают, что отрасль все больше внимания уделяет подготовке к будущей безопасности сети.

5: Медведи временно контролируют ситуацию

В январе этого года мы описали два сценария, в которых быки и медведи были бы уравновешены к началу 2026 года, ожидая, что макроусловия приведут к нелинейному движению, несмотря на улучшение структурных основ.

В этом году сценарий медвежьего рынка в значительной степени преобладал: биткоин упал на 13% на фоне делевериджа, вызванного ликвидациями, устойчиво высокой инфляции и геополитической неопределенностью, которая заставила рынок ожидать дальнейшего повышения процентных ставок. Однако недавние рыночные действия демонстрируют более тонкую динамику.

После первоначальной волны распродаж, вызванной недавним геополитическим конфликтом, биткоин отскочил и в тот же период опередил традиционные активы, что, возможно, отражает спрос на высоколиквидные, нейтральные активы в периоды стресса.

В то же время структурные преимущества сохраняются, включая продолжающееся формирование институционального капитала, постепенное повышение нормативной ясности и расширение глобальной ликвидности.

Несмотря на то, что краткосрочная среда остается сдерживающей, наша более макроскопическая оценка, похоже, по-прежнему верна, хотя и продвигается неравномерно.

6: Золото сохраняет силу, что будет дальше?

Мы отмечали, что еще один сильный год для золота не станет неожиданностью, учитывая поддержку со стороны спроса центральных банков и глобальной тенденции к постепенному отходу от долларовой системы.

В этом году золото сначала выросло почти на 30% на фоне геополитической напряженности, а затем откатилось к более умеренному росту примерно на 3–4%. Несмотря на коррекцию, золото все еще может показать лучшую динамику к концу года.

Также появляется все больше свидетельств в поддержку отхода от долларовой системы, включая некоторые новые альтернативные способы расчетов, такие как принятие Ираном биткоина для оплаты транзитных сборов и платежи, связанные с деятельностью в Ормузском проливе.

В то же время спрос центральных банков на золото остается сильным. Последние данные показывают, что накопление продолжается, примечательно, что золото уже превзошло доллар США и казначейские облигации США, став основным компонентом глобальных резервов.

Движение золота и сохраняющийся спрос со стороны центральных банков в основном соответствуют нашим первоначальным ожиданиям; однако ожидаемого нами последующего опережающего роста биткоина пока не произошло.

Заключение: Накапливая силы под поверхностью

На середину года ландшафт цифровых активов 2026 года демонстрирует баланс между краткосрочным давлением и долгосрочным прогрессом. Несколько тем из «Перспектив» развиваются в соответствии с ожиданиями, особенно в области институционального участия, регулирования и инфраструктуры; другие же все еще находятся на ранней стадии или еще не полностью реализованы.

Для инвесторов это означает необходимость смотреть сквозь краткосрочные колебания цен на то, как формируются структурные изменения. Многие основы, поддерживающие следующий этап роста, по-видимому, укрепляются, даже если это еще не полностью проявилось.