Автор: Fidelity Digital Assets

Перевод: Джяхуань, ChainCatcher

Середина года — хороший момент для оценки: инвесторы могут проверить, как изменилась динамика рынка и остаются ли в силе суждения, сделанные в начале года.

В «Прогнозе на 2026 год» исследовательская команда Fidelity Digital Assets предположила, что ключевым моментом этого года будет не немедленный рост цен, а более тонкая динамика «перестройки» структуры всей экосистемы цифровых активов. Несмотря на то, что ценовые показатели в этом году были то вялыми, то волатильными, при более глубоком рассмотрении можно увидеть, что несколько фундаментальных трендов продолжают развиваться.

В этой статье рассматривается прогресс по нескольким ключевым темам из «Прогноза на 2026 год», отмечается, какие из наших суждений подтвердились, а какие разошлись, и что эти изменения могут означать для будущего.

1: Ускорение интеграции цифровых активов и традиционных рынков капитала

Мы ожидали, что в 2026 году интеграция цифровых активов с традиционными рынками капитала продолжится. До сих пор этот тренд действительно развивается, в некоторых областях даже быстрее, чем ожидалось.

Несмотря на волатильность на рынке, спрос на доступ к цифровым активам через основные финансовые каналы остается устойчивым, а традиционные платформы продолжают расширять продуктовые линейки.

Примечательно, что открытые позиции по опционам на спотовые биткойн-ETP (такие продукты впервые появились только в ноябре 2024 года) теперь могут конкурировать с опционами, рассчитываемыми напрямую в биткойнах, что отражает продолжающийся рост внедрения среди институциональных и розничных инвесторов.

Импульс в сфере токенизации также усиливается, и активность, кажется, превосходит ожидания. Традиционные финансовые учреждения все чаще запускают инвестиционные продукты на основе блокчейна, а крупные биржи сотрудничают с цифровыми активами или приобретают их доли, чтобы расширить каналы дистрибуции и подключиться к ончейн-инфраструктуре.

В то же время, нормативно-правовая база становится яснее. Комиссия по ценным бумагам и биржам США (SEC) и Комиссия по торговле товарными фьючерсами (CFTC) совместно опубликовали руководство по определению классификации цифровых активов, а продвижение законодательства, такого как закон CLARITY, означает, что участники рынка получат более четкие рамки.

В целом, эти достижения указывают на то, что цифровые активы продолжают интегрироваться в более широкую финансовую систему, причем рыночный спрос и расширение инфраструктуры совместно способствуют этой тенденции.

2: Права держателей токенов постепенно привлекают внимание, но остаются неясными

Мы ожидали, что в 2026 году интересы держателей токенов станут более тесно связанными, и больше ончейн-предприятий будут отдавать приоритет таким механизмам, как обратный выкуп (buyback) и более четкое право собственности.

До сих пор это направление, похоже, не изменилось, и эксперименты продолжаются по всей экосистеме: от динамики обратного выкупа на основе резервов (например, альянс Hyperliquid/USDC) до обновлений в области управления и структуры, таких как реорганизация Aave DAO/Labs.

Однако, несмотря на расширение применения этих механизмов, явная «премия за права держателей токенов» еще не полностью отразилась в рыночных ценах. Эта тенденция развивается, но все еще находится на ранней стадии, и инвесторы все еще оценивают, какие модели действительно могут обеспечить устойчивое накопление стоимости.

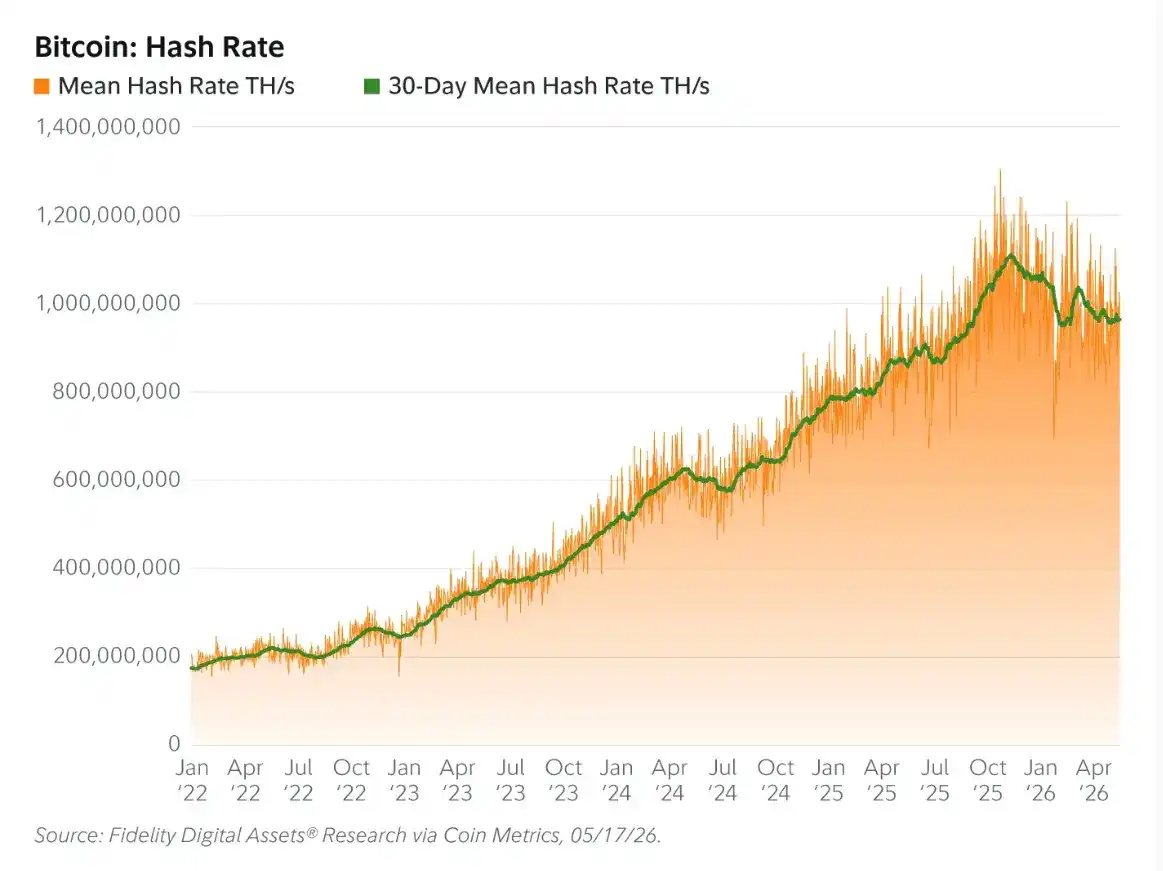

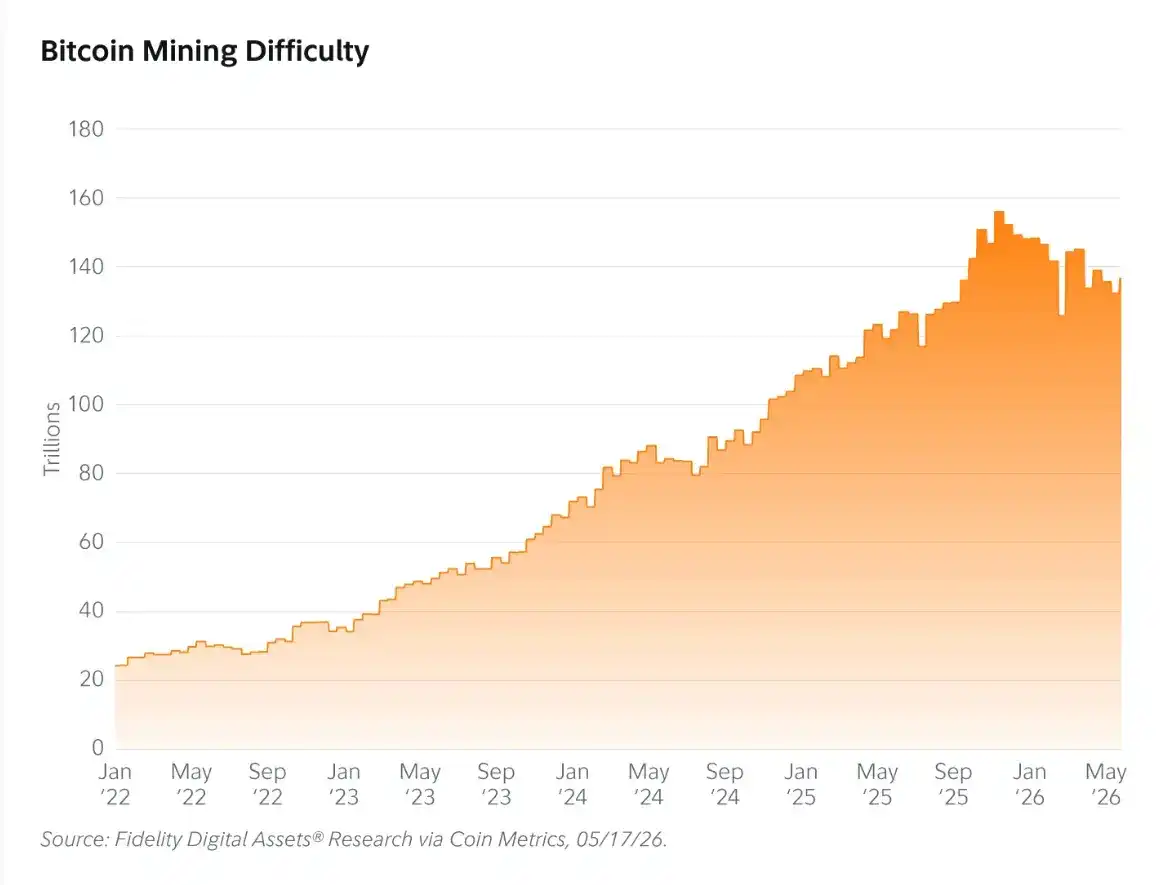

3: Потенциальный переход: майнинг и искусственный интеллект

Мы предполагали, что усиление конкуренции со стороны спроса на вычислительные мощности для ИИ может стабилизировать рост хешрейта биткойна, поскольку майнеры будут перенаправлять энергию и инфраструктуру в потенциально более прибыльные направления. В этом году эта динамика, возможно, начинает проявляться: средний 30-дневный хешрейт и сложность майнинга снизились примерно на 8,8% и 7,8% соответственно.

При рассмотрении более длительной траектории скорость роста хешрейта по сравнению с предыдущими годами замедлилась, что может быть ранним сигналом структурных изменений. Деятельность центров обработки данных для ИИ становится все более прибыльной, особенно для крупных операторов, имеющих доступ к энергетической инфраструктуре, и это, похоже, становится все более вероятной движущей силой.

Хотя это все еще рано, наблюдаемое замедление роста соответствует нашим первоначальным ожиданиям и может отражать постепенный переход майнеров к другим источникам дохода.

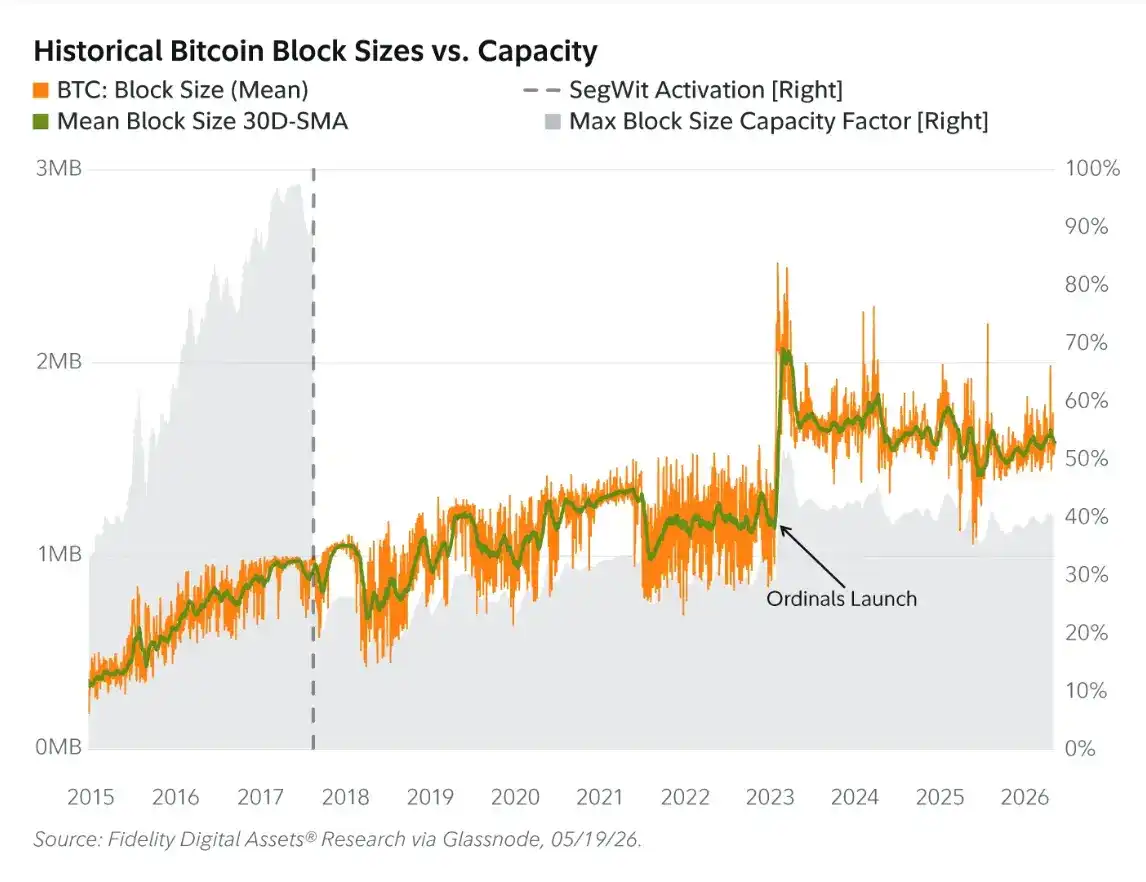

4: Биткойн находится на новой переломной точке

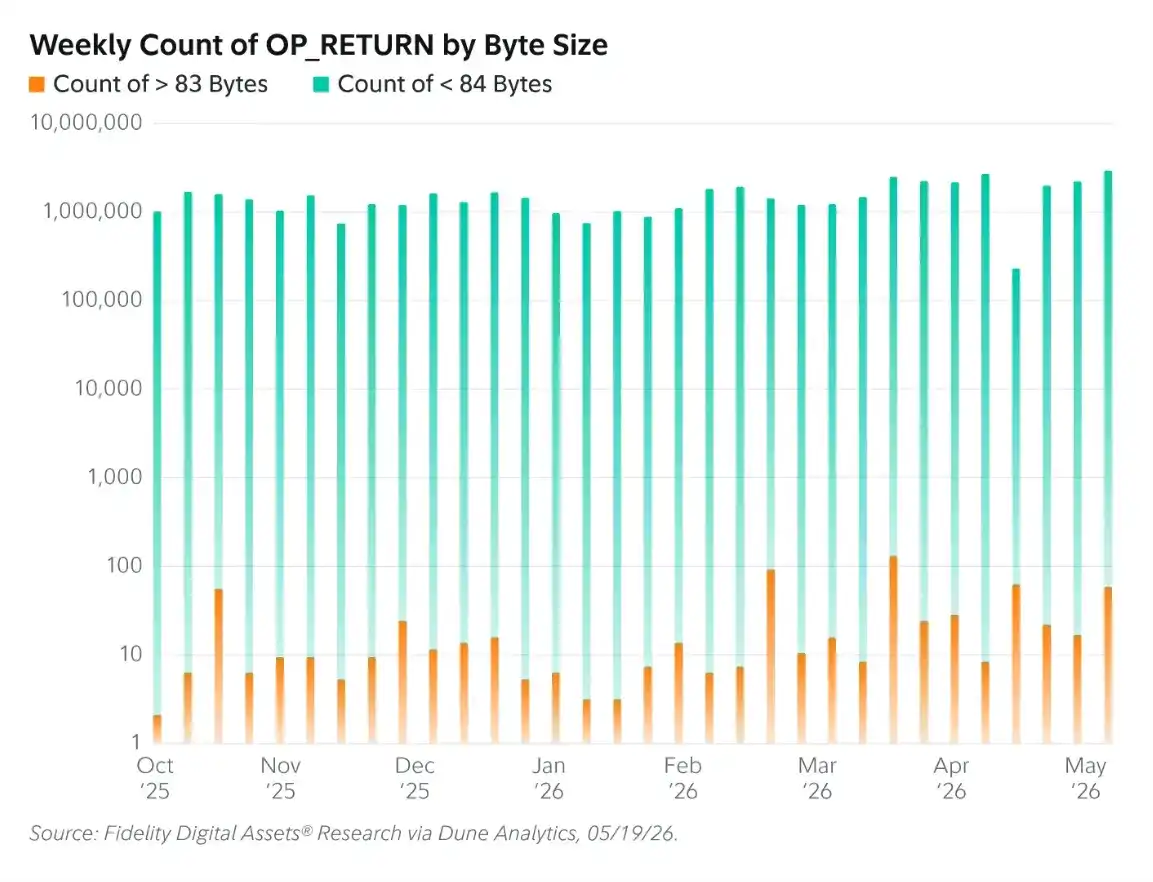

Мы ожидали, что увеличение объема данных, которые можно записать с помощью операционного кода OP_RETURN, не приведет к значительному увеличению размера блокчейна (OP_RETURN используется для записи данных в блокчейн, и, поскольку за это взимается комиссия, увеличение его лимита данных не привело к злоупотреблениям или перегрузке сети). До сих пор данные, кажется, подтверждают это предположение.

Использование OP_RETURN большого размера (≥84 байта) в основном не изменилось, а общий рост блокчейна остается в прогнозируемом диапазоне (около 1,35–2,5 МБ). Другие показатели использования блоков показывают, что емкость все еще ниже 50%, что указывает на то, что увеличение гибкости данных не оказало существенного давления на сеть.

В то же время внимание сместилось на более макроскопическую динамику сети. В узлах Bitcoin Knots наблюдались значительные колебания — быстрый рост и столь же быстрый спад, что вызвало предположения о потенциальной сиблил-активности (Sybil-like).

Согласно текущим данным, узлы Bitcoin Core по-прежнему составляют около 77% сети, а узлы Knots — около 17%. Хотя это меньшинство, это создает риск неожиданного раскола — вероятность невысока, но она не нулевая: при определенных условиях узлы Knots могут отделиться в цепочку, которая остановится или будет менее безопасной. Согласно текущим оценкам, такая ситуация может возникнуть примерно через 80 дней.

Тем не менее, доминирующая доля Core по-прежнему закрепляет консенсус сети. В то же время усиливается импульс вокруг долгосрочных обновлений безопасности. BIP-360 был упрощен и ввел квантово-устойчивый тип вывода (Pay-to-Merkle-Root, или P2MR); продолжающиеся исследования OP_CHECKSHRINCS отражают изучение схем хеш-основанной постквантовой подписи.

Хотя конкретное время возникновения квантовой угрозы не определено, эти достижения показывают, что отрасль все больше внимания уделяет ранней подготовке к будущей безопасности сети.

5: Медведи временно контролируют ситуацию

В январе мы описали два сценария с равными силами быков и медведей на старте 2026 года, ожидая, что макроэкономические условия приведут к нелинейному движению, несмотря на улучшение структурных фундаментальных факторов.

До сих пор в значительной степени преобладал медвежий сценарий: биткойн упал на 13% на фоне деклевереджа из-за ликвидаций, сохраняющейся высокой инфляции и геополитической неопределенности, которая заставила рынки ожидать дальнейшего повышения процентных ставок. Однако недавние рыночные результаты демонстрируют более тонкую динамику.

После первоначальной волны распродаж, вызванной недавним геополитическим конфликтом, биткойн восстановился и в тот же период показал лучшие результаты, чем традиционные активы, что, возможно, отражает спрос на высоколиквидные, нейтральные активы в периоды стресса.

В то же время структурные положительные факторы остаются, включая продолжающееся формирование институционального капитала, постепенное повышение регуляторной ясности и расширение глобальной ликвидности.

Хотя краткосрочная среда по-прежнему ограничена, наша более широкая оценка, кажется, остается верной, хотя и развивается неравномерно.

6: Золото сохраняет силу. Что будет дальше?

Мы отмечали, что еще один сильный год для золота не станет неожиданностью, учитывая поддержку со стороны спроса со стороны центральных банков и глобальную тенденцию постепенного ухода от долларовой системы.

В этом году золото сначала выросло почти на 30% на фоне геополитической напряженности, а затем отступило до более умеренного роста около 3–4%. Несмотря на коррекцию, золото все еще может показать лучшие результаты к концу года.

Свидетельств в пользу ухода от долларовой системы также становится все больше, включая некоторые новые альтернативные способы расчетов, такие как принятие Ираном биткойнов для оплаты сборов за проезд, а также платежи, связанные с активностью в Ормузском проливе.

В то же время спрос центральных банков на золото остается высоким. Последние данные показывают, что накопление продолжается, и что примечательно, золото уже превысило доллар США и казначейские облигации США, став основным компонентом глобальных резервов.

Показатели золота и продолжающийся спрос со стороны центральных банков в целом соответствуют нашим первоначальным ожиданиям; а ожидаемое нами превосходство биткойна пока не проявилось.

Заключение: Накопление сил под поверхностью

К середине года ландшафт цифровых активов в 2026 году демонстрирует баланс между краткосрочным давлением и долгосрочным прогрессом. Несколько тем из «Прогноза» развиваются в соответствии с ожиданиями, особенно в области институционального участия, регулирования и инфраструктуры; другие же все еще находятся на ранней стадии или еще не полностью реализованы.

Для инвесторов это означает, что необходимо смотреть за пределы краткосрочных ценовых колебаний и наблюдать, как формируются структурные изменения. Многие основы, которые поддержат следующий этап роста, кажется, укрепляются, даже если это еще не полностью проявилось.