Original author: ChandlerZ, Foresight News

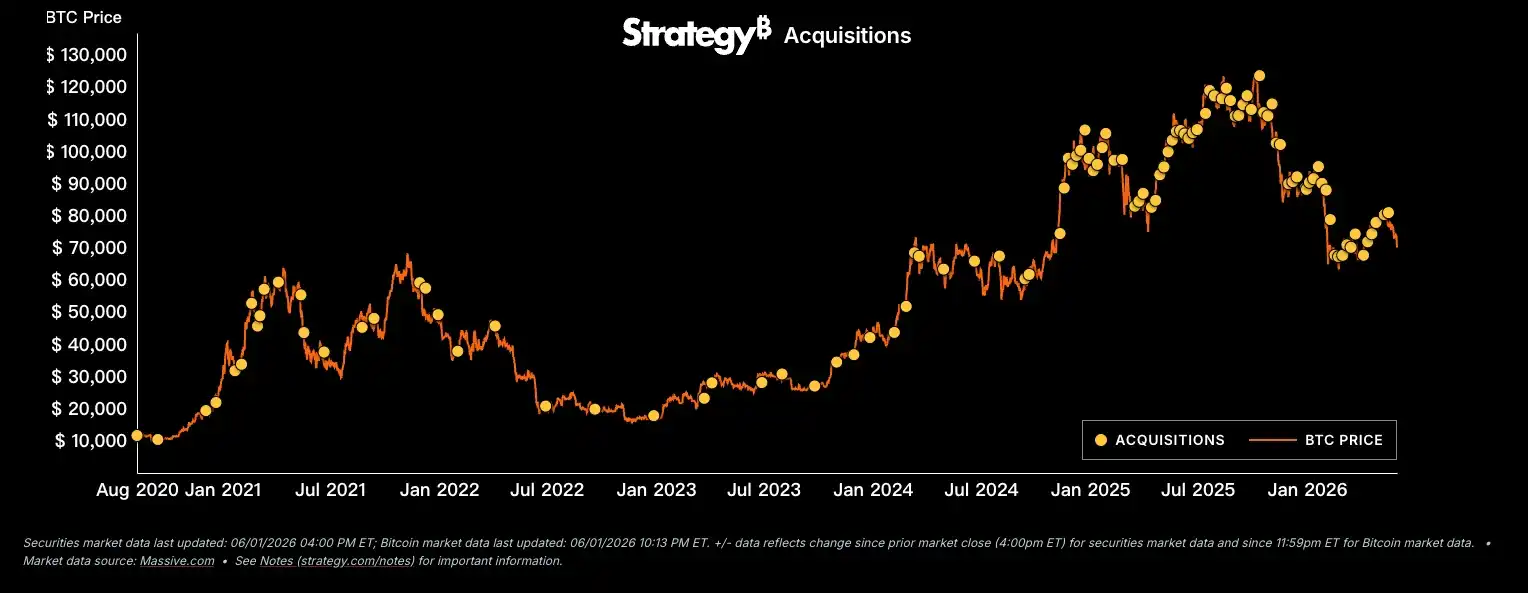

On June 1, Strategy filed an 8-K form with the SEC, disclosing the sale of 32 bitcoins between May 26 and 31 at an average price of $77,135, totaling approximately $2.5 million. After the sale, the company still holds 843,706 BTC, with a total cost of $63.87 billion and an average cost basis of $75,699.

The 32 BTC represents 0.004% of its total holdings, and the $2.5 million is equivalent to Strategy's average daily purchase volume over the past 12 months. From a financial perspective, this transaction is almost meaningless. However, what it broke is far more significant than the amount realized. Since its first bitcoin purchase in August 2020, Strategy has only sold once before: in December 2022, it sold 704 BTC for $11.8 million at an average price of $16,776 for the purpose of tax-loss harvesting, repurchasing 810 BTC at a lower price two days later. That sale was essentially a tax operation, not a genuine reduction in holdings.

But this time is different. The $2.5 million is explicitly marked for paying preferred stock dividends, and Strategy does not intend to buy them back.

The Dividend Bills Are Coming Due

Strategy began issuing preferred stock intensively from early 2025: STRK with an 8% annual coupon, STRF at 10%, STRD at 10%, and STRC at 11.5%. With these four series stacked together, the company has cumulatively paid over $693 million in dividends so far.

The logic behind these preferred shares is that investors give money to Strategy, Strategy uses it to buy Bitcoin, and then pays fixed-rate dividends from its cash reserves and operating income. If Bitcoin rises, the mNAV premium expands, and Strategy can continue to issue new shares to raise funds and keep the cycle going. If Bitcoin falls or moves sideways, the dividend obligations do not disappear, but the financing window narrows.

MicroStrategy's Bitcoin Accumulation Pace

In December 2025, Strategy established a $2.25 billion cash reserve specifically to cover dividends and debt payments, which at the time could last about 30 months. But by May 31, 2026, this reserve had fallen to $900 million, a $1.35 billion drawdown in six months.

During the Q1 earnings call, Strategy CEO Phong Le, for the first time in a public setting, listed a 'disciplined sale of bitcoin' as one of the capital management tools. Not many people noticed that statement at the time; in retrospect, it was a preview of this 32 BTC sale.

Saylor posted a tweet on February 2, 2025, saying 'Never sell your bitcoin.' This tweet was widely shared after the 8-K disclosure. He himself only discussed STRC's product positioning in a post afterward, stating Strategy's goal is to make STRC the world's best credit instrument, completely sidestepping the topic of selling Bitcoin.

MSTR's stock price fell about 6% that day. Mizuho maintained its Buy rating but lowered its price target from $320 to $265. Most analysts believe the $2.5 million sale is not materially impactful financially, but the core significance of this event lies in the signal it sends: a crack has been opened. If cash reserves continue to deplete while dividend obligations remain unchanged, the scale of future sales might not stop at 32 bitcoins.

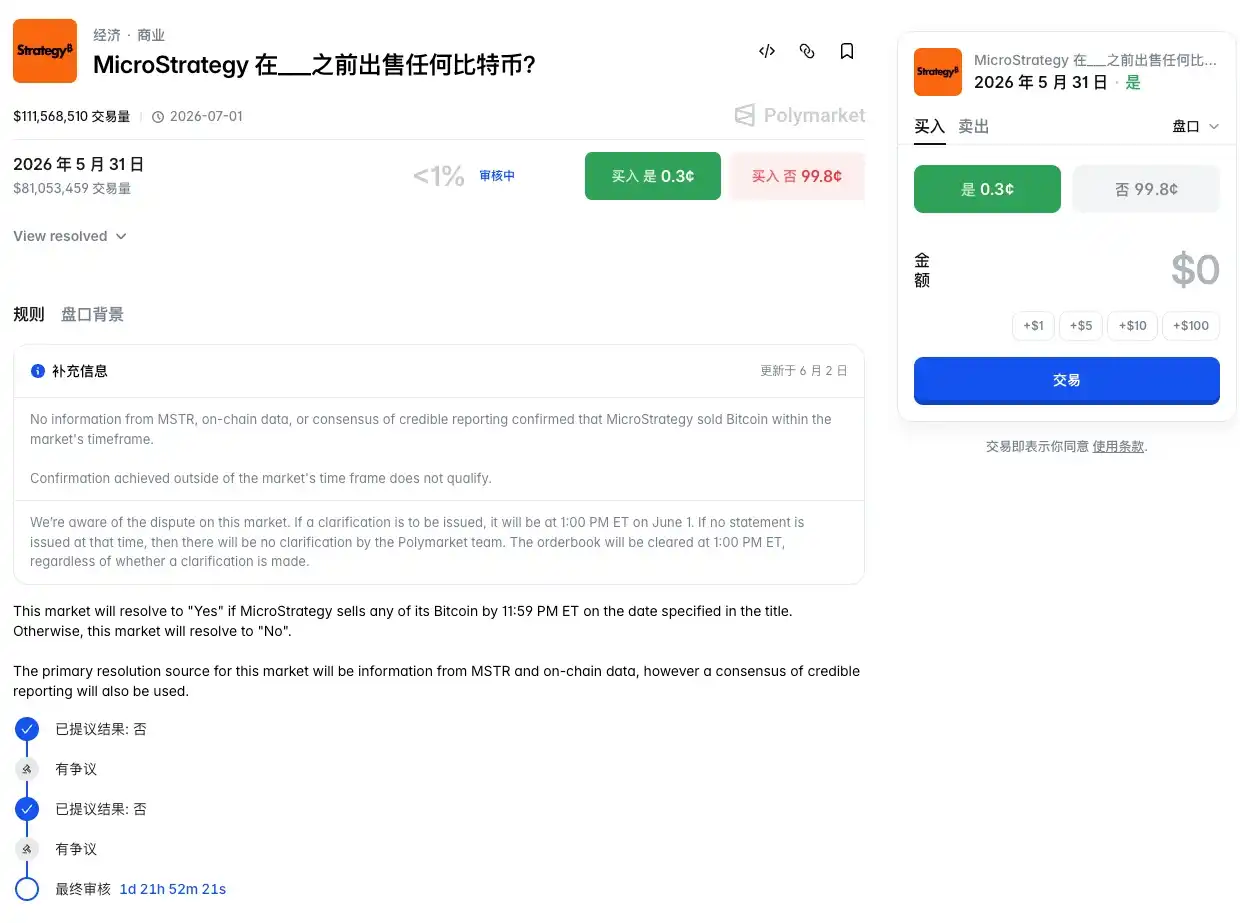

A $110 Million Word Game on Polymarket

Strategy's selling timing also ignited a prediction market on Polymarket.

The market's question was: Will Strategy sell Bitcoin before May 31? The cumulative trading volume currently exceeds $111 million. The 8-K filing shows the transactions occurred between May 26 and 31, with the filing itself timestamped 'May 31, 2026, 4:00 PM ET'. However, the 8-K was only submitted to the SEC on June 1, and the public learned about it after the deadline had passed.

Those who bought 'Yes' argued that the transaction happened before the deadline, as the 8-K clearly states May 31. Those who bought 'No' argued that there was no public information before the deadline proving the sale occurred, so according to the rules, it should be judged as 'No'. After two 'No' proposals were challenged, the dispute escalated to UMA's token-voting arbitration.

Polymarket subsequently added a note to the page, stating that 'consensus from MSTR, on-chain data, or reliable reporting did not confirm that Strategy sold bitcoin within the market's defined time frame. Confirmations obtained outside the market-defined time frame do not satisfy the requirement.'

Behind this controversy lies a deeper issue with Polymarket's arbitration mechanism. A May investigation by *The Wall Street Journal* found that in most of Polymarket's disputed markets, over half of UMA voting power is concentrated in the top 10 largest wallets, approximately 60% of active voters can be linked to Polymarket accounts, and roughly one in five disputes involves voters simultaneously holding positions in the contracts being adjudicated. So far in 2026, Polymarket has generated over 1,150 disputed markets, exceeding the total for all of 2025.

It's Not Just Strategy Selling; Bitcoin Drops Below $72K

Strategy's 8-K disclosure overlapped with an already weak market environment. Bitcoin fell below $72,000 on June 1, hitting its lowest level since April 13. CoinShares data shows digital asset investment products saw net outflows of $1.67 billion last week, the second-largest weekly outflow in 2026. For the entire month of May, Bitcoin spot ETFs saw net outflows of $2.3 billion, the largest monthly net outflow this year. Total digital asset assets under management have dropped to approximately $141 billion, a low since the beginning of the year.

Strategy sold 32 bitcoins, but it is not the first Bitcoin treasury company to make a move. Q1 data shows selling has become a collective behavior. MARA Holdings sold 15,133 BTC between March 4 and 25, raising about $1.1 billion, mostly used to repurchase convertible bonds maturing in 2030 and 2031. Riot Platforms sold 3,778 BTC during the same period, raising $289.5 million, reducing its holdings from 19,223 BTC to 15,680 BTC, a 18% shrinkage. David Bailey's Nakamoto Holdings sold 284 BTC in March, about 5% of its holdings. Empery Digital sold 370 BTC in April to repay loans. Genius Group liquidated its final 84 BTC to repay $8.5 million in debt.

Just MARA, Riot, and Nakamoto collectively offloaded over 19,000 BTC in Q1. On-chain data from CryptoQuant shows that Bitcoin's apparent demand fell to negative 63,000 BTC by late March. This apparent demand (a measure of total demand relative to changes in new supply) turning negative indicates a deep market contraction, with overall selling pressure significantly outweighing buying pressure.

Some companies aren't just selling but are directly abandoning the treasury model. Forum Markets (formerly ETHZilla) liquidated approximately $114 million worth of ETH at the beginning of the year, pivoting to tokenization business. VivoPower, which originally planned to build an XRP treasury, directly pivoted to data centers and AI infrastructure in February, disposing of its entire XRP holdings along the way.

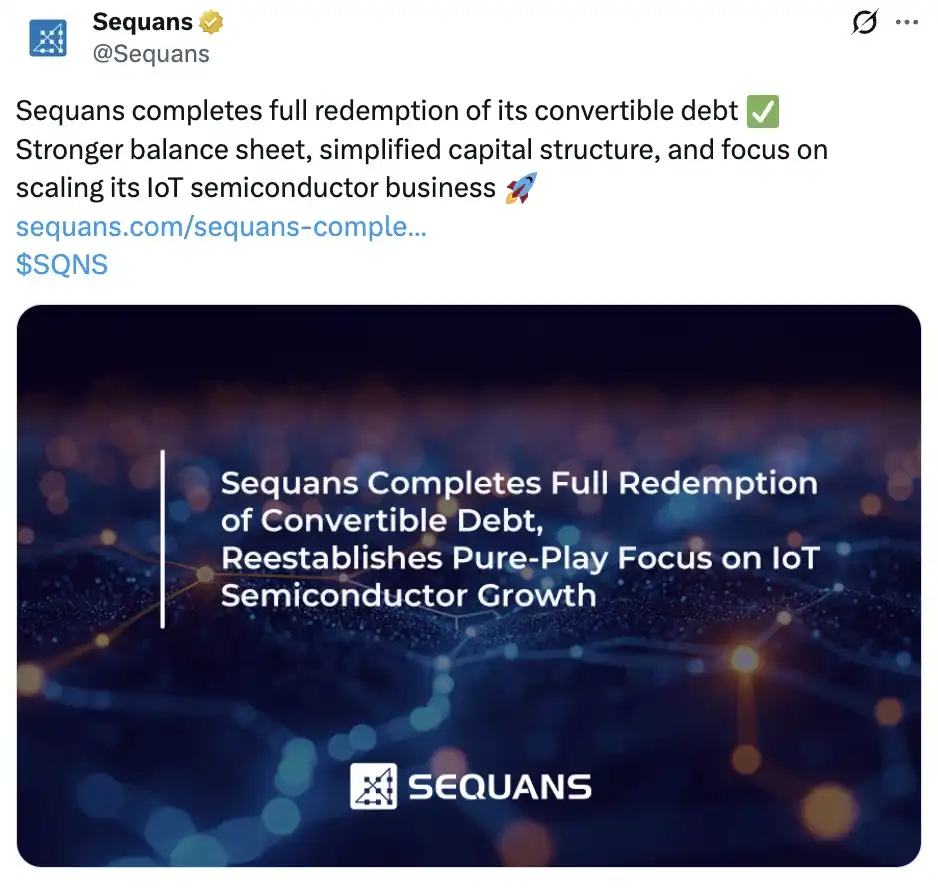

On May 28, French semiconductor company Sequans Communications confirmed it had fully repaid its convertible bonds by selling its Bitcoin holdings, and also planned to gradually liquidate its remaining 658 bitcoins. The company's Bitcoin holdings once peaked at 3,234 BTC.

Sequans had previously publicly stated its intention to accumulate over 3,000 bitcoins as long-term reserve assets. But this so-called 'long-term' ultimately lasted less than a year. The company's stock (ticker SQNS) has fallen 77% year-to-date, with a cumulative decline of 97% over the past five years.

The business model of Bitcoin treasury companies was validated during the upward cycle in the second half of 2025. Rising Bitcoin prices pushed up the mNAV premium, allowing companies to issue new shares or convertible bonds at a premium to raise funds to buy more Bitcoin, further pushing up the price and premium, creating a positive feedback loop. After the market peaked last October, this flywheel reversed. Falling Bitcoin prices compress the premium, narrowing the financing window, while dividend and debt payment obligations do not decrease with the price drop. Selling Bitcoin became the most direct source of liquidity. According to Bitwise statistics, as of the end of Q1, publicly traded companies collectively held about 1.15 million BTC, representing 5.47% of the total supply. This scale itself constitutes a risk. If multiple treasury companies are forced to reduce holdings within the same time window, they, being the largest buyers of Bitcoin, could also become the most concentrated source of selling pressure.

Currently, there are very few companies still buying. Strive accumulated purchases of approximately 1,944 BTC in May, spending about $150 million. Metaplanet bought 5,075 BTC in early April. Strategy itself was also buying in May, accumulating purchases of over 25,000 BTC for the month, worth over $2 billion.

Spending $2 billion to buy while taking out $2.5 million to pay dividends illustrates that Strategy is far from a liquidity crisis at this point. But the signaling significance of the 32 BTC is that even the largest HODLer has begun to acknowledge that selling is an option in the toolbox.