TL;DR

Over the past few years, the core question for AI investments has been simple: Will AI change the world? As long as the answer leaned towards "yes," the market was willing to assign higher valuations to chipmakers, cloud providers, software companies, and model developers.

Recently, the market narrative has begun to shift. Some semiconductor and high-valuation AI software stocks have seen pullbacks, with market participants shifting capital preferences towards areas with clearer order pipelines and more stable cash flows. Concurrently, Alphabet announced a large-scale equity fundraising and had previously revised its 2026 capital expenditure guidance upward in its Q1 earnings report.

These two events cannot be simplistically framed as "fundraising caused the decline." A more accurate context is that the market is repricing AI—from a software-style growth story to a capital-intensive infrastructure cycle.

The keyword here is capital expenditure. AI is not a business that can scale by writing a few lines of code; it requires chips, data centers, networks, power, and land. The greater the capex, the more investors ask three questions: Where is the money coming from, how expensive is it, and how long will it take to get a return.

Alphabet's Fundraising Makes the Market Recalculate the Capital Account

Alphabet's fundraising itself is not a crisis signal, but it is a strong reminder: AI build-out is now a mega-capital project.

According to SEC filings and reports from Reuters and Investing, Alphabet announced plans in June 2026 for an approximately $80 billion equity fundraising, later adjusted to $84.75 billion. The funds are intended for uses including AI infrastructure and computing capacity expansion, though not all will be directly allocated to AI capex. SEC documents show that of a $40 billion ATM (At-The-Market) program, about $30 billion is anticipated for administrative arrangements related to tax obligations for employee stock vesting.

This distinction is important. Labeling the entire $84.75 billion as "AI construction funds" overstates the direct allocation, but it still alters investor sentiment. Because even a cash cow like Alphabet needs to expand fundraising in public markets, the market naturally wonders: If it needs to bolster financial flexibility, who will provide the capital needed next by OpenAI, Anthropic, xAI, data center REITs, and power companies?

Capital expenditure and operating expenses are also not the same. Spending on hiring and marketing is an opex; buying servers, building data centers, and securing power is capex. The latter is more like building a factory—it creates significant upfront cash flow pressure, appears on the books slowly through depreciation, but the market immediately assesses the payback period.

In its Q1 2026 earnings call, Alphabet raised its full-year capital expenditure guidance from $175-185 billion to $180-190 billion. The company cited reasons including investments related to the Intersect acquisition, as well as AI compute demand. Management emphasized maintaining a healthy balance sheet and financial flexibility and did not describe the fundraising as a survival pressure.

Investors are calculating a different equation. When capex guidance is repeatedly revised upward, the denominators in valuation models change: depreciation increases, free cash flow faces pressure, financing costs and potential equity dilution enter the calculation. The AI trade is entering its next phase. The previous phase rewarded imagination; the next phase rewards capital efficiency.

AI Money Isn't Just Burning on Big Tech's Books

The capital requirements for AI infrastructure don't fall solely on giants like Alphabet, Microsoft, Amazon, and Meta. What truly makes the market nervous is that multiple types of entities may simultaneously compete for the same pool of capital.

The first category is frontier model companies. Companies like OpenAI, Anthropic, and xAI see rapid revenue growth, but training and running models require continuous computing power purchases, leading to significant cash burn. Unlike established cloud providers with the cushion of advertising, cloud, and software cash flows, they rely more on external funding, strategic investments, and may later depend on IPOs or debt markets.

The second category is data center companies. AI doesn't need ordinary office servers but high-density, energy-intensive data centers. Data center REITs raise capital to build facilities and then lease computing infrastructure to cloud providers or AI companies. Assets like Digital Realty and Equinix benefit from demand expansion, but the expansion itself requires continuous financing.

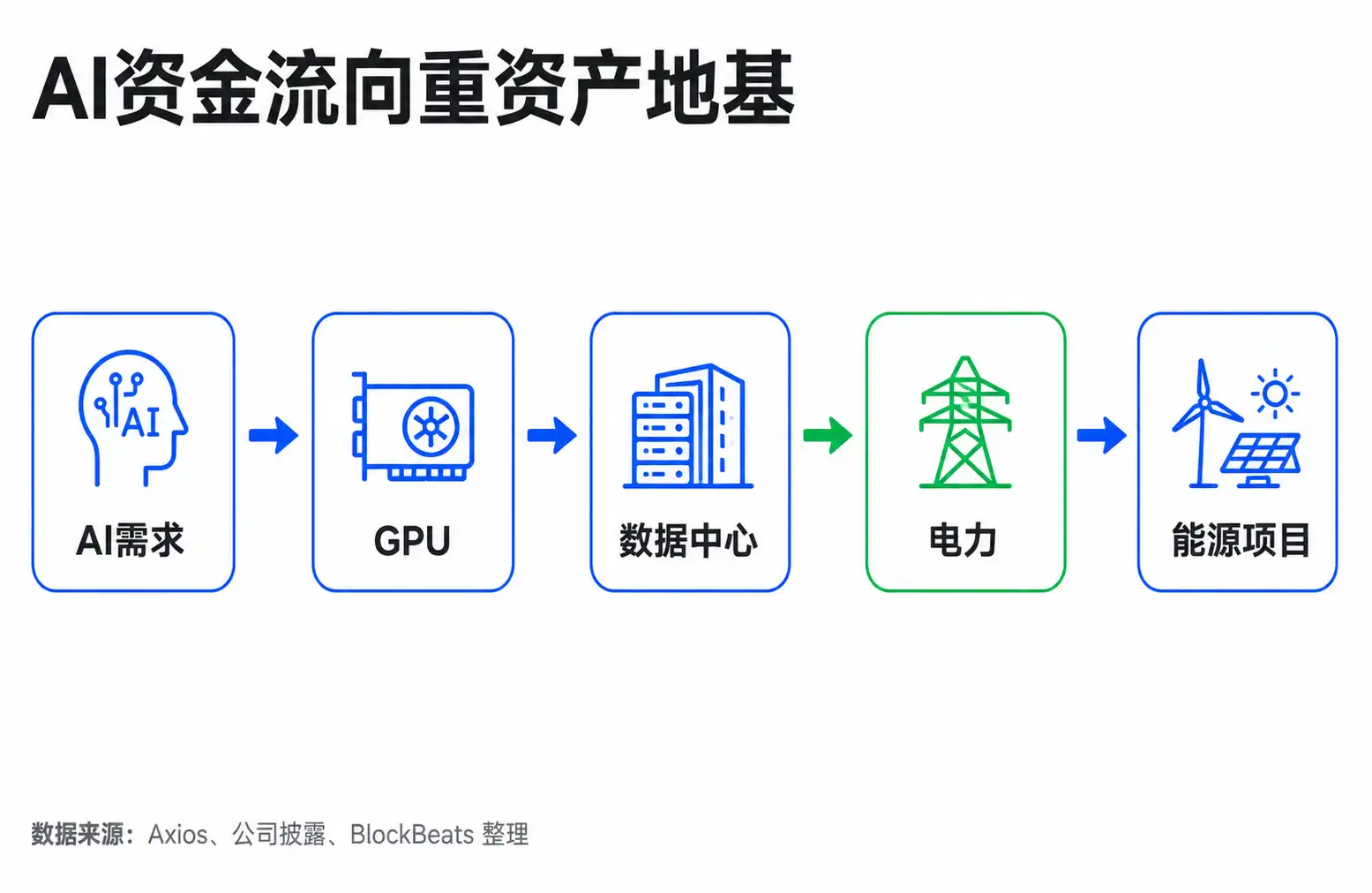

The third category is power and utilities. One of the biggest bottlenecks for large AI data centers isn't chips, but electricity. Large data centers transfer pressure to the power grid, substations, transmission lines, and long-term power purchase agreements. The money burned by AI companies doesn't stop at GPUs; it flows along the supply chain to land, facilities, cooling, the grid, and energy projects.

According to an Axios report on June 10, 2026, Alphabet, Amazon, Meta, Microsoft, and Oracle had raised $255.34 billion through equity and debt in 2026, stating that the five companies' AI data center spending for the year would reach approximately $750 billion. This figure shouldn't be taken as precise causal proof, but it gives the market a sense of scale: AI's capital needs are transitioning from a single-company issue to a financing cycle that the entire financial market needs to absorb.

The market used to view AI as a software revolution: low marginal cost, fast growth, high margins. Now, frontier AI resembles infrastructure revolutions like railroads, electricity, and fiber optics: requiring concentrated build-out early on, massive investment, potentially creating immense value eventually, but facing tests of financing capacity, cost of capital, and capacity utilization in between.

Valuation Logic Shifts to Payback Speed

When a market reassessment occurs, prices initially reflect not that fundamentals have deteriorated, but that investors are starting to ask a different set of questions.

Previously, they asked: Whose AI narrative is strongest? Whose revenue growth is fastest? Who is closest to the next platform entrance? Now the questions are: Who can convert invested capital into cash flow? Whose order book is sufficiently certain? Who has access to low-cost financing? Who will see profit dilution or pressure during this high-capex cycle?

This explains the recent divergence within the AI sector. High-valuation AI software companies and those with heavier long-term narratives are more vulnerable because their valuations rely on future growth. Once the market raises its cost of capital estimate, the discounted present value of future cash flows declines. Some semiconductor companies may also be affected, as investors worry whether order growth can continue at super-expected rates.

But this doesn't mean all AI assets are being abandoned. Hardware, storage, networking equipment, data centers, and power assets with clearer order visibility might反而 find relative support during this reassessment. The reason is straightforward: when the market starts focusing on the build-out cycle, the "pick-and-shovel" sellers still have demand; but investors will be more挑剔 in asking whose orders are truly visible and who is just riding the narrative for valuation.

This is also the divergence between Alphabet management and cautious investors. Management emphasizes that AI investment is a strategic necessity, and fundraising is to maintain initiative in long-term competition. The cautious camp worries that AI monetization速度 may lag behind capital expenditure, especially when multiple giants and model companies simultaneously expand fundraising, prompting capital markets to demand higher returns and thus压低 valuations.

Both sides can be true simultaneously. AI can be the correct long-term infrastructure investment while also temporarily depressing free cash flow and valuation multiples in the short term. For investors, being "bullish on AI" and "bearish on a subset of AI valuations" are not contradictory.

Next Steps: Watch Capex and Revenue Realization

It's too early to attribute the recent pullback solely to AI financing pressure driving the market, let alone claim an AI liquidity crisis has emerged. Macro interest rates, profit-taking, cooling of crowded trades, and employment data fluctuations could all be reasons for sector volatility. The fundraising news更像是 incorporated into the market's explanatory framework rather than a button单独 driving prices.

But this explanatory framework itself deserves attention. Once the market starts pricing AI with "capex, cost of capital, payback period," the ranking of many assets will change.

For cash cows like Alphabet, the question isn't whether they can raise money, but whether AI investment will持续挤压 free cash flow and whether new投入 can translate into cloud revenue, advertising efficiency, subscription revenue, or enterprise service revenue. As long as revenue growth can cover depreciation and financing costs, the market can accept higher capex; if capex continues to be revised upward while returns迟迟不出现, valuation pressure will become more pronounced.

For pure-play AI companies, the question is more direct: Can high revenue growth keep pace with computing power consumption? If OpenAI, Anthropic, xAI can prove that enterprise customers are willing to持续付费 and unit economics improve, external capital will still flow in; if revenue growth is largely consumed by higher training and inference costs, the next round of financing or IPO pricing will be more挑剔.

For data center and power assets, the market will watch long-term contracts, utilization rates, financing structures, and power constraints. The more real the AI demand, the more important these "foundation" assets become; but if financing costs rise, or if data center construction超前于 real demand, they could shift from beneficiaries to承压方 of heavy-asset压力.

The most important validation points going forward are not the daily涨跌 of a semiconductor index, but whether the next round of earnings reports shows further upward revisions to capex guidance, whether AI revenue can materialize faster, and whether public markets can still smoothly absorb large-scale equity and debt issuance. As long as these variables remain positive, the AI trade isn't over; but the valuation language the market uses for AI has likely moved past the phase of只看想象空间.