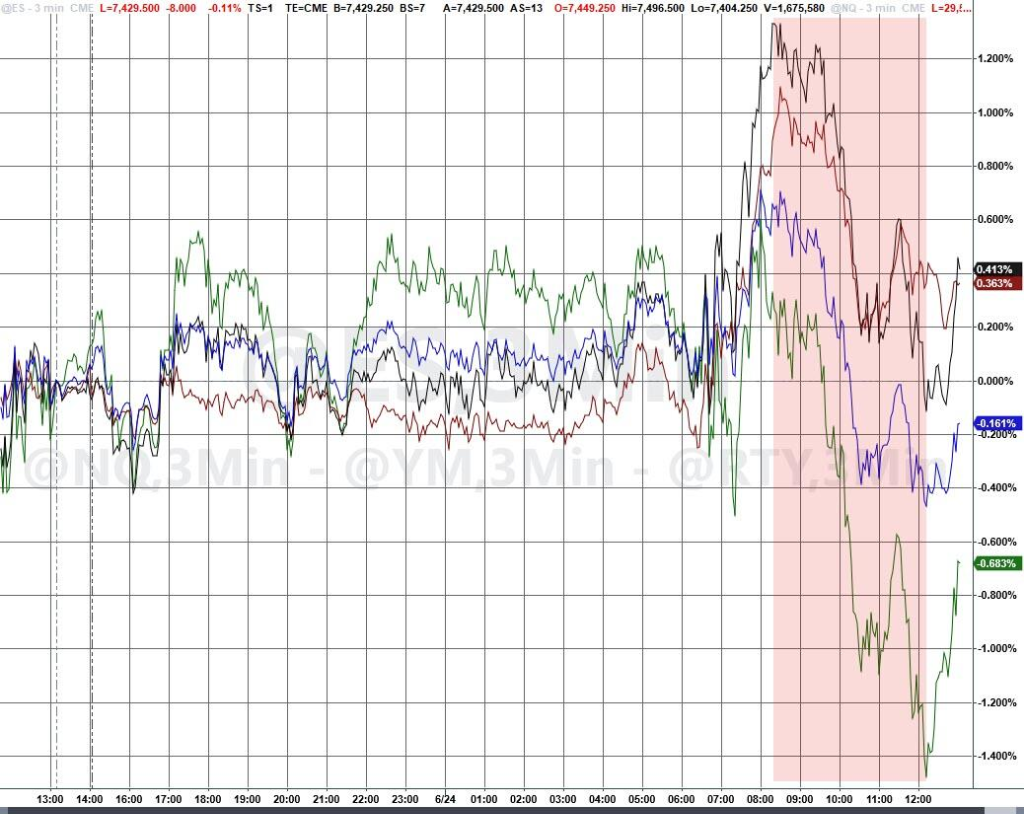

The weakness in the tech sector led to mixed intraday performance for major U.S. stock indices. Oil prices fell to their lowest level since the outbreak of the Iran war, and the fading inflation risk premium pushed the 10-year U.S. Treasury yield down by 9 basis points in a single day.

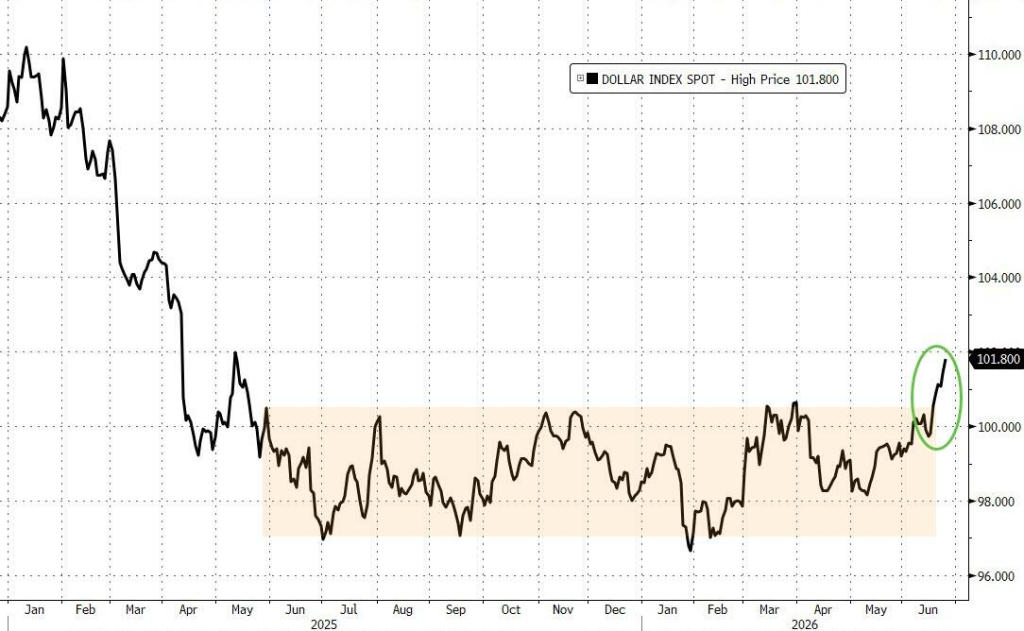

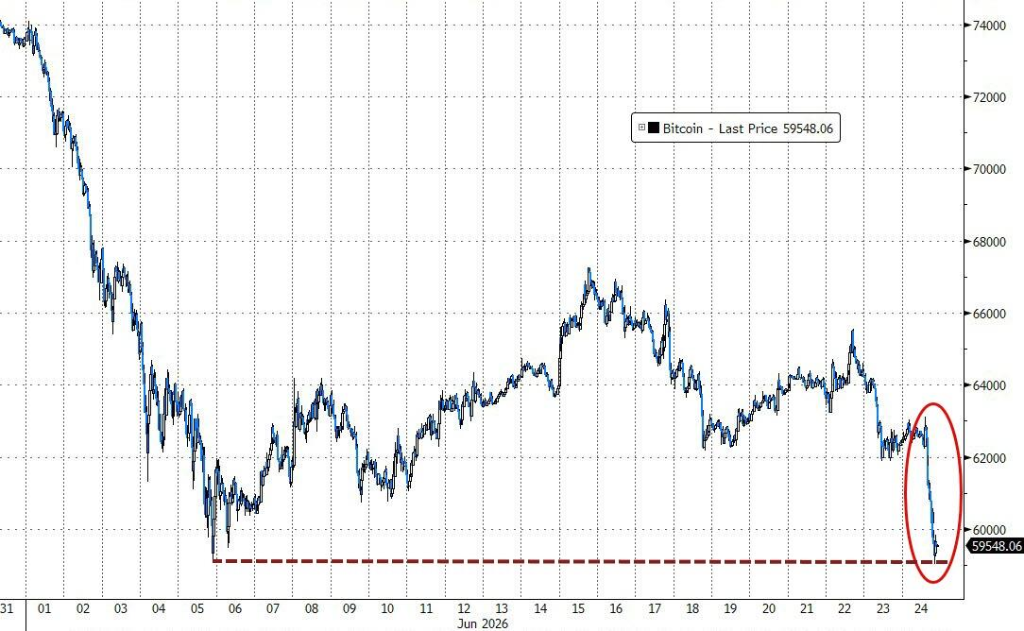

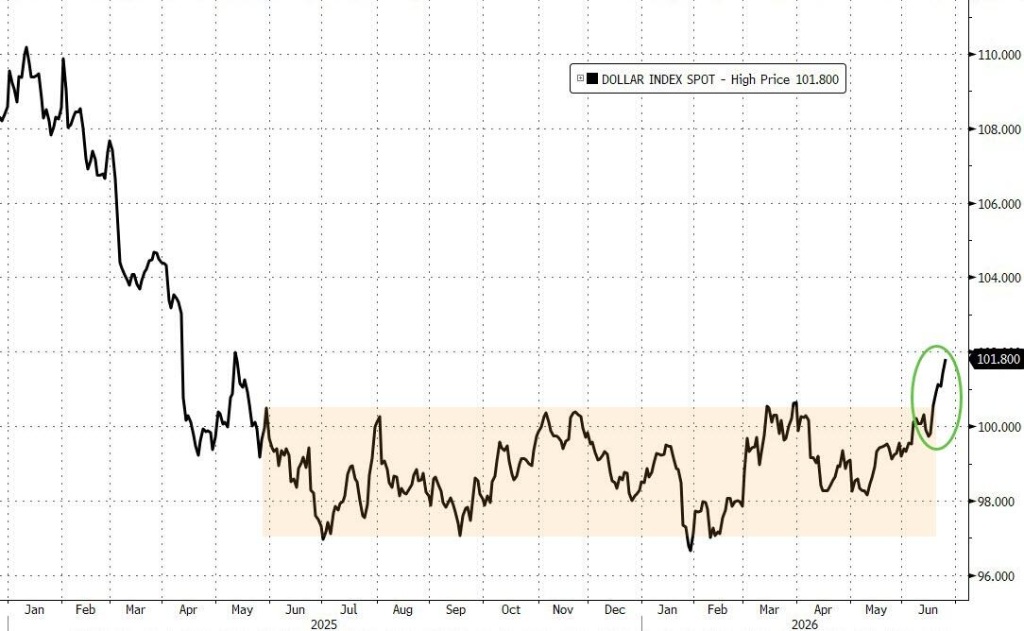

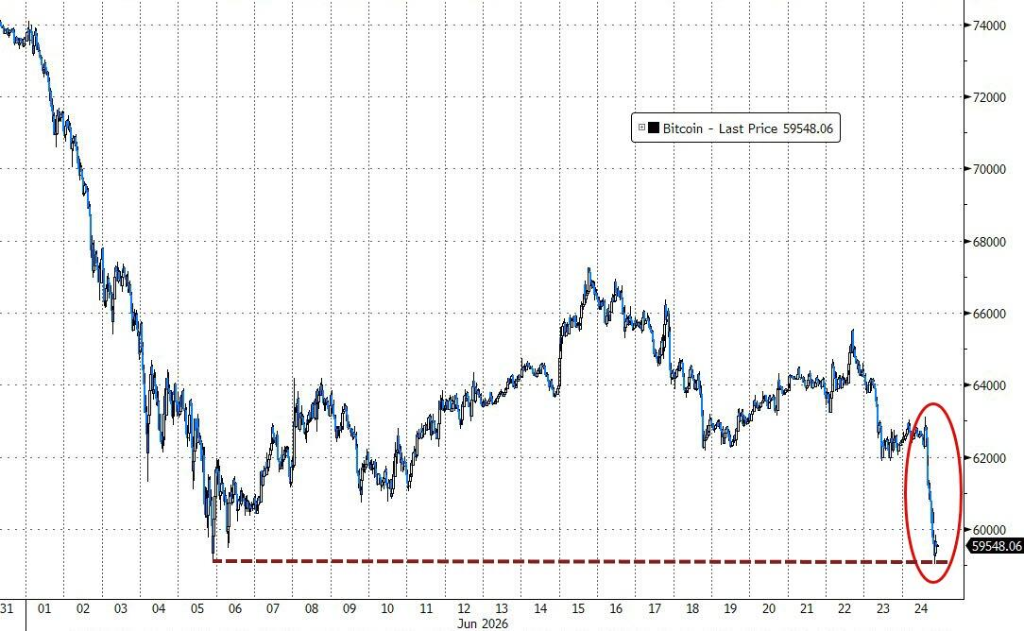

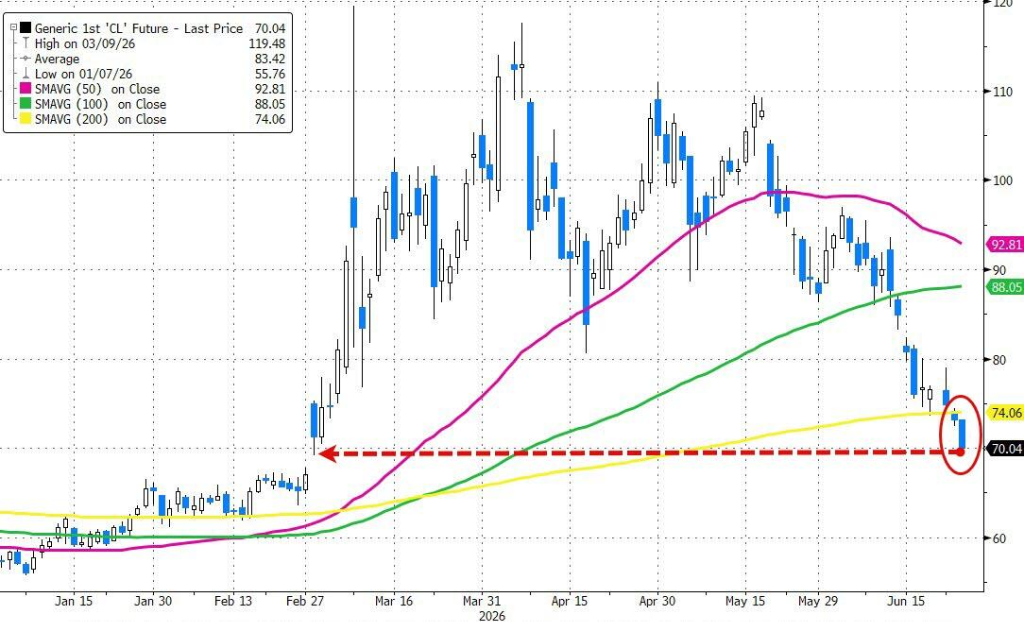

The dollar broke through a 13-month high, weighing heavily on the commodity markets. Gold prices briefly fell below $4000, oil dropped below $70, and Bitcoin once dipped below $60,000.

Micron Technology's stock jumped over 16% after-hours as the company reported earnings that beat analyst expectations. An AI-driven shortage of memory chips is driving product prices significantly higher. The Nasdaq 100 ETF rose 1% after-hours.

Following an overnight V-shaped recovery in South Korean stocks, the three major U.S. indices initially rose after Wednesday's opening. However, selling pressure began as European markets closed and persisted with each rebound attempt. The Nasdaq experienced the largest decline, while the Dow Jones and the small-cap index barely managed to hold onto gains.

Notably, despite overall index pressure, more than 310 stocks in the S&P 500 closed higher on the day. The 'Magnificent Seven' tech giants underperformed the remaining 493 S&P components, showing a clear "rotation" pattern in the market.

Technology and energy stocks were the biggest drags of the day, while consumer discretionary and industrial sectors relatively outperformed. Over the past two days, the AI "leader" sector has shown notable weakness. The S&P 500 index (excluding the AI sector) actually rose over 1%, while the AI semiconductor sector plummeted nearly 10%.

The Philadelphia Semiconductor Index fell 0.82% for the day. Qualcomm dropped over 4%, Arm and Marvell Technology fell over 3%, ON Semiconductor declined over 2%, and Micron Technology also fell 0.81%.

Cerebras Systems plunged about 19%, falling below its IPO issue price after the company forecast its full-year profit margin would be lower than Q1 levels in its first post-IPO quarterly report.

OpenAI announced the launch of its first self-developed AI chip, codenamed "Jalapeño," jointly developed with Broadcom on the same day, further increasing competitive pressure on external chip suppliers.

Mark Hackett of Nationwide believes the recent tech weakness is more of a position adjustment and rotation rather than a fundamental warning signal. Rick Gardner of RGA stated:

Stocks rose too fast and too much; a pullback was almost inevitable. For investors underweight this sector, this correction actually provides a buying opportunity, as the fundamentals of this sector remain strong.

Micron Technology's after-hours report of its fiscal 2026 Q3 (ended May 31) results and guidance became a key variable for whether the market could stabilize.

As mentioned by Wall Street News, Micron's Q3 revenue grew approximately 346% year-over-year to $41.46 billion, about 16% above analyst expectations. Non-GAAP adjusted EPS grew over 12-fold to $25.11, more than 20% above estimates.

Analysts generally believe the guidance is even more important than the quarterly data itself. Micron expects Q4 adjusted revenue between $49 billion and $51 billion, implying record revenue this quarter. The midpoint guidance of $50 billion is 15.6% above analyst expectations.

Nomura pointed out that the implied volatility premium for Micron's earnings in the options market exceeded the market impact of recent Federal Reserve meetings. The options market implied a breakeven volatility range of about ±7% to 8%. If the actual price movement reaches 10% and breaks this range, the market may interpret it as a signal verification of demand in the semiconductor and AI industry chain, potentially triggering broader directional volatility in tech stocks.

In the end, Micron's after-hours sales forecast was comprehensively ahead of market expectations, causing its stock price to jump over 16%, drawing a provisional pause to the tech sell-off of the previous days.

Memory stocks hit highs again after Micron's report, and the rally wasn't limited to Micron or just 16%. Influenced by Micron's results, Qualcomm's stock price also rose over 10%.

At an investor day event on Wednesday, Qualcomm made a series of positive comments on the growth prospects in the AI field. The company stated that its expansion into data center chips would generate "billions of dollars" in revenue in the fiscal year starting in October.

Other U.S. chip stocks also surged after-hours. Memory stocks Western Digital, SanDisk, and Seagate Technology all jumped over 10%.

Arm and Applied Materials rose over 6%, ASML and Intel gained over 4%, AMD climbed over 3%. In early Thursday Asia-Pacific trading, Nasdaq 100 index futures once surged over 2%.

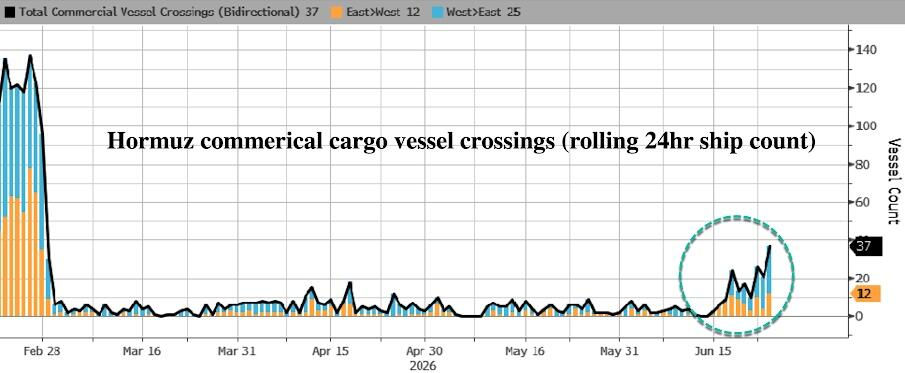

According to International Energy Agency estimates, UAE oil exports have recovered to nearly 85% of pre-war levels, reflecting a significant increase in oil shipments via the Strait of Hormuz in recent weeks.

Just the UAE alone sold about 60 million barrels of crude from within the Persian Gulf in recent weeks. Data shows vessel traffic through the Strait of Hormuz has reached new highs since the signing of the Memorandum of Understanding and continues to rise.

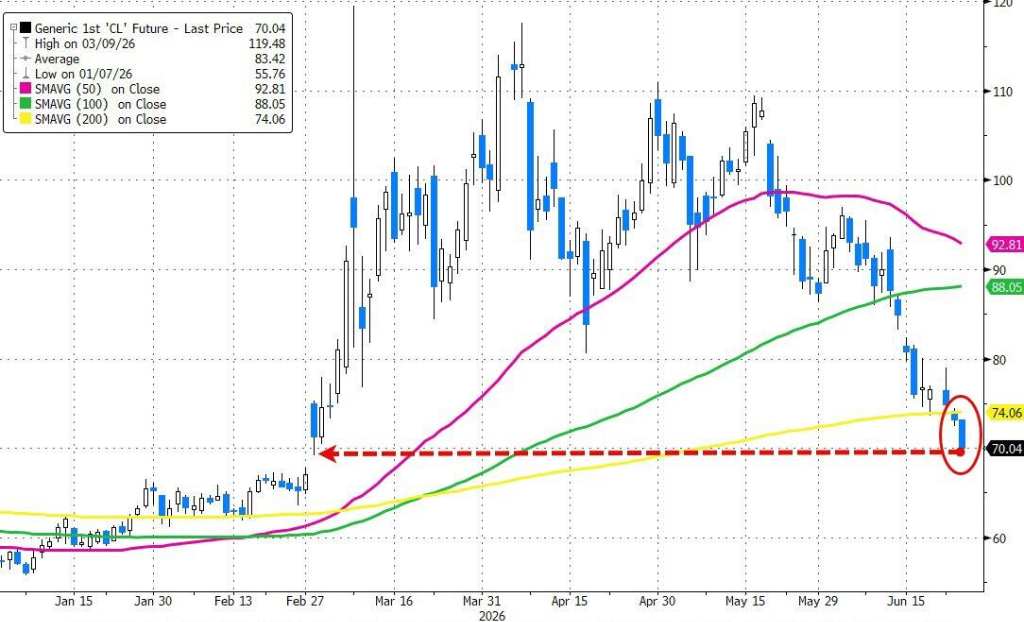

The spot crude market also softened, with premiums for regional crudes relative to benchmarks from the North Sea to West Africa rapidly declining. WTI crude futures broke below $70, touching near pre-war lows, with a daily drop of 4.5%.

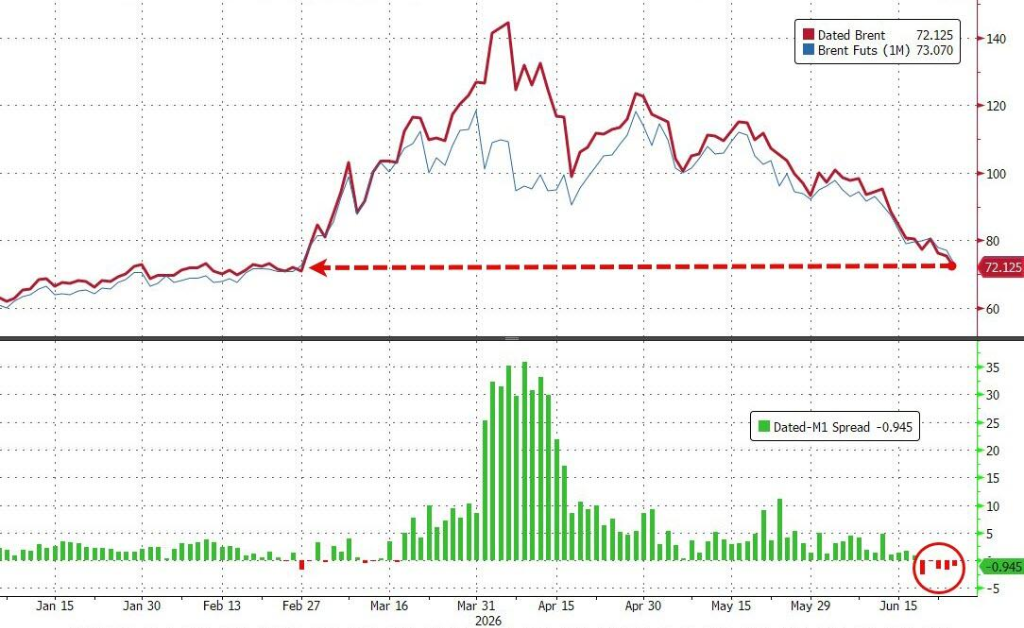

Brent crude has largely erased all the geopolitical risk premium accumulated since the outbreak of the Iran war.

On the news front, Trump posted on social media on the 24th, stating Iran had informed the U.S. it would not impose any transit fees, insurance fees, or other charges on vessels passing through the Strait of Hormuz. However, he also threatened that negotiations would terminate immediately if this information was false.

He also revealed the U.S. would unfreeze some Iranian funds for purchasing U.S. agricultural products, but no funds have been unfrozen yet. He told reporters after meeting with Senate Republicans:

I see oil just fell below $70, who would have thought this would happen? And this is during wartime. Iran is behaving very well.

Stephen Innes, Managing Partner at SPI Asset Management, pointed out, "The oil price decline is not because the market believes geopolitical risks have disappeared, but because the improvement in physical flows has been faster than expected."

Options market data shows investors are positioning for further downside in oil, with put option volume exceeding call options. The most actively traded contracts are August and September expiry puts with strike prices between $60 and $68.

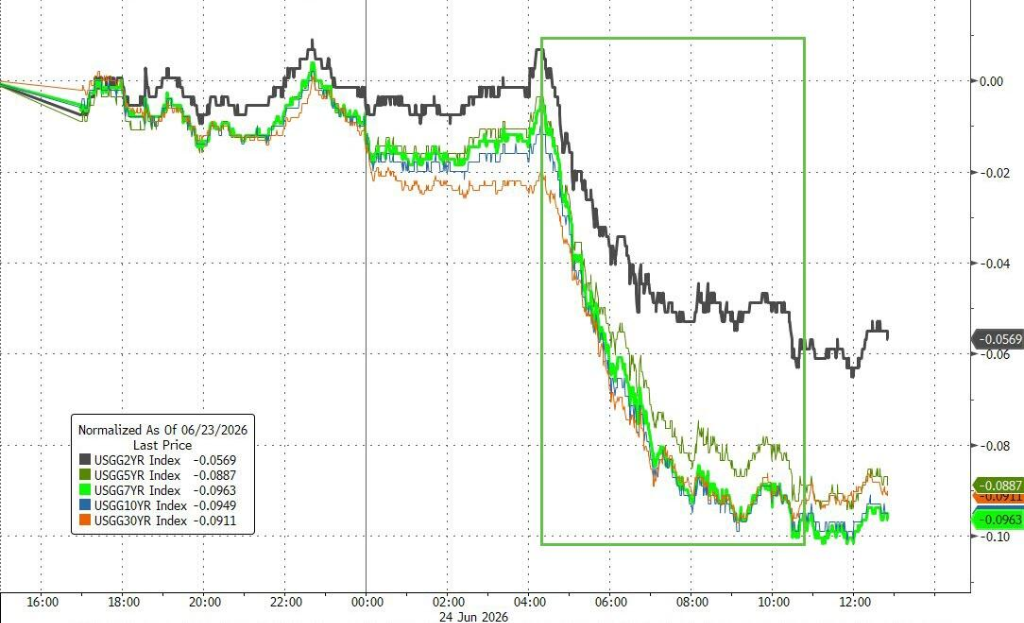

The oil price decline provided a clear boost to the bond market. The 10-year U.S. Treasury yield fell 9 basis points to 4.40%, and the 30-year yield touched 4.85%, its lowest level since April 8th.

The PCE price index release on Thursday will be the next key node. Forecasters expect the May data to show acceleration on both a monthly and yearly basis, providing a new reference for the Federal Reserve's policy direction.

Goldman Sachs Chief Economist Jan Hatzius reiterated that his baseline forecast remains for no rate hike, citing that a lasting peace in the Middle East would create a more moderate inflation environment than the Fed currently expects.

The logic chain for gold's pressure is clear: cooling geopolitical tensions reduce safe-haven demand, rising Fed rate hike expectations support a stronger dollar, and a stronger dollar directly depresses dollar-denominated precious metal assets.

The U.S. Dollar Index (DXY) continued to hit new 13-month highs.

On the policy front, U.S. Treasury Secretary Besant stated on CNBC that negotiations with Iran involved having Iran price its oil and gas exports in dollars, Venezuela is returning to the dollar system, and Russia is expected to return to dollar settlements after the Russia-Ukraine conflict ends. He characterized these developments as part of a broader reshaping of the dollar's global dominance.

Besant also predicted U.S. GDP growth could return to 3% within the year. The strong dollar narrative thus gained policy endorsement, further suppressing gold's attractiveness.

Amid the strong dollar, Bitcoin plunged over 5.3%, once breaking below the $60,000 mark during the session.

Persistent weakness in tech stocks on Wednesday left the S&P 500 essentially flat, with the Nasdaq Composite falling 0.41%, but the Dow Jones Industrial Average rising 0.36%. The Nasdaq Biotech Index and the Regional Bank Index hit record closing highs. Cerebras Systems plunged 19% during the session.

Major U.S. Stock Indices:

The S&P 500 Index closed down 7.24 points, or 0.10%, at 7358.22.

The Dow Jones Industrial Average closed up 182.06 points, or 0.35%, at 51848.90.

The Nasdaq closed down 110.403 points, or 0.43%, at 25476.636. The Nasdaq 100 Index closed down 127.216 points, or 0.43%, at 29220.056.

The Russell 2000 Index closed up 0.37% at 2986.629.

The VIX Volatility Index closed down 4.31% at 18.65, showing an M-shaped pattern since 00:00 Beijing Time.

U.S. Sector ETFs:

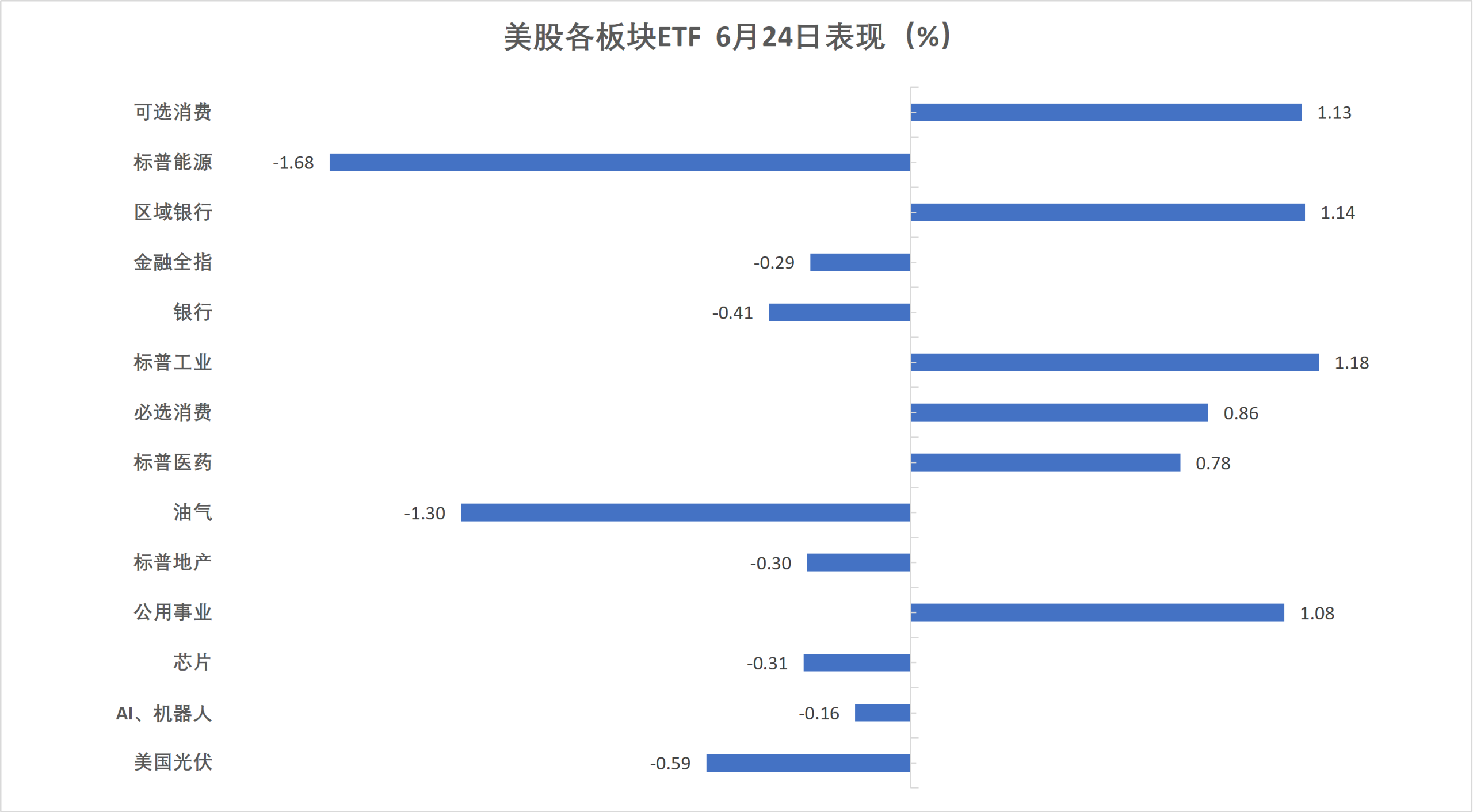

Most U.S. sector ETFs closed higher. The Global Airlines ETF rose 4.17%, the Biotech Index ETF, Regional Bank ETF, Consumer Discretionary ETF, and Utilities ETF rose up to 1.93%.

(U.S. Sector ETFs on June 24)Magnificent Seven Tech Giants:

The Wind Magnificent 7 Index fell 0.70%.

Amazon rose 0.11%, Google (Class A) fell 0.25%, Apple fell 0.38%, Nvidia fell 0.56%, Meta fell 0.78%, Tesla fell 1.61%, Microsoft fell 2.27%.

Chip Stocks:

The Philadelphia Semiconductor Index closed down 0.18% at 13458.195.

TSMC ADR rose 1.01%, AMD fell 0.15%.

Chinese Stocks:

The Nasdaq Golden Dragon China Index closed down 1.77% at 5847.87, approaching its September 20, 2024 close of 5838.26 and its August 28, 2024 close of 5399.48.

- Among popular Chinese stocks, Nio, Meituan, and Alibaba fell at least about 3%, Baidu fell 2.3%, PDD fell 1%, Tencent rose 2.4%, ASE Technology rose 3.5%.

Other Notable Stocks:

Circle fell 6.20%.

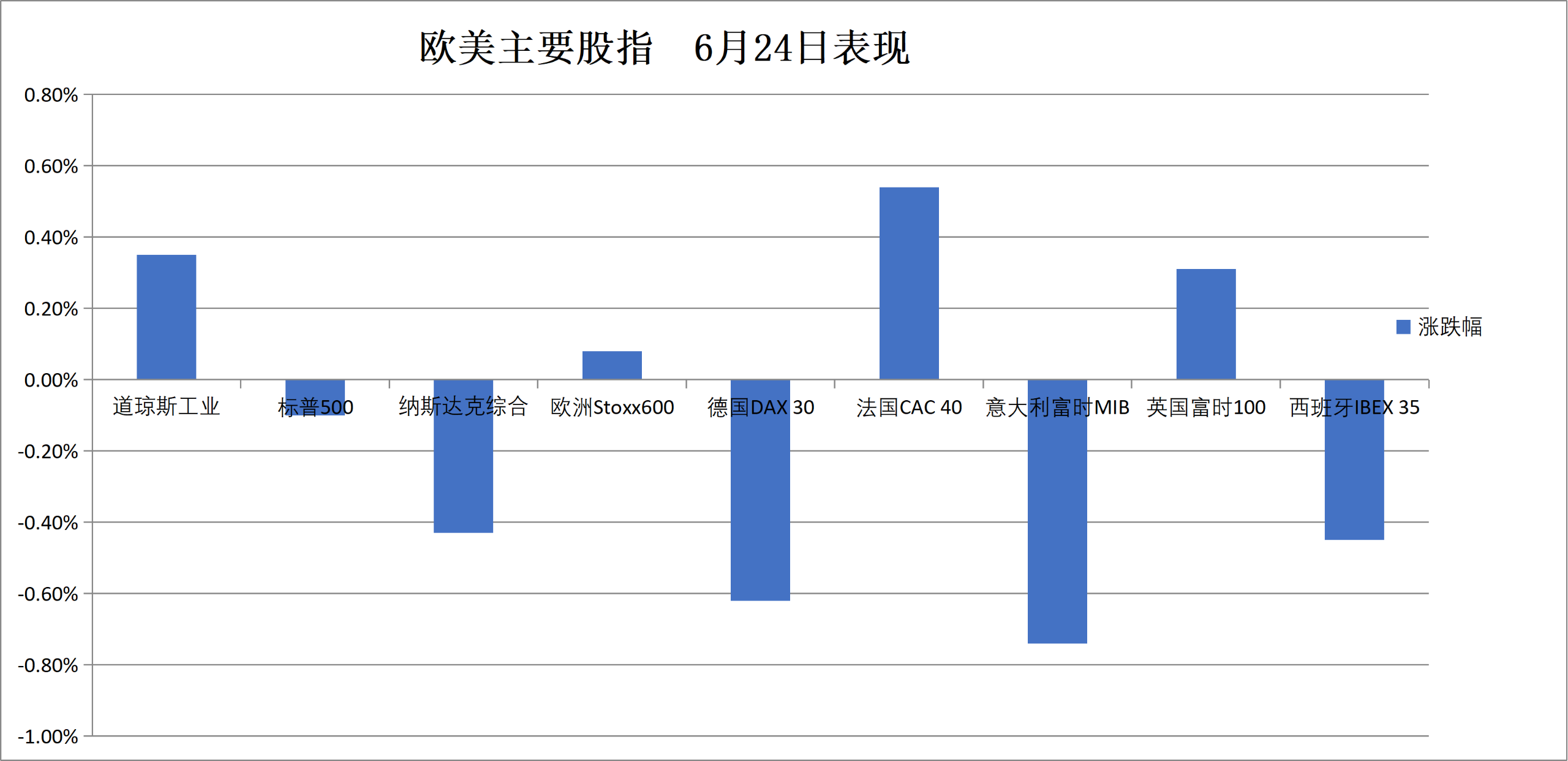

Eurozone blue-chip stocks closed down over 0.2%, with defense stock Rheinmetall (RHM) falling over 18.6%, leading declines among constituents. German stocks closed down over 0.6%, Defense ETF fell over 2.6%, UK's FTSE 250 rose over 0.7%.

Pan-European Indices:

The STOXX Europe 600 Index closed up 0.08% at 635.16.

The EURO STOXX 50 Index closed down 0.25% at 6214.70.

National Indices:

Germany's DAX 30 Index closed down 0.62% at 24740.36.

France's CAC 40 Index closed up 0.54% at 8385.49.

The UK's FTSE 100 Index closed up 0.31% at 10461.63.

(Performance of Major European and U.S. Indices on June 24)Sectors and Stocks:

Among Eurozone blue-chips, Germany's Rheinmetall (RHM) closed down 18.65%, Argenx fell 7.92%, Eni fell 3.28%, Deutsche Bank fell 2.58%, Volkswagen fell 2.44%.

Among all constituents of the STOXX Europe 600, Soitec closed down 10.888%, Hochschild Mining fell 9.03%, KGHM Polska Miedź S.A. fell 7.29%, joining RHM and Argenx as leading decliners.

Medium and long-term U.S. Treasury yields fell over 10 basis points. Eurozone sovereign bond prices rose broadly, with the 10-year Greek bond yield down about 6 bps. The UK 30-year gilt yield fell about 8 bps.

U.S. Treasuries:

At the New York close, the yield on the 10-year U.S. Treasury note fell 10.47 basis points to 4.3922%.

The 2-year yield fell 5.28 bps to 4.1456%; the 30-year yield fell 10.57 bps to 4.8396%.

(Yields on Key U.S. Treasuries)European Bonds:

At the European close, the yield on the 10-year German Bund fell 5.5 bps to 2.865%, in decline throughout the day.

The UK 10-year Gilt yield fell 7.0 bps to 4.684%. The 2-year yield fell 3.7 bps to 4.129%.

The French 10-year OAT yield fell 5.2 bps to 3.629%.

Dollar recovery, emerging market currencies fell for the fifth consecutive session.

U.S. Dollar:

At the New York close, the ICE U.S. Dollar Index rose 0.18% to 101.592, trading between 101.356 and 101.800 during the session.

The Bloomberg Dollar Index rose 0.27% to 1226.97, trading between 1223.32 and 1228.36, approaching its November 21, 2025 high of 1228.98 around 21:12.

(Bloomberg Dollar Index)Offshore Renminbi (CNH):

At the New York close, USD/CNH stood at 6.8132, up 184 pips from Tuesday's New York close, trading between 6.7910 and 6.8195 during the session.

Cryptocurrencies:

At the New York close, Bitcoin plunged over 5.3%, once breaking below $60,000 during the session. Ethereum fell 3.10%.

(Bitcoin Price)

International oil prices hit new closing lows since late February.

Crude Oil:

WTI July crude oil futures closed down $2.87, or 3.92%, at $70.34 per barrel.

(WTI Crude Oil Futures)

Brent July crude oil futures closed down $3.34, or 4.33%, at $73.74 per barrel.

- Middle East Abu Dhabi Murban crude futures fell 3.43% to $67.24 per barrel.

Natural Gas:

NYMEX July natural gas futures settled at $3.2210 per million British thermal units.

New York gold futures fell 3.2% Wednesday, spot gold lost the $4000 psychological level, silver fell over 6%. Aluminum prices returned to pre-Iran war levels on a stronger dollar and hopes for restored Gulf supply.

Gold:

At the New York close, spot gold fell 2.86% to $3999.08 per ounce, in decline throughout the day.

(Spot Gold Price)

COMEX gold futures fell 3.21% to $4016.40 per ounce, hitting a low of $3975.70 around midday in New York.

Silver:

At the New York close, spot silver fell 6.72% to $57.4512 per ounce, trading between $62.3762 and $55.6125, approaching its November 28, 2025 low of $53.3447 around 02:04.

COMEX silver futures fell 6.64% to $57.940 per ounce.

Other Metals:

At the New York close, COMEX copper futures fell 2.57% to $6.0525 per pound.

Spot platinum fell 4.25%, spot palladium fell 5.01%.

- LME copper futures closed down $284 at $13,086 per metric ton. LME tin closed down $1,473 at $49,681 per ton. LME nickel closed down $354 at $16,818 per ton. LME aluminum closed down $110 at $3,122 per ton.