Author:Zhou,ChainCatcher

In this downturn for ETH, the two largest treasury companies are already facing unrealized losses of over 50%.

SharpLink has resumed accumulation after an eight-month hiatus, recently purchasing a cumulative 39,196 ETH at an average cost of around $3,609, now facing unrealized losses exceeding $1.7 billion.

Bitmine has continued to expand its balance sheet in the same period, with holdings reaching 5.7 million ETH, accounting for approximately 4.7% of ETH's circulating supply, and unrealized losses have surpassed $11 billion.

Both companies have been included in the Russell Indexes and are also funders of the newly established Ethereum research institute, Ethlabs.

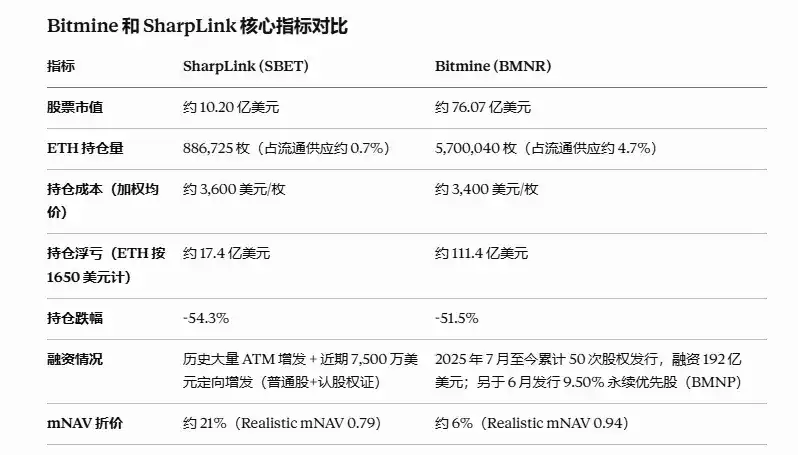

The two companies' holding costs and stock price declines are actually quite similar, yet the valuation discount the market is willing to give them shows a clear divergence. SharpLink trades at a discount of about 21% relative to its ETH net asset value, while Bitmine's discount is only about 6%, a difference of over three times.

If this ETH downturn bottoms out and investors want to gain indirect ETH exposure through stocks, which one should they choose between SharpLink and Bitmine?

The answer may not lie in who tells a better story, but in specific dimensions such as holding cost, financing capability, liquidity, and whether narratives can materialize, especially in understanding where this discount divergence comes from.

What Chips Do They Hold?

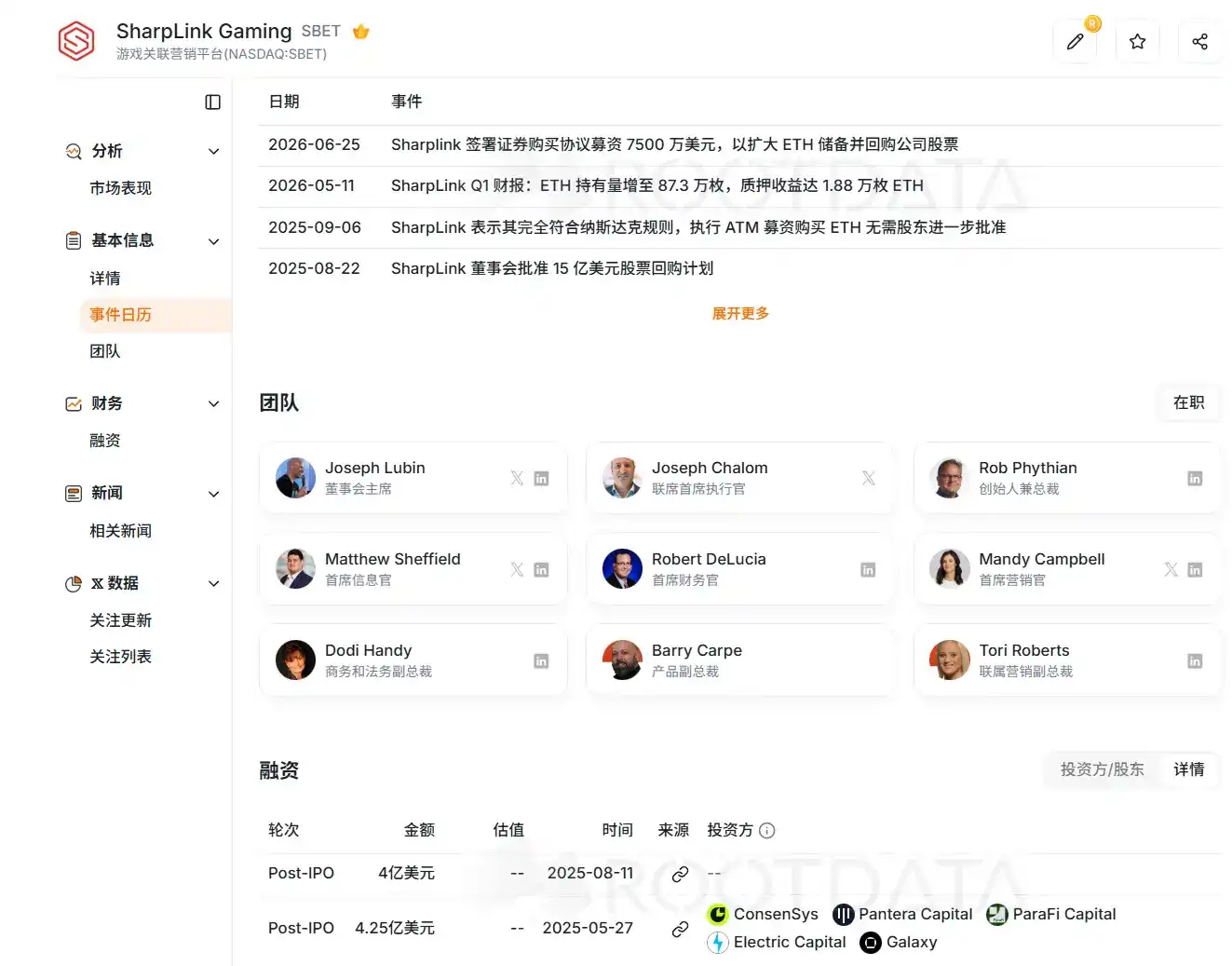

SharpLink holds a complete institutional narrative: Ethereum co-founder Joe Lubin serves as Chairman, and former BlackRock digital asset executive Joseph Chalom holds the position of Co-CEO; the company began promoting RWA tokenization collaborations last year, planning to tokenize SharpLink's own stock on Ethereum.

Image Source:RootData

Add inclusion in the Russell Index and the cumulative revenue from ETH staking. Each of these labels individually could justify a valuation premium story.

Bitmine's chips are more straightforward scale advantages. Holdings of 5.7 million ETH, and Chairman Tom Lee's own market voice and media exposure far exceed peers.

The company was included in the higher-threshold Russell 1000 Index. According to management, this will bring in hundreds or even thousands of new institutional investors, as passive funds typically hold 18% to 20% of a public company's float.

Both lists of chips look strong, but the market has ultimately only recognized the discount repair for one. What really created the gap are several more specific metrics.

Holding Costs and Stock Price Reaction

First, the most direct question: who bought ETH cheaper?

According to SharpLink's June 30 announcement, the company purchased 10,000 Ethereum at an average price of approximately $1,611, increasing total holdings to 886,725 ETH, consisting of 632,719 native ETH, 181,299 ETH redeemable via LsETH, and 72,707 ETH redeemable via weETH.

SharpLink's average holding cost is approximately $3,609 per ETH. At the current price of around $1,650, the unrealized loss is about $1.74 billion, a decline of approximately 54.3%.

As of June 28, 2026, BitMine's total Ethereum holdings reached 5,700,040 ETH, accounting for about 4.7% of Ethereum's total supply. According to on-chain data, its holding cost is approximately $3,400 per ETH, with unrealized losses of about $11 billion, a decline of approximately 51.5%.

The two companies' holding costs and percentage declines are actually very close. The gap lies in the absolute size of holdings; Bitmine is 6.4 times larger than SharpLink, and the absolute value of unrealized losses is correspondingly magnified by over 6 times.

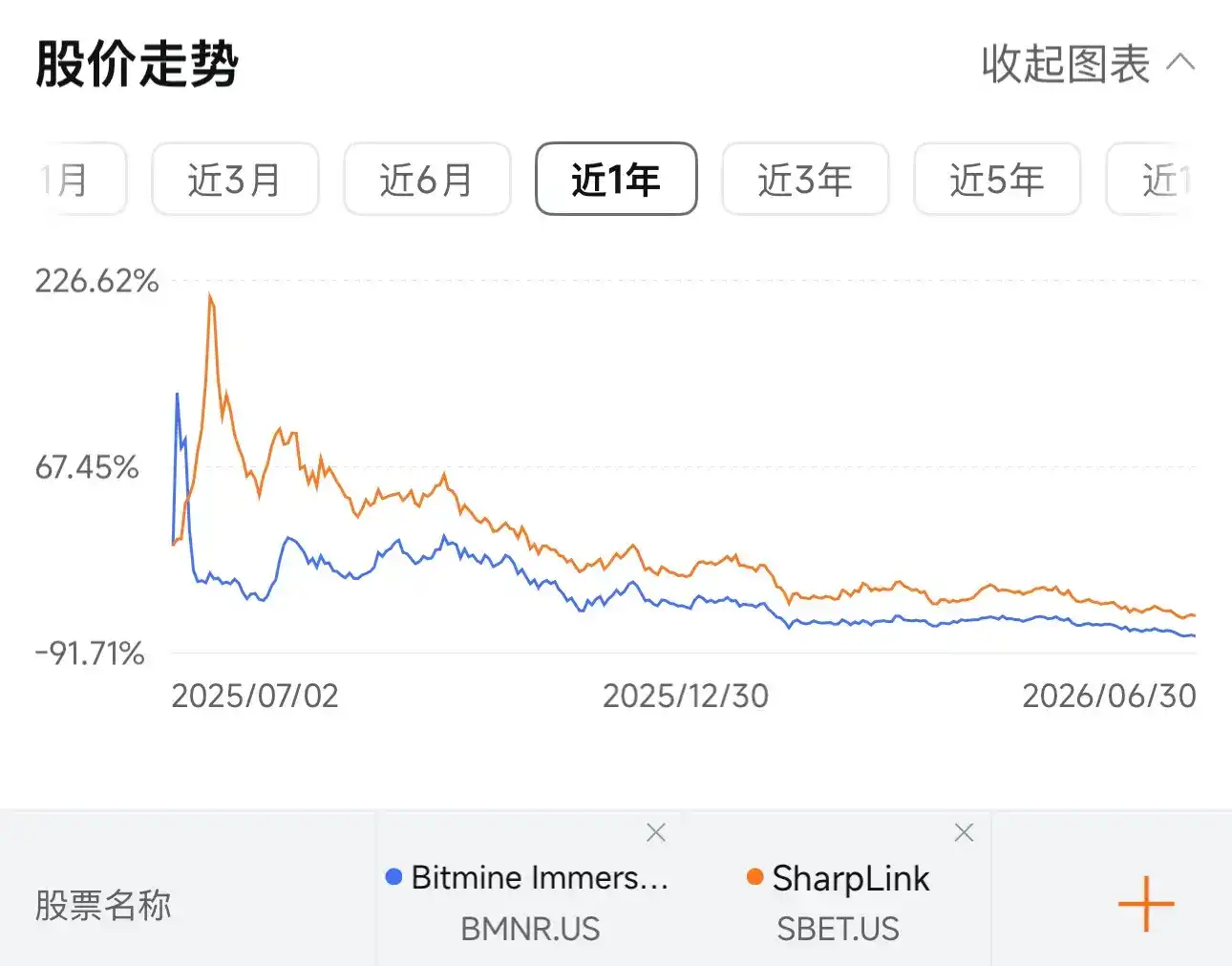

At the stock price level, the trends of the two are also highly similar, both experiencing a sharp initial surge post-IPO, followed by a continuous decline, and are currently consolidating at low levels.

As of the close on July 1st, SharpLink's stock price has fallen from a high of $124 to around $5, a drawdown of about 96%. Bitmine has fallen from a high of $160 to around $14, a drawdown of about 91%. In terms of market cap, SharpLink is approximately $1.02 billion, and Bitmine is about $7.6 billion.

Financing Capability and Liquidity

SharpLink's financing history has essentially been continuous small-scale offerings. The company has primarily relied on ATM offerings to raise funds for gradually purchasing ETH. This method has a slow fundraising pace and causes gradual dilution.

The funds for resuming accumulation mainly come from a $75 million private placement completed at the end of last month, issuing 1,001.34 million shares of common stock and an equal number of warrants, with funds explicitly for working capital, continued ETH accumulation, and share repurchases.

Besides financing to buy tokens, SharpLink also enhances returns through staking. Since initiating its ETH treasury strategy, the company's cumulative staking reward income has reached 22,102 ETH.

In contrast, Bitmine's financing pace has been much more aggressive. According to a 10x Research report, Bitmine raised a cumulative $19.2 billion through 50 equity offerings between July 2025 and May 2026, all used to purchase approximately 5.54 million ETH.

Last month, the company began to emulate the approach of the largest bitcoin treasury company, Strategy, by issuing preferred share products. Its Class A Perpetual Preferred Shares, BMNP, have been approved for listing on the New York Stock Exchange. The board has approved a cash dividend of $0.1056 per share, to be paid on July 10 to shareholders of record as of June 30.

It's worth noting that inclusion in the Russell Indexes has to some extent enhanced both companies' financing capabilities. SharpLink is included in the Russell 3000, while Bitmine is included in the higher-threshold Russell 1000.

BitMine Chairman Tom Lee stated that many actively managed funds only buy stocks that are Russell 1000 constituents, and typically 20% to 25% of a single stock's market cap is held by passive index funds or ETFs.

Thus, the inflow of passive funds from index inclusion directly increases stock trading depth and buying power. For DAT companies that need continuous equity offerings for financing, this effectively broadens their financing channels.

However, the disparity in financing capability is ultimately reflected in the mNAV. According to the latest data tracked by DefiLlama, SharpLink currently trades at a discount of about 21% relative to its ETH net asset value, while Bitmine's discount is only about 6%.

A deeper discount can further depress the stock price when issuing new shares, creating a negative cycle. SharpLink's eight-month pause in accumulation was largely stuck in this cycle.

In terms of liquidity, Bitmine has long been among the most actively traded stocks in the US, with daily trading volume often reaching hundreds of millions of dollars. SharpLink's average daily trading volume is an order of magnitude smaller.

For investors wanting to execute a discount trading strategy, liquidity directly determines entry and exit costs. Bid-ask spreads and slippage can materially erode theoretical discount gains. Bitmine clearly has the advantage here.

However, this advantage is not without cost. According to 10x Research calculations, Bitmine's overall loss over the past year is approximately $10.1 billion. This figure includes not only unrealized losses from ETH price declines but also another layer of loss: investors who bought BMNR stock at prices representing a premium to mNAV in the past have paid a cumulative premium of about $4.6 billion.

That is to say, investors buying Bitmine stock bear an additional layer of risk compared to simply holding ETH: they not only bear the risk of token price decline but also the risk of the stock price falling from premium to discount. SharpLink, which has long traded at a discount, conversely bears less of this additional loss.

RWA and Ecosystem Narrative Fulfillment Capability

Regarding the recently highlighted stock tokenization narrative, SharpLink actually announced a plan in September 2025, partnering with Superstate to tokenize SBET stock on Ethereum via its Opening Bell platform, aiming to become the first publicly listed company to natively issue stock on Ethereum.

In October this year, Co-CEO Joseph Chalom mentioned in an interview that the company plans to launch a compliant tokenized version in the near future, prioritizing Ethereum over Solana as the underlying infrastructure.

However, to date, this plan remains at the expression-of-intent stage, with no actual on-chain transactions or revenue seen. The company and Superstate previously stated that how tokenized stocks would trade on decentralized exchanges requires additional regulatory approvals.

Bitmine takes a different path on ecosystem narratives, hedging single-asset exposure through so-called "moonshot" equity holdings, including indirect exposure to OpenAI and equity investments in Beast Industries. Such investments, while not forming stable cash flow contributions in the short term, primarily provide an additional layer of imagination for the market.

Additionally, both companies jointly fund the newly established Ethereum research institute, Ethlabs. The establishment of this institute coincides with the Ethereum Foundation cutting about 40% of its 2026 budget and eliminating 54 positions, with former core development coordinator Trent Van Epps warning that core development could face funding gaps within three to nine months.

Faced with such specific warnings about governance risks, SharpLink Co-CEO Joseph Chalom stated that Ethlabs would complement the Ethereum Foundation but acknowledged some "overlap" and that "the most intense talent" would be concentrated at Ethlabs. Bitmine Chairman Tom Lee directly stated the possibility of a crisis was zero and that funding was already in place.

Overall, whether it's RWA tokenization or Ethlabs, they are currently more suitable to be positioned as industry-level long-term narrative support rather than hard businesses already converted into revenue or valuation. On this front, the two companies are essentially on the same starting line.

Conclusion

If focusing solely on trade execution during this bottoming-out phase, Bitmine is a more convenient entry. The market is willing to price it closer to its net asset value, and its liquidity is better, meaning lower transaction friction and more certain entry/exit costs—these are tangible advantages.

However, if looking at longer-term holding, Bitmine's soft spots are not hard to see. The perpetual preferred shares layered into its capital structure represent a fixed cost that has already begun to be paid.

In comparison, SharpLink's capital structure is simpler, and its current stock price already reflects more pessimistic expectations. Investors buying now do not need to pay for past premiums.

Looking ahead at a few scenarios: If ETH continues to decline, both companies' unrealized losses will expand simultaneously. Bitmine, due to its larger holdings, will see faster growth in absolute losses. The valuation advantage the market currently gives it may then narrow, which would truly test its financing flywheel for the first time.

If ETH stabilizes and rebounds, SharpLink, starting from a lower base, theoretically has greater room for valuation repair. Bitmine, however, would first need to digest the high valuation bubble accumulated in the past before seeing a repair rally.

What these two companies expose are actually two risk distributions of the same model. SharpLink's fragility is written in its stock price and liquidity; Bitmine's fragility is hidden in its capital structure and the valuation bubble accumulated in the past.

However, this is not a binary either-or choice. The answer depends on which type of risk you care about more.