Over the past six weeks, Strategy's two core securities have experienced a significant crisis of confidence. The MSTR stock price fell below $87, hitting a new low since February 2024, down over 50% from its peak. STRC plummeted from near its par value to a historic low of $74 last Thursday, a 26% discount to its $100 par value.

Public discourse surrounding this global largest corporate Bitcoin holder has shifted from its previous long-termist narrative to widespread questioning of the sustainability of its financing model.

Just as market concerns intensified, Strategy yesterday launched a Digital Credit Capital Framework, formalizing what was previously a one-time Bitcoin sale for emergency purposes into an institutionalized capital management tool.

How the Pressure Mounted Step by Step

The earliest hidden trigger of this crisis dates back to May 15th. Strategy repurchased $1.5 billion of convertible bonds maturing in 2029 at an approximately 8% discount. This transaction utilized dollar reserves that were supposed to be earmarked specifically for preferred stock dividends and debt interest payments, slashing the company's cash coverage capacity from the promised 24 months to about 6 months.

In the last week of May, Strategy sold Bitcoin for the first time since 2022, offloading 32 BTC to demonstrate the company's ability to support dividends by liquidating assets. However, this signal was interpreted negatively by the market. For a company whose core narrative has long been "never selling Bitcoin," even a small-scale sale subtly conveyed that its funding chain was beginning to tighten.

Subsequently, the company's shareholder meeting approved a plan to change STRC's dividends to twice a month, and dollar reserves also recovered to over $1 billion. Last week, Strategy sold over 12.66 million shares of MSTR through a common stock ATM offering, raising approximately $1.15 billion net. The secondary market is still digesting the new shares.

Meanwhile, the company's Bitcoin purchasing pace noticeably slowed. During the fundraising in the previous two weeks, about half was used to buy Bitcoin; in the third week, the purchase size drastically shrank, with most funds retained to pay STRC dividends.

On June 26th, STRC fell to its historic low of $74. Concurrent data showed that STRC's 90-day correlation coefficient with Bitcoin rose to nearly 0.70, the highest level since the product's launch in July 2025.

The Framework Passes Costs Down the Capital Structure

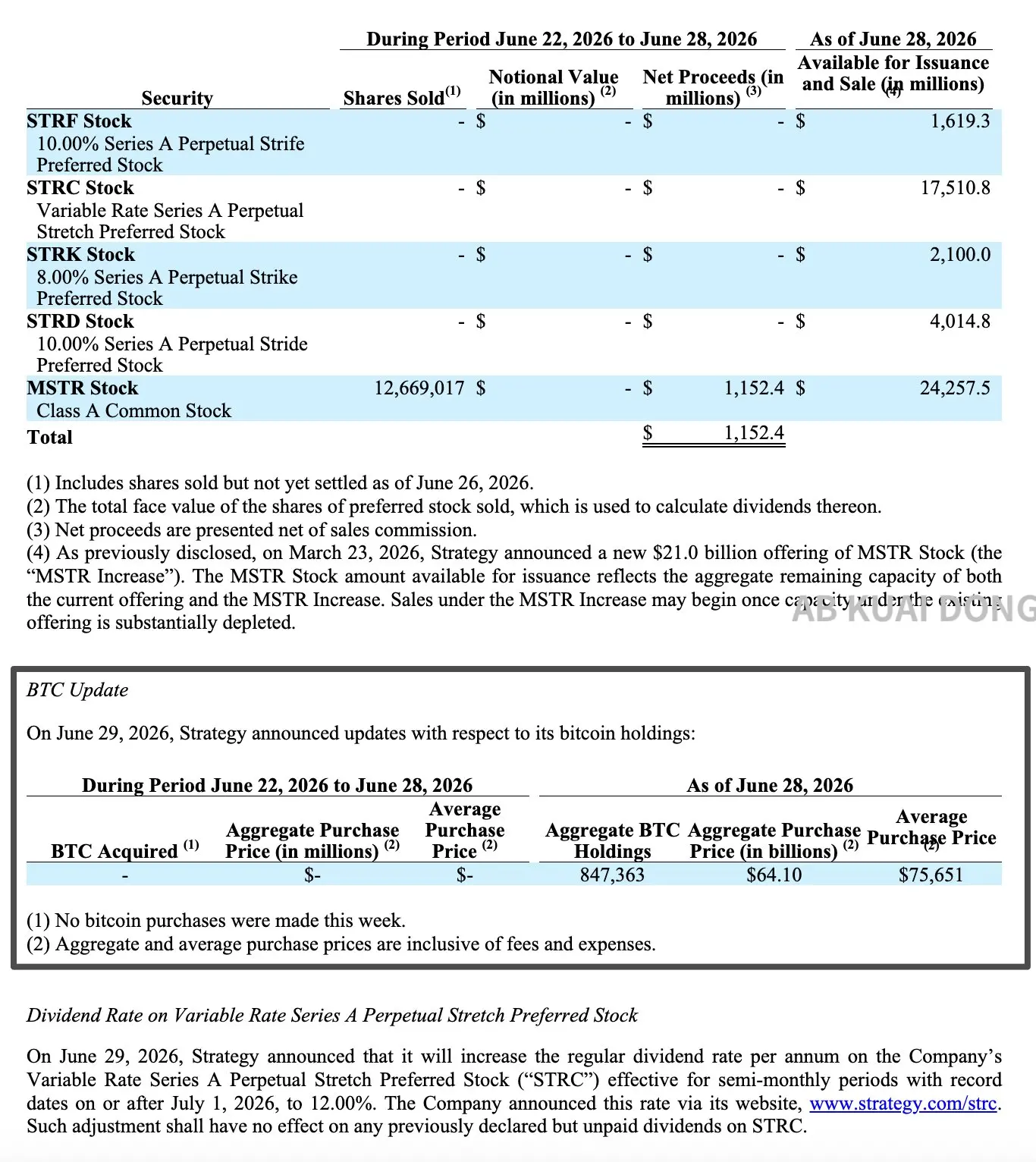

On June 29th, Strategy filed an 8-K form, introducing the Digital Credit Capital Framework. This framework includes hard coverage requirements for dollar reserves, a dynamic evaluation mechanism for STRC dividends, a total of $2 billion in repurchase authorization, and a BTC liquidation plan of up to $1.25 billion.

The emergence of the Digital Credit Capital Framework essentially channels the pressure accumulated over the past six weeks down the company's capital structure step by step.

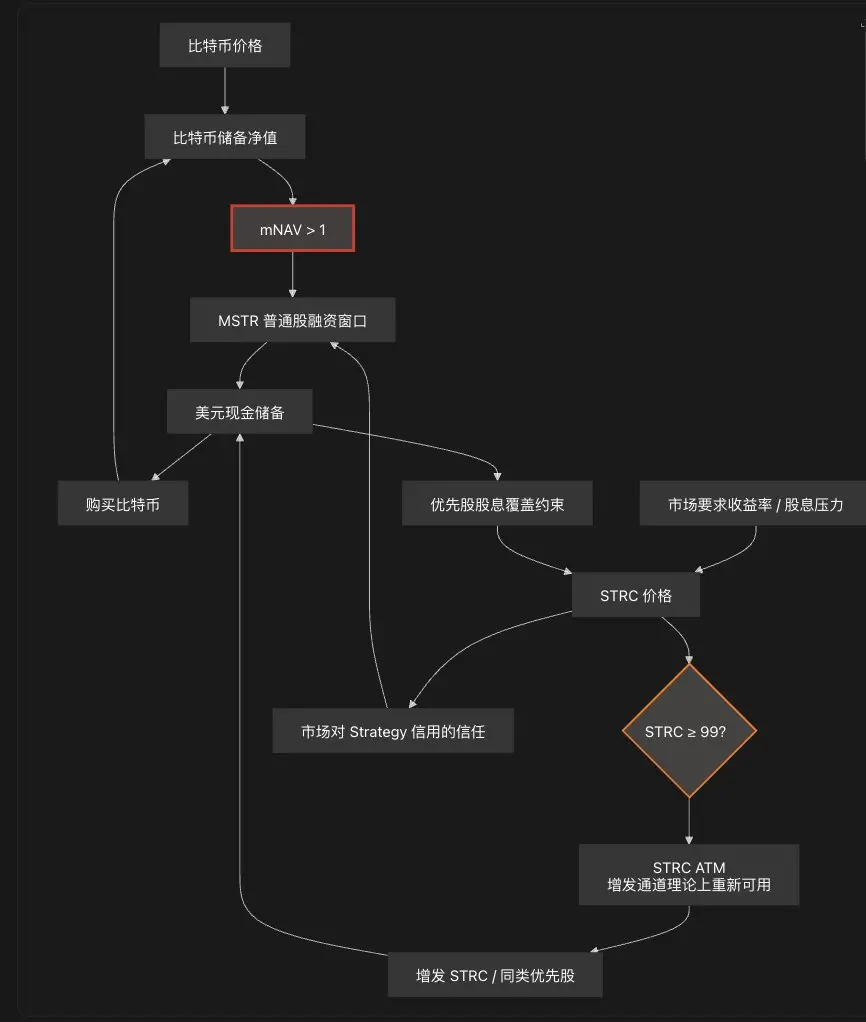

Delphi Digital's analysis noted that when Bitcoin appreciates, the cost is borne by common shareholders paying preferred stock dividends. Once the mNAV falls below 1x, this transmission channel fails, forcing the company to turn to reserves and selling Bitcoin. Strategy is currently in this stage.

Image Source: X user @bitfish

The first wave of costs is borne by common shareholders. The entire $1.15 billion raised from last week's ATM offering was transferred into reserves, meaning common shareholders are already footing the bill for the preferred stock's solvency at the cost of equity dilution.

The second step is to establish hard rules for dollar reserves. The framework stipulates that this cash reserve can only be used to pay preferred stock dividends and debt interest. Management must maintain a size sufficient to cover at least the next 12 months of expected expenditures. As of June 28th, the company's reserve balance was $2.55 billion. Based on annualized dividend and interest expenses of approximately $1.76 billion, the coverage period is about 17.4 months.

The third step is to raise STRC's annualized dividend yield from 11.5% to 12%, effective July 1st. The company also stated that future dividend yields will be assessed monthly on a comprehensive basis and will not be increased solely because STRC trades below par value. This arrangement attempts both to maintain the preferred stock's attractiveness and avoid excessive future cash flow pressure.

The fourth step, and the one that elicited the strongest market reaction, is that Bitcoin itself is formally incorporated into the capital management toolkit. The Board authorized a BTC liquidation plan, allowing the sale of Bitcoin to raise up to $1.25 billion to replenish dollar reserves, pay preferred stock dividends and interest expenses, or fund the repurchase plan. If all uses—paying dividends/interest, repurchasing preferred and common stock—are counted, the theoretical liquidation scale could exceed $1.25 billion, with any excess requiring further Board approval.

It's worth noting that Zach Pandl, Head of Research at Grayscale Research, recently stated that, rather than raising STRC's dividend yield by 50 basis points, it would be better to directly sell over $3 billion worth of Bitcoin to more thoroughly fulfill cash payment obligations and restore market confidence. This view aligns with the company's new framework, indicating that the market has long recognized the company has few options left.

Faced with the three options of repurchasing STRC, selling Bitcoin, or cutting dividends, Strategy rejected the last one. The two $1 billion repurchase authorizations and the Bitcoin sale plan were simultaneously activated, and the dividend was not only not cut but raised by 50 basis points.

In the short term, the rate hike helps pull STRC back from deep discount to near par value. But in the long run, a higher dividend rate means future cash flow pressure hasn't truly eased, and Bitcoin has officially transformed from a long-term asset to be only bought and never sold into a capital management tool that can be liquidated under specific conditions.

The Market Remains Half-Convinced, Half-Skeptical

On the day the framework was announced, MSTR closed up 12.6%, and STRC rose 12.2% in sync, rebounding to $83.67, both marking the largest single-day gains recently. However, the STRC price still has about a 16% discount, with a considerable distance from the company's target range of $99 to $100.

Some supportive voices for Strategy view this as a relatively pragmatic crisis management move. Dollar reserve coverage has significantly improved from its previous strained state, and the introduction of repurchase tools provides an expectation of price support for the preferred stock. Benchmark Equity Research reiterated its Buy rating, maintaining a $570 price target. Based on MSTR's Monday closing price of $92.68, this target implies about 515% upside potential.

Analyst Mark Palmer pointed out in a report that the framework formally grants management permission to operate the capital machine in reverse when market conditions require, including repurchasing common and perpetual preferred stock, liquidating Bitcoin to fulfill obligations, and suspending common stock issuance when the stock price no longer trades at a premium to net asset value. He believes this means Strategy has become an active manager on both ends of the capital structure, which is a significant positive for shareholders.

But skeptical voices are equally clear. Crypto KOL @MengLayer pointed out that institutionalizing Bitcoin sales from a one-time emergency move not only weakens the narrative tension but, more directly, poses the problem that the current Bitcoin price is already below the company's average holding cost of about $75,700. Selling assets below cost to maintain the credit structure in this range is, in itself, a difficult operation, hardly an easy path.

Ripple CEO Brad Garlinghouse has previously stated that financial engineering itself does not create long-term value; an asset's long-term value ultimately stems from actual utility. He believes Strategy's model of relying on preferred stock financing to buy Bitcoin over the past year has already negatively impacted the overall crypto market.

More notably, this discussion has transcended the company level. Galaxy Digital CEO Mike Novogratz stated that the recent drop in Bitcoin price is fundamentally caused by the confidence collapse triggered by Strategy. As the world's largest corporate Bitcoin holder, Strategy's stock and preferred securities performance have become a key indicator for traders to gauge risk across the entire Bitcoin market.

Finally

Following the framework release, the market experienced a short-term rebound, but formally including Bitcoin as a capital management option has brought the previously implied tension to the surface.

The flip side of market sentiment is also worth noting. For the week ending June 26th, U.S. spot Bitcoin ETFs saw a net outflow of $1.79 billion, marking the second-largest single-week net outflow on record, with net outflow weeks extending to seven consecutive weeks. Global non-mining publicly traded companies' net Bitcoin purchases last week were only $14.65 million, an 83% decrease month-over-month.

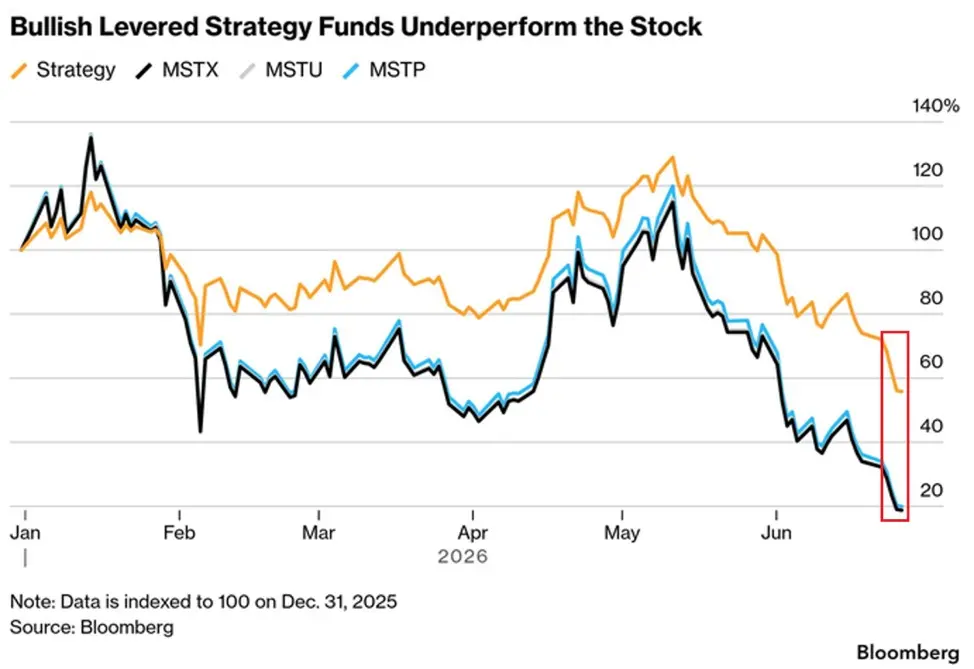

Meanwhile, the leveraged MicroStrategy ETFs (both long and short) launched in 2024 have each fallen over 90% since inception. Despite billions of dollars in inflows earlier, the leverage effect is magnifying losses dramatically.

On one side, incremental buying from institutional channels like ETFs and public companies has clearly dried up; on the other, retail leverage exposure is being repeatedly crushed.

This new framework may alleviate liquidity and credit issues to some extent, giving Strategy more maneuvering room during Bitcoin's downturn. But whether STRC can truly return near par value ultimately depends on whether the market believes the company can sustainably cover these dividends without further dilution or Bitcoin liquidation. A rebound in Bitcoin price would make this task easier.