President Donald Trump has signed an executive order pushing US financial regulators and requesting action from the Federal Reserve to review whether fintech and crypto-linked firms should get broader access to core payment infrastructure. For Ripple, which has been seeking a Fed master account tied to its RLUSD stablecoin strategy, the order moves a long-running industry fight closer to the center of Washington’s financial policy agenda.

The May 19 order, titled “Integrating Financial Technology Innovation into Regulatory Frameworks,” frames the issue as one of competition and modernization. “The Federal Government must update regulations to allow integration of digital assets and innovative technology into traditional financial services and payment systems. The Federal Government must also remove overly burdensome and fragmented regulations and supervisory practices that form barriers to entry and primarily benefit incumbent financial services firms,” the order says.

The most important section for crypto firms is the part on Federal Reserve services. The order asks the Fed to evaluate the legal, regulatory and policy framework for access to Reserve Bank payment accounts and payment services by uninsured depository institutions and non-bank financial companies, including those engaged in digital assets. The Fed is requested to submit findings and recommendations within 120 days, including whether existing law allows expanded access and whether regional Reserve Banks can act independently when granting or denying applications.

What This Means For Ripple

For Ripple, the timing is notable. In July 2025, CEO Brad Garlinghouse said the company had applied for a US national bank charter, while also seeking a Fed master account that would let it access Federal Reserve payment infrastructure and hold RLUSD reserves directly with the central bank. Ripple’s charter application was confirmed by the Office of the Comptroller of the Currency, while the master account bid was positioned as part of the company’s broader stablecoin and payments strategy.

Ripple’s application is not occurring in isolation. Kraken Financial, the exchange’s Wyoming-chartered banking arm, announced in March that it had received a Federal Reserve master account, becoming the first digital asset bank in the US to gain direct access to the Fed’s payment infrastructure. Kraken said the approval followed more than five years of regulatory engagement and would allow direct connectivity to Fedwire without relying on intermediary banks.

That approval has become the template and warning sign for the rest of the sector. Kraken’s account is limited-purpose and initially granted for one year, giving it access to Fedwire and limited overnight balances, but not interest on reserves, emergency Fed lending, FedNow or ACH. Other firms seeking similar access include Ripple, Anchorage Digital and Wise.

Notably, the issue has already been tested in court. Custodia Bank, another Wyoming crypto-focused institution, applied for a master account in October 2020, sued the Fed in 2022 over delays, and saw its application denied in January 2023. In 2025 and 2026, appeals court decisions reinforced the view that Reserve Banks retain discretion to reject master account requests, a legal backdrop Trump’s order now explicitly asks the Fed to examine.

Ripple has also shown interest in a more limited route. In November, Ripple chief legal officer Stu Alderoty said the Fed’s “skinny” account concept was attractive despite restrictions, because it could still improve RLUSD reserve redeemability without granting the full benefits of a traditional master account.

The Fed had already opened that door before Trump’s order. In December, it requested public input on a special-purpose “payment account” for eligible institutions focused on payments innovation. The prototype would be distinct from a master account, would not pay interest, would not provide Fed credit, and would be subject to balance caps.

Ripple’s stablecoin push gives the master account question added weight. The company said in December that the OCC had conditionally approved Ripple National Trust Bank, a federally supervised trust bank that would manage RLUSD reserves under both NYDFS and OCC oversight.

Overall, Trump’s order does not grant Ripple a master account. It does, however, force the policy question into a formal timeline: whether firms building crypto payment and stablecoin infrastructure should remain dependent on bank intermediaries, or gain direct, risk-limited access to the sovereign rails beneath dollar settlement.

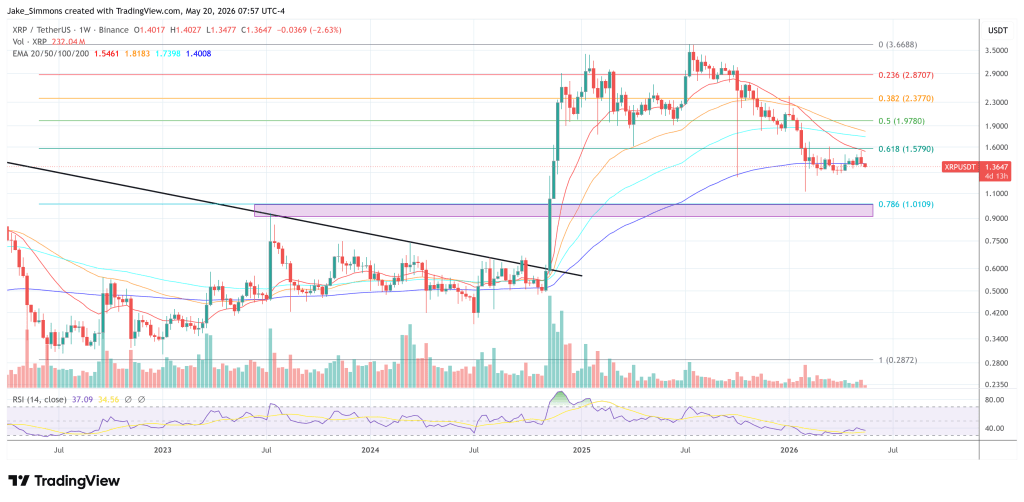

At press time, XRP traded at $1.3647.