Автор Виталик Бутерин, основатель Ethereum

Компиляция | Odaily Planet Daily Цинь Сяофэн (@QinXiaofeng 888 )

Особая благодарность Владимиру Новаковски, разработчикам Curve и всем, кто предоставил отзывы и рецензии к этой статье.

Предположим, у вас есть ценовой индекс T, который представляет собой некий ценовой индекс, выраженный в ETH. Например, T может быть ценой USD/ETH (т.е. обратной величиной ETH/USD), или CPI/ETH (т.е. CPI/USD * USD/ETH), или любым другим товарным индексом, или даже более экзотическим индексом (например, средней арендной платой в городе). Вы хотите предоставить пользователям доступ к риску (экспозиции) по T.

Проще говоря, ваша цель — создать синтетический актив, отслеживающий T, в экосистеме, где только ETH является «бездоверительным» активом (или можно расширить до других бездоверительных активов), без зависимости от централизованного эмитента. Единственная зависимость от доверия — оракул, но оракулы могут быть минимально доверительными, в отличие от эмитента.

Если рассматривать T как цену USD/ETH, то эта проблема по сути аналогична «алгоритмическим стейблкоинам». Но, по сути, это бессрочные фьючерсы.

Все методы, пытающиеся предоставить такую функциональность, сталкиваются с фундаментальной проблемой: вся система может держать только ETH, а сумма её активов и обязательств, выраженная в T, должна быть равна нулю. Поэтому на каждого пользователя, имеющего позитивную позицию по T, должен быть другой пользователь с такой же величиной негативной позиции по T. Что, если T вырастет слишком высоко, и держатели отрицательного T «обанкротятся»?

В традиционных алгоритмических стейблкоинах эта проблема решается с помощью принудительных ликвидаций.

Например, предположим, что цена ETH составляет 2500 долларов, и у пользователя есть позиция (1 ETH, -2000 долларов). Если цена ETH упадёт до 2000 долларов (на самом деле, для запаса безопасности, она срабатывает чуть выше), система должна иметь возможность «принудительно ликвидировать» этого пользователя: позволить любому другому лицу внести 2000 долларов и получить базовый 1 ETH, чтобы вся система не оказалась в затруднительном положении из-за недостаточно обеспеченного долга в 2000 долларов.

Проблема зависимости от ликвидаций заключается в том, что ликвидации зависят от оракулов в реальном времени. Вам нужен оракул, который может предоставлять обязательные значения цены ETH/USD и делать это в реальном времени.

Оракулы в реальном времени трудно сделать безопасными. Вы можете полагаться только на ограниченное количество участников, которые автоматически отслеживают сигналы в реальном времени. Вы не можете использовать любые механизмы с регрессом. Вы также не можете использовать наиболее эффективную на сегодня технологию для создания безопасных и дешевых оракулов: рынок прогнозов перед безопасным, но дорогим оракулом, используя дорогой оракул только в случае серьезных разногласий.

В этой статье предлагается перевернутый подход, который может позволить синтетическим активам полагаться только на «медленные» оракулы: мы полностью удаляем концепцию ликвидации и меняем «базовый строительный блок» системы с долга на опционы. На этой основе вы можете построить актив, отслеживающий индекс, как структуру более высокого уровня, или вообще не делать этого, позволяя пользователям самостоятельно ребалансировать. Разделение этих двух механизмов обеспечивает большую стабильность и гибкость.

Синтетические опционы

Мы определяем два актива: P и N.

Параметры включают: (i) код T, (ii) страйк-цену S, (iii) дату экспирации M.

В любой момент можно сгенерировать пару (P, N), разделив 1 ETH. Точно так же вы можете в любой момент объединить P и N, чтобы получить обратно 1 ETH.

Во время M вызывается оракул для определения значения T. Обозначим это значение как x. После определения оракулом:

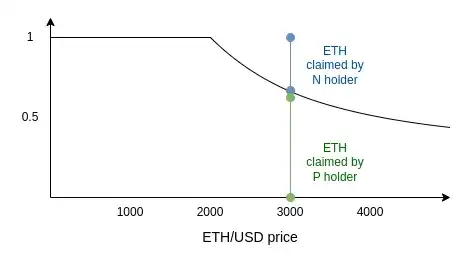

- P получает

min(1, S / x)ETH - N получает

max(0, 1 - S / x)ETH

Обратите внимание: P + N = 1. Следовательно, возможность ликвидации отсутствует.

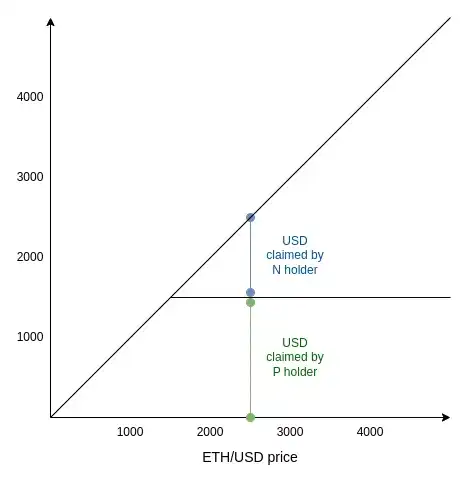

Также, для удобства понимания, вот тот же график, выраженный в долларах:

Интересная особенность этого дизайна в том, что он «по сути» является рынком прогнозов, и такие рынки уже существуют и торгуются много лет. См.: Скалярные рынки (Scalar Markets | Seer).

Это означает, что этот дизайн может использовать один и тот же оракул с системой прогнозных рынков, повышая безопасность.

Как использовать синтетические опционы

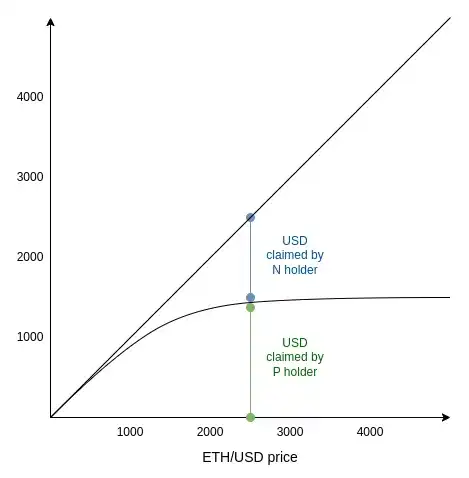

Предположим, текущая цена составляет 2500, и вы, как пользователь, хотите создать инвестиционный портфель с некоторой долларовой экспозицией. Вы покупаете немного (P 1500), что является активом P со страйк-ценой значительно ниже 2500 (здесь 1500). Достаточно ли этого?

Не совсем. Хотя текущая цена значительно выше 1500, к моменту экспирации цена все еще может упасть ниже 1500. Чем выше этот риск, тем больше стоимость (P 1500), выраженная в долларах, отклоняется от своего максимума. На самом деле, она начинает отклоняться от 1 доллара квадратично. График выглядит так:

Заметьте, это просто сглаженная версия верхней кривой. Степень сглаживания зависит как от разрыва между текущей ценой и 1500, так и от ожиданий рынка относительно будущей волатильности цены.

Чтобы понять механизм, предположим, что M наступит через две недели, а текущая цена — 1499. Сколько тогда стоит (P 1500)? Это эквивалентно вероятности того, что «через две недели цена ETH/USD будет выше 1500». ETH иногда очень волатилен, эта стоимость может быть высокой или низкой, например, 50 долларов. А если текущая цена упадет до 1399? Цена P упадет, но не до нуля, потому что цена все еще может восстановиться выше 1500 до наступления M.

Когда ETH/USD значительно ниже 1500, стоимость N стремится к нулю. Когда ETH/USD значительно выше 1500, стоимость N стремится к цена - 1500. В промежуточной области это сглаженная кривая, переходящая от одной модели к другой.

Уравнение Блэка-Шоулза — это формализованный способ (по крайней мере, когда индекс T представляет собой какую-то цену, а не более экзотический базовый актив, как погода) попытаться оценить справедливую цену (P 1500). Однако с 2008 года уравнение Блэка-Шоулза стало синонимом катастрофической хрупкости из-за чрезмерной зависимости от математических моделей — и не без оснований. Поэтому мы не должны слепо доверять конкретным деталям кривой, хотя бы потому, что не хотим вводить еще один оракул, который нужно измерять ожидаемую волатильность, асимметрию или эксцесс.

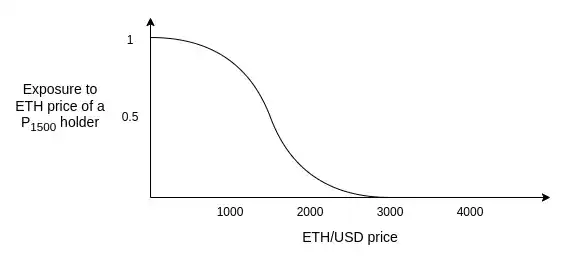

Вместо этого следует запомнить следующий график, который является производной от предыдущего. Он показывает: при текущем уровне цен, сколько ETH-экспозиции приходится на единицу (P 1500)?

Помните, что, как держатель (P 1500), ваша цель — «удерживать» доллары, не имея никакой экспозиции к ETH. Этот график подсказывает вам стратегию: безопаснее держать глубокие «в деньгах» опционы, а затем, когда цена приблизится к страйку, роллировать их в опционы с более низким страйком.

Например, вы можете следовать алгоритму: если текущая цена X, купить PS со страйком S < X/2 и экспирацией через 1-2 месяца. Если цена упадет ниже S * 1.5, то роллировать в PS' со страйком S' < X/4. Не держать до экспирации, потому что тогда вы будете подвержены риску ETH в момент определения цены оракулом.

Пусть спекулянты и маркет-мейкеры держат N и обеспечивают вам ликвидность.

Мы можем сравнить свойства синтетических активов на основе ликвидаций и на основе опционов следующим образом:

В обеих системах необходимо действовать при значительных колебаниях цен: в одной — это ликвидация протоколом, в другой — ребалансировка пользователем. Ключевое различие синтетических активов на основе опционов в том, что пользователь может выбирать, как выполнить это действие.

Ребалансировка может быть выполнена полностью автоматическим DAO на блокчейне (примечание: полностью автоматическим. Все правила устанавливаются DAO, голосование не требуется, ИИ тоже не нужен). Такой DAO будет «оберткой» для опционной системы и предоставлять «стейблкоин». Или пользователь может выбрать локальную ребалансировку, используя демон на своем устройстве.

Перенося точку принятия решения «когда {ликвидировать/ребалансировать}» из ончейн-инструмента к пользователю, мы получаем два преимущества:

- Снижение риска MEV для пользователя, поскольку транзакции не видны заранее.

- Устранение зависимости от глобального канонического оракула. Пользователям все еще нужен оракул, реагирующий быстрее, чем (например) две недели, но пользователи могут скрывать, какой оракул они используют (например, локальный прокси, опрашивающий десятки финансовых новостных сайтов, никто не знает, какие именно, и берущий медиану). Это помогает защитить систему от атак на оракулы.

Основной выбор пользователя касается времени и порогов. Если пользователь ребалансирует часто, он более уязвим для краткосрочных колебаний цены со стороны контрагента. Если пользователь ребалансирует консервативно, он несет больший квадратичный дрейф.

Я считаю, что принятие умеренного квадратичного дрейфа (например, стандартное отклонение около 1-4% годовых) — недооцененная стратегия. Эта стоимость действительно значительна, и она контр-интуитивна, что делает такой дизайн непригодным для «учетного стейблкоина» (т.е. он не может заставить получателя, отправителя или налоговый орган по приросту капитала «притворяться, что это доллар»).

Однако, если смотреть на это не с точки зрения «я хочу симулировать доллар», а с точки зрения «я хочу стабильности цен» (т.е. возможности оплачивать будущие известные расходы), это выглядит гораздо разумнее. Годовые колебания между фиатными валютами намного превышают 1-4%. Ожидаемые будущие расходы каждого человека или бизнеса в их локальной фиатной валюте также колеблются с годовой волатильностью, намного превышающей 1-4%. Кроме того, равновесная доходность алгоритмических стейблкоинов (таких как RAI) также часто колеблется примерно в таких же пределах.

Важное решение, которое необходимо принять: даже при консервативной ребалансировке, каков рыночный механизм её проведения? Очень легко потерять 2% или более в год из-за проскальзывания на нескольких этапах, и это самый большой риск, при котором вся схема может потерять конкурентоспособность.

К счастью, временные предпочтения пользователей почти всегда очень низкие. Пользователям не важно, ребалансировать сегодня, завтра или через три дня. Мы должны использовать это, чтобы спроектировать идеальную рыночную структуру, у которой проскальзывание будет намного ниже, чем у традиционных автоматических маркет-мейкеров. Ребалансировка будет больше похожа на односторонний маркет-мейкинг, чем на немедленную продажу.