8 апреля нативный протокол Hyperliquid Hyperbeat запустил Liquid Banking, самокастодиальный «банк», развернутый на HyperEVM, который объединяет депозиты в стейблкоинах, оплату картой VISA, торговлю перпетуальными контрактами и онрамп/оффрамп в фиатных валютах в одном ончейн смарт-кошельке.

Команда Hyperbeat сформировалась из первых валндаторов тестовой сети Hyperliquid, изначально в ней было всего 5 человек, стартовый капитал около 200 тыс. долларов был собран самостоятельно. Два сооснователя, Kilian Boshoff(@Fundi_Crypto) и 800.HL(@degennQuant), сохраняют низкий профиль; первый имеет образование в Stellenbosch University в Южной Африке. Компания зарегистрирована на Каймановых островах.

В августе 2025 года было завершено раунд seed-финансирования на 5,2 млн долларов, со-лидерами раунда выступили ether.fi Ventures и Electric Capital, при участии Coinbase Ventures, Maelstrom, Anchorage Digital и др. Оценка составила около 40 млн долларов.

Движок от Morpho, «банк» построен за десять месяцев

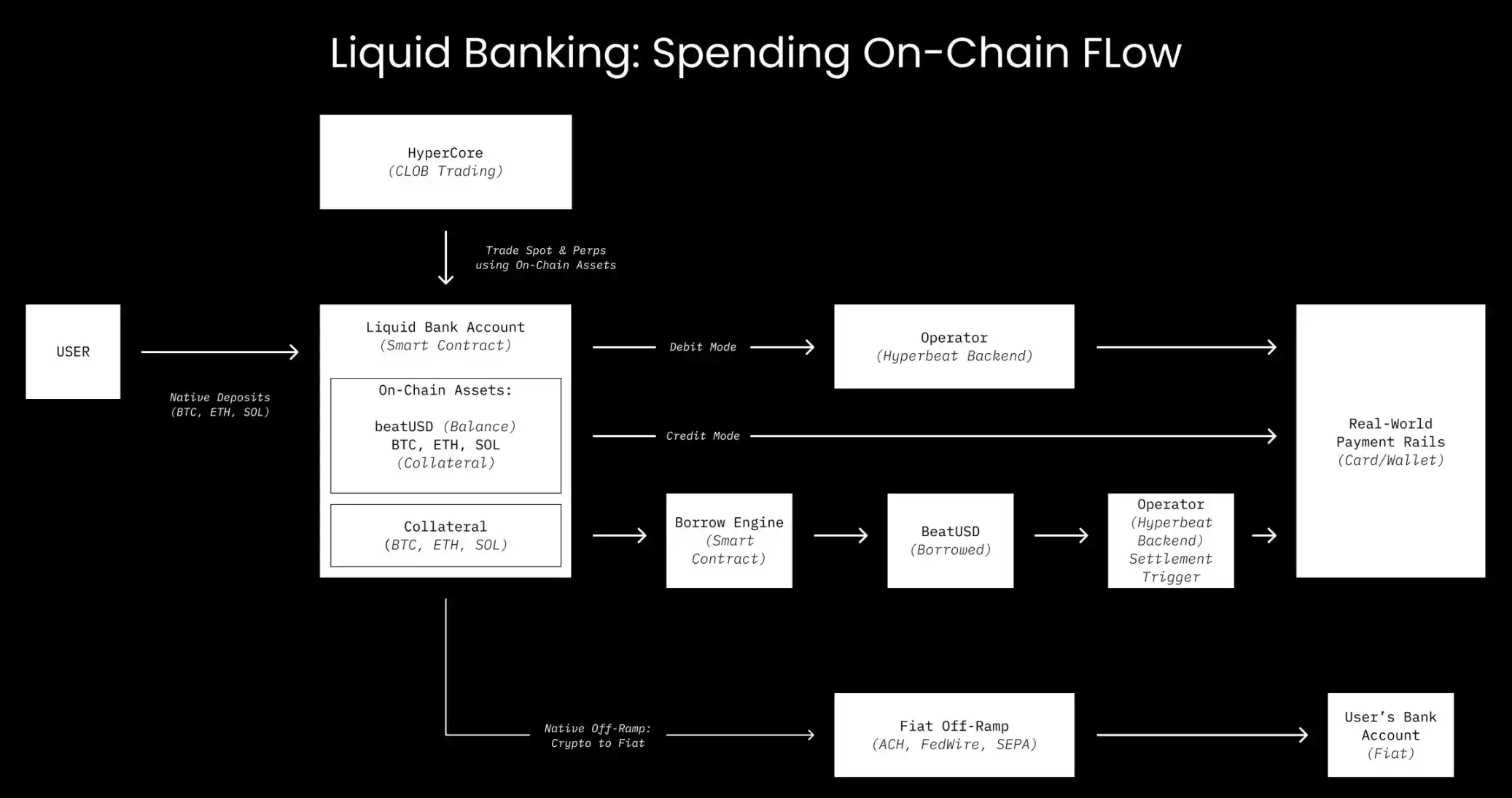

Ключевая особенность Liquid Banking — это Credit Mode.

Пользователь вносит такие активы, как BTC, ETH, HYPE, в качестве залога, а при оплате картой VISA система через рынок Morpho Blue мгновенно занимает стейблкоины для завершения платежа, в то время как залог остается в блокчейне и продолжает приносить доход. Пользователь вообще не взаимодействует с интерфейсом кредитования — сам факт оплаты картой является ончейн-займом.

Базовый движок кредитования предоставлен Morpho. Hyperbeat с помощью механизма ончейн-белых списков подключает Morpho к смарт-кошельку пользователя. В настоящее время Credit Mode работает на шести изолированных рынках, а залоги включают HYPE, UBTC, UETH, USOL и даже токен золота XAUT.

Hyperbeat не касается основной логики кредитования, Morpho не касается пользовательского интерфейса. Первый создает «банковский фронтенд», второй поставляет «кредитный движок».

Депозиты в стейблкоинах в Liquid Banking построены вокруг нативного стейблкоина beatUSD, выпущенного в партнерстве с Paxos Labs. Paxos предоставляет инфраструктуру для стейблкоинов (на базе USDG0), доход от резервов напрямую возвращается в программу вознаграждений Hyperbeat и в конечном итоге распределяется между пользователями, а не остается у эмитента.

Сторона депозитов, валютка USD+, автоматически распределяет средства пользователей между такими протоколами, как Morpho, Hypuur, Hyperlend, Felix, с годовой доходностью 3%-8%.

Доход поступает от реальных процентов по займам потребителей в Credit Mode. Чем больше потребление, тем выше доходность депозитов. Но то, насколько устойчивым будет этот цикл, зависит от объема реального потребления.

Потребление без продажи монет, но с начислением процентов с момента оплаты

Онрамп/оффрамп в фиат для Liquid Banking обеспечивается Noah, поддерживается внесение долларов (ACH, FedWire) и евро (SEPA), каждый счет привязан к уникальному IBAN.

В марте 2026 года была добавлена прямая поддержка пополнения и вывода вьетнамских донгов и малайзийских рингитов, вывод также покрывает более десяти валют, включая фунты стерлингов, дирхамы, тайские баты.

Карта VISA выпускается Third National, базовая инфраструктура предоставлена Rain, являющейся Principal Member Visa. По состоянию на начало января 2026 года ее оценка после финансирования достигла 1,95 млрд долларов, годовой объем обработки превышает 3 млрд долларов, покрытие — более ста стран.

Уровень карты — Visa Signature, с такими привилегиями, как доступ в аэропортовые залы ожидания. За операции в иностранной валюте взимается комиссия FX 1% (официальный курс Visa), годовое обслуживание бесплатное, комиссия за оплату картой отсутствует; снятие наличных в банкоматах: 1 доллар + 0,65%; лимит расходов по умолчанию — 100 тыс. долларов в месяц.

Процентная ставка по займам в Credit Mode колеблется в зависимости от утилизации рынка Morpho, но беспроцентного периода нет — каждый акт «потребления без продажи монет» начинает начислять проценты с самой секунды оплаты.

Заявление Hyperbeat «no hidden fees» относится к прозрачности стратегии получения доходов, а не к ценообразованию на комиссии карты. Процентная ставка по займам в Credit Mode динамически определяется рынком Morpho, отсутствие беспроцентного периода означает, что удобство «потребления без продажи монет» имеет реальную и немалую мгновенную стоимость.

Цена самокастодиальности — однодневный период охлаждения

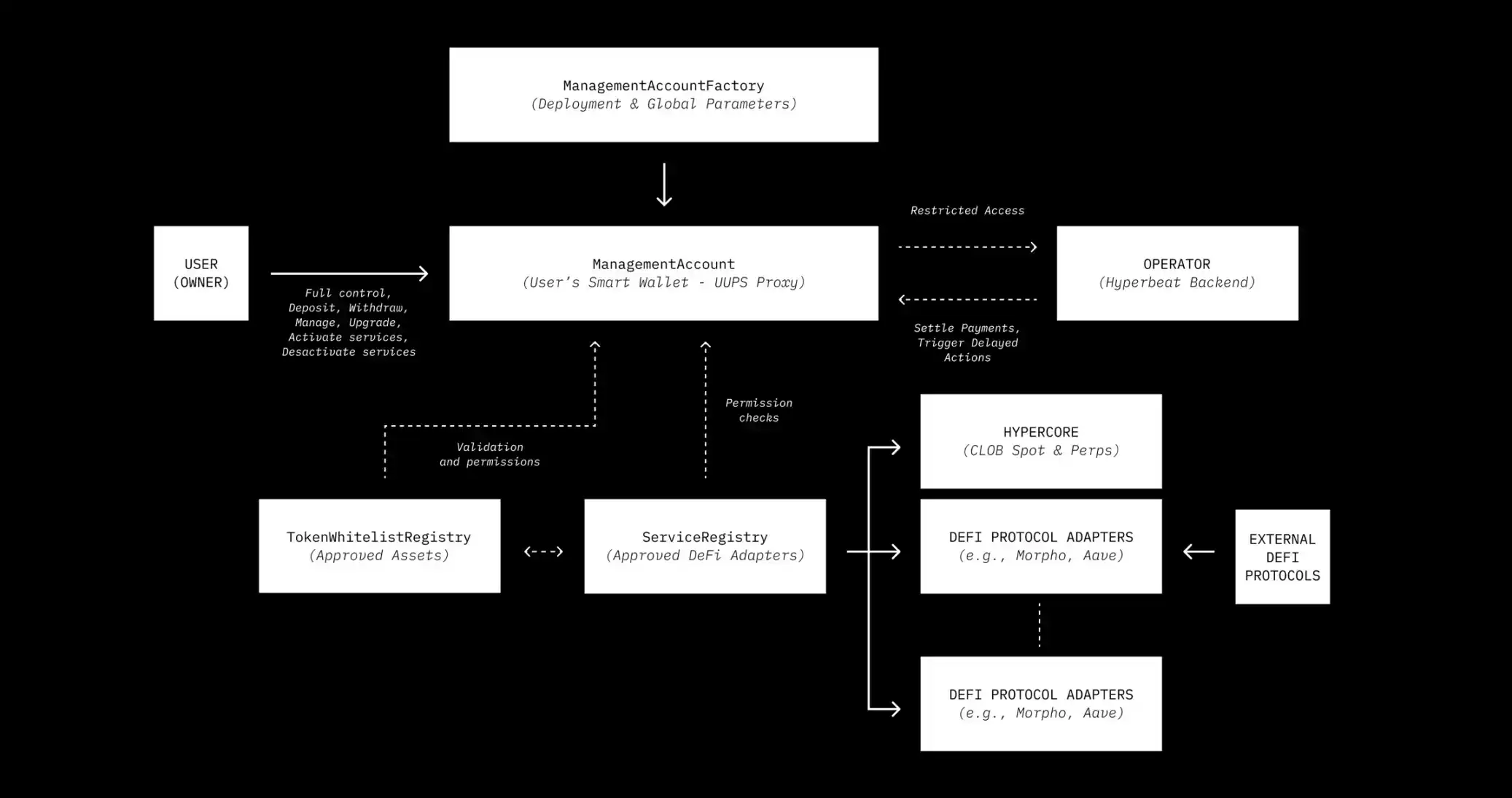

В отличие от всех централизованных крипто-карт, активы пользователя всегда остаются в его собственном управляемом смарт-кошельке ManagementAccount. Бэкенд Hyperbeat обладает лишь ограниченной ролью Operator и может выполнять расчеты только в пределах установленного пользователем лимита, не имея возможности переводить активы на неавторизованные адреса.

Но самокастодиальность должна решать одну проблему: что, если пользователь, оплатив картой, попытается быстро вывести средства? Hyperbeat внедрил механизм ончейн-временной блокировки.

Для вывода расчетных токенов требуется период охлаждения и процесс подтверждения, для вывода залога требуется одобрение Operator во избежание плохих долгов, переключение режимов также имеет задержку. Контракты прошли аудит Zellic и Nethermind, управление ключами обеспечивается Turnkey.

Эти трения — не баг, а фича. Они признают, что существует разница в скорости между ончейн-расчетами и оффейн-потреблением, и заполняют эту пропасть с помощью правил контракта, а не просьб «пожалуйста, доверьтесь нам». Но пользователь должен сам следить за коэффициентом здоровья, и ошибки в действиях не могут быть отменены службой поддержки.