Автор: Thejaswini M A

Компиляция: Chopper, Foresight News

Любой вариант по умолчанию в конечном итоге становится выбором большинства. В поведенческой экономике это известно как «эффект умолчания».

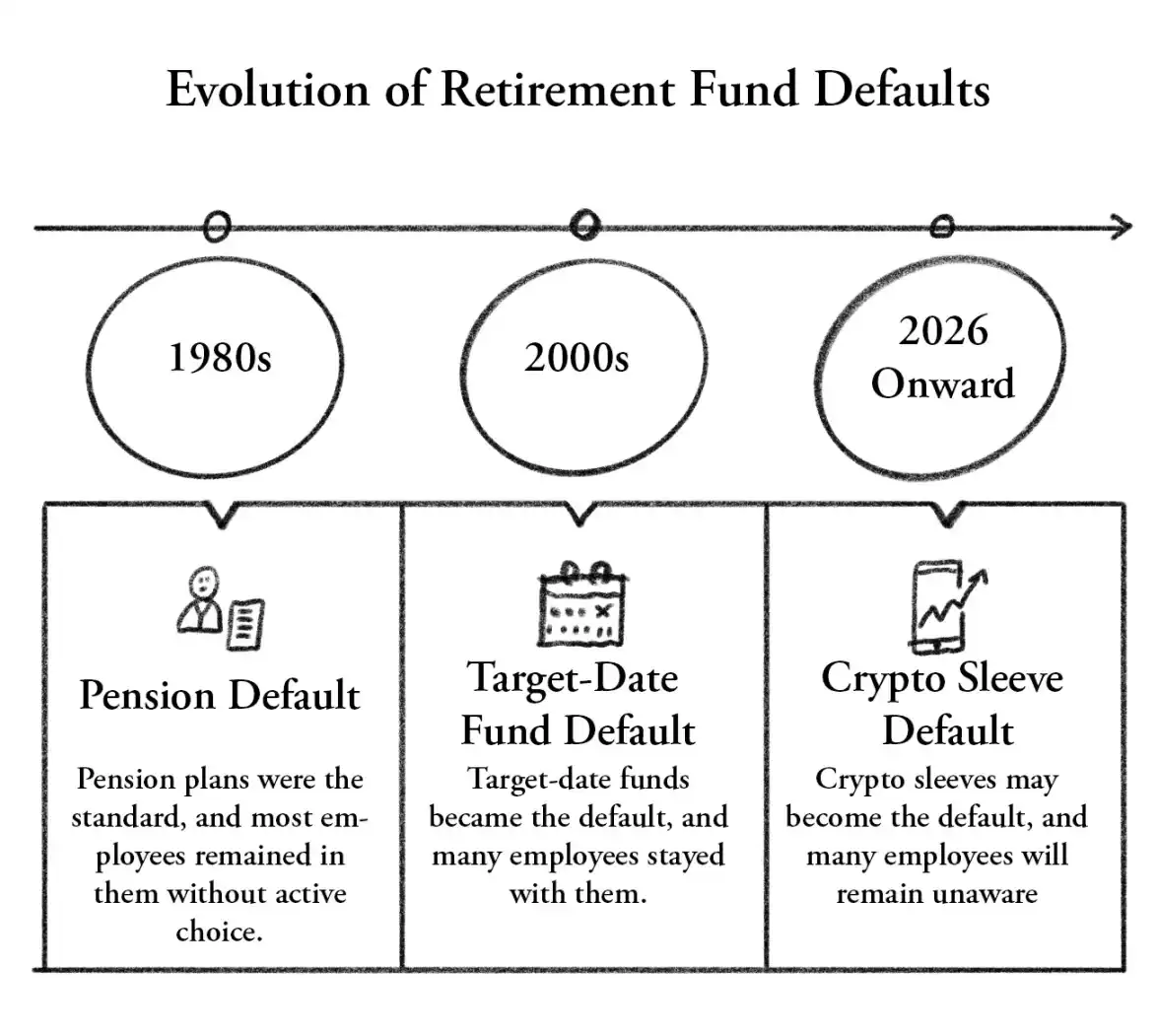

Вся история пенсионной системы США — это история вариантов по умолчанию. В 1980-х годах вариантом по умолчанию вместо традиционных пенсий стал план 401(k), который большинство сотрудников приняли по умолчанию, не до конца понимая, от чего они отказываются. В начале 2000-х годов фонды с установленной датой (target date funds) стали вариантом по умолчанию для подавляющего большинства пенсионных планов, и десятки миллионов людей оказались владельцами таких фондов, никогда сознательно их не выбирая.

Каждая смена варианта по умолчанию сопровождалась перемещением огромных сумм денег и в конечном итоге меняла способ выхода на пенсию целого поколения. Большинство затронутых людей осознавали это лишь позже, просматривая свои выписки.

В ближайшие годы родится новый вариант по умолчанию. Сейчас он еще не выглядит таковым, а скорее похож на проект правил, предложенный Министерством труда, который в настоящее время проходит 60-дневное общественное обсуждение. Он составлен осторожно, с акцентом на фидуциарные обязанности и соответствие Закону о пенсионном доходе сотрудников (ERISA). Они часто появляются как опции, постепенно распространяются и в конечном итоге становятся вариантами по умолчанию.

30 марта Министерство труда США опубликовало правило, впервые открывающее путь для криптовалют на рынок пенсионных планов 401(k) США объемом 12 триллионов долларов. Индиана уже в марте приняла закон, требующий, чтобы государственные пенсионные планы к июлю 2027 года предлагали как минимум один вариант инвестирования в криптовалюты; пенсионная система Висконсина уже владеет биткоин-ETF на 321 миллион долларов; Мичиган разместил 45 миллионов долларов в биткоин- и эфириум-ETF. Флорида и Нью-Джерси также продвигают аналогичную политику.

Давайте сначала посмотрим, как ранее криптовалюты не допускались.

Стена, преграждавшая путь криптовалютам

До появления этого правила криптовалюты не были прямо запрещены законом для планов 401(k). Реальная преграда была эффективнее запрета.

Согласно Закону о пенсионном доходе сотрудников (ERISA), регулирующему пенсионные планы, попечичи несут личную ответственность за убыточные инвестиционные решения. Ответственность несут не компания или фонд, а конкретное лицо, принявшее решение.

С 2016 года было подано более 500 исков о нарушении ERISA; с 2020 года суммы урегулирования по таким искам превысили 1 миллиард долларов. Управляющие пенсионными планами воочию видели, как их коллег судили из-за завышенных комиссий, неправильного выбора индексных фондов, проблем с категориями паев взаимных фондов. Подобные иски бесчисленны, предъявляются под неожиданными углами и нацелены непосредственно на физических лиц.

Подумайте о создаваемых этим стимулах: вы управляете пенсионным планом, покупаете биткоин, после чего его цена падает на 50%. Адвокаты истцов присылают письма, и вы три года защищаетесь в ходе доказывания.

И наоборот, если вы не добавляете биткоин, даже если он вырастет до 200 000 долларов, никто не подаст на вас в суд.

Рациональный выбор всегда один: держаться подальше от криптовалют. И почти все так и поступали.

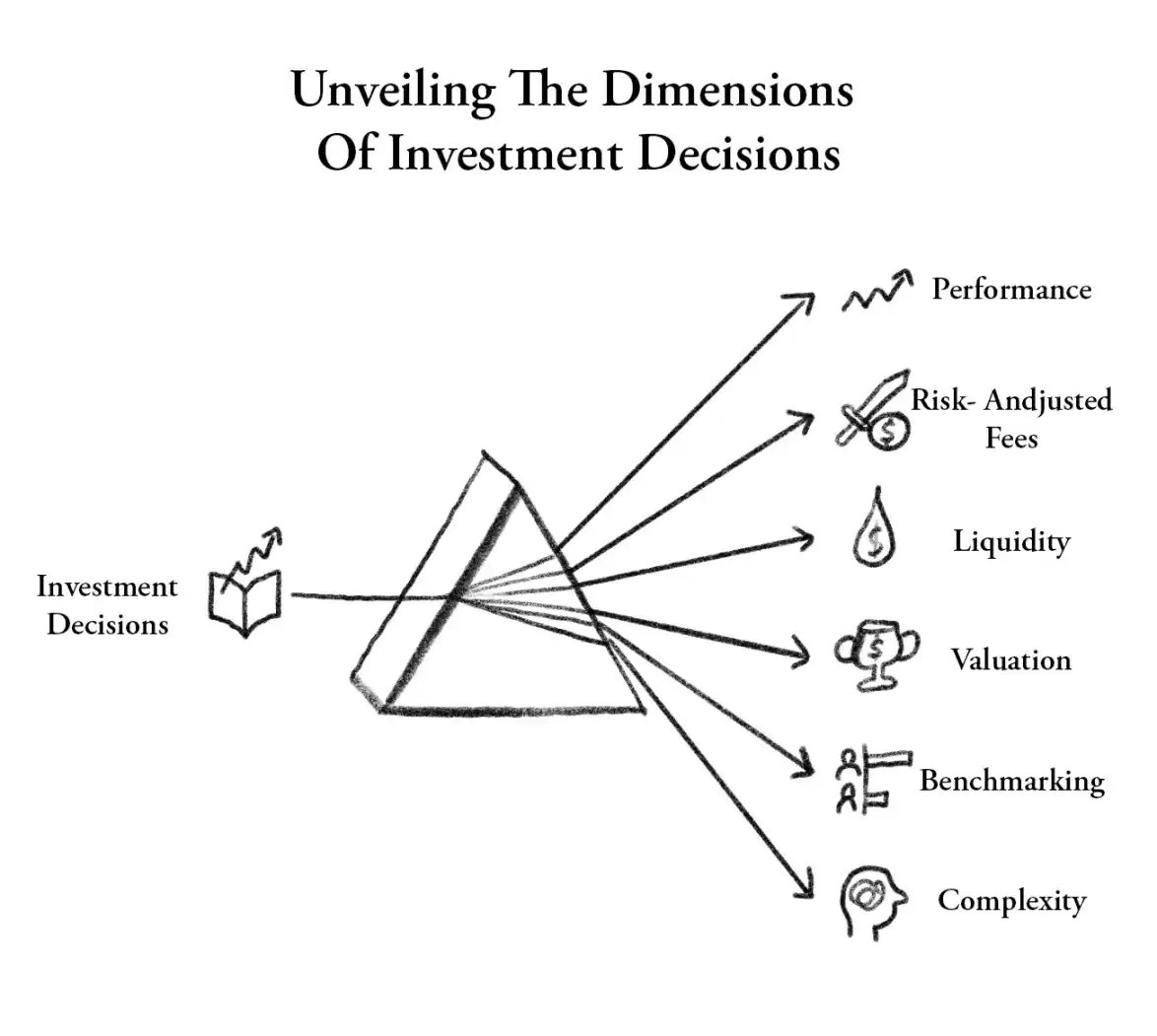

Министерство труда при администрации Байдена в 2022 году更是 четко дало понять, что попечичи должны проявлять «крайнюю осторожность» перед接触 с цифровыми активами. Теперь эти указания отозваны и заменены правилом «безопасной гавани» из шести элементов: если попечичи проведут проверку в соответствии с письменными процедурами, охватывающими шесть аспектов — результаты, комиссии, ликвидность, оценка, бенчмарк, сложность, — они будут считаться выполнившими предусмотренные ERISA обязанности по проявлению осмотрительности. Если процесс соответствует требованиям, даже при падении цены актива, они защищены от персональных судебных исков.

Не стоит воспринимать изменение правил как изменение рыночных fundamentals. Для обычного инвестора волатильность криптоактивов一如既往. Это правило действительно защищает управляющих фондами. Оно исправляет дисбаланс юридических рисков, который маргинализировал криптовалюты в течение десятилетия, и позволяет попечичам наконец-то с уверенностью сказать «да».

Механизм передачи: фонды с установленной датой

Само Министерство труда прогнозирует, что основным каналом доступа станут фонды с установленной датой. Это крайне важно для практического воздействия на обычных вкладчиков.

Большинство людей при трудоустройстве по умолчанию выбирают фонд с установленной датой. Вам нужно лишь выбрать фонд с годом, наиболее близким к предполагаемому году вашего выхода на пенсию, например, фонд 2045 года. Он автоматически adjusts соотношение акций и облигаций по мере вашего взросления, становясь более консервативным по мере приближения срока. Подавляющее большинство владельцев таких фондов никогда больше не смотрят на них вторым взглядом.

Если криптоактивы будут配置роваться через фонды с установленной датой, инвесторы не будут actively покупать биткоин. Их пенсионный инвестиционный портфель автоматически будет включать 1%–3% биткоина, управляемый профессиональными учреждениями и автоматически ребалансируемый.

Так же, как многие имеют золото в своих 401(k), даже не подозревая об этом. Золото когда-то вошло в пенсионную систему exactly так же, через тот же носитель, по той же логике, не спрашивая разрешения у настоящих владельцев этих денег.

Fidelity в 2022 году первой предприняла шаги, предложив спонсорам пенсионных планов option включить цифровые активы в инвестиционные портфели еще до того, как администрация Байдена выпустила свои указания. Тогда Fidelity允许 спонсорам планов включать инвестиции в цифровые активы в свои портфели, позволяя участникам инвестировать до 20% остатка на счете в биткоин. Всегда существовал недостаток соответствующей юридической защиты для спонсоров планов, которая позволила бы им спокойно配置ровать биткоин без персональной ответственности. В настоящее время соответствующая юридическая защита разрабатывается.

12 триллионов долларов

Объем планов 401(k) в США составляет около 12 триллионов долларов. Даже при allocation всего в 1% в цифровые активы поступит около 120 миллиардов долларов, что превышает общий объем заблокированных средств (TVL) во всем DeFi.即使只有 0.1%, это 12 миллиардов долларов, что эквивалентно规模 пяти крупнейшим биткоин-ETF.

Предыдущие волны институционального принятия криптовалют исходили от активных решений: покупатели ETF actively покупали, MicroStrategy actively держала, банки actively создавали продукты для хранения. Эти решения можно отменить: CFO может продать казначейские активы, инвесторы ETF могут погасить паи.

Канал 401(k) структурно completely иной, это то, чего отрасль ждала с момента запуска спотовых ETF. Пенсионные деньги — это пассивные деньги, они будут храниться до 30 лет. Они не будут panic продавать при обвале, на них не влияет индекс страха и жадности, им не важно, как колебались цены на нефть на прошлой неделе.

Эми Олденбург из Morgan Stanley指出, в настоящее время 80% торгов крипто-ETF приходится на самостоятельных инвесторов, а не на allocation, рекомендованные советниками. Рынок 401(k) почти полностью управляется профессиональными советниками. Новые правила Министерства труда США открывают канал, который ранее было трудно использовать по структурным причинам, потому что люди, контролирующие канал, несли чрезмерную личную ответственность и не решались открыть дверь.

Это то, что криптовалюта多年来一直 подчеркивала: настоящая волна массового принятия придет не от трейдеров или ранних последователей технологий, а когда инфраструктура систем сбережений обычных людей автоматически повернется в сторону криптовалют. Фонды с установленной датой — это и есть эта инфраструктура.

Риски и опасения

Падение торгового счета на 50% — это просто плохой квартал. Падение пенсионного счета 55-летнего учителя на 50% — это совершенно другая природа.

Биткоин в прошлых медвежьих рынках откатывался более чем на 80%, в текущем цикле — примерно на 50%, что некоторые интерпретируют как «взросление». Но потеря половины пенсионных сбережений не станет легче от того, что это назовут «прогрессом».

Джарет Сайберг из TD Cowen写道, он все еще сомневается, что попечичи будут легко действовать, пока суды не подтвердят, что положения «безопасной гавани» действительно защищают от исков. ERISA — это закон, основанный на процессах, но окончательное толкование остается за судами.

«Безопасная гавань» на бумаге может работать, но если фонд с установленной датой, содержащий криптоактивы, упадет на 40% на медвежьем рынке, вызовет первый раунд судебных исков, whether он выдержит, пока неизвестно.

Период обсуждения правил закончится 1 июня. Министерство труда может изменить правила, отозвать их или直接продвинуть к реализации. Даже если окончательная версия не изменится, от предложения правил до реального попадания на пенсионные счета предстоит пройти процессы compliance-команд, инвестиционных комитетов, интеграции систем recordkeeper, проверок попечичей, на что уйдут месяцы, а更 вероятно, годы.

Жесткий指令 Индианы с крайним сроком в июле 2027 года — это жесткое указание, whereas федеральные правила — лишь мягкое разрешение, и их темпы реализации будут совершенно разными.

В 1980-х годах акции вошли на пенсионные счета через взаимные фонды; в начале 2000-х международные акции вошли через фонды с установленной датой; затем последовали REITs, inflation-protected bonds, товарные ресурсы. Их приход не был обусловлен активным требованием пенсионных вкладчиков.

Криптовалюты сейчас находятся в этой переломной точке. Спотовые ETF — это продукт, новые правила Министерства труда — это нормативное сопровождение, Fidelity,嘉信, Morgan Stanley — это каналы дистрибуции, Закон «CLARITY»写入писание классификации криптоактивов в статутное право, предоставляя попечичам правовую основу для проведения проверок осмотрительность.

Все части головоломки на месте, не хватает только последней.

Если有一天 в будущем某位управляющий пенсионным планом добавит биткоин в фонд с установленной датой. Биткоин рухнет на 60%,某位пенсионер потеряет крупные сбережения,律师подаст иск.

В тот момент единственным важным вопросом будет: признает ли судья, что «безопасная гавань» защищает человека, принявшего это решение.

На данный момент никто не знает ответа. Министерство труда считает, что да, TD Cowen считает, что для выяснения могут потребоваться годы.

До рассмотрения и вынесения решения по первому делу всех управляющих пенсионными планами США просят поверить в листок бумаги, никогда не испытанный в суде.