Начало недели после снижения ставок оказалось неудачным.

Биткоин откатился до отметки около 85 600 долларов, Ethereum потерял уровень в 3000 долларов; акции, связанные с криптовалютой, также оказались под давлением: Strategy и Circle упали почти на 7% за день, Coinbase снизилась более чем на 5%, а майнинговые компании CLSK, HUT и WULF потеряли даже более 10%.

От ожиданий повышения ставок Банком Японии до неопределенности дальнейшего пути снижения ставок ФРС и системного снижения рисков со стороны долгосрочных держателей, майнеров и маркет-мейкеров — причины этого падения носят скорее макроэкономический характер.

Повышение ставок в Японии: недооцененная первая «костяшка домино»

Повышение ставок в Японии является крупнейшим фактором текущего падения, возможно, это последнее крупное событие в финансовой отрасли в этом году.

Исторические данные показывают, что когда Япония повышает ставки, держателям биткоина приходится несладко.

После предыдущих трех повышений ставок Банком Японии биткоин падал на 20–30% в течение 4–6 недель. Как подробно подсчитал аналитик Quinten: биткоин упал примерно на 27% после повышения ставок в Японии в марте 2024 года, на 30% после повышения в июле и снова на 30% после повышения в январе 2025 года.

А на этот раз это первое повышение ставок с января 2025 года, и уровень ставок может достичь 30-летнего максимума. В настоящее время прогнозы рынка показывают, что вероятность повышения ставок по иене на 25 базисных пунктов составляет 97%, что практически решенный вопрос; заседание в этот день, вероятно, является лишь формальностью, и рынок уже заранее отреагировал падением.

Аналитик Hanzo заявил, что игнорирование крипторынком动向 Банка Японии является серьезной ошибкой. Он указал, что Япония, как крупнейший зарубежный держатель казначейских облигаций США (с объемом более 1,1 трлн долларов), своими действиями может повлиять на глобальное предложение долларов, доходность гособлигаций и такие рисковые активы, как биткоин.

Несколько пользователей Twitter, фокусирующихся на макроанализе, также отметили, что иена является вторым по величине игроком на валютном рынке после доллара, и ее влияние на рынки капитала может быть даже больше, чем у евро; многолетний бычий рынок акций США во многом связан с иеновым кэрри-трейдом. В течение многих лет инвесторы брали кредиты под низкие процентные ставки в иенах для инвестиций в акции и облигации США или покупки высокодоходных активов, таких как криптовалюты. Когда японские ставки растут, эти позиции могут быть быстро закрыты, что приведет к принудительным ликвидациям и делевериджу на всех рынках.

И текущий рыночный фон таков: в то время как большинство крупных центральных банков снижают ставки, Банк Японии их повышает. Этот контраст спровоцирует закрытие кэрри-трейдов, что означает новую турбулентность на криптовалютном рынке из-за такого повышения ставок.

Что еще более важно, возможно, само по себе текущее повышение ставок в Японии не является ключевым риском, а более关键的是 сигнал, который Банк Японии подаст в отношении политических ориентиров на 2026 год. В настоящее время Банк Японии подтвердил, что с января 2026 года начнет продажу ETF-портфеля стоимостью около 550 млрд долларов. И если в 2026 году Банк Японии снова или неоднократно повысит ставки, то последуют дальнейшие повышения и ускоренные продажи облигаций, что further раскрутит иеновый кэрри-трейд, спровоцирует распродажу рисковых активов и отток иен, и может нанести持续的 удар по фондовому рынку и криптовалютам.

Но если повезет, и после этого повышения ставок Банком Японии на следующих заседаниях будет объявлена пауза в дальнейшем повышении, то после рыночного обвала может начаться период восстановления.

Неопределенность ожиданий дальнейшего снижения ставок в США

Конечно, любое падение не бывает обусловлено единственным фактором или переменной. В этот период повышения ставок Банком Японии и резкого падения биткоина также simultaneously наблюдались следующие情况: достижение пика leverage; сжатие долларовой ликвидности; экстремальные уровни позиций; влияние глобальной ликвидности и leverage и т.д.

Давайте снова обратим взгляд на США.

Первая неделя после того, как ставки были finally снижены, началась со слабости биткоина. Потому что фокус рынка сместился на вопрос: «Сколько еще раз можно будет снижать в 2026 году и не замедлится ли вынужденно темп?». А два показателя, публикуемые на этой неделе: отчет по занятости в несельскохозяйственном секторе США (NFP) и данные по CPI (индекс потребительских цен), являются одними из ключевых переменных для этого пересмотра ожиданий.

После окончания длительного shutdown правительства США, Бюро трудовой статистики (BLS) на этой неделе集中发布 данные по занятости за октябрь и ноябрь, среди которых наиболее ожидаемым является отчет по несельскохозяйственной занятости, публикуемый сегодня в 21:30. Текущие рыночные ожидания: число новых рабочих мест вне сельского хозяйства составит всего +55 тыс., что значительно ниже предыдущего значения +110 тыс.

На поверхности, это типичная структура данных, «благоприятствующая снижению ставок» », но проблема как раз в том: если занятость охлаждается слишком быстро, не забеспокоится ли ФРС о срыве экономики и не выберет ли более осторожный подход к корректировке политики? Если данные по занятости покажут «обрывное охлаждение» или структурное ухудшение, ФРС может instead выбрать выжидательную позицию, а не ускорение смягчения.

Теперь посмотрим на данные CPI. По сравнению с данными по занятости, момент, который反复 обсуждается на рынке в отношении данных CPI, публикуемых 18 декабря: дадут ли CPI ФРС повод «мне тоже нужно ускорить сокращение баланса», чтобы хеджировать ужесточение Банка Японии?

Если данные по инфляции покажут отскок или усиление ее устойчивости, ФРС, даже сохраняя позицию по снижению ставок, может ускорить сокращение баланса для изъятия ликвидности, тем самым достигнув баланса между «номинальным смягчением» и «фактическим ужесточением ликвидности».

Следующее truly определенное снижение ставок, самое раннее, произойдет не раньше окна заседания в январе 2026 года, и временной跨度 все еще довольно далека. В настоящее время Polymarket прогнозирует 78% вероятность сохранения ставок без изменений на 28 января, вероятность ожиданий снижения составляет лишь 22%, неопределенность ожиданий снижения слишком велика.

Кроме того, на этой неделе Банк Англии и Европейский центральный банк также проведут свои заседания по вопросам денежно-кредитной политики, чтобы обсудить свои монетарные позиции. В условиях, когда Япония уже первой развернулась, США колеблются, а Европа и Великобритания выжидают, глобальная monetary policy находится на高度分化 stage, где трудно достичь synergy.

Для биткоина такая «несогласованная liquidity среда» часто оказывается более разрушительной, чем явное ужесточение.

Закрытие майнинговых ферм, continued уход «старых денег»

Еще одна распространенная аналитическая точка зрения: долгосрочные держатели продолжают продавать, и на этой неделе темпы сокращения ускорились.

Прежде всего, это продажи со стороны ETF-институтов. В тот день чистый отток из спотовых биткоин-ETF составил около 350 млн долларов (примерно 4000 BTC), основными источниками оттока стали FBTC от Fidelity и GBTC/ETHE от Grayscale; что касается Ethereum ETF, совокупный чистый отток составил около 65 млн долларов (примерно 21 000 ETH).

Например,非常 интересно то, что биткоин проявляет相对 большую слабость в американские торговые часы. Данные, приведенные Bespoke Investment, говорят: «С момента начала торгов биткоин-ETF IBIT от BlackRock, доходность при удержании в послечасовое время составила 222%, но если удерживать только в течение дневных торговых часов, то убыток составил 40,5%».

Затем на уровне链上 появляются более прямые сигналы к продаже.

15 декабря чистый приток на биткоин-биржи достиг 3764 BTC (около 340 млн долларов), установив阶段性高点. Среди них仅 на одну Binance чистый приток составил 2285 BTC, что примерно в 8 раз больше, чем на предыдущем этапе, что явно указывает на行为集中ого пополнения крупными держателями и подготовки к продаже.

Кроме того, изменения позиций маркет-мейкеров также构成了重要的 фон. Например, Wintermute в период с конца ноября до начала декабря累计 перевела на торговые платформы активы на сумму более 15 млрд долларов. Хотя в период с 10 по 16 декабря ее чистые запасы BTC увеличились на 271 монету, рынок все же испытывал некоторую панику из-за ее行为 крупных переводов.

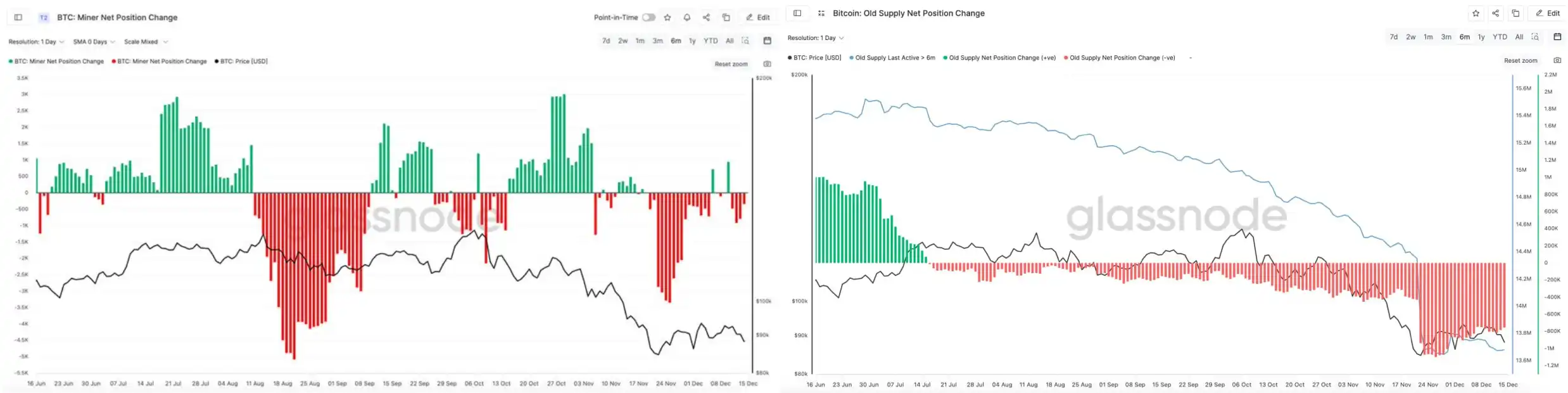

С другой стороны, продажи со стороны долгосрочных держателей и майнеров также引起了 очень большое внимание.

Платформа链上 мониторинга CheckOnChain зафиксировала смену (轮换) хэшрейта биткоина,这种现象 ранее часто совпадала с периодами давления на майнеров и сжатия ликвидности. А链上 аналитик CryptoCondom указал: «Друг спросил меня, действительно ли майнеры и OG (старички) продают свои BTC. Объективный ответ — да, можно посмотреть данные Glassnode о чистых позициях майнеров и ситуации с долгосрочными запасами BTC у OG».

Можно видеть, что данные Glassnode показывают, что продажи биткоинов OG, не трогавшими их в течение последних 6 месяцев, продолжаются уже несколько месяцев и明显 ускорились в период с конца ноября до середины февраля.

В叠加 с падением общего сетевого хэшрейта биткоина. По состоянию на 15 декабря, согласно данным F2pool, общий хэшрейт сети биткоина暂时报 988.49 EH/s, что на 17.25% ниже, чем в тот же момент на прошлой неделе.

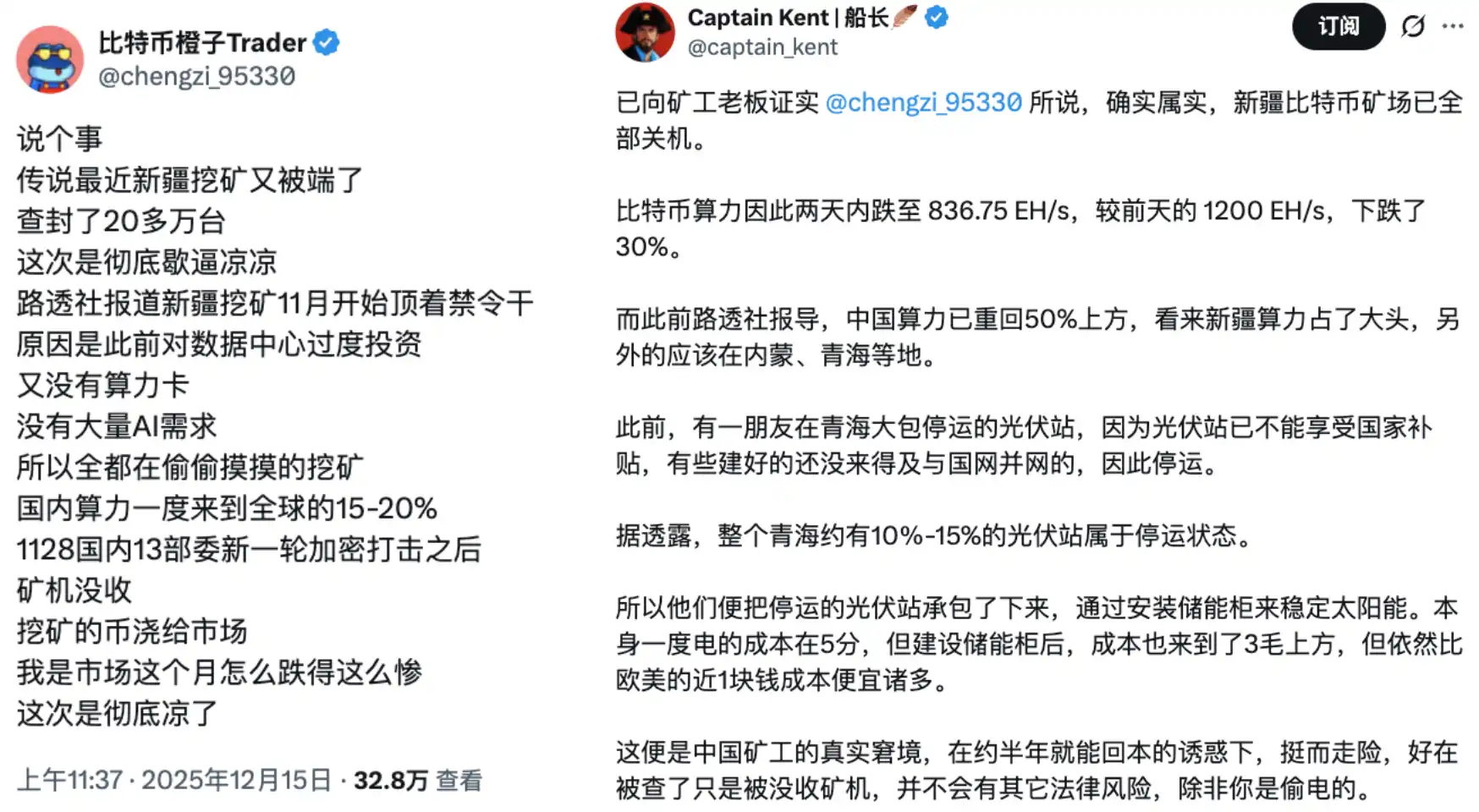

Эти данные также соответствуют текущему фону слухов о том, что «майнинговые фермы биткоина в Синьцзяне陆续 отключаются». Основатель и председатель правления Nano Labs Кун Цзяньпин также прокомментировал ситуацию с недавним падением хэшрейта биткоина: по (средним) расчетам (на одну машину) 250T (хэшрейта),近期 было отключено как минимум 400 000 биткоин-майнеров.

В целом, факторами этого раунда падения являются: Банк Японии率先转向 ужесточению, что расшатало иеновый кэрри-трейд; ФРС, завершив первое снижение ставок, не может дать четкий последующий путь, заставляя рынок主动 снижать ожидания по ликвидности на 2026 год; а на链上 уровне поведение долгосрочных держателей, майнеров и маркет-мейкеров further усилило чувствительность цены к изменениям ликвидности.