Автор оригинала: CM(X:@cmdefi)

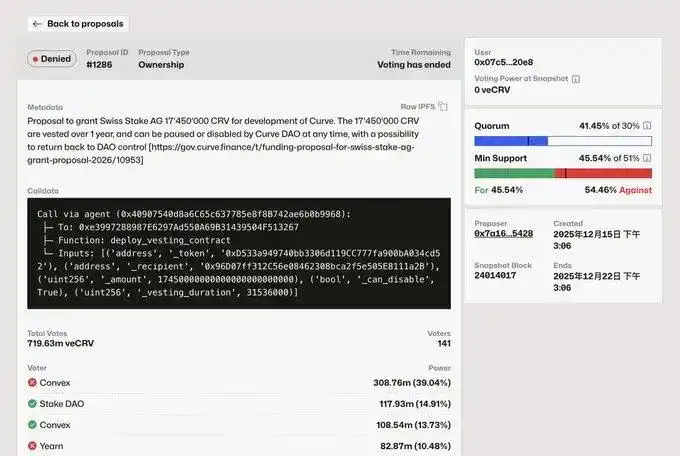

Несколько дней назад предложение о финансировании в Curve было отклонено. Оно касалось выделения 17 миллионов $CRV команде разработчиков (Swiss Stake AG) на разработку. И Convex, и Yearn проголосовали против, и их доли голосов были достаточны для влияния на окончательный результат.

С тех пор как начали обсуждаться проблемы управления в Aave, управление стало привлекать внимание рынка, и инерция «просить и получать деньги»也开始打破. За этим предложением Curve стоят два ключевых момента:

1. Часть сообщества не против выделения средств AG, но они хотят знать, как были использованы предыдущие деньги, как они будут использоваться в будущем, является ли это устойчивым, принесло ли это прибыль проекту. В то же время такая примитивная модель грантов приводит к тому, что一旦 деньги ушли, никаких ограничений нет. В будущем DAO необходимо создать Казначейство (Treasury), сделать доходы и расходы прозрачными или добавить управленческие ограничения.

2. Крупные держатели голосов veCRV не хотят размывать стоимость своих активов. Это очевидный конфликт интересов. Если проект, поддерживаемый грантом CRV, не может предсказуемо приносить выгоду veCRV, то он, скорее всего, не получит поддержки. Конечно, у Convex и Yearn также есть свои собственные интересы и амбиции, но пока не будем углубляться в эти вопросы.

Это предложение было инициировано основателем Curve Михом. AG также является одной из команд, занимающихся维护核心代码库 с 2020 года. В этой сделке о финансировании AG представила дорожную карту, которая включает продолжение развития llamalend, включая поддержку PT, LP, а также расширение ончейн-рынка форекс и crvUSD. Это выглядит стоящим делом, но стоит ли это 17 миллионов $CRV — это уже другой вопрос, особенно учитывая, что управление в Curve во многом отличается от Aave. Его власть распределена между несколькими командами с четкими позициями.

Сравним модель ve с обычными моделями управления:

Сначала вывод: большинство обычных моделей управления на данный момент по designу практически не имеют преимуществ. Конечно, если DAO достаточно зрелое, то традиционная структура также может работать хорошо, но, к сожалению, в Crypto еще нет проекта,成熟到这个层次. Например, даже признанный лидер рынка Aave столкнулся с проблемами.

Если говорить отдельно о designе модели, то у ve есть некоторые передовые черты. Во-первых, у него есть cash flow (поток доходов), за ним стоит право контроля над ликвидностью. Когда извне возникает потребность в ликвидности, это право становится объектом «взяток» (bribery). Поэтому, даже если вы не хотите долго блокировать активы, вы можете делегировать свои токены таким прокси-проектам, как Convex/Yearn, чтобы получать доход.

Таким образом, ve — это модель, где право голоса привязано к cash flow. Вероятное направление будущей эволюции — это путь «управленческого капитализма» (governance capitalism). Vetoken привязывает право голоса к «долгосрочной блокировке», что по сути отбирает тех, у кого большой объем средств, кто может позволить себе потерю ликвидности и способен вести долгосрочную игру. Таким образом, со временем управляющие из числа обычных пользователей постепенно превратятся в «капиталистическую группу».

В то же время, due to the existence of proxy layers like Convex/Yearn, многие обычные пользователи и даже лояльные пользователи, желающие получать доход без потери ликвидности и гибкости, также будут постепенно выбирать делегирование управления этим проектам.

В этом голосовании также можно увидеть некоторые признаки того, что в будущем управлением Curve, возможно, будет заправлять не Мих, а эти крупные держатели голосов. Когда возникли проблемы с управлением в Aave, некоторые предлагали идею «делегированного управления/элитного управления», которая довольно похожа на нынешнюю структуру Curve. Хорошо это или плохо — покажет время.