Author | jk

Last October, on the night BTC surged past $120,000, countless people screenshotted the chart and posted it on their social feeds, captioned with "History is being made." Just eight months later, the same people are staring at a price of $59,100, their social posts now asking, "Will it go lower?"

From the peak of $126,198 to the low of $59,100, BTC has experienced a drawdown of over 52%; in early June, the Crypto Fear & Greed Index plunged to 8, hitting its lowest level since 2022.

So, entering the market now—is it brave bottom-fishing, or just catching a falling knife?

In 2018, they said BTC would eventually go to zero; in 2022, they said the crypto industry was finished after the FTX collapse; and now in 2026, the narrative has shifted to "the four-year cycle is broken," "institutions only come to dump," and "risk assets have no place in a high-rate era." Every time, these narratives sound most convincing when prices are at their lowest.

However, narratives are emotional, while data is neutral. Only by separating the two does our current position in the BTC cycle become clear. Let's examine together: where exactly are we in this BTC cycle?

Where Does a 52% Drop Rank in Historical Cycles?

On October 6, 2025, BTC touched its all-time high of $126,198. From that day to an intraday low of around $59,100 on June 5, 2026, this drawdown exceeded 52% from the peak.

A 52% drop sounds alarming, but compared to BTC's past three full bear markets, this figure is actually below the historical median. The 2014 bear market fell 86% from top to bottom, the 2018 one dropped 84%, and the 2022 bear saw a decline of about 77% from $69,000 to $15,479. The current maximum drawdown of approximately 52% so far is significantly milder than the previous three.

This means historically, it has always recovered from deeper declines. While this statement might seem simplistic, from a market confidence perspective, the fear associated with the current price likely exceeds the actual risk implied by the fundamentals.

This is precisely why they say market confidence is more precious than gold.

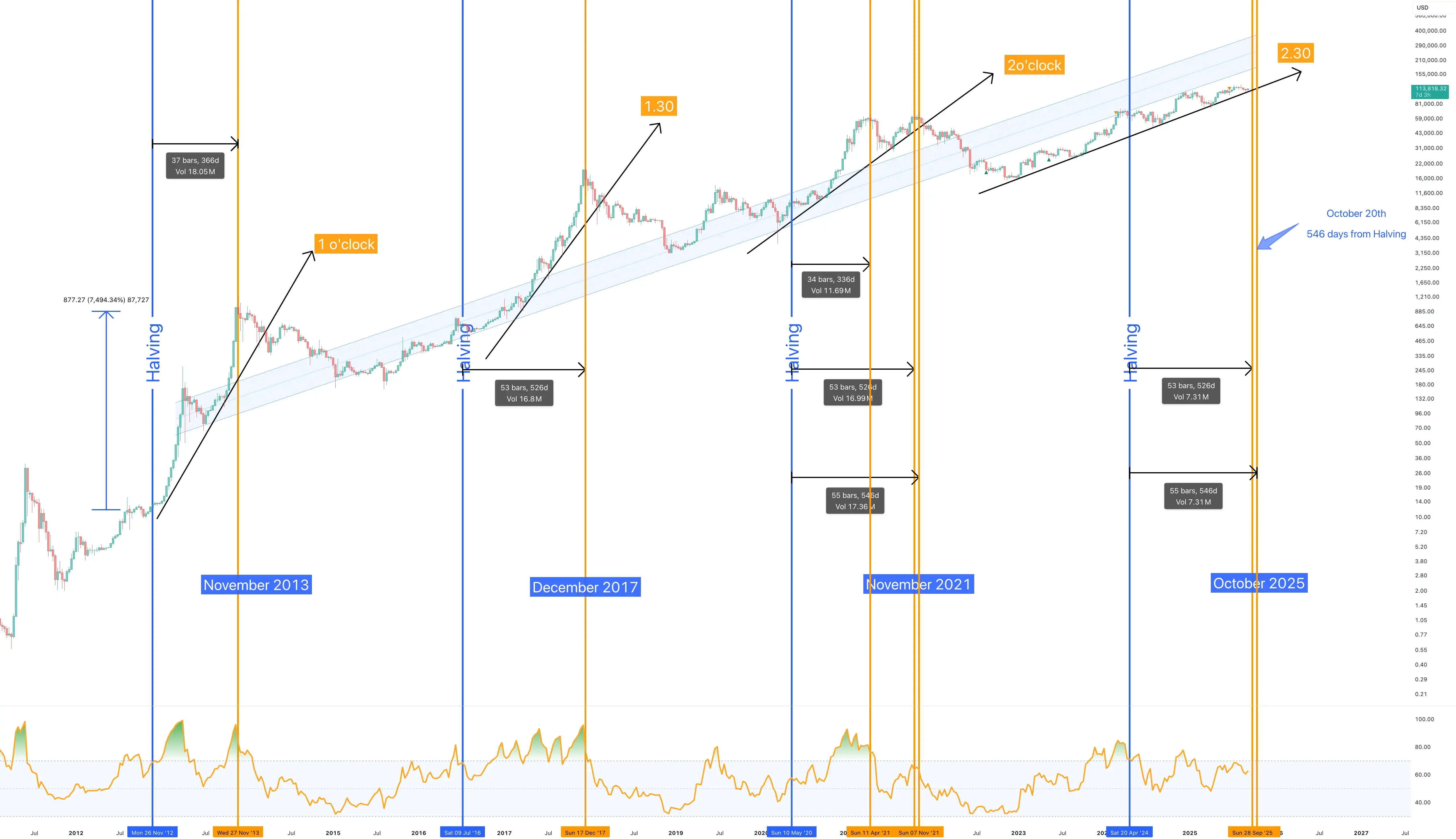

Four Halvings, Three Nearly Identical Curves

Understanding the current position is inseparable from the halving cycle framework.

BTC undergoes a halving approximately every four years, reducing the block reward for miners by half and contracting new supply. Surrounding each halving, the past three cycles have followed highly similar bull-bear rhythms: a peak occurs 12 to 18 months post-halving, followed by a bottom 12 to 14 months after the peak, with the bottom typically arriving about 17 months before the next halving.

- First cycle: Halving in November 2012 when BTC was around $12. About 12 months later, in November 2013, the price peaked at $1,150. The subsequent bear market lasted roughly 13 months, bottoming around $160 in January 2015—about 18 months before the next halving in July 2016.

- Second cycle: Halving in July 2016 when BTC was around $650. About 17 months later, in December 2017, the price peaked at $19,800. The subsequent bear market lasted about 12 months, bottoming around $3,200 in December 2018—again, about 17 months before the next halving in May 2020.

- Third cycle: Halving in May 2020 when BTC was around $8,600. About 18 months later, in November 2021, the price peaked at $69,000. The subsequent bear market lasted about 13 months, bottoming around $15,500 during the FTX collapse in November 2022—once more, about 17 months before the next halving in April 2024.

- Now, the fourth cycle: Halving on April 19, 2024, reducing the block reward from 6.25 to 3.125 BTC at a price of about $63,000. About 18 months later, BTC peaked at $126,198 on October 6, 2025, perfectly falling within the historical "12 to 18 months to peak" window.

As of June 2026, it's been about 26 months since the 2024 halving and about 8 months since the October 2025 peak. According to historical patterns, the bottom typically occurs 12 to 14 months after the peak, suggesting a bottoming window might arrive around October 2026. This would be about 17 months before the next halving (estimated April 2028), almost perfectly aligning with the timing of the previous three cycles.

BTC Halving Timeline

From the current vantage point, the second half of 2026 appears more like a phase to reassess the risk-reward ratio within this cycle, rather than a time for simple panic selling.

The supply contraction post-halving continues, and the structural change brought by spot ETFs and institutional capital has altered the market dynamics from being solely driven by retail sentiment. If historical cycles continue to exert influence, the area around Q4 2026 might precisely be the critical window where the market shifts from pessimism to repair, from deleveraging to re-accumulation. For investors bullish on BTC's long-term value, short-term pullbacks might offer more attractive opportunities for phased accumulation. As the bottoming zone gradually approaches, market confidence could begin to reconsolidate, laying the groundwork for the next uptrend.

On-Chain Data: Three Low-Level Signals Illuminate Simultaneously

Beyond price charts, on-chain data provides more fundamental valuation references.

- Signal 1: MVRV Z-Score. This metric measures the deviation between the current market price and the average cost basis of all coin holders. Historically, a Z-Score above 7 signals severe overvaluation near a top; falling near 0 or turning negative corresponds to deep undervaluation zones. When BTC peaked in October 2025, the Z-Score was around 5-6. According to data from MacroMicro on June 9, the current Z-Score is approximately 0.27, nearing the boundary of historical bottom areas.

- Signal 2: Realized Price. This is the volume-weighted average price at which all circulating BTC last moved on-chain (i.e., their aggregate cost basis). CryptoQuant Head of Research Julio Moreno noted on June 10 that this value is currently around $53,600. With a market price of $62,000, the premium above the aggregate cost basis is only about 9%, a historically rare low level. In past three cycles, major bottoms formed at or slightly below the realized price; it was briefly breached in November 2022.

- Signal 3: 200-Week Moving Average (200WMA). This line represents the average price over nearly the past four years and is currently around $62,200. On June 4, 2026, BTC touched this line for the first time in this cycle. The three major bear market bottoms in 2015, 2018, and 2020 all occurred precisely near this line. 2022 was the only exception, where the price broke below and remained under the line for about 16 months, culminating with the FTX collapse.

200-Week Moving Average Price. Source: TradingView

Capital Flows: Retail Out, Whales In

Beyond low valuation signals, the structure of capital flows is also showing some bottoming characteristics.

On the ETF front, from mid-May to early June, US spot BTC ETFs experienced net outflows for 13 consecutive trading days, totaling about $4.4 billion (approximately 59,400 BTC), marking the longest continuous outflow period since their launch. BlackRock's IBIT saw a weekly outflow of about $980 million, its worst single-week record. This reflects panic-driven redemptions from short-term and retail capital.

Simultaneously, opposite actions appeared on-chain. The number of whale addresses holding 100+ BTC reached a new 2026 high of around 20,229. The net buying volume by whales in the first five months of 2026 has already matched the total for all of 2025. MicroStrategy sold 32 BTC in late May to pay preferred stock dividends, its first sale in four years, sparking concerns about a strategic shift. However, two weeks later, on June 8, the company bought 1,550 BTC at an average price of $65,332, bringing its total holdings to 845,256 BTC. Michael Saylor described this as "an opportune time to add."

On the exchange front, BTC balances on major exchanges have been declining over the past months, with coins flowing from trading platforms to long-term holders' and institutional cold wallets. Currently, long-term holders (holding for over 155 days) control about 78% of the circulating supply, one of the highest proportions in history.

Macro: The Biggest Uncertainty, Just Half Removed

Over the past months, the core macro logic suppressing BTC has stemmed from two main lines: high interest rates and the Iran war.

In early 2026, US-Israeli military strikes on Iran led to a partial blockade of the Strait of Hormuz. The IEA labeled it the largest supply disruption in global oil market history, with international oil prices briefly surging to $105-120 per barrel. Inflation rebounded as a result; US May CPI rose to 4.2%, far exceeding the 2% policy target. The Federal Funds Rate was forced to remain unchanged in the 3.50%-3.75% range, and the market priced the probability of "zero cuts in 2026" to about 79% at one point. The US Dollar Index strengthened to the 99-100 vicinity. The dual pressure of high rates and risk-off sentiment meant that despite ongoing global liquidity expansion, funds could not flow into the crypto market.

However, on the night of June 14, US President Trump announced the completion of a US-Iran agreement. Iran's Supreme National Security Council formally confirmed the ceasefire memorandum of understanding in the early hours of June 15, with the official signing ceremony scheduled for June 19 in Switzerland. The Strait of Hormuz will subsequently reopen.

The market reaction was immediate and intense. WTI crude oil fell over 4% that day to around $80.25/barrel, and Brent crude dropped to around $83.51. BTC jumped from around $61,500 before the announcement to above $65,000, a single-day gain of over 5%—the largest one-day rebound in the past three months—with volume surging. Futures for the three major US stock indices all rallied over 300 points, and Asian markets followed suit.

Following the agreement, Deutsche Bank stated that it expects the risk of a Fed rate hike to subside in the near term. However, due to sticky inflation, a resilient labor market, and the possibility of a higher neutral rate, a rate hike in 2027 remains possible. The Fed's specific path, of course, depends on the debut of the new chair, Kevin Warsh.

Conclusion: It's the Bottom, and Also When Confidence Is Most Lacking

When BTC stood above $120,000, everyone was willing to believe it would go higher; but now, as it trades around $60,000, with on-chain valuation, cycle positioning, long-term holder dominance, and macro variables all pointing to a bottoming area, what the market lacks most is precisely confidence.

Yet, investing is never done when emotions are most comfortable. Historically, every major BTC bottom has been accompanied by "this time is different" skepticism, alongside comprehensive doubts about the industry, the cycle, and the asset itself. The difference lies only in whether one uses this doubt as a reason to exit or as an opportunity to reprioritize risk-reward.

Current BTC levels certainly don't guarantee it won't fall further or that this is *the* absolute bottom. But when viewed with a longer timeframe, separating short-term panic from long-term structure, the current zone is no longer defined by "chasing highs." It more closely resembles a window for phased accumulation—one requiring patience, discipline, and confidence.

Market confidence is more precious than gold. Because gold can only hedge against inflation, while confidence can navigate cycles. For those who still believe in the long-term value of BTC, in scarcity, and that global liquidity will eventually return to risk assets, the most important question in the second half of 2026 might not be "will it go lower?" but rather, when the market begins to believe in it again, will you already be positioned?

What will you choose?