Author: Lawyer Shao Shiwei

Recently, in a case involving the buying and selling of USDT (Tether) by a U merchant that Lawyer Shao is handling, the judicial authorities accused the client of engaging in illegal business activities involving the buying and selling of foreign exchange using virtual currency as a medium.

Although, in Lawyer Shao's view, the case has not yet formed a complete chain of evidence sufficient for conviction, due to the amount involved being as high as several billion, and the fact that in recent years the client used dozens of bank cards of relatives and friends for the collection and payment of virtual currency transactions, from the perspective of the case handlers, this operational model indeed does not resemble a "normal" business. Therefore, the prosecutor believes that even if it does not constitute the crime of illegal business operations, they are still considering charging the client with other crimes, such as the crime of obstructing credit card management, the crime of aiding information network criminal activities, the crime of concealing criminal proceeds, etc.

In (Case Notes | What are the risks of using others' bank cards to receive payments when buying and selling USDT?—Looking at the boundaries of determination and defense points for the crimes of illegal business operations, aiding information network criminal activities, and concealing criminal proceeds from a virtual currency case involving billions), I have preliminarily sorted out the related issues. This article will further focus on practical controversies and systematically discuss the following core issues:

Why should buying and selling virtual currency to earn price differences not constitute the crime of illegal buying and selling of foreign exchange, the crime of aiding information network criminal activities, or the crime of concealing criminal proceeds?

1、The Logic of Presumption of Guilt from a Judicial Perspective: Is Buying and Selling Virtual Currency to Earn Price Differences an Abnormal Business?

From the perspective of case handling, the model of U merchants earning price differences typically has two characteristics:

First, using multiple bank cards for collection and payment; second, the huge volume of funds.

Compared with traditional businesses, this funding path is more likely to be presumed to have legal risks. Because of this, even if the crime of illegal business operations is difficult to substantiate, the case handling authorities often look for other "fallback charges."

But Lawyer Shao wants to emphasize that, according to domestic policies, buying and selling virtual currency (over-the-counter OTC) is not prohibited by law, and there is an objective fact that a large number of U merchants, arbitrageurs, and ordinary investors participate in OTC transactions in China.

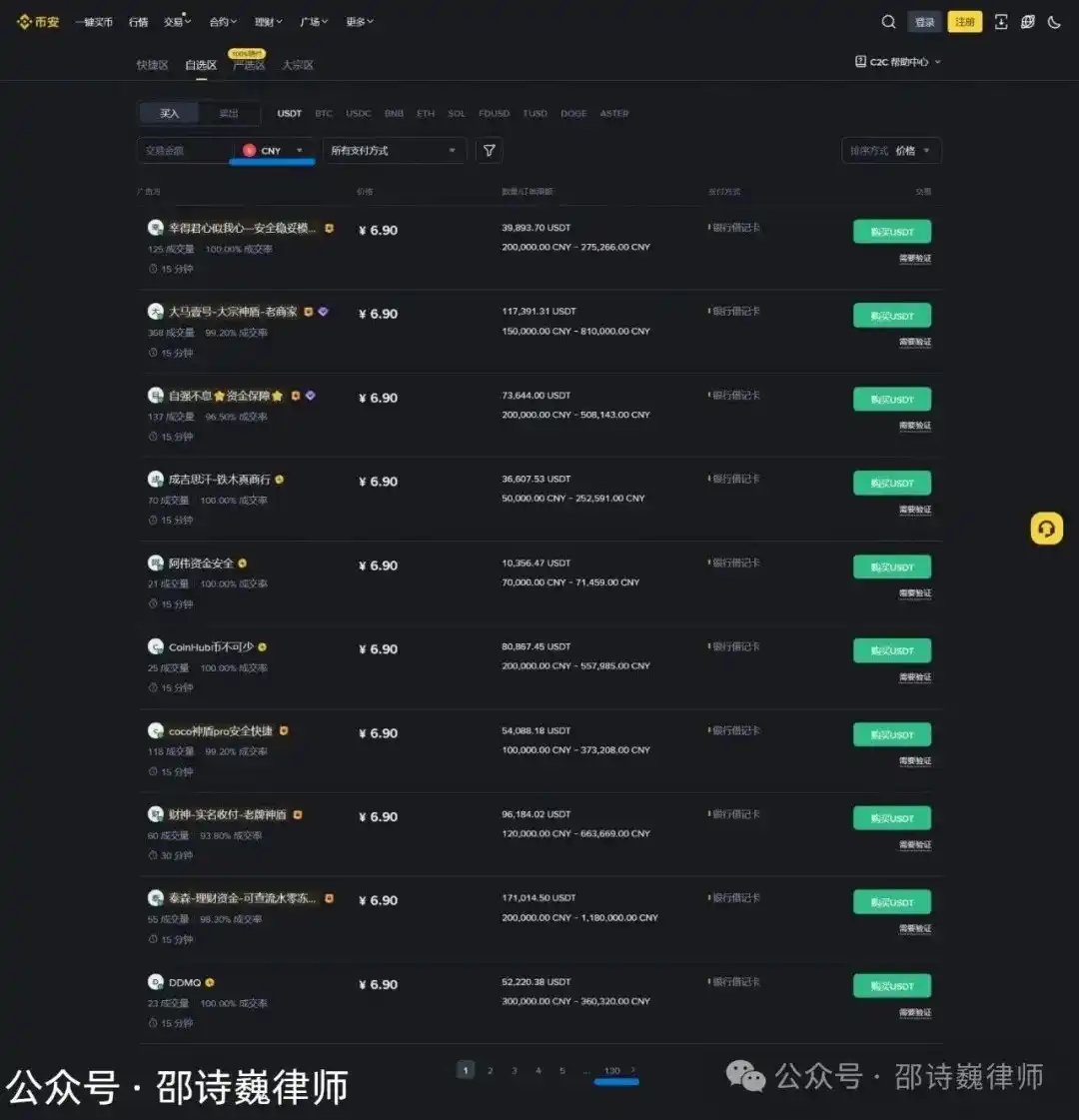

Taking the Binance exchange as an example, opening the C2C section and selecting the conversion currency CNY (Renminbi) shows 1,300 merchants (10 per page, 130 pages)—this indicates that OTC U merchants are not an isolated phenomenon but a规模化 (large-scale) existence.

Furthermore, on the C2C sections of mainstream trading platforms such as OKX, Bybit, Bitget, MEXC, and Gate.io, U merchants普遍 (commonly)入驻 (enter) the transaction matching pages as compliant merchants.

It should be noted that platform merchants are just the tip of the iceberg. In practice, there are also a large number of purely offline matching U merchants who complete transactions through communities, acquaintance circles, or channels such as Telegram and WhatsApp. This part is also extremely large in volume.

From the types of cases in recent years, Lawyer Shao believes that the focus of judicial打击 (crackdown) is not "the act of buying and selling USDT itself," but three types of behaviors:

-

Continuing the transaction knowing that the funds received are involved in fraud;

-

Using virtual currency to help launder money;

-

Knowing that the upstream is engaged in disguised buying and selling of foreign exchange, still providing assistance.

Therefore, whether the model of OTC merchants earning price differences is "normal" should not be compared to traditional businesses. Instead, the perspective should be placed within the normal模式 (patterns) of the U merchant industry to compare whether the client's behavior is abnormal.

Otherwise, if one always views this industry and group with colored glasses simply because the model is unfamiliar, it carries the suspicion of "presumption of guilt."

Next, Lawyer Shao will systematically explain why this behavior does not constitute the crime of illegal business operations, nor does it constitute the crime of concealing criminal proceeds or the crime of aiding information network criminal activities.

2、Reasons for Not Constituting the Crime of Illegal Business Operations

The prerequisite for认定 (determining) that a person constitutes the crime of illegal business operations involving the buying and selling of foreign exchange using virtual currency is that there is evidence to prove that they subjectively knew that the upstream was engaged in "matching exchange" and still provided assistance for the upstream crime.

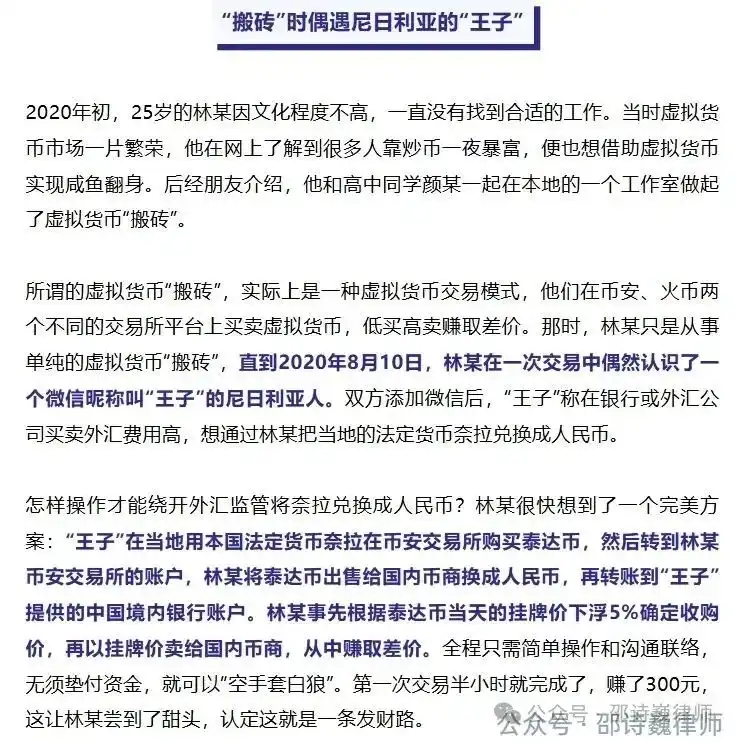

The case of Lin某 and Yan某 for illegal business operations published by the Supreme People's Procuratorate on December 21, 2024, is a typical case of this type:

-

From the perspective of the degree of subjective knowledge, Lin某, after being clearly informed by the Nigerian "Prince" of his intention to exchange currency, still provided assistance knowing the circumstances;

-

From the perspective of fund flow, Lin某 participated in the entire process where Prince used virtual currency as a medium to convert the local Nigerian legal currency, Naira, into Renminbi;

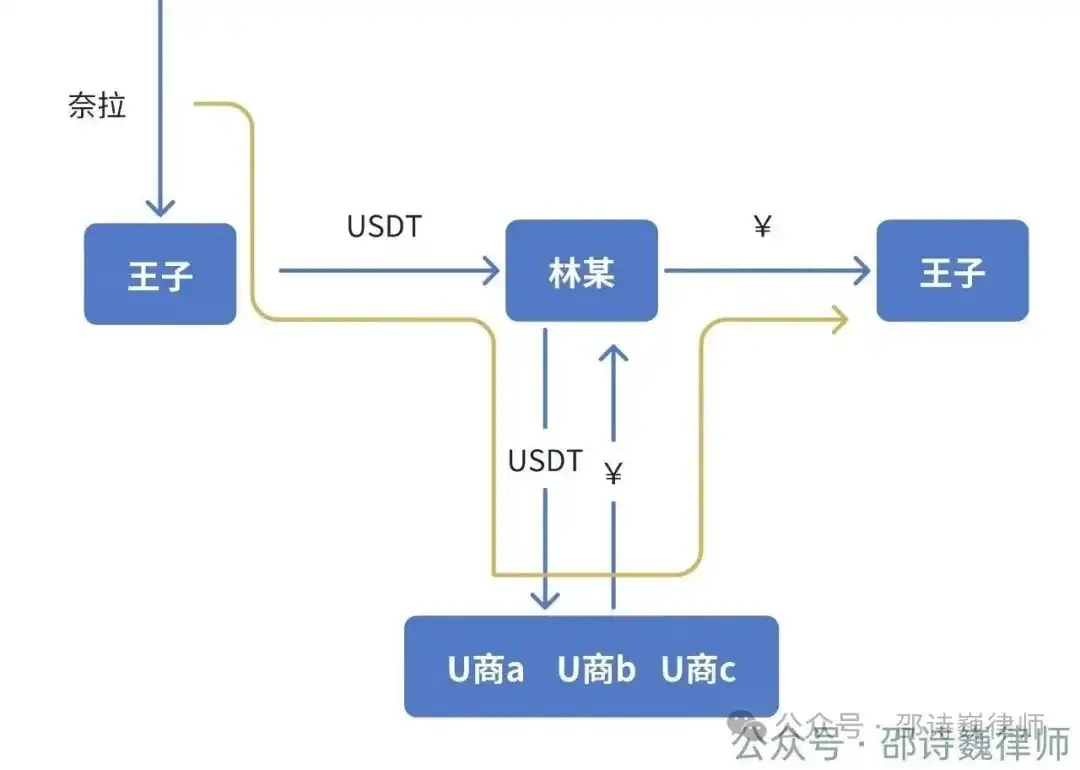

Therefore, Lin某's so-called "arbitrage" was essentially operating under the instructions of the Nigerian "Prince": Prince transferred Naira into Lin某's Binance account, Lin某 then sold the received USDT to domestic U merchants in exchange for Renminbi, and transferred the funds back to Prince. Lin某 determined the purchase price at 5% below the daily USDT listing price, then sold it to U merchants at the listing price, earning the price difference, thus constituting the crime of illegal business operations.

Therefore, U merchants a, b, and c, in such roles, would not constitute accomplices in Lin某's illegal business operation case simply because they had transactions with Lin某. Additionally, from the perspective of fund flow, another reason why U merchants a, b, and c in the above diagram do not constitute the crime of illegal business operations is that the transaction between the U merchants and Lin某 was limited to the one-way exchange between U and Renminbi, with the U merchants only earning the price difference profit. In contrast, the reason Lin某 constitutes the crime is that, although he was also earning a price difference profit, his transaction实际上 (actually) used virtual currency as a medium to achieve de facto exchange between different currencies for the Nigerian Prince, thus constituting the crime of illegal buying and selling of foreign exchange.

3、Reasons for Not Constituting the Crime of Concealing Criminal Proceeds

Is it possible to easily认定 (determine) that a U merchant is suspected of the crime of concealing criminal proceeds simply because the case involves huge fund transfers and multiple people's bank card receipts and payments?

Lawyer Shao believes that the determination of this crime cannot停留 (stop) at intuitive judgments such as "complex fund chain," "multi-card circulation," "large-value transactions," but must return to the core issue of the constitutive elements of criminal law: what is the criminal proceeds in the sense of criminal law?

According to the interpretation published on the official website of the Supreme People's Procuratorate[i], so-called criminal proceeds refer to the increase in property benefits obtained by the perpetrator through criminal acts and the maintenance of the part of their own property that should have been reduced. Simply put, criminal proceeds are the "profits" or "saved costs" generated by the crime, not the "principal" used for the crime.

Taking the typical underground currency exchange model as an example, the funds provided by the exchange customer are often Renminbi or foreign currency they originally obtained legally, but were used for illegal exchange行为 (behavior). This part of the funds is the principal for the exchanger; for the underground bank, it is not their criminal proceeds. The true "illegal gains" of the underground bank are usually only the exchange handling fees or exchange rate differences charged.

That is to say, the exchange principal itself does not automatically become "criminal proceeds" simply because it was used for illegal exchange. Only the benefits actually obtained by the underground bank for providing services may constitute criminal proceeds.

Looking at the role of U merchants based on this. The behavior of the vast majority of U merchants is essentially buying and selling USDT based on market prices to earn price difference profits. In this process, the funds received by U merchants are mainly the Renminbi or USDT principal paid by the counterparty, not the "already laundered criminal proceeds" of the underground bank.

In other words, U merchants are more involved in the circulation of the transaction principal, rather than helping to transfer, conceal, or realize the criminal proceeds of the underground bank.

This is also a point that is easily confused (confused) in many cases: case handlers often see "upstream crime + downstream receipt of money" and habitually think that the downstream is concealing criminal proceeds. But in fact, if the upstream funds themselves are not criminal proceeds, then even if the downstream participates in the circulation, it lacks the core object basis for the crime of concealing proceeds.

From judicial practice, the typical behaviors真正 targeted (truly targeted) by the crime of concealing proceeds are often helping to transfer fraud proceeds, splitting funds to evade supervision, layered laundering,代为提现 (cashing out on behalf of others), or converting criminal proceeds into "seemingly legal" assets.单纯的 (Simply) OTC transactions by U merchants, normal transaction matching, completing consideration exchange based on market prices, are essentially not (not) part of this "concealing criminal proceeds" behavior pattern.

Therefore, in most scenarios where USDT is simply bought and sold to earn price differences, if the U merchant:

-

Did not participate in the overall closed loop of the underground bank's currency exchange;

-

Did not knowingly help the underground bank transfer funds;

-

Only engaged in normal transaction matching based on market prices;

Then, even if there is illegal exchange behavior upstream, it is difficult to determine that the U merchant constitutes the crime of concealing criminal proceeds based solely on fund flow records.

4、Reasons for Not Constituting the Crime of Aiding Information Network Criminal Activities

The crime of aiding information network criminal activities is also a "high-frequency alternative charge" for case handling units in such cases. But according to the provisions of Paragraph 1, Article 287之二 (bis) of the Criminal Law, the prerequisite for the crime of aiding is "knowing that others are using the information network to commit crimes." Therefore, the prerequisite for applying this charge is: the upstream crime belongs to an information network crime.

Thus, whether the upstream of a U merchant belongs to an "information network crime" becomes the prerequisite for whether the U merchant themselves can be认定 (determined) as committing the crime of aiding.

What is an information network crime? The key issue is whether the core perpetrating act of the crime relies on the information network for implementation and completion.

Even if the buyer and seller of the exchange agree on the exchange rate and match funds through communication software, the settlement of Renminbi and foreign exchange funds is completely done offline through bank transfers or cash within China. At this time, the information network is only a communication tool, and the core of the crime (illegal foreign exchange买卖 buying and selling) is realized offline. Therefore, the criminal behavior in this model is not a network crime.

If the行为人 (actor) not only makes contact through communication software but also completes the collection and payment of funds (especially using domestic Renminbi accounts and foreign foreign currency accounts for "separate collection and payment") entirely through online banking and third-party payment platforms. At this time, the core link of the illegal business operation crime (payment and settlement) relies on the information network. This behavior may be认定 (determined) as "using the information network to commit a crime." If a person provides bank accounts to assist such online收款 (collection), it符合 (conforms to) the applicable scenario for the crime of aiding.

A typical case where using virtual currency as a medium for illegal foreign exchange was determined as the crime of aiding is the入库案例 (case entered into the database) published by the Supreme People's Court on June 18, 2025—The Case of Guo某zhao, Fan某pin for Illegal Business Operations, Zhan某xiang, Liang某zuan for Aiding Information Network Criminal Activities (Database Number: :2025-03-1-169-001. This case is also one of the typical cases of punishing foreign exchange-related crimes jointly released by the Supreme People's Procuratorate and the State Administration of Foreign Exchange in December 2023)

Basic Facts of the Case[ii]:

Guo某zhao, builder of the illegal exchange website.

Fan某pin, member of the illegal exchange group trading virtual currency.

Zhan某xiang, Liang某zuan, persons who provided virtual currency trading platform accounts and Renminbi bank accounts to Fan某pin.

From January 2018 to September 2021, Chen某guo (handled in a separate case), Guo某zhao, and others built websites such as "TW711 Platform" and "Rapid Platform," using the virtual currency Tether as a medium to provide customers with exchange services between foreign currency and Renminbi. After exchange customers placed orders in the top-up, payment on behalf, and other business sections of the aforementioned websites, they paid foreign currency to the overseas accounts designated by the websites. The websites used the aforementioned foreign currency to purchase Tether overseas, then Fan某pin sold it through illegal channels to obtain Renminbi, and then paid the corresponding amount of Renminbi to the domestic third-party payment platform accounts designated by the customers according to the agreed exchange rate, earning exchange rate differences and service fees从中 (from this). The aforementioned websites illegally exchanged over 220 million Renminbi. Among them, Fan某pin, by operating the virtual currency trading platform accounts and Renminbi bank accounts provided by Zhan某xiang, Liang某zuan, and others, received over 6 million Tether from Chen某guo, exchanging it for over 40 million Renminbi.

The reasons for the judgment in this典型案例 (typical case) were:

-

In this case, Chen某guo, Wang某, and others built illegal exchange websites, adopted the method of collecting New Taiwan Dollars through overseas accounts and paying Renminbi through domestic accounts to buy and sell foreign exchange for profit, constituting the crime of illegal business operations.

-

Guo某zhao, in the joint crime, was responsible for providing technical assistance and did not participate in specific business activities or share illegal gains; Fan某pin, in the criminal process, followed instructions to operate transactions. According to law, both should be determined as accomplices in the crime of illegal business operations.

-

Zhan某xiang and Liang某zuan had a general knowledge that others were using the information network to commit crimes and provided bank accounts to defendant Fan某pin and others, thus they were convicted of the crime of aiding.

From this case, it can be seen that under the premise that the upstream was sentenced for the crime of illegal business operations, the reason Zhan某xiang and Liang某zuan were determined to have committed the crime of aiding in this case was: the method of illegal exchange upstream was carried out by building illegal exchange websites, and the core link of the illegal business operation crime relied on the information network.

Therefore, if although the actors also communicate online through communication tools (such as WeChat, Telegram, and WhatsApp), the information network is actually only a communication tool, and the illegal buying and selling of foreign exchange is realized offline, then the upstream crime does not constitute an "information network crime." Therefore, in this situation, the prerequisite for determining the downstream U merchants receiving funds as committing the crime of aiding is lost.

Additionally, judicial organs often use the fact that the actor's bank card was frozen, restricted from counter services, etc., during the process of buying and selling virtual currency as a reason to consider that the actor meets the subjective "knowing" requirement for the crime of aiding. But according to the following judicial interpretation, it can be seen that only upon receiving "funds involved in fraud"等 (etc.) can it be determined as "knowing" in the crime of aiding. This article actually regulates actors who provide assistance to电信网络诈骗 (telecommunications network fraud). But as mentioned earlier, in the crime of illegal business operations involving foreign exchange, the reason U merchants are implicated is that they unknowingly received the exchange funds from the customers of the upstream underground bank (usually the legal income source of the exchanger), which is not the "funds involved in fraud" mentioned in the following judicial interpretation.

Opinions of the Supreme People's Court, the Supreme People's Procuratorate, and the Ministry of Public Security on Issues Concerning the Handling of Criminal Cases such as Aiding Information Network Criminal Activities

5. Accurately Determining the "Knowing" in the Crime of Aiding Information Network Criminal Activities......

(2) After being subjected to measures such as restriction or suspension of services by financial institutions, telecommunications business operators, or internet service providers due to involvement in fraud and other abnormal circumstances,仍然实施有关行为的 (still carrying out the relevant behaviors);

5、Final Words

In cases involving virtual currency, the determination of guilt or innocence should still return to the examination of the evidence chain and the constitutive elements themselves. As emphasized in the discussion by the Shanghai No. 2 Intermediate People's Court, "In the absence of virtual currency legislation and insufficient financial supervision in China, we should结合 (combine) China's national conditions and the spirit of relevant policies, use presumptions cautiously, and strictly control the scope of determining knowledge[iii]." Therefore, for behaviors such as buying and selling USDT to earn price differences, and acting as a collection and payment agent,定性 (qualification) should be done prudently, avoiding inferring subjectivity from the outcome.