Over the past two decades, the internet's most valuable assets have been two things: user time and advertising space.

Those who could keep users scrolling longer and clicking more could take the biggest slice of the digital economy. Traffic was the hardest currency of this era.

But today, a new signal is emerging.

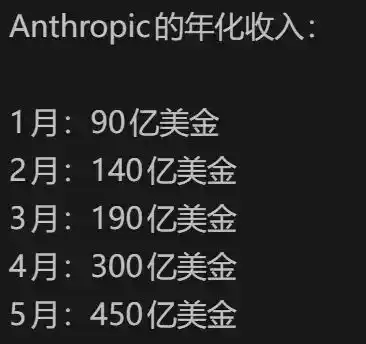

From January to May 2026, Anthropic's annualized revenue surged from $9 billion to $45 billion.

Meanwhile, ChatGPT's personal subscriptions stagnated, and the global paid conversion rate for consumer AI applications generally remained below 5%. The notion that users would switch to Doubao after being charged a single dollar is not just a meme—it's a reality repeatedly validated.

On one side, ice in the consumer sector; on the other, fire in the enterprise sector.

This is not a contradiction but a clear structural shift: the focus of AI commercialization is moving from serving consumers to helping enterprises save on labor costs.

The internet era profited from traffic.

The AI era profits from wages.

Ice and Fire: The Two Extremes of AI Commercialization

First, the icy side. Over the past year, numerous consumer-facing AI products have faced growth anxiety. ChatGPT's monthly active user growth has noticeably slowed, with low conversion rates between its free and paid tiers. Domestic large-model apps are caught in a price war, with API prices approaching zero. The user mentality is: use whichever is free; pay? Not happening.

The struggle of consumer AI is no accident. The differentiation in AI capabilities for chat, writing, and image generation is diminishing, and switching costs are nearly zero. No company has achieved indispensability. According to SearchLab data, ChatGPT Plus subscription conversion rates have long been below 5%, while the quality of free alternatives has approached that of GPT-4. Users calculate clearly: paying $20 per month for a 10% performance improvement isn't worth it.

Now, the fiery side. Anthropic's ARR went from $9 billion to $45 billion in just five months. Over 90% of this comes from enterprise API and Agent deployments, not personal subscriptions. Claude Code programming Agent became the core growth engine, with enterprise customers spending over $1 million annually growing from 500 in February to over 1,000 by May. OpenAI's enterprise revenue continues to climb, Microsoft Copilot's penetration rate among Fortune 500 companies jumped to 55%, and companies like Salesforce and ServiceNow are using AI Agents as a core pricing lever.

Why are enterprises so willing to pay? The core logic is ROI. A single Claude Code Agent can replace the workload of hundreds of junior programmers. An enterprise spends $3 on AI and saves $10 in wages. This formula is so clear it hardly needs a sales pitch. Industry estimates put the average ROI for enterprise clients at 3.7x, with the highest exceeding 10x. In a macroeconomic environment focused on cost reduction and efficiency, such deterministic returns are irresistible.

This is not just a phenomenon for a few leading companies but a collective shift for the entire industry. According to PitchBook data, venture capital flowing to enterprise AI startups grew 210% year-over-year in Q1 2026, while funding for consumer AI dropped by 35%. Talent is also migrating: industry observations indicate over 40% of consumer AI product founders have announced a pivot to the enterprise track. On the surface, it's a split; in essence, it's the first time AI commercialization has truly validated who pays and why—a closed loop.

Moreover, B2B is not a low-margin business. Anthropic's gross margin exceeds 70%, with a net revenue retention rate of 140%, and profitability is projected for Q2 2026. Enterprises pay a premium because they save far more than they spend. This isn't a price war; it's a positive ROI cycle driven by productivity premiums. The global annual labor cost pool for backend operations, customer service, and junior R&D exceeds $5 trillion. Even if AI achieves only a 10% replacement rate, that's a $500 billion market. Anthropic's $45 billion ARR accounts for less than 10%—the ceiling is far from being reached.

Break and Build: The Clash Between Traffic Logic and Cost Logic

Many people habitually understand AI through the lens of the internet: acquire users for free, then monetize through advertising or premium services. But AI is not the internet. Mixing these two logics is the biggest misconception in understanding AI commercialization.

Why can't the consumer sector make money? Because it faces insurmountable structural barriers:

First, efficiency tools struggle to compete for entertainment time. Short videos and games satisfy emotional needs; users are willing to pay for enjoyment. AI solves specific tasks and is used on a need-to-use basis. The average ChatGPT session lasts about 7 minutes, while TikTok exceeds 30 minutes. AI is inherently disadvantaged in the battle for user time.

The second issue is homogeneous competition and extremely low switching costs. AI capabilities are rapidly becoming homogeneous. In 2024, GPT-4 stood alone; by 2026, open-source models have caught up to the same range. When performance is similar, price becomes the only differentiator, eventually leading to freemium models and price wars. This has already been validated in text-to-image and translation fields.

Of course, the lack of network effects leading to a failure of moats is also a significant problem. Whether you use ChatGPT or Claude doesn't affect anyone else. Users only need to change a bookmark to migrate. User scale is not a moat; OpenAI's hundreds of millions of monthly active users cannot lock in users.

Most importantly, there is a ceiling effect on consumer payments. The amount users are willing to pay for a productivity tool does not exceed its replacement cost. Low-frequency users only accept free services, while high-frequency users turn to enterprise bulk procurement. Squeezed from both ends, consumer subscriptions become a chicken rib.

Conversely, the B2B market is experiencing explosive growth precisely because its commercial DNA aligns perfectly with AI.

It's crucial to understand that enterprises buy AI based solely on ROI. Consumers might pay for a nice interface, but enterprise procurement decision-makers only run the numbers: spend $3, save $10, buy. Goldman Sachs reports show that the customer lifetime value of enterprise AI software is 8 times the customer acquisition cost, far above the SaaS average, with极强的 stickiness.

And AI in the B2B space doesn't replace a few individuals but entire job functions. When enterprises gradually hand over customer service, financial preliminary review, and code generation to AI, they save the labor costs of entire functional modules. A large e-commerce company that introduced AI customer service reduced its team from 500 to 80 people, with response times shrinking from 5 minutes to 30 seconds. AI replaces workflows, not headcount.

Deep integration creates extremely high switching costs. Once an enterprise deeply integrates AI into its CRM, CI/CD, and data warehouse, migrating to another model requires re-tuning and改造, which itself forms a moat. Business-specific fine-tuning data and prompt templates are also assets.

Of course, there's also the reason that B2B pricing power is stronger. A company with annual revenue of $1 billion spending $3 million on AI accounts for only 0.3% of its revenue but can save $10 million in labor costs. Enterprises won't sacrifice quality and stability to save a few cents on token pricing. This is precisely why Anthropic enjoys a gross margin of over 70%—pricing is based on value, not cost-plus.

The consumer sector follows traffic logic; the enterprise sector follows cost-replacement logic. The failure in the consumer sector isn't due to AI's inadequacy but to a business model mismatch. AI commercialization is switching from the former to the latter. This isn't a short-term fluctuation but a fundamental shift in underlying logic.

Virtual and Real: The Evolution from Digital Tool to Digital Labor

What does Anthropic's $45 billion ARR truly validate? Not just that B2B can be profitable, but a more fundamental transformation: AI is evolving from a digital tool into digital labor.

First, AI is no longer assistive software but the main agent of production. Over the past forty years, the logic of enterprise software has been to enhance human efficiency—Excel helps accountants calculate faster, but the accountant remains. Photoshop helps designers work more efficiently, but the designer remains. All software was a tool, with humans as the decision-makers. But AI Agents are different: Claude Code writes code directly; a customer service Agent responds to users directly. AI has transformed from a tool into an executor, and humans have shifted from operators to supervisors. This is a qualitative change.

Second, B2B revenue and the AGI narrative are not opposites but a symbiotic, closed loop. Some question: if revenue mainly comes from enterprise tools rather than AGI, is AGI a bubble? The opposite is true. B2B revenue feeds back into model training; the $45 billion ARR is invested in the next-generation model. The stronger the model, the more willing enterprises are to pay. Model progress sustains AGI belief; the market doesn't need AGI to be realized today, only to see continuous approximation. AGI belief supports high valuations, high valuations bring funding, which is then invested in R&D. This is a complete positive cycle. Today's Agents are, in a commercial sense, the embryo of AGI. The market wants a path, not an endpoint, and B2B revenue is the foundation paving that path.

Third, AI is replicating the essential logic of the Industrial Revolution. Over two hundred years ago, the steam engine replaced human and animal labor, becoming the new core of productivity. Enterprises that connected to steam engines earliest gained overwhelming efficiency advantages. The Industrial Revolution was, in essence, a labor substitution revolution, using machines to replace physical labor and liberating productivity from the constraints of biology.

Today, AI is doing the same thing, only it's replacing mental labor. Programmers, customer service agents, data analysts, accountants—white-collar positions are being infiltrated one by one by AI. This is not incremental efficiency improvement but structural labor substitution. Enterprises that earliest integrate AI Agents into their business processes are gaining dual advantages in cost and response speed.

In the internet era, the most valuable assets were traffic and user attention. That was the logic of the consumer internet. In the AI era, the most valuable asset is digital labor—algorithms and computing power capable of performing mental labor at extremely low cost. This is the logic of the productivity internet. The global annual wage bill exceeds $50 trillion. Even if AI replaces only 10% of that, it's a $5 trillion annual market. In contrast, the combined global market for internet advertising and subscriptions is just over $1 trillion.

Therefore, AI is not the next Facebook, nor the next Google. It is not a traffic business. It is the next steam engine—a new factor of production redefining labor and cost. When it substitutes human labor on a large scale, the market value it creates will far surpass that of the internet. Wages are much larger than traffic.

Looking back, we may have been using the wrong analogy to understand AI. In the internet era, the most valuable asset was traffic. Those who captured users' time and attention built empires. But AI is not a traffic business. Its real value lies not in making users scroll a few more minutes but in replacing human labor and enhancing organizational efficiency.

This is more like the Industrial Revolution. Over two hundred years ago, the steam engine emerged, replacing human and animal labor, becoming the new core of productivity. Today, AI is doing the same. It is not the next Facebook, nor the next Google. It is the next steam engine—a new factor of production, redefining labor and cost.

When an Agent replaces not 10 people but an entire job function; when an enterprise spends $3 to save $10; when AI's ARR surges from tens of billions to hundreds of billions... only then will we truly understand: the internet era profited from traffic, the AI era profits from wages. And wages are much larger than traffic.

AI is not replicating the internet. It is replicating the Industrial Revolution.

References:

36Kr, For the First Time in History, Anthropic Is About to Make a Profit, May 2026 https://www.36kr.com/p/3819897940562307

PitchBook, Q1 2026 AI VC Trends Report https://pitchbook.com/news/reports/q12026aivctrends

NetEase News, The More AI Is Used, the More Profitable It Becomes: Reading Goldman Sachs' Agent Economics Report, May 2026 http://www.163.com/dy/article/KSAL8CLK05568W0A.html

Caizhongshe, Haitong International: Anthropic Profitable Two Years Ahead of Schedule, AI Commercialization Milestone Established, May 2026 https://www.caizhongshe.cn/article7465239590204012512.html

This article is from the WeChat public account "科技新知" (ID: kejixinzhi), Author: Juzi