Written by: Alice French, Bloomberg

Compiled by: Saoirse, Foresight News

Within Tokyo's tightly-knit financial circles, few figures are as polarizing as Michael Lerch.

To some, he is a white knight—a mysterious American investor who rescues struggling Japanese companies from the brink of collapse. To others, he is a greedy hyena: a profit-obsessed hedge fund manager who preys on vulnerable, crisis-ridden firms.

Throughout Japan's capital market, Lerch is synonymous with death spiral financing, a highly profitable yet deeply controversial funding model. His boutique investment fund, Evo, is the largest buyer of floating-strike equity warrants in Japan. These niche financial instruments are primarily targeted at small, cash-strapped listed companies. The contracts can quickly inject cash flow to keep businesses afloat but often trigger massive equity dilution, hence the pejorative nickname for this model.

(Note: Floating-strike equity warrants, commonly known as death spiral financing tools, have exercise prices that dynamically adjust downward with the stock price, easily causing a vicious cycle of continuous equity dilution and stock price decline. Their rampant abuse in the Japanese market stems from a lack of financing channels for local small-cap, low-quality companies, exchange market value regulations forcing survival measures, lax regulatory constraints, and a monopoly on financing supply by major institutions, compelling companies to accept high-risk contracts to maintain their listing status.)

After graduating from Princeton University, Lerch arrived in Japan in the 1990s. For many years thereafter, he remained largely out of the public eye, building his financial empire through arbitrage trading. This changed last year: the previously struggling hotel operator Metaplanet suddenly gained fame, acquiring over $2 billion worth of Bitcoin, with almost all of the funds coming from warrant financing provided by Evo.

This疯狂的 (frenzied) bitcoin accumulation drove Metaplanet's stock price soaring, attracting retail investors, major institutional giants, and even the Trump family to participate, vividly demonstrating the astounding profitability of Lerch's business model.

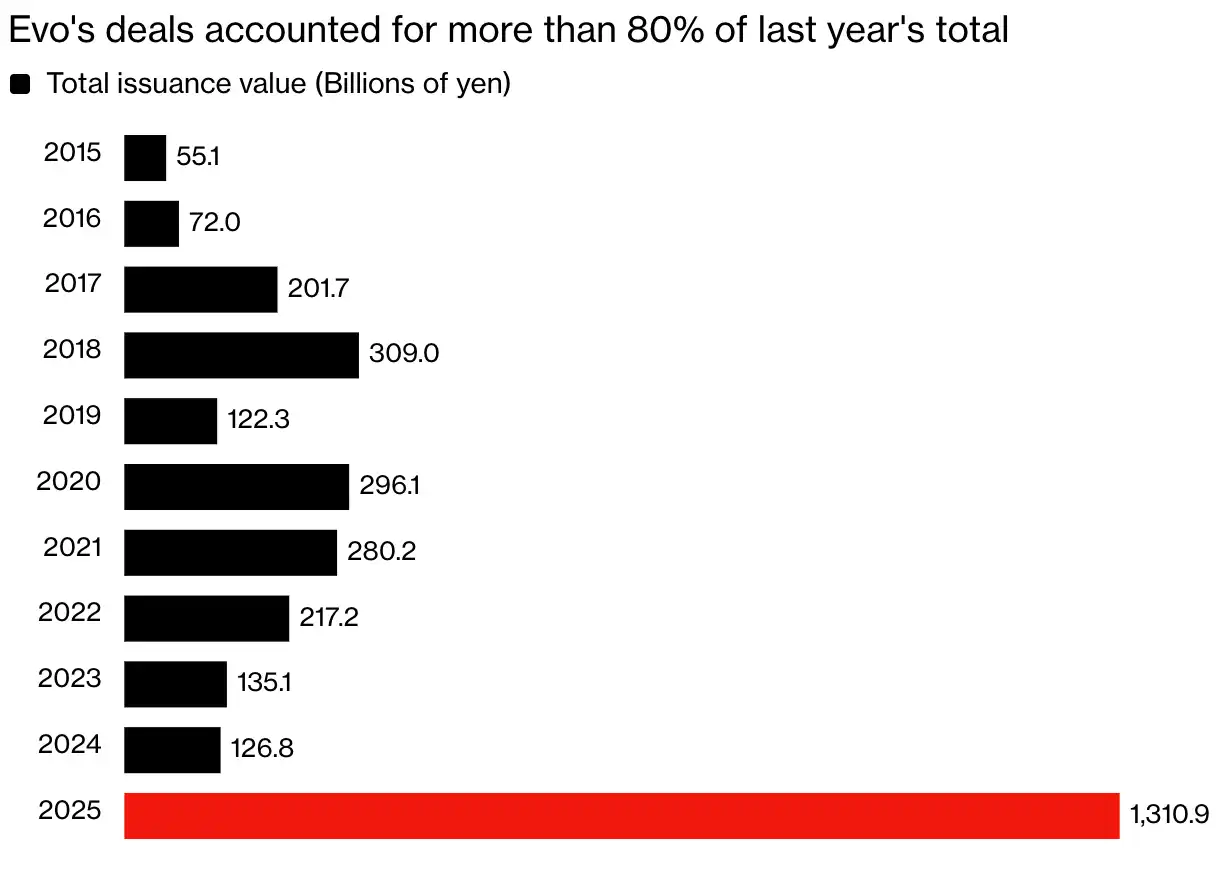

According to data from Japan's I-N Information Systems Co., the series of transactions between Evo and Metaplanet made 2025 the year with the highest issuance volume of floating-strike warrants in Japanese history. Lerch's fund concluded such financial transactions totaling over 1 trillion yen (approximately $6.3 billion) in Japan last year, accounting for more than 80% of the total market size.

Japanese Floating-Strike Warrant Issuance Hits Record High

Evo's transactions accounted for over 80% of last year's total market volume

Note: Statistical value includes initial issue price and maximum fundraising amount

Data source: I-N Information Systems Co., Bloomberg

This boom has continued into 2026. According to disclosures on the fund's official website, Evo has signed equity financing agreements with at least 10 Japanese companies so far this year.

The surging market demand for Lerch's financing services has also brought to light the issue of abuse of floating-strike warrants in Japan. Coinciding with the Japanese government's upgrade of its tax-free investment scheme, a record number of retail investors have flooded into the stock market, exacerbating potential risks. These warrants issue large quantities of new shares at low prices to third parties, continuously diluting the ownership stakes of small and medium shareholders.

Sadakazu Osaki, chief researcher at Nomura Research Institute and a seasoned expert in Japan's equity capital markets, stated: 'These warrants are the last financing resort for underperforming companies. This spiral trading can cause equity dilution and suppress stock prices. If ordinary retail investors get caught up in it, they will face significant risks.'

Evo's stellar performance last year also brought the long-low-profile Lerch into the public eye. He has always operated secretively throughout his career, having only granted one interview to Bloomberg in 2015. He made news again last December: a London court ruled that his Nevada-based Evolution Capital Management company must pay over $5 million in disputed bonuses to a disgruntled former trader.

This report is based on interviews with more than 20 of Lerch's former employees, client partners, and industry insiders familiar with his business (most requested anonymity to protect their privacy), combined with financial reports from Japanese listed companies, London court litigation documents, and other judicial materials. Together, they reveal the truth:凭借极具优势的合作条款与强硬果决的行事风格 (Leveraging highly advantageous partnership terms and a resolute, assertive style), this previously obscure fund has leapt to become the financing institution of choice for Tokyo companies vying for cooperation.

Lerch, who now resides year-round at his lakeside estate in Lake Tahoe, Nevada, and his Evolution Financial Group, both declined to comment for this article. The lawyer representing Evolution Capital in the London case also did not respond to requests for comment.

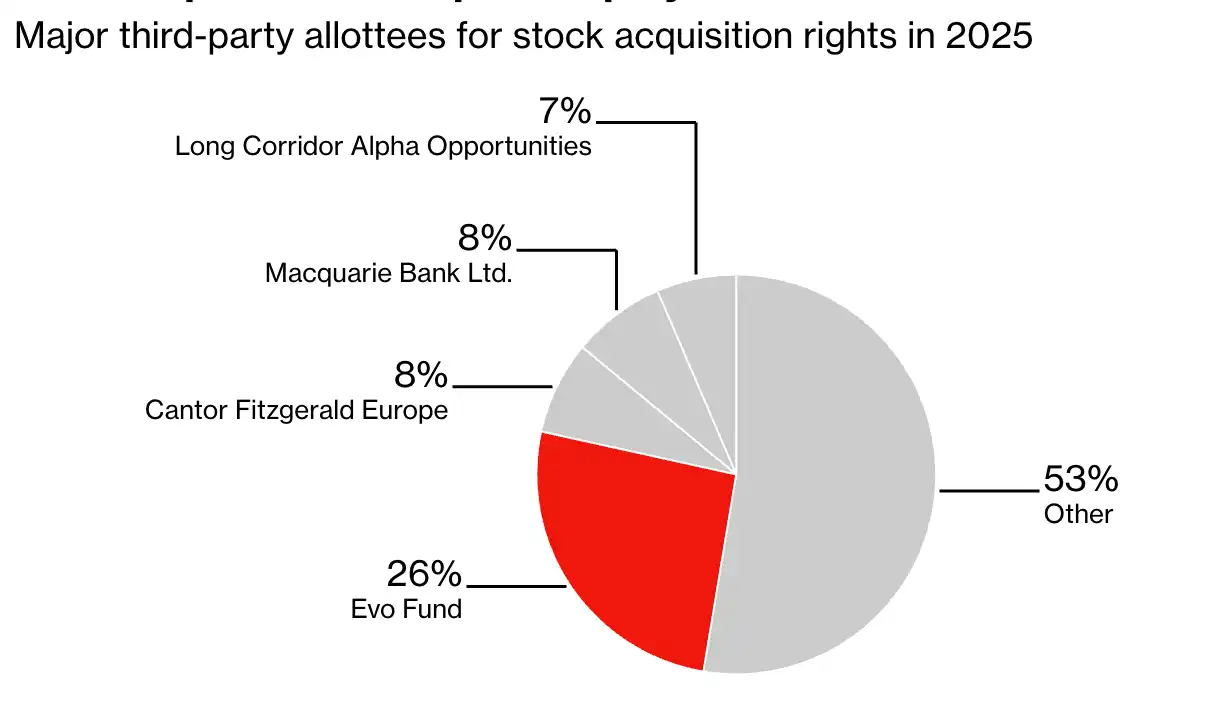

Evo is Japan's Most Popular Warrant Partner

Main third-party allottees for stock subscription rights in 2025

Note: Based on number of issues; percentages may not sum to 100 due to rounding

Source: I-N Information Systems

Lerch began his career in Japan in 1994. Later that year, he joined Barings Bank to work in options trading, just months before the rogue trader Nick Leeson's unauthorized actions directly led to the bank's collapse.

Starting in 1996, Lerch honed his trading skills at Merrill Lynch, Crédit Agricole, and Lehman Brothers, before establishing the Evolution Financial Group in Tokyo in 2002. Evo was the group's first fund, capitalized with his own money and investments from friends and family.

Andrew Jackson, who came to Japan in 1997, worked as a trader at Jefferies' Tokyo branch in the mid-2000s, and is now head of Japanese equity strategy at Ortus Advisors, recalled: 'Investment opportunities were everywhere in Japan back then, and Evo made a fortune. Market regulation was loose, all networking happened in bars over drinks, and Japan's capital market was truly a wild jungle at that time.'

Jackson stated that he had extensive business dealings with the Evolution group back then. The firm made its name among brokers by arbitraging the huge bid-ask spreads prevalent in the Japanese stock market at the time.

Lerch, now around 55 years old, has expanded the Evolution Group into a cross-regional family office with operations in Los Angeles, Hong Kong China, and an outpost on Hawaii's famous North Shore. According to disclosures in the London court files, the entire group has approximately 55 employees globally.

Those who know him say his exceptional networking skills are key to his business expansion. To others, Lerch is intelligent and shrewd, with a slightly eccentric personality: in conservative Japanese business circles, he favors brightly colored suits and thick-framed glasses, making him highly conspicuous. In a 2023 YouTube video, he wore a bright yellow sweater, matching glasses, and a heavy pendant necklace while walking through his office; the video promoted the group's involvement in a US-Japan youth leadership exchange program.

This is a screenshot of Michael Lerch from a 2023 YouTube video

Lerch was a football player in college, and his Ivy League pedigree also helped elevate his prestige in Tokyo. In the group's early days, he prioritized hiring graduates from Ivy League schools and incorporated 'tiger' elements into many business names, paying homage to his alma mater Princeton University's mascot.

Over the years, Lerch has leveraged his connections to secure several major deals:

- In 2010, Evolution Capital Management acquired the now-defunct professional basketball team Tokyo Apache;

- The following year, Evolution Japan Securities acquired the electronic covered warrant business from Goldman Sachs Japan, spinning it off and selling it to Japan's Caica Digital company seven years later;

- In 2022, the group announced the sale of its self-developed electronic trading platform Tora (Japanese for 'tiger') to the London Stock Exchange Group for $325 million.

But Lerch's business path has not been smooth sailing. According to court documents submitted by the plaintiff in the London bonus dispute, after the 2008 global financial crisis erupted, his multi-strategy hedge fund launched in 2004 was forced to liquidate under the impact of密集的投资者赎回 (intense investor redemptions). The fund's assets under management had once reached about $1 billion at its peak.

Evo's financing business centers on floating-strike warrants, alongside other financing tools like convertible bonds, with the entire operation rooted in Lerch's decades of arbitrage experience. The fund's Japanese website介绍称 (states): its advantage lies in tailoring to companies' individualized needs and offering flexible and efficient investment decisions.

Floating-strike warrants have been a常规工具 (standard tool) in Japan's equity capital market since the early 2000s, as the country recovered from the slump of its asset bubble burst. These warrants grant the holder the right to purchase company stock in the future, with the exercise price varying over time as agreed by both parties, typically based on the previous trading day's closing stock price.

It is very similar to the market-priced direct stock offering model in the US stock market and serves as a fast, low-cost financing channel for companies unable to obtain credit from banks or large institutions.

When the exercise price is lower than the market price of the stock, warrant holders exercise their rights to convert into shares and then sell the stock to profit from the difference.

NRI's Osaki said: 'Some people think this model is fraught with hidden dangers, but Evo's logic is very simple: when no institution is willing to lend to a company, it is the only lifesaving solution.'

Nobuhiro Nagasawa, president of the seafood restaurant group Sanko Foods, knows this well: 'Without Evo, we might have already shut down our business.'

A seafood restaurant in Tokyo operated by Sanko Foods. Source: Sanko Foods

During the pandemic, Sanko Foods closed many stores and fell into financial crisis,濒临退市 (teetering on delisting) in early 2020. Around 2022, Evo business personnel主动到访 (actively visited) Sanko Foods' stall at the Numazu fish market, about 100 kilometers south of Tokyo, to promote financing services. Soon after, Nagasawa met with Lerch and reached a financing cooperation agreement with Evo.

Nagasawa坦言 (stated frankly) in an interview at an izakaya in Tokyo: 'It's undeniable that these warrants确实压制了 (did indeed suppress)) our stock price and caused short-term losses for existing shareholders. But these funds saved the company, it was all worth it, and I am very grateful to Evo.'

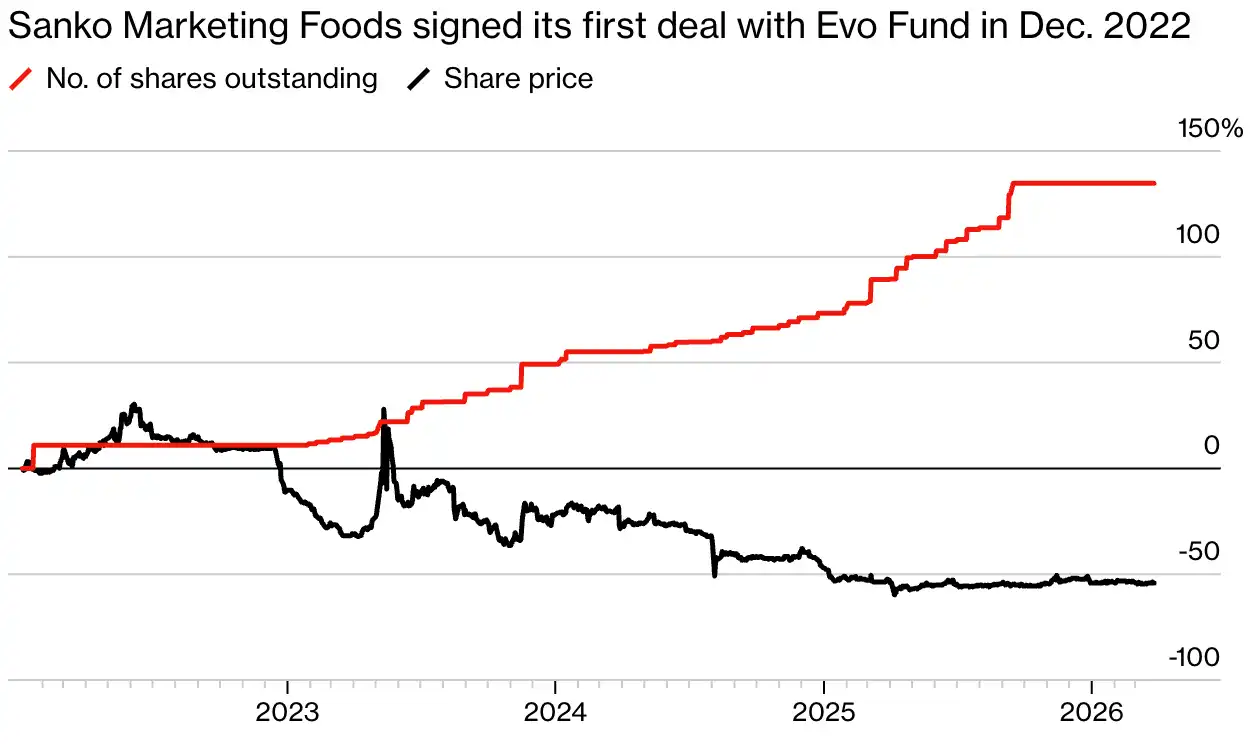

Evo's Financing Activity Suppressed Sanko Foods' Stock Price

Sanko Foods signed its first transaction with Evo Fund in December 2022

Note: Data normalized to percentage change as of January 4, 2022

Source: Bloomberg; Sanko Foods Co. disclosures

In stark contrast is Shingo Kameda, president of the investment firm Banka Investment Co. He said the company's reputation is still recovering since its cooperation with Evo in 2023.

'That financing severely damaged the company's image,' Kameda admitted, stating that the company was in financial distress at the time and did not actively seek Evo's financing; it simply had no other choice and signed a fixed-strike warrant agreement without fully understanding the risks involved.

Before partnering with Evo, the company's stock price was already in a downward trend. Evo's repeated exercises at prices below the market price further depressed the stock price, causing strong dissatisfaction among existing shareholders. 'Evo's contract design guaranteed their profit from the very beginning.'

Evo's website claims the fund can provide flexible solutions, offer full support throughout the financing process, and engage in ongoing prospective communication and cooperation with Japanese companies.

Shingo Kameda, CEO of investment company Banka Investment Co.

Metaplanet President Simon Gerovich stated that Evo's highly competitive partnership terms make it the highest-quality warrant financing partner in Japan. After the pandemic forced the closure of many of its hotels, Metaplanet entered into a floating-strike warrant agreement with Evo in early 2025 to raise funds for massive Bitcoin purchases.

'In terms of advantageous合作条件的优势 (cooperation terms), no institution can match Evo,' Gerovich explained. Other potential investors would take an 8%~10% risk premium on the exercise price, while Evo承诺 (promised) not to charge any discount fee upon exercise.

Additionally, Evo's exercise efficiency is extremely high, allowing Metaplanet to raise funds extremely quickly. Evo also signed a stock lending agreement with Gerovich's investment company (Metaplanet's major shareholder) to hedge positions before each transaction, further speeding up the exercise process.

Last year, Gerovich publicly thanked Lerch for his support of Metaplanet on social platform X.

Industry insiders who previously worked at Evo revealed that the fund's ability to offer favorable terms relies on its mature warrant arbitrage capabilities. The team's traders have a high risk tolerance, and Lerch himself often scouts and recruits talent at various Tokyo social events.

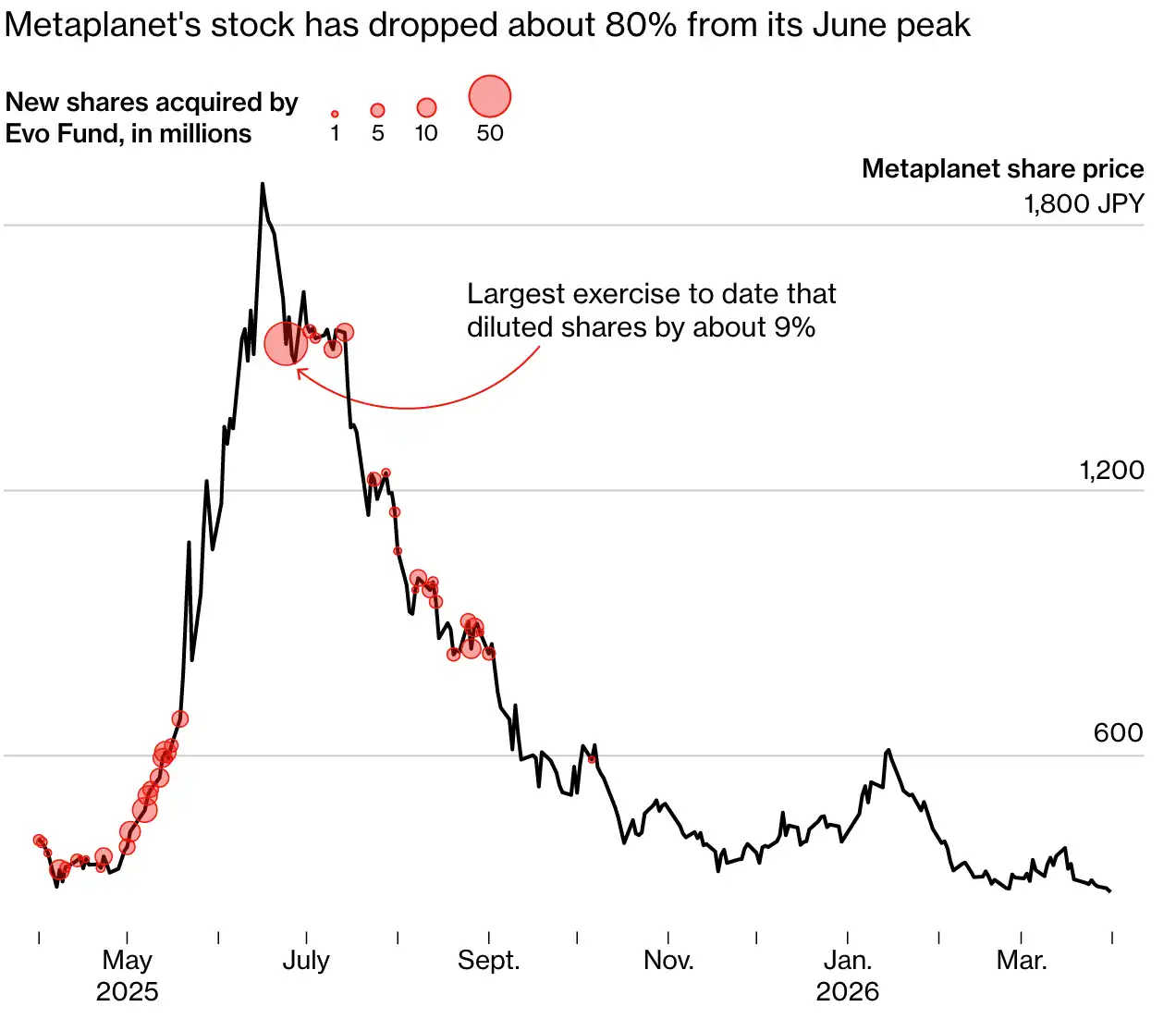

Evo's large-scale exercise transactions with Metaplanet直观展现了 (vividly demonstrate) the lucrative potential of this model. According to Metaplanet's regulatory announcements and Bloomberg calculations: on June 24, 2025, Evo acquired 54 million Metaplanet shares at a price nearly 10% below the closing price. Within just one week, the fund sold 16% of these shares, profiting 2.2 billion yen.

Gerovich stated: 'Evo indeed made substantial profits, but it's a win-win situation.' Metaplanet raised over 290 billion yen through warrants in 2025 and currently holds more than 40,000 Bitcoins.

As Metaplanet continued to raise funds to hoard Bitcoin, Evo's exercise transactions不断稀释 (continuously diluted) the equity of existing shareholders, including a large number of retail investors holding shares through Japanese tax-free investment accounts. Just that one exercise on June 24 expanded Metaplanet's total share capital by approximately 9%.

Gerovich explained this: 'In this business model, all shareholders' equity will be diluted, but no one minds because this dilution is良性 (benign)—our Bitcoin assets are continuously appreciating.'

After an initial surge of over 2000%, Metaplanet's stock price has plummeted about 80% since its mid-June high. Since October 2025, Metaplanet has sought other financing channels, and Evo has ceased exercising warrants for it.

Even as Metaplanet's Stock Price Crashed, Evo Continued Exercising MS (Moving Strike) Warrants

Metaplanet's stock price has fallen about 80% from its June peak

Message source: Metaplanet submitted documents; Bloomberg

Japan Exchange Group (operator of TSE) declined to comment specifically on Evo's business. Officially, it stated that floating-strike warrants issued to third parties are a常规股权融资工具 (standard equity financing tool) for listed companies.

The exchange also acknowledged: market concerns that such tools could harm shareholder权益 (rights and interests) through equity dilution and stock price declines have led to regulatory constraints, such as setting monthly exercise caps. Listed companies can also mitigate the impact of equity dilution by setting minimum exercise prices, lock-up periods for sales, and other terms.

But Lerch has always been known for his强硬 (tough), uncompromising approach, making many Japanese companies wary of cooperating with him.

Alexey Shitov, a former executive at the Evolution Group in the 2010s who handled the warrant business acquired from Goldman Sachs, said: 'Evo has always had a reputation for being aggressive in the industry. The perception of us by clients noticeably changed after the Evolution Group took over the business.'

Regulatory penalty records show: in early 2016, the Evolution Group's Cayman Islands subsidiary, Evo Investment Advisors, was fined 9.2 million yen by Japan's Financial Services Agency (FSA) for manipulating the stock price of a Tokyo-listed company. The FSA's Securities and Exchange Surveillance Commission did not comment further on the matter.

In 2024, Evolution Japan Securities sued robot manufacturer Kuramoto Co. in Tokyo court, seeking 71 million yen in damages, alleging the company violated the warrant contract by issuing warrants to other third parties.

Kuramoto President Mamoru Komine said: 'Evo approached us to discuss cooperation, but we ultimately rejected their warrant proposal. Even though the contract was dissolved, they still filed a lawsuit.' The case is still under review, and Kuramoto has accrued the litigation as an estimated loss in its February financial report.

Several合作方 (cooperating parties) and former employees who wished to remain anonymous revealed that Lerch can become dominant and irritable under pressure, having been known to unexpectedly fire traders and lose his temper during business communications.

Last year's labor dispute in London also exposed his强硬偏执的处事风格 (tough and paranoid handling style). The court ruled that Evolution Capital Management无故克扣 (unreasonably withheld) bonuses from former employee Robert Gagliardi—who generated the vast majority of the company's revenue during his tenure. The group had previously argued that the employee's involvement in a US market investigation incident damaged the company's reputation. Text messages disclosed in the case files showed that Lerch had even insulted the employee.

Putting aside various controversies, Evo's rise reflects the普遍困境 (widespread predicament) faced by Japan's micro-cap listed companies: over 60% of Japan's listed companies are small or micro-cap stocks. As the TSE raises market capitalization listing requirements, a large number of companies urgently need capital infusion, making balancing the need for rapid fundraising with the rights of retail shareholders a棘手难题 (thorny problem).

Zhihua Yao, associate professor of economics at the University of Kitakyushu, believes: floating-strike warrants are a lifeline for underperforming companies; otherwise, they would struggle to attract investment. Market opinions on this tool are mixed, but the high-profile cooperation between Evo and Metaplanet will inevitably drive demand for such financing contracts across the market.

For Banka Investment's President Kameda, the risk of damaging shareholder interests far outweighs the benefits of cooperation, and he is unwilling to partner with Evo again. For the company's new round of warrant financing this March, he chose Hong Kong hedge fund Long Corridor Asset Management as the partner, stating that the new contract would prioritize protecting the rights of existing shareholders.

Kameda revealed that Evo still sends financing invitations to this day, but he一概拒绝 (flatly refuses them all). 'In different people's eyes, Lerch is both a savior and a scavenging vulture. These kinds of financing deals have always been a double-edged sword.'

(This article was written with assistance from: Jonathan Browning, Bailey Lipschultz, Finbarr Flynn, Wu Jin)