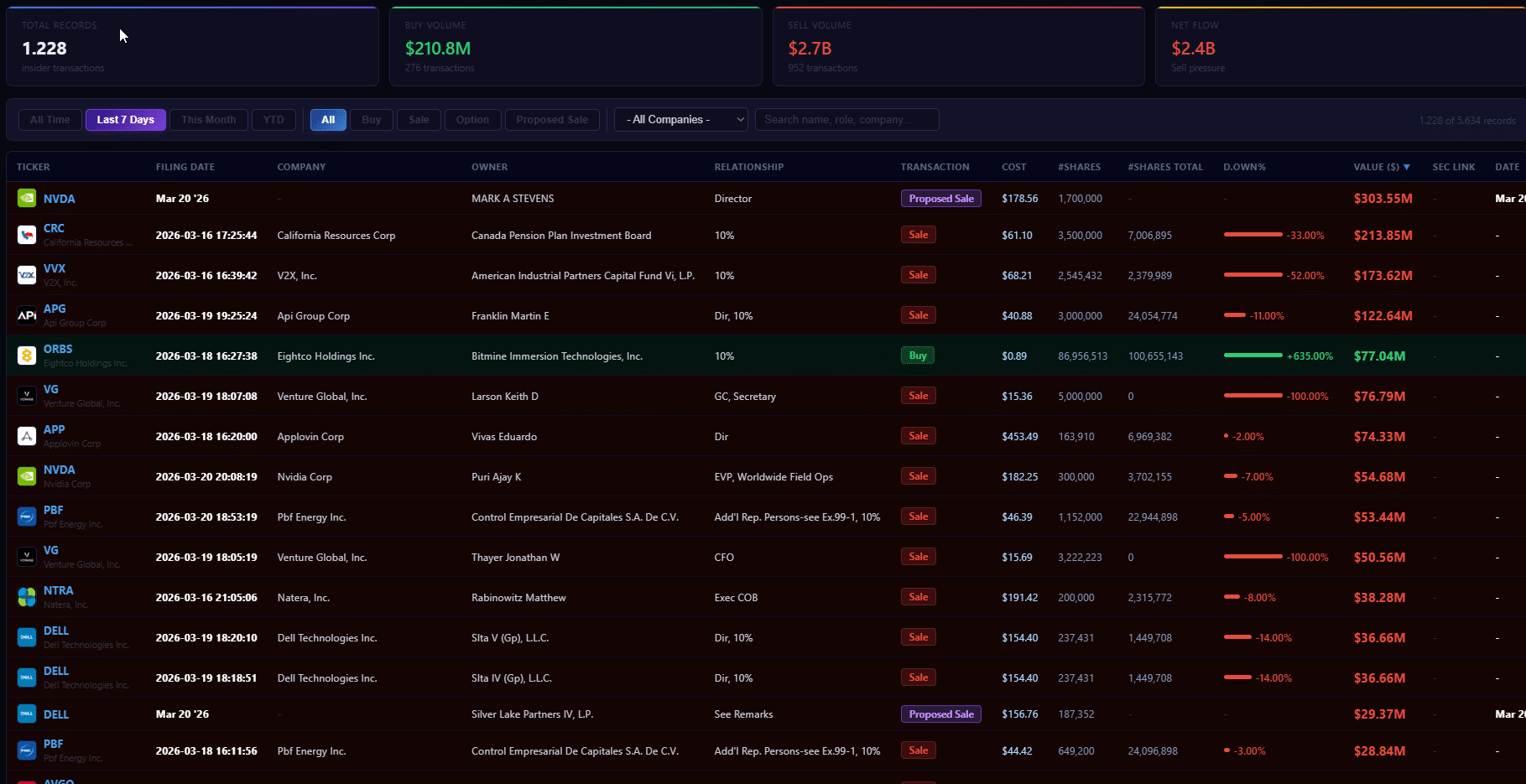

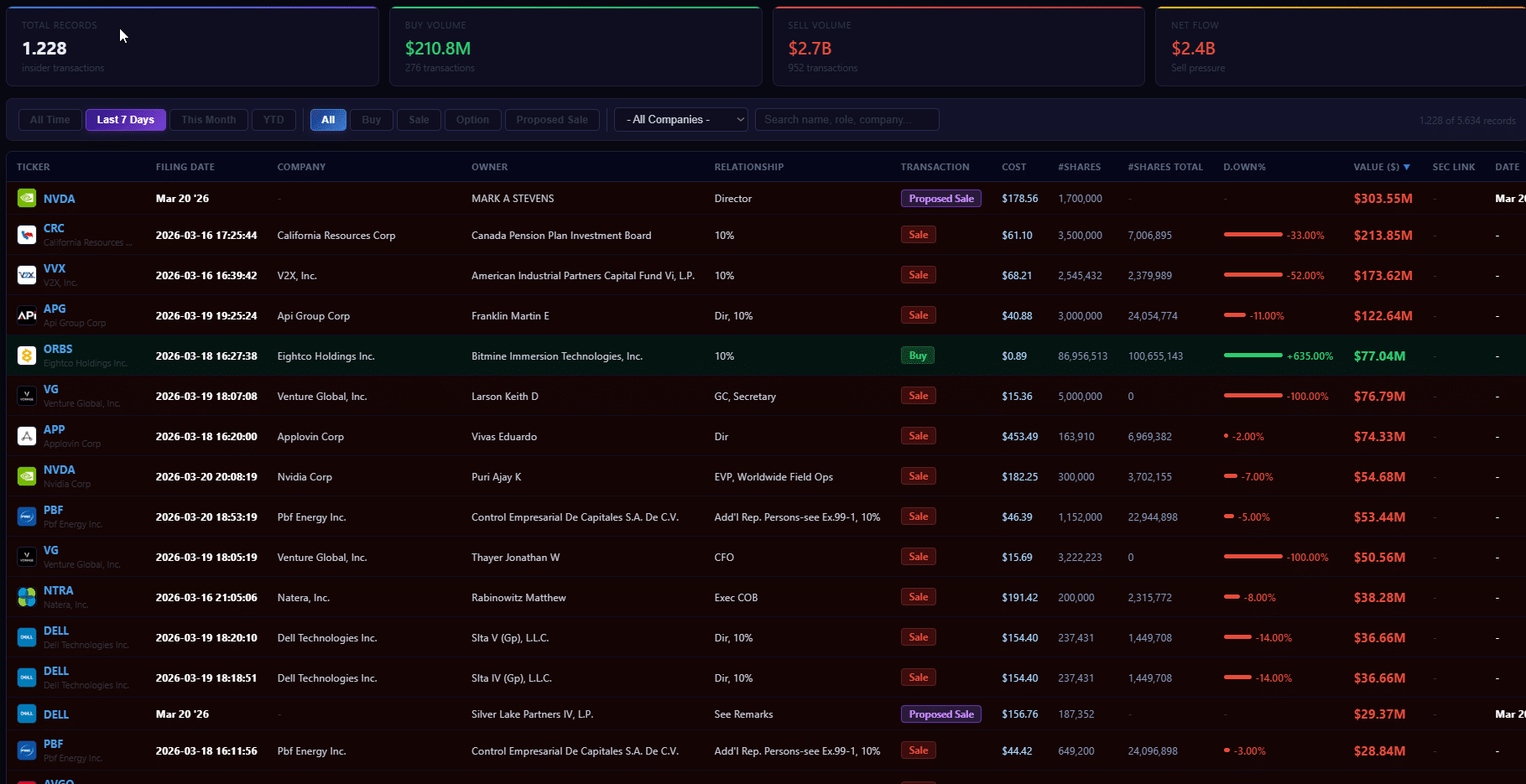

Insider distribution already signals weakening risk appetite, and liquidity behavior now reinforces that shift toward defense. Capital is not exiting markets entirely; instead, it rotates into safer instruments, leaving risk assets underbid despite easing supply pressure.

Stablecoin supply rises to $316.69 billion, up 0.26% weekly and 2.83% monthly, reflecting growing idle capital.

Tether [USDT] expanded to $184.1B and USD Coin [USDC] to $79 billion, while exchange inflows increasingly point to parking rather than deployment, which mirrors weak conviction.

At the same time, U.S. money market funds add $38.68 billion, pushing totals to $7.86 trillion. Government funds alone absorbed $40.55 billion, highlighting a clear institutional move toward safety and yield.

Short-term Treasury yields hold at 3.71% and 3.76%, sustaining this rotation, while Bitcoin [BTC] and Ethereum [ETH] flows remain neutral to negative, confirming liquidity stays sidelined.

Supply tightens, yet demand remains absent

Liquidity remains defensive, and Bitcoin net exchange flows show where capital is moving.

According to Glassnode data, 7,844 BTC have left the exchanges, as holders shift coins into self-custody wallets rather than keeping them liquid.

This movement reduces immediate sell pressure, yet it also reveals how demand is failing to engage. Instead of rotating into spot markets, capital stays inactive, which leaves the price without strong absorption.

Realized Profit reached $746 million, while BTC SOPR held near 1.01 and ETH at 0.96, showing participants take profits cautiously while avoiding aggressive re-entry.

This behavior confirms cautious profit-taking, showing capital is preserving gains rather than re-entering, leaving the price without strong support.

Final Summary

- Bitcoin [BTC] liquidity shifts defensively as 7,844 BTC moves into self-custody and SOPR near 1.01 signals profit-taking without redeployment, leaving markets underbid.

- Tether [USDT] and USD Coin [USDC] expansion alongside $7.86T in money funds shows liquidity parking in safety, reinforcing weak risk appetite and fragile structure.