Original | Odaily Planet Daily(@OdailyChina)

Author | Qin Xiaofeng(@QinXiaofeng 888 )

Today, Asian stock markets experienced violent fluctuations.

The South Korea Composite Stock Price Index (KOSPI) plummeted by over 8% intraday, triggering the market circuit breaker mechanism and halting trading for 20 minutes; it eventually closed down nearly 10% at 8203.84 points, marking the third-largest single-day decline record for the year. The Japanese stock market was also under pressure, with the Nikkei 225 Index falling approximately 3.5% to close around 69,788 points, ending its previous eight-day winning streak; the Tokyo Stock Price Index (TOPIX) declined about 2.6%.

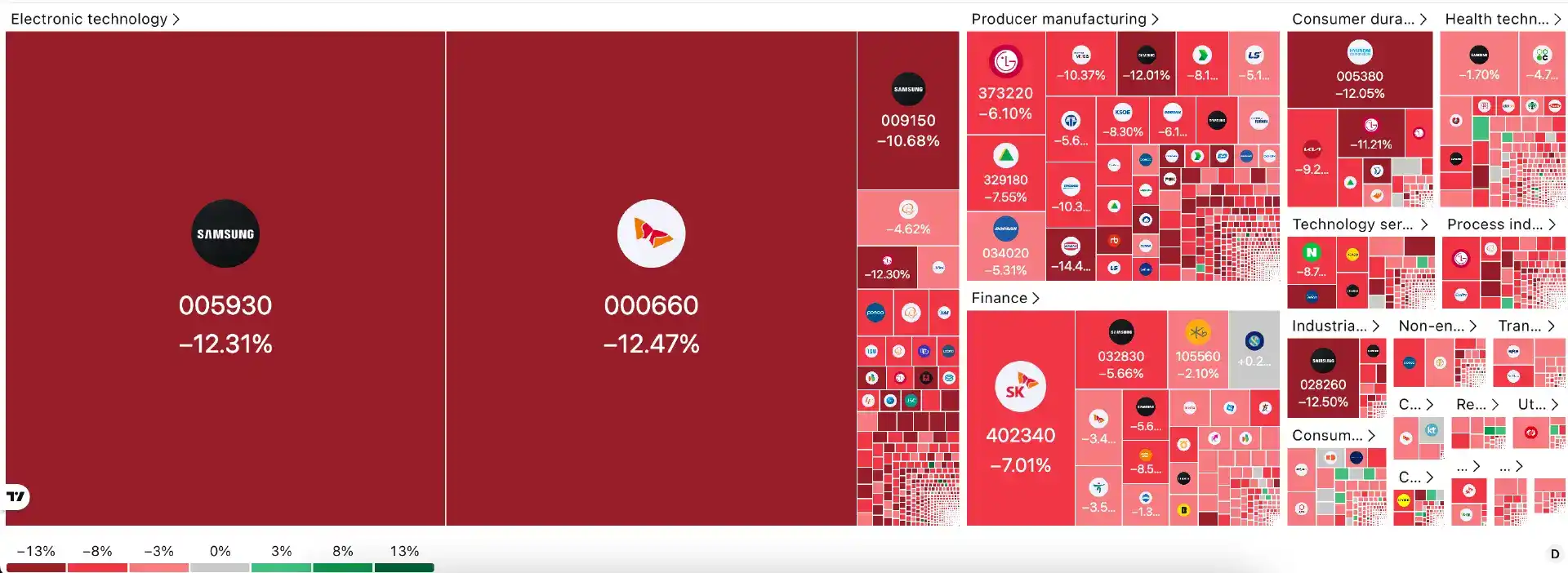

The technology sector, especially semiconductors, was the hardest hit in this adjustment, with heavyweights like Samsung Electronics and SK Hynix leading the decline and dragging down the entire market. Foreign capital accelerated selling, trading volume surged significantly, and market panic sentiment noticeably intensified.

Since June, Japanese and South Korean stock markets have experienced sharp volatility multiple times, with the South Korean market triggering circuit breakers four times this year. Previously driven by the AI and semiconductor boom, KOSPI once approached its all-time high of 9385 points; the Nikkei 225 also briefly stood above 70,000 points. In just a few weeks, the shift from historical highs to significant corrections highlights market fragility and profit-taking pressure. Odaily Planet Daily will analyze from three aspects: market performance, underlying causes, and future trends.

I. Market Plunge: From Historical Highs to Circuit Breaker Alerts

On June 23, KOSPI opened higher at 9083.54 points, once surging to 9175.45 points intraday. However, driven by foreign selling and follow-on selling pressure, the index quickly nosedived. Around 14:33 in the afternoon, a decline exceeding 8% triggered the circuit breaker mechanism of the Korea Exchange (KRX), suspending trading for all KOSPI constituent stocks for 20 minutes. A similar mechanism had been activated on multiple days such as June 5 and 8, indicating that volatility has become the norm.

At the close, KOSPI reported 8203.84 points, a single-day decline of 9.99%, with trading volume surging to 4.8371 billion shares. Semiconductor giants like SK Hynix and Samsung Electronics led the decline, both falling over 12%. The Korea Composite Stock Price Index (KOSDAQ) appeared even more fragile, falling in sync by over 6%, with small-cap tech stocks collectively declining. Net selling by foreign investors was significant, becoming the main source of selling pressure.

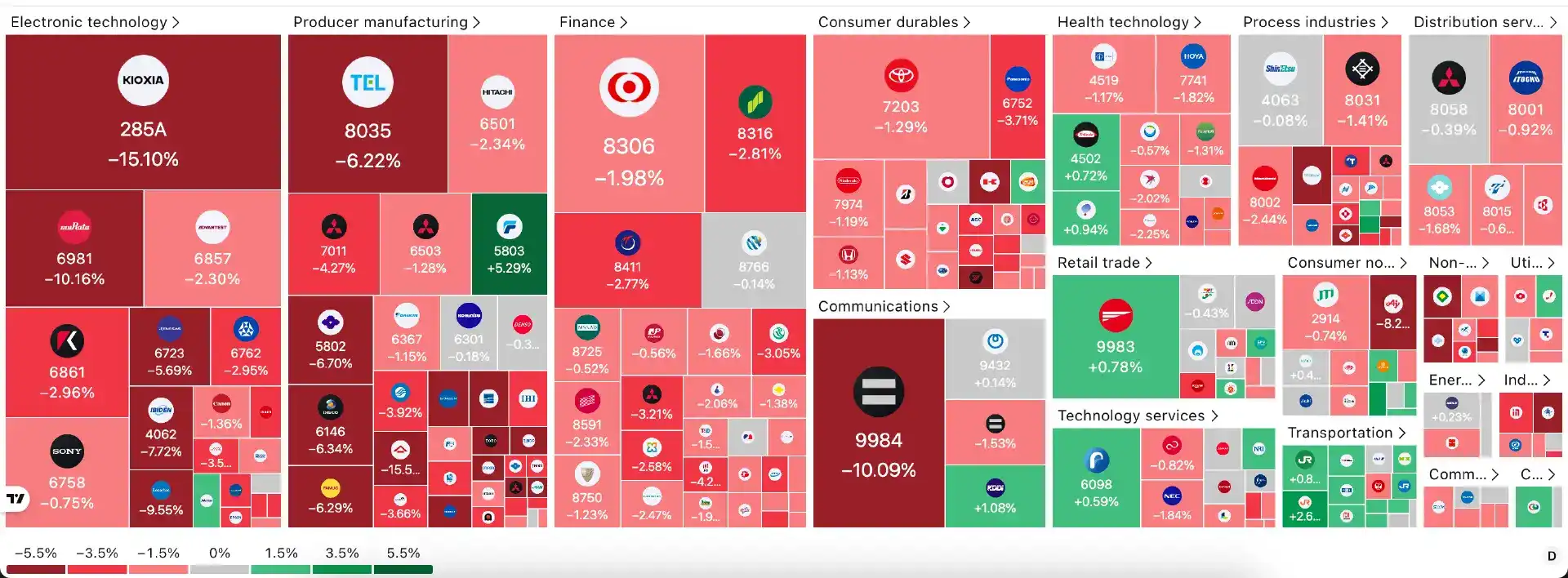

The Japanese market reaction was relatively moderate but still noteworthy. The Nikkei 225 Index fell over 3% intraday, closing at around 69,788 points, a single-day decline of about 3.47%, with the TOPIX falling in sync. Technology and semiconductor-related stocks performed the worst: SoftBank Group fell over 10%, chip manufacturer Kioxia plummeted 15.1%, and Tokyo Electron declined 6.2%. The AI and semiconductor sectors, which had previously driven the Nikkei's surge, underwent a comprehensive correction, ending the continuous upward momentum of eight trading days.

Compared to recent highs, the magnitude of this adjustment is astonishing. KOSPI has retreated over 12% from its mid-June peak, and the Nikkei 225 has corrected significantly from above 70,000 points.

Global market linkages were evident. U.S. tech stocks collectively faced pressure overnight, with the Nasdaq Index falling over 1% and the S&P 500 slightly retreating. Rotation occurred within the "Magnificent Seven," with stocks like Amazon and Meta leading the decline; other Asian markets, such as Taiwan's stock market, were also affected, forming a regional tech stock sell-off.

Overall, this was a fast and severe adjustment led by the technology sector, with the South Korean market experiencing far greater declines than Japan's due to its high concentration.

II. Cause Analysis: Phased Burst of the AI Bubble Under Multiple Overlapping Factors

The sharp decline in Japanese and South Korean stock markets is the result of the combined effect of multiple factors, which can be analyzed from the dimensions of direct triggers, macro policy pressures, and structural risks.

1. Direct Trigger: Overnight Weakness in U.S. Tech Stocks and Profit-Taking Pressure

Significant corrections in the U.S. technology sector the previous trading day directly transmitted to Asian markets. The Nasdaq Index fell over 1.2%, with notable rotation within the Magnificent Seven, and some individual stocks faced clear pressure.

Lisa Shalett, Chief Investment Officer (CIO) of Morgan Stanley Wealth Management, pointed out: "Rotation within the Magnificent Seven is evident, with news of departures by some executives or researchers exacerbating market concerns about the pace of AI commercialization. Investors are beginning to demand more evidence that massive AI capital expenditure can translate into sustainable profits."

This concern quickly spread to the Japanese and South Korean markets, which heavily rely on the global AI supply chain. South Korea's semiconductor exports account for over 20% of total exports long-term, with Samsung Electronics and SK Hynix together comprising about 40% of KOSPI's weighting. On June 23, these two giants fell approximately 8%-12%, directly dragging down the index.

Furthermore, Japanese and South Korean stock markets have accumulated substantial gains since June, resulting in extremely rich profit positions. The KOSPI index surged from around 5000 points at the beginning of the year to above 9000 points in mid-June, with a maximum year-to-date gain exceeding 80%; the Nikkei 225 also rose from around 40,000 points at the start of the year to above 70,000 points, setting a historical high. With valuations at high levels (KOSPI's forward P/E ratio once approached historical highs), any negative catalyst could easily trigger profit-taking. The concentrated selling on June 23 was a natural correction following the overly rapid gains.

2. Macro and Policy Factors: Heightened Fed Rate Hike Expectations and Impact of Economic Data

Consistently strong U.S. employment data has further fueled market expectations for the Federal Reserve to maintain high interest rates or even raise them. According to Reuters, non-farm payrolls increased by 172,000 in May, far exceeding economists' expectations of 85,000, with the unemployment rate stable at 4.3%. This data prompted some institutions (like Goldman Sachs) to postpone expectations for the first rate cut to 2027. More crucially, the Federal Reserve's FOMC meeting on June 16-17 decided to maintain the federal funds rate target range at 3.5%-3.75%. The statement emphasized robust economic expansion but noted increased uncertainty from Middle East conflicts, with inflation still above the 2% target.

The Fed's latest dot plot released a clear hawkish signal: the median forecast for the federal funds rate at the end of 2026 was raised to 3.8% (a significant increase of 0.4 percentage points from the March forecast of 3.4%), hinting at at least one rate hike within the year. Simultaneously, the FOMC raised its 2026 inflation forecasts: the median core PCE inflation rose to 3.3%, and overall PCE to 3.6% (both were around 2.7% previously); GDP growth forecast was slightly lowered to 2.2%.

Interest-rate-sensitive growth stocks (especially technology and semiconductors) bore the brunt. Previously seen as typical "high-beta" assets due to the AI boom, South Korean stocks are extremely sensitive to changes in global liquidity. Japanese stocks are also constrained by global liquidity expectations, although improved domestic wage growth data provided some support.

A series of macro signals significantly pushed up U.S. Treasury yields, exerting pressure on global risk assets and directly intensifying selling pressure on Japanese and South Korean tech stocks.

3. Structural Risks: Excessive Market Concentration and Foreign Capital Outflow

The structural fragility of the South Korean stock market is particularly prominent. KOSPI heavily relies on the two semiconductor giants, Samsung Electronics and SK Hynix. Once the semiconductor cycle or global AI demand fluctuates, the index experiences violent volatility.

Sustained foreign capital outflow is another key factor. Foreign investors reaped substantial profits during the previous rally, with net selling occurring multiple times since June, especially in South Korean stocks, as some funds may have shifted to U.S. IPO subscriptions (like SpaceX) or other assets. On June 23, the scale of net selling by foreign capital significantly amplified, becoming the primary source of selling pressure.

In contrast, although also dragged down by tech stocks, the Japanese market has relatively higher sector diversification, with the Nikkei 225 decline controlled at around 3.5%.

Additionally, specific corporate dynamics intensified market pressure. According to market news, SK Hynix recently adjusted its AI chip (particularly HBM) memory production capacity allocation, shifting some production lines to more profitable traditional DRAM to optimize short-term profits. This move raised investor concerns about short-term HBM supply-demand balance, triggering selling.

III. Future Outlook: Short-Term Volatility Unavoidable, Long-Term AI Narrative Remains Resilient

Looking ahead, Japanese and South Korean stock markets will exhibit characteristics of "volatile bottoming + structural differentiation." Short-term market volatility will remain high, while medium- to long-term fundamental support persists, with corrections instead providing a window for positioning in quality assets.

Short-term volatility dominates; recovery depends on U.S. stocks and Fed signals. In the short term, the market remains in a high-volatility adjustment phase. The trend of U.S. tech stocks is a key barometer. If the Nasdaq Index stabilizes or experiences a technical rebound, Japanese and South Korean markets are expected to follow suit in recovery; conversely, if the Fed releases further hawkish signals or Japanese and South Korean companies' Q2 earnings fall short of expectations, the correction may continue or even deepen. Key events to watch include:

- U.S. June-July inflation (CPI/PCE) and employment data;

- The Fed's next FOMC meeting (July);

- Q2 earnings of heavyweight stocks like Samsung Electronics, SK Hynix, and Tokyo Electron.

Medium- to long-term fundamental support is strong; corrections present opportunities. Global AI capital expenditure is still growing rapidly, and the underlying logic of the semiconductor supercycle remains unchanged. According to forecasts from institutions like Goldman Sachs, global AI-related capital expenditure (computing, data centers, power) from 2026-2031 will accumulate to approximately $7.6 trillion, with single-year AI CapEx in 2026 approaching $765 billion, rising year by year to $1.6 trillion in 2031; new data center capacity is expected to add nearly 100GW from 2026-2030, with total investment potentially reaching the $3 trillion level.

South Korea's leading position in HBM (High Bandwidth Memory) and advanced process technology remains solid. SK Hynix's HBM market share has long been maintained at 50%-62%, with its supply share for the NVIDIA Rubin platform potentially reaching around 70% in the HBM4 era; Samsung Electronics is also accelerating capacity expansion, planning to increase HBM production capacity by about 50% in 2026. Long-term orders for these two giants are basically locked in until 2027, and the AI memory demand supercycle is still in its early stages.

From a long-term perspective, AI remains a productivity tool that will reshape the world's landscape, and phased adjustments cannot reverse the major trend of technological progress. Just like corrections after every previous tech bubble, they ultimately leave rich rewards for true infrastructure builders and innovators. This "Black Tuesday" might just be the turning point where AI investment shifts from狂热 to rationality, from concept to practical industry. The resilience and potential of Japanese and South Korean stock markets remain worthy of expectation.