Written by: Thejaswini M A

Compiled by: Saoirse, Foresight News

When we think of competition, the phrase 'survival of the fittest' often comes to mind. Hearing it, I picture a brutal scene of everyone fighting each other: the strongest predator wins by eliminating all rivals.

But I've started to doubt that sustainable ecosystems are built this way. In the early 20th century, naturalist and philosopher Peter Kropotkin challenged this notion in his evolutionary essays on mutual aid. Kropotkin observed that species surviving extreme climate changes relied on sophisticated systems of collective cooperation. From a long-term evolutionary perspective, the power of mutual support far outweighs individual struggle. The true 'fittest' are those who know how to cooperate and build stable, shared frameworks to navigate unpredictable environments.

This principle applies across industries.

Right now, all crypto projects are finding their niche; protocols that weathered the bear market have made crucial choices for their future.

Some development teams are returning to their original core tenets, pursuing absolute censorship resistance and pure decentralization; others are adding centralized controls to maintain basic solvency; a few are building walled-garden ecosystems, funneling internal liquidity into isolated scaling chains.

ZKsync has taken a distinctly different path, centered on mutual aid: it is building infrastructure for banks.

The Boston Consulting Group (BCG) predicts the tokenized asset market will fully migrate to blockchain systems, reaching $10-16 trillion by 2030. Major mainstream banks are already running pilots, with some moving from trials to full-scale operations. The infrastructure solutions being chosen now will determine the flow of trillions in capital and who controls the underlying rails.

ZKsync is now a highly competitive Layer 2 solution for these financial rails. Even if you haven't looked at Layer 2 since the last bull run, its trajectory is worth noting.

Why are banks moving into blockchain? And why specifically ZKsync?

The ZKsync environment used by Deutsche Bank is completely segregated from regular crypto users. The bank relies on ZKsync's Prividium suite, with Memento building a private, permissioned Layer 2 network—Memento ZK Chain.

Prividium is ZKsync's commercial product for institutions, supporting private transactions, tiered access controls, built-in compliance tools, with all transactions ultimately settling on Ethereum. Memento compared and tested five blockchain ecosystems before choosing ZKsync. This solution shortened capital deployment timelines from two-to-three months down to two-to-three weeks.

The core reason banks favor zero-knowledge technology: it can prove a statement is true without revealing the underlying private information. Banks can verify transactions without disclosing sensitive details like counterparty names, amounts, or specific assets to the public. This privacy architecture gives banks full control over data visibility, protecting corporate secrets while providing clear evidence to regulators, perfectly fitting Wall Street's existing operational models.

The Tradable platform already hosts $1.7 billion in private credit products on ZKsync, listing nearly 30 institutional-grade investment vehicles with 8% to 15.5% annual yields. In October 2024, Buenos Aires, the capital of Argentina, quietly migrated its entire city-wide digital identity system to ZKsync Era, giving 3.6 million citizens officially recognized, crypto-protected identity credentials overnight, with local governments unable to trace the data—making it the first city globally to deploy such an application.

By the end of 2025, the global private credit market reached $3.5 trillion, while Tradable's volume represents less than 0.05% of that total. The tokenized credit sector will either capture significant market share or remain niche, but current data shows it's on a growth trajectory. Regardless, a vast gap remains between current on-chain capital and the overall market size.

Consider the decision from a corporate risk team's perspective: they have three options—a completely self-controlled, isolated private network; a contractual enterprise consortium; or a public network governed by an online community.

JPMorgan's Kinexys is an example of a fully internal, private network. Since 2019, this operation has independently built a blockchain system, handling repo trades, cross-border payments, and asset settlement with partners like BlackRock and Siemens. JPMorgan runs its own servers, manages the ledger, and has no interaction with the public crypto community. Fees don't change arbitrarily based on token holder votes, system upgrades follow internal planning, and governance is entirely in JPMorgan's hands.

But the bank's own data reveals this model's weakness: Kinexys processes about $5 billion in daily transaction volume, while JPMorgan's payment division handles $10 trillion daily. Five years after launch, its own blockchain business carries only 0.05% of the bank's payment traffic. The bank with the highest level of infrastructure control has the lowest adoption rate. Full self-control hasn't solved the core problem of scaling.

Another competitor, R3 Corda, has cleared $10 billion in tokenized real-world assets and processes one million transactions daily. It's a consortium of over 200 financial institutions, with all rules agreed upon via contracts before launch; to update features, all members must sign off. Every bank gets a seat at the rule-making table before the first transaction settles.

These platforms are ZKsync's competitors, but ZKsync has unique advantages that dedicated consortium or private chains cannot replicate: publicly verifiable transaction validity without leaking private data, coupled with a settlement layer independent of any single corporate entity's survival. If a firm shuts down its internal blockchain tomorrow, on-chain assets are immediately at operational risk; assets anchored on ZKsync ultimately settle on the Ethereum mainnet, with no corporate executive who can order the network shut down. This underlying isolation is its core differentiating advantage, but balancing this with the risks of open governance remains an ongoing industry debate.

Before pivoting fully to institutional business, ZKsync launched an incentive program called Ignite, subsidizing DeFi protocols to maintain on-chain activity. After the strategic shift, the project terminated Ignite, clearly refocusing on enterprise clients, and on-chain activity declined along with the incentives.

Around the same time, the original network ZKsync Lite, launched in 2020, was permanently shut down. Matter Labs signaled this as early as December 2025 and announced the exact shutdown date in late February the following year. User assets remain withdrawable permanently, and no institutional deployments were built on ZKsync Lite, so they were unaffected.

The leading lending DeFi protocol, Aave, proposed shutting down its lending market on ZKsync Era, citing dismal revenue data: over 30 consecutive days, ZKsync generated only $714 in fee revenue for Aave. In contrast, Base chain brought in $300,000, and Ethereum mainnet a staggering $7.7 million during the same period. The governance forum concluded this Layer 2 chain didn't truly meet retail DeFi market demand and proposed a new rule: Aave would only consider deploying a market on any public chain generating at least $2 million in annual fee revenue.

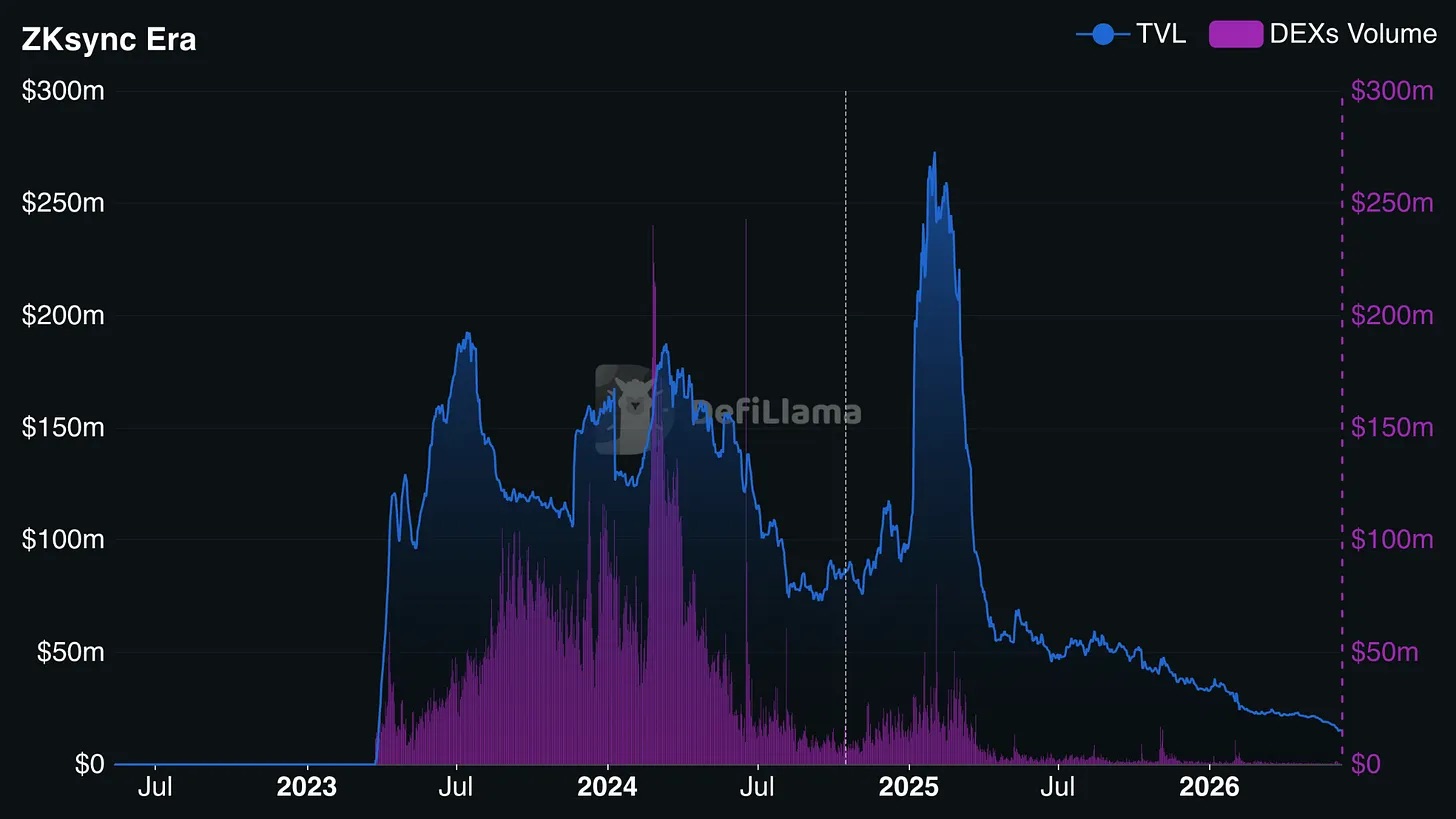

At the peak of the retail Layer 2 scaling frenzy, ZKsync Era's Total Value Locked (TVL) consistently held at several hundred million dollars; now, its public DeFi ecosystem TVL is only about $15 million. In comparison, top retail-focused Layer 2 networks typically have TVLs in the tens of billions.

After launching in 2023, ZKsync Era's on-chain TVL (blue line) and DEX volume (purple bars) peaked in early 2025 before sharply and continuously declining, with retail DeFi activity becoming extremely low by 2026. Source: @defillama.com

If the retail ecosystem continues to wither, the chain's entire development will bet solely on the institutional business line. Is a Layer 2 network a retail crypto playground gradually infiltrated by banks, or merely an enterprise financial rail settled on Ethereum? The answer will determine ZKsync's ultimate fate.

Earlier this year, Matter Labs CEO Alex Gluchowski publicly revealed a roadmap clearly refocusing the project on building heavy-duty financial infrastructure for traditional markets.

Product evolution confirms this: the team first launched Prividium, creating segregated environments for banks with non-leaking transaction data; then launched the Bank Stack suite, partnering with institutions like Cari Network to onboard regional banks managing hundreds of billions in traditional deposits. So Aave's departure wasn't a surprise to the development team.

As for Cari Network's rollout plan: led by former US Office of the Comptroller of the Currency officials, it plans to pilot with five regional banks next quarter, which collectively hold over $600 billion in deposits.

If this pilot succeeds, the transaction volume gap left by departing retail DeFi apps will be completely filled by banks' massive flows; but if it fails, ZKsync will become an technologically advanced yet experimental tool with no real mainstream users, hosting only a handful of corporate pilot projects.

The v31 protocol upgrade, passed via ZKsync governance forum vote, officially went live in early May.

ZKsync's official X account posted a reminder: this protocol upgrade was submitted to the governance forum for review. The v31 upgrade includes several core updates, using the ZK token as a universal pricing unit to enable native interoperability across all ZK-based scaling chains.

Key announcement points: This ZKsync Improvement Proposal (ZIP-16) was submitted for forum vote:

- ZKsync Interoperability Protocol: Enables native cross-chain interaction for all ZK-based scaling chains;

- Phase 1 supports scaling chains that can settle on Ethereum Layer 1;

- Expands ZKsync OS compatibility.

Under v31 rules, each cross-chain call between different ZK chains costs a flat fee of 10 ZK tokens, a rate set by DAO vote. Banks already constantly deal with variable costs—like blockchain gas fees, cloud computing costs, foreign exchange spreads—so such fluctuating costs are a normal part of business.

Not just the fee rate, but the entire fee mechanism can be rewritten via the same governance forum, with no obligation for the project to pre-notify institutional partners on the chain.

The ZK Nation governance forum is already discussing next-stage adjustments, currently debating node operator transaction fees, staking rules, and customized pricing for zero-knowledge proof verification. Any topic could trigger a community vote, altering the cost model for all cross-chain operations of institutions like Deutsche Bank and Tradable. All discussions are publicly viewable at forum.zknation.io.

In contrast: JPMorgan's Kinexys system permissions are entirely in its own hands; R3 Corda's rule changes also have formal contracts specifying amendment conditions and processes.

So why would banks choose ZKsync over JPMorgan's private chain? Because ZKsync can provide publicly verifiable proof of transaction validity without leaking private data.

If JPMorgan shuts down its blockchain business tomorrow, all on-chain assets would be frozen; even if Matter Labs, the development company behind ZKsync, goes bankrupt, the network can still run because all assets are ultimately anchored to Ethereum for settlement. But the price for this underlying security is accepting the network belongs to no single entity. An ownerless network's governance belongs to all participating token holders who vote.

The ZK token currently trades around $0.01, having hit an all-time high of $0.3285 in June 2024, a 96% drop from its peak. At a 10 ZK token cross-chain fee, a transaction cost about $3.28 at the bull market peak, now just $0.10. Token price volatility can be managed through hedging, but a community-voted mechanism that can change rules at any time makes long-term, stable budgeting difficult for corporate financial planning.

Layer 2 rating agency L2Beat classifies ZKsync Era as a Stage 0 network: an independent security council can bypass the full DAO voting process to directly pause or modify smart contracts. Mature Stage 1 Layer 2 networks like Arbitrum lack such centralized intervention powers. Enterprise risk managers often favor emergency kill switches to mitigate losses from smart contract bugs; but this control resides with a Web3 security council, completely outside traditional corporate management structures.

Sygnum tokenized $50 million of Matter Labs' corporate treasury assets on ZKsync, connecting to a Fidelity liquidity fund; subsequently, Fidelity also launched an institutional money market fund on the network. The development team injected initial transaction volume by deploying its own capital, creating core enterprise use cases. This asset flow operates smoothly, but the entire business setup directly serves the project's founding team.

The core infrastructure remains subject to an independent security council holding the highest system permissions. In emergencies, the council can bypass normal delay processes entirely, modifying smart contract parameters or freezing functions without prior notice. Actual network control is split between the security council and the active token governance community, meaning partnering banks must operate within a continuously dynamic governance system, not a fixed corporate cooperation agreement.

ZKsync is betting its entire existence on a group that has never led crypto project development—licensed traditional financial institutions. Banks don't care about token prices, nor will they participate in governance forum votes.

But once a bank chooses a core infrastructure to build its business on, it often becomes deeply embedded and difficult to migrate. This adoption path has higher initial barriers, but once established, it's hard to replace.

ZKsync will either become the first crypto project to achieve this, or serve as an expensive case study proving banks ultimately choose to build their own blockchains, then abandon external public chain solutions. The market will deliver its verdict within the next 18 months.

In crypto, many projects boast strong technology but falter on governance mechanisms and long-term sustainability, eventually fading away. ZKsync's grand experiment in governance models is still ongoing.