Source: Wall Street News

A report from the star AI industry chain analysis firm SemiAnalysis, which directly pointed to delays in two core technological pathways for AI data centers, ignited severe volatility in the optical communication sector on June 10th, simultaneously sparking intense debate about future technology roadmaps and investment opportunities in both the investment and industrial communities.

The report suggests that NVIDIA's 800VDC power architecture shipments will be delayed until 2028, and the mass production of CPO (Co-Packaged Optics) may be postponed to 2028 or even 2029. The simultaneous downward revision of these two expectations caught the market off guard.

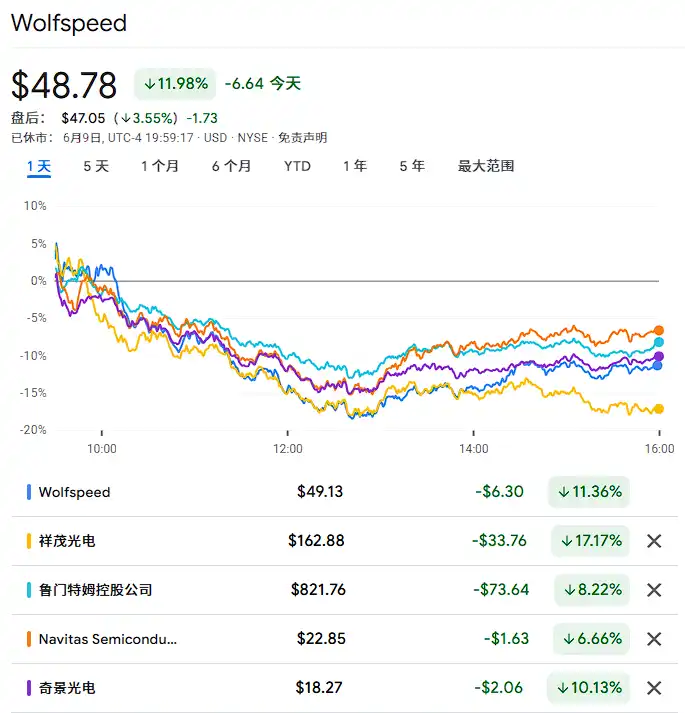

After the news broke, the US stock market's optical communication sector generally suffered heavy losses. Applied Optoelectronics (AAOI) plummeted by 17% in a single day, Lumentum fell by about 8%, and companies mentioned in the report as warranting caution, such as Himax Technologies (HIMX), Navitas Semiconductor Corp, and Wolfspeed, also faced significant pressure.

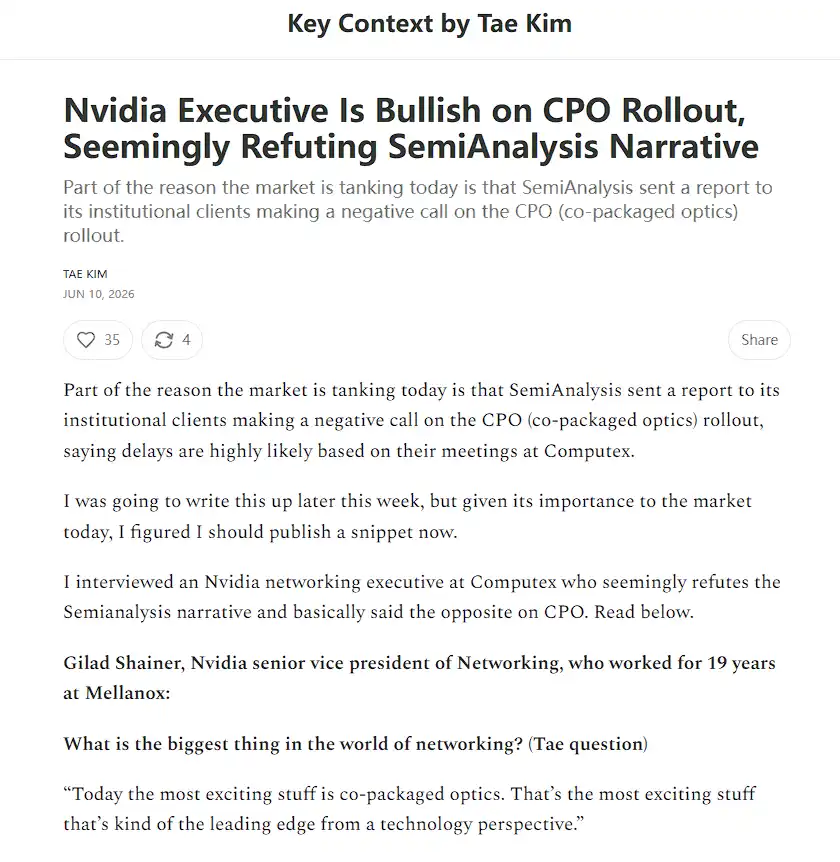

Concurrently with the release of the SemiAnalysis report, interview content with an NVIDIA executive was also published. According to资深半导体和科技投资记者Tae Kim, NVIDIA's Senior Vice President of Networking, Gilad Shainer, expressed a starkly optimistic stance on CPO's prospects at the 2026 Computex exhibition, stating directly that "CPO is the most exciting technology right now," and announced that volume shipments would begin in the second half of the year. This sparked a heated online debate about the CPO timeline on social platforms.

Notably, several market observers pointed out that the CPO delay does not mean the demand for optical interconnects disappears, but rather it is more likely to redirect capital flows back to traditional pluggable optical modules and the NPO (Near Package Optics) track — this logic led some investors to seek opportunities among oversold stocks during the panic selling.

SemiAnalysis Report Core: Dual Delays in Two Technological Pathways

In this research note distributed to institutional clients, SemiAnalysis presented two core judgments with profound market impact.

800VDC Power Architecture Delayed Until After 2028.

The report indicates that NVIDIA's originally planned large-scale adoption of a single-ended 800VDC power design has seen its shipment window significantly pushed back. Hyperscale cloud providers are currently more inclined to stick with mature low-voltage solutions or gradually transition to 400VDC, rather than rushing to switch to 800VDC.

The report argues that the marginal efficiency gains of 800VDC under current grid power supply conditions are insufficient to justify its system complexity. In contrast, 400VDC products are expected to start ramping in Q2 2026, with significant growth in 2027.

CPO Mass Production Timeline Lags Significantly Behind Market Expectations.

The report states that CPO shipment volumes in 2027 will be substantially lower than previous aggressive forecasts, and the timeline for mass production may be delayed until 2028 or even 2029. The main bottlenecks are concentrated at three levels:

Optical engine connection yield (optimistically around 95%, but CPO production driven by a single ASIC remains extremely limited), ASIC integration difficulty, and overall cost economics.

Scale-out CPO switch shipment volumes face downward revision risks, and shipments of Sidecar relying on new platforms like Rubin Ultra/Kyber are also postponed to a 2028 window.

At the individual stock level, SemiAnalysis maintains a relatively positive view on companies like Amphenol, Vertiv, and Legrand, while adopting a cautious stance towards Lumentum, Himax Technologies, Navitas Semiconductor, and Wolfspeed.

However, the report itself acknowledges that CPO, as an important direction for future data center network architecture, is not denied; the core reason for the delay lies in unresolved engineering challenges, not disappearing demand.

Simultaneously, the report also points out that some NPO (Near Package Optics) projects may accelerate.

NVIDIA Executive Publicly Counters, Tae Kim's Exclusive Interview Draws Attention

Just as the SemiAnalysis report was widely circulated among institutional circles,资深半导体和科技投资记者Tae Kim published an excerpt from a one-on-one interview with NVIDIA's Senior Vice President of Networking, Gilad Shainer, during Computex in his Substack column. The content starkly contrasted with SemiAnalysis's assessment.

Shainer stated in the interview, "The most exciting thing today is co-packaged optics, it's the leading edge of technology."

He further revealed that NVIDIA is ready to start shipping, that partner Lambda had published a blog confirming receipt of CPO switches, that volume shipments of CPO would accelerate in the second half of the year, extending from scale-out to scale-up scenarios. "If it were up to me, I would put CPO everywhere that we use optical networking."

Tae Kim added in his article that Shainer's overall demeanor and body language during the interview showed high enthusiasm for both near-term and long-term ramp-up of CPO. He stated that this statement "seems to directly contradict the narrative from SemiAnalysis."

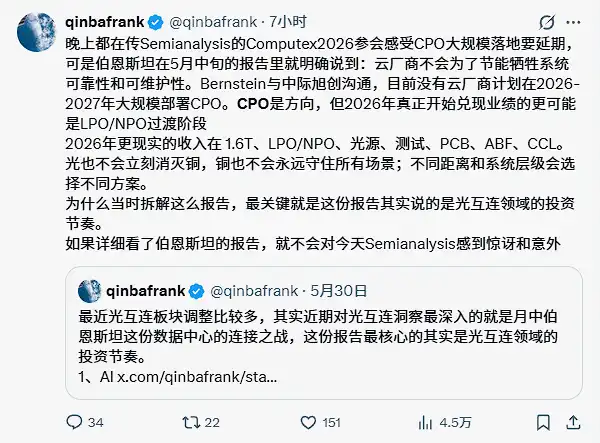

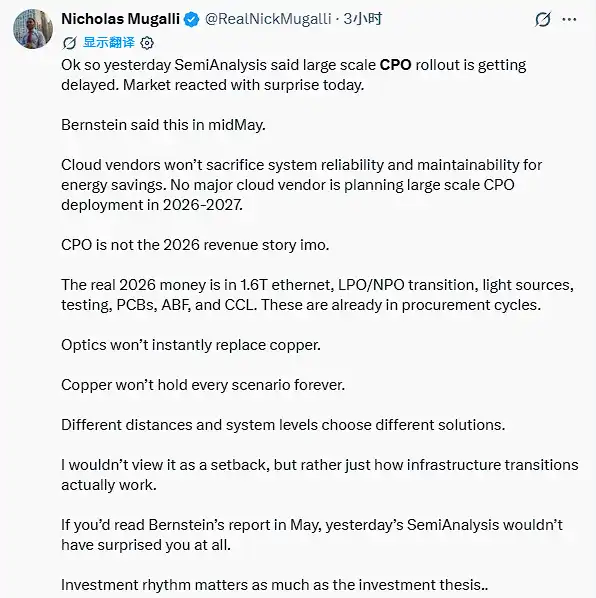

This discrepancy plunged the market into an information war. User @qinbafrank on social platform X pointed out that Bernstein had already clearly stated in a mid-May report that cloud providers would not sacrifice system reliability for energy savings, and that no cloud provider currently plans large-scale CPO deployment in 2026-2027. "If you had read the Bernstein report in detail, you wouldn't be surprised by SemiAnalysis today."

Online Debate: Is CPO Delay a Negative or a Market Overreaction?

The market volatility triggered by the report quickly spread to social media, where opinions on the investment logic surrounding the CPO delay diverged significantly.

Bearish View: Yield and Reliability Are Real Bottlenecks.

SemiAnalysis emphasized in its report that in the CPO architecture, the optical engine is co-packaged with a large ASIC worth tens of thousands of dollars on the same substrate. If the optical engine fails due to laser aging or fiber damage, it often requires the entire motherboard to be disassembled and returned to the factory. The maintenance cost and downtime risk are far higher than with traditional pluggable modules. This engineering challenge is considered the core obstacle preventing large-scale CPO adoption in the short term.

Bullish View: CPO Delay Actually Benefits Pluggable Modules and NPO.

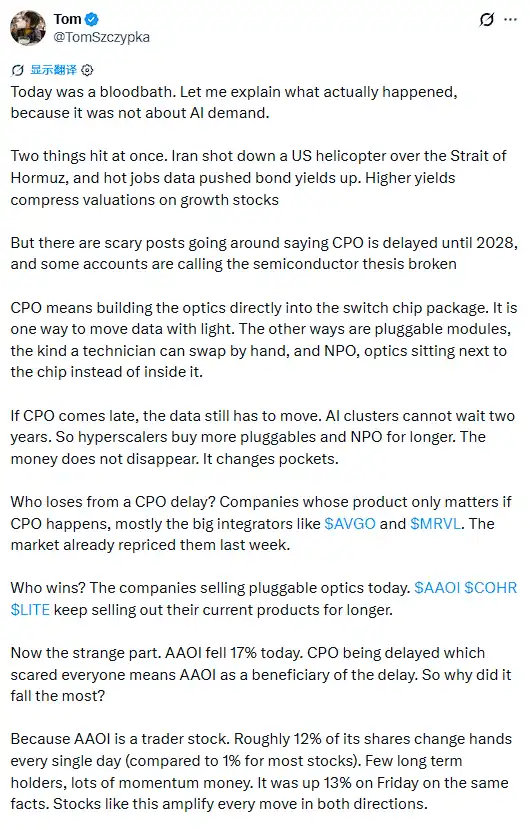

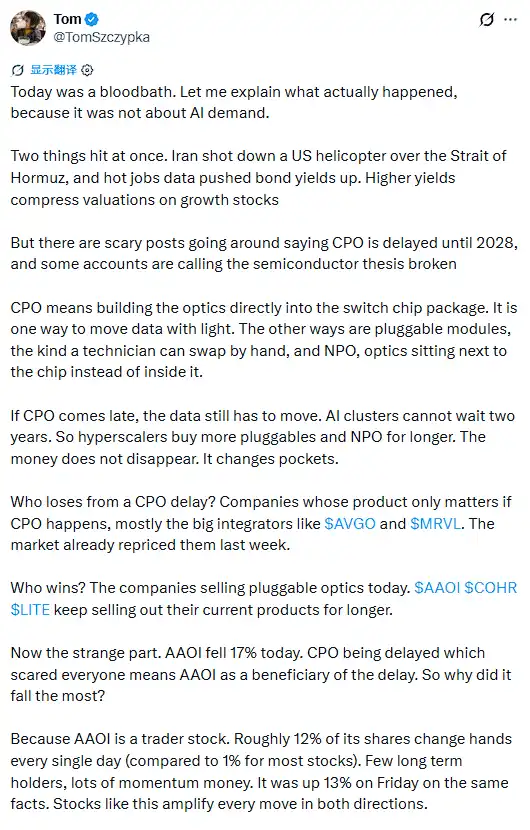

User @TomSzczypka on social platform X analyzed, "If CPO comes later, data still needs to be transmitted, AI clusters can't wait two years, hyperscalers will buy more pluggable modules and NPO for longer. The money doesn't disappear, it just changes pockets."

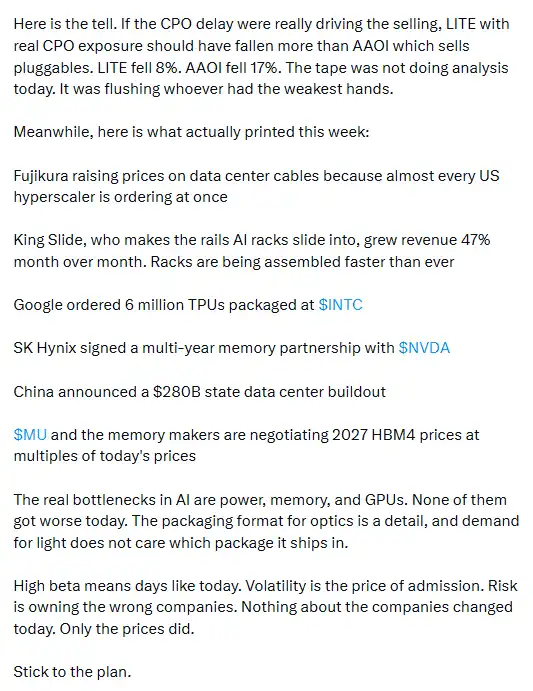

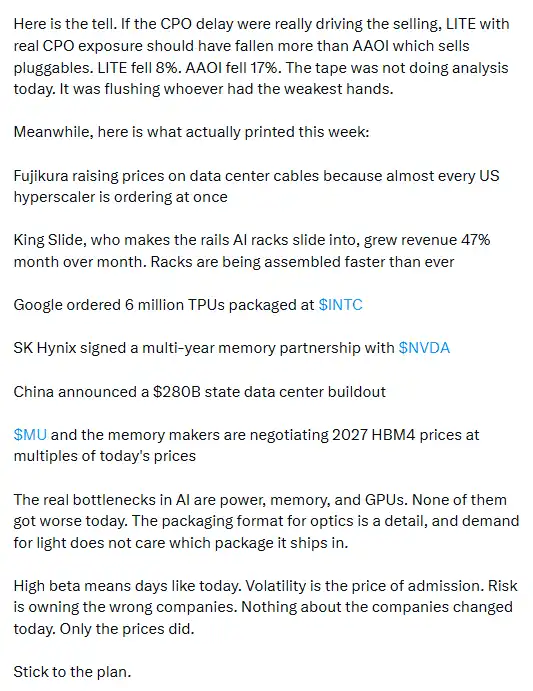

He also pointed out that the fact that Applied Optoelectronics' decline (17%) far exceeded Lumentum's (8%) on that day itself indicated that the market's sell-off was not based on rational analysis but was flushing out the weakest holdings.

User @michaelsikand stated that currently, revenue from CPO for any photonics company is zero, and the current high growth comes from the huge, unmet NPO opportunity. "The timeline may slip, but the TAM doesn't."

Voices questioning the report's logic also exist.

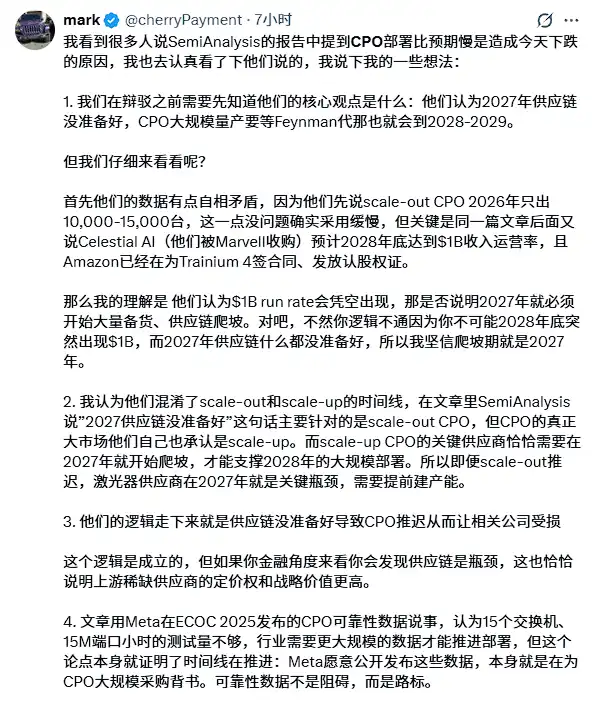

User @cherryPayment posted a lengthy article pointing out internal contradictions in the SemiAnalysis report: on one hand, it says the supply chain won't be ready in 2027; on the other hand, it predicts Celestial AI (acquired by Marvell) will reach a $1 billion revenue run rate by the end of 2028, and Amazon has already signed contracts for Trainium 4. "You can't suddenly have $1 billion by end of 2028 with the supply chain not ready for anything in 2027."

He also pointed out that SemiAnalysis's target audience is the procurement decision-makers at hyperscale cloud providers, and its conclusion is "no need to all-in yet," not an investment timing judgment for the capital market. "They are analyzing deployment pace, not investment timing."

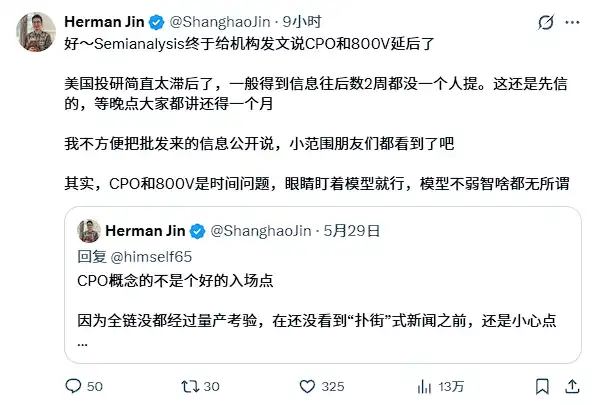

User @Herman Jin on platform X criticized the timeliness of information from US investment research firms, arguing that delays in CPO and 800VDC were "a matter of time," and such information had long been circulating in institutional circles; the SemiAnalysis report merely formalized known information on paper.

Unexpected Beneficiaries: Copper Connections and Pluggable Modules

Against the backdrop of widespread market pressure, some analysts turned their attention to potential beneficiaries of the CPO delay.

User @qinbafrank梳理认为,梳理认为梳理认为梳理认为,梳理认为梳理认为梳理认为 the more realistic revenue opportunities in 2026 are concentrated in 1.6T pluggable modules, LPO/NPO, light sources, testing, PCB, ABF, and CCL segments. "Optics won't eliminate copper immediately, and copper won't hold onto all scenarios forever; different distances and system levels will choose different solutions."

The CEO of Lumentum also recently stated that interest in NPO from non-NVIDIA customers has increased noticeably over the past two months.

User @RealNickMugalli analyzed that at 1.6T rates and 200G per channel, copper cables, even with retimer technology, have reached their physical limits. Optical solutions become a mandatory option, not an optional one, within reasonable distances, and the potential market size for NPO might even exceed that of CPO.

SemiAnalysis also noted in its report that some NPO projects may accelerate, and 400VDC products will start ramping in Q2 2026. For companies like Amphenol and Vertiv, the report maintains a relatively positive stance, believing they benefit from sustained demand during the 400VDC transition.

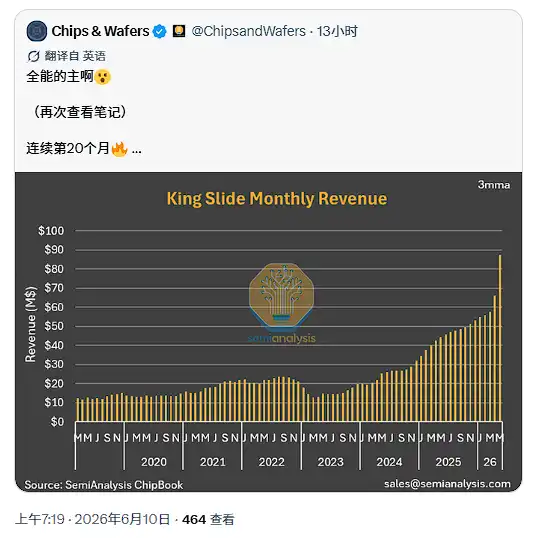

User @TomSzczypka cited this week's industry chain data to support that AI infrastructure demand has not weakened:

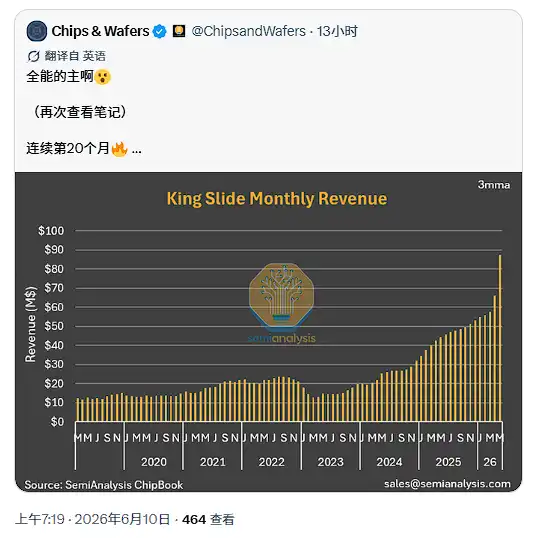

Fujikura raised prices for data center cables because almost all US hyperscalers placed orders simultaneously; King Slide's rack rail revenue increased 47% sequentially; Google ordered 6 million TPUs from Intel; SK Hynix signed a multi-year memory supply agreement with NVIDIA, etc.

"The real bottlenecks for AI are power, memory, and GPUs. None of these three have gotten any worse today."

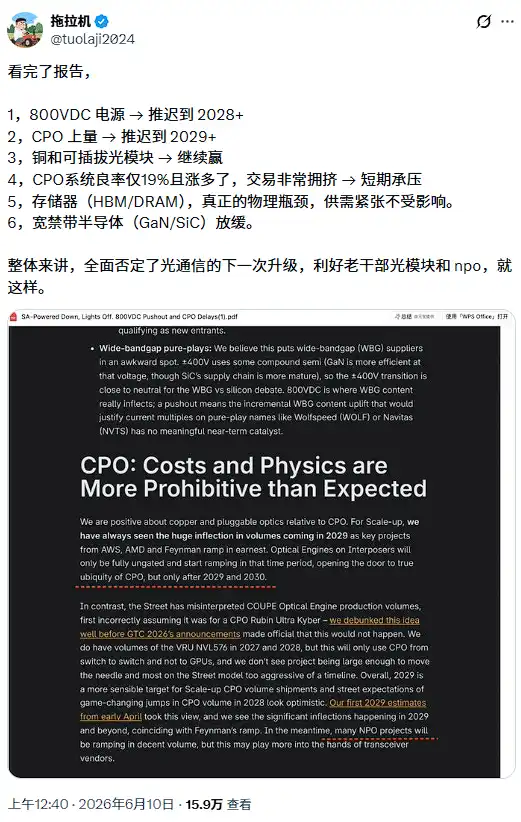

Meanwhile, @tuolaji2024 posted on social platform X, stating that memory (HBM/DRAM), as the real physical bottleneck, remains completely unaffected by this technology delay event.

Analysis points out that, synthesizing various viewpoints, the market volatility triggered by this SemiAnalysis report reflects more of a recalibration of the technology roadmap timeline, rather than a fundamental reversal of overall AI data center demand.