Австралия стала ближе к токенизации, поскольку Резервный банк Австралии (RBA) изложил свой следующий этап.

На форуме «Beyond Tomorrow» 25 марта помощник управляющего Брэд Джонс заявил, что фокус сместился с вопроса «будет ли» на вопрос «как» будет реализована токенизация.

Он заявил:

Во-первых, мы больше не считаем главным вопросом, есть ли у токенизации будущее в финансовой системе Австралии, а скорее, как это будет реализовано.

Как будет реализована токенизация

Австралия, по всей видимости, готова продвигать токенизацию across различных классов активов, с акцентом на обеспечение круглосуточной торговли.

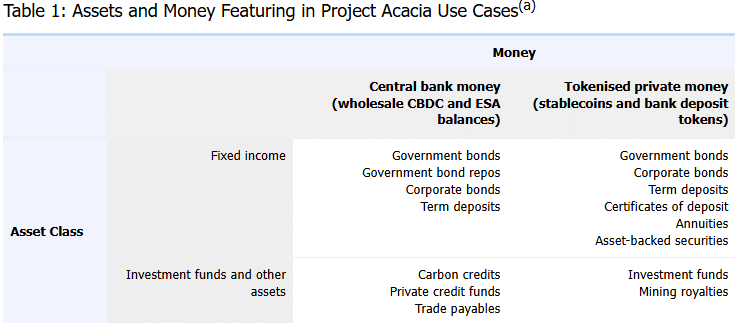

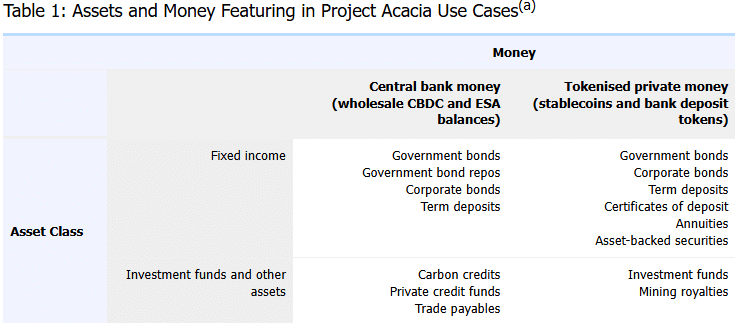

На сайте RBA Джонс подробно изложил выводы проекта Acacia, который прогнозирует ежегодный прирост эффективности в размере 16,7 миллиардов долларов.

Центральный банк отметил, что стейблкоины и банковские депозиты могут сосуществовать в системе.

Пилотный проект охватил инструменты с фиксированным доходом и инвестиционные фонды, при этом транзакции проходили как через деньги центрального банка, так и через токенизированные частные деньги.

К ним относятся государственные облигации, корпоративные облигации, углеродные кредиты и фонды частного кредитования.

Тем не менее, RBA подтвердил, что будет работать с Советом финансовых регуляторов (CFR) и DFCRC для поддержки реализации.

Такая координация может ускорить развитие рынка стейблкоинов Австралии и цифровой экономики в целом.

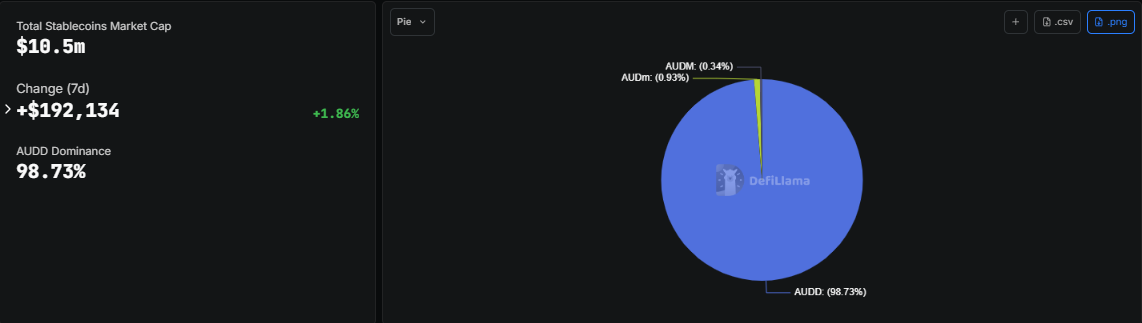

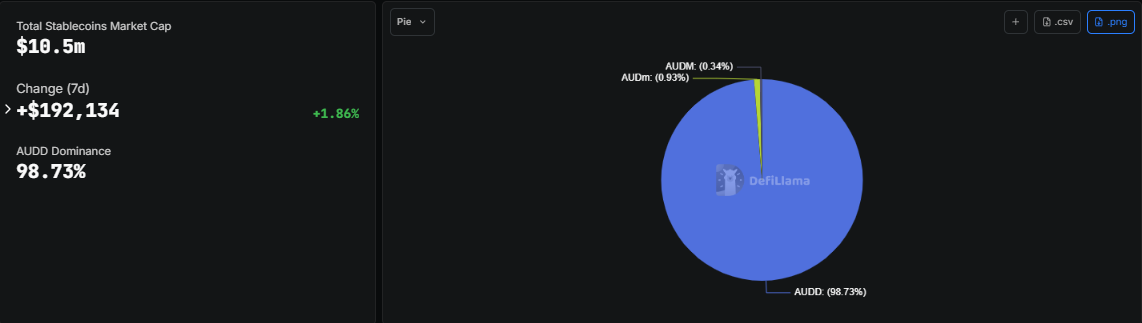

Рыночная капитализация стейблкоинов в австралийских долларах [AUD]

Что касается рыночной капитализации стейблкоинов в австралийских долларах, то она относительно низка, вероятно, из-за регуляторных препятствий до шага RBA.

Согласно данным DeFiLlama, их общая рыночная капитализация составила 10,5 миллиона долларов, что на 1,86% больше, чем на прошлой неделе. В этом списке лидирует AUDD с долей 98,73%, что эквивалентно 10,35 миллионам долларов.

Другими в списке были AUDm и AUDM, на которые приходится 0,93% и 0,34% от общей капитализации соответственно. Их совокупная капитализация составила около 133 тысяч долларов.

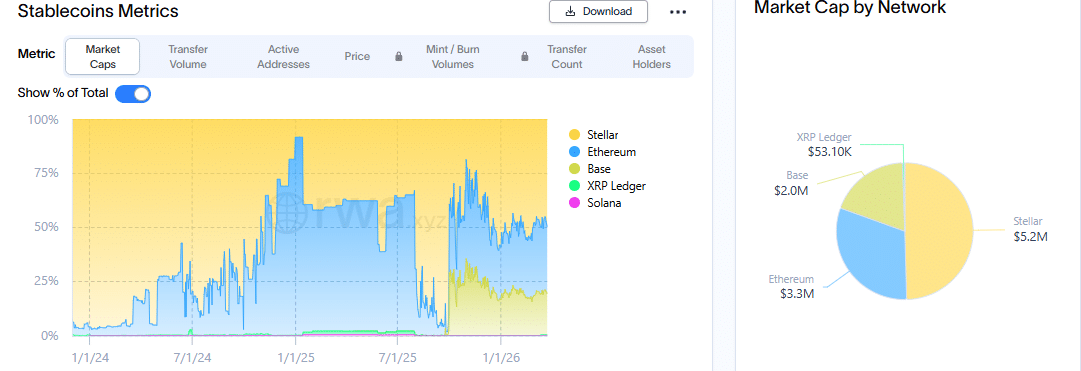

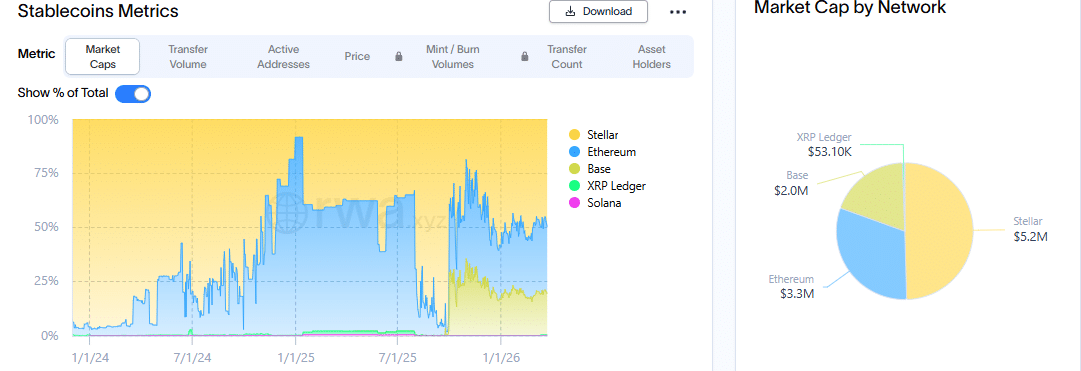

Сужение анализа до AUDD показывает, что он распределен по пяти основным блокчейнам.

Наибольшая доля его капитализации, около 48%, приходится на Stellar [XLM], что равно 5,2 миллионам долларов, в то время как Ethereum [ETH] занял второе место с 31% от общего объема.

Base Chain удерживал 19%, что представляло 2 миллиона долларов. Между тем, менее 1% от его общей доли приходилось на Solana [SOL] и XRP Ledger.

Прогноз проекта Acacia вместе с реализацией стал прецедентом для роста токенизации на австралийском рынке.

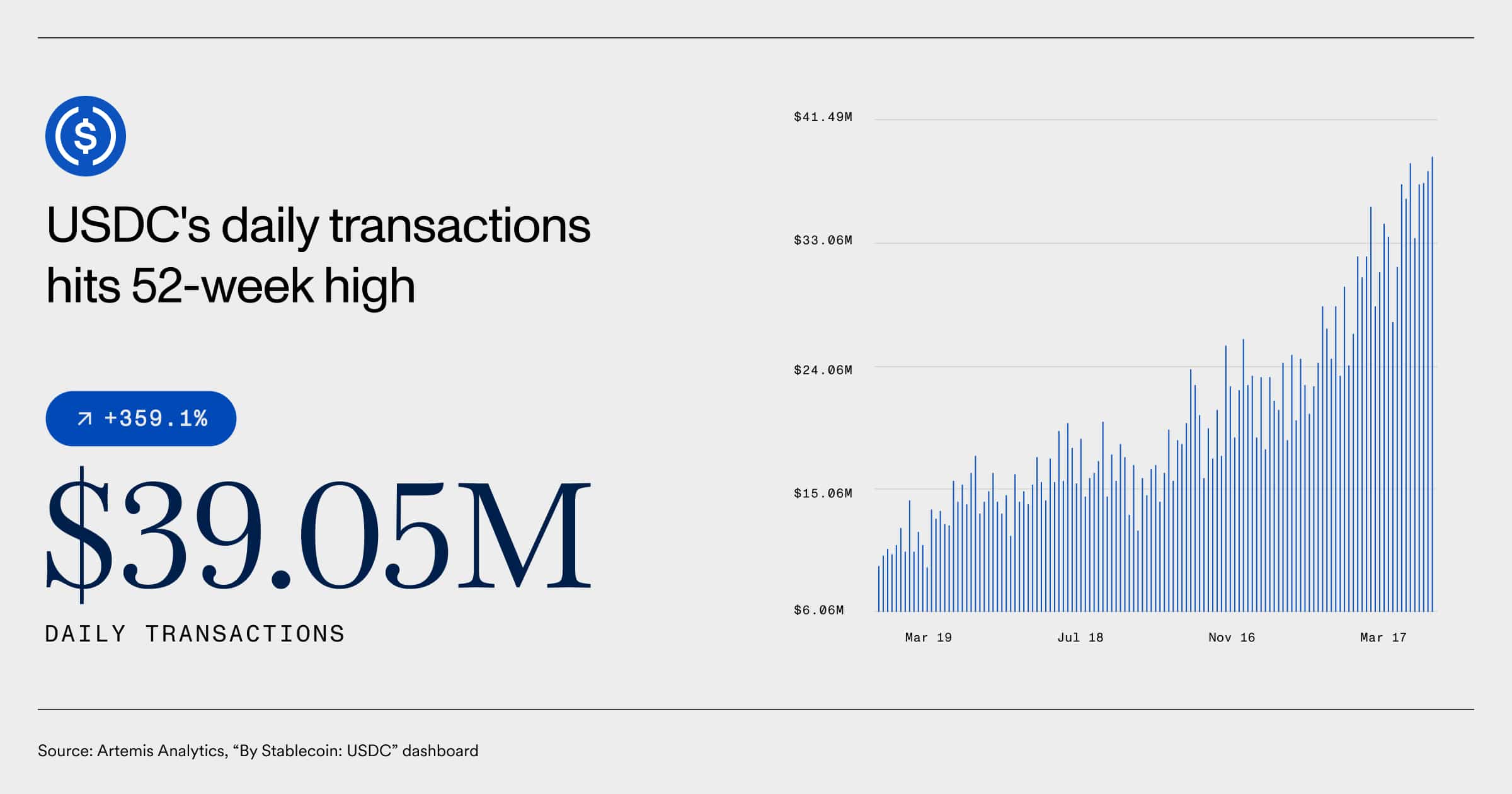

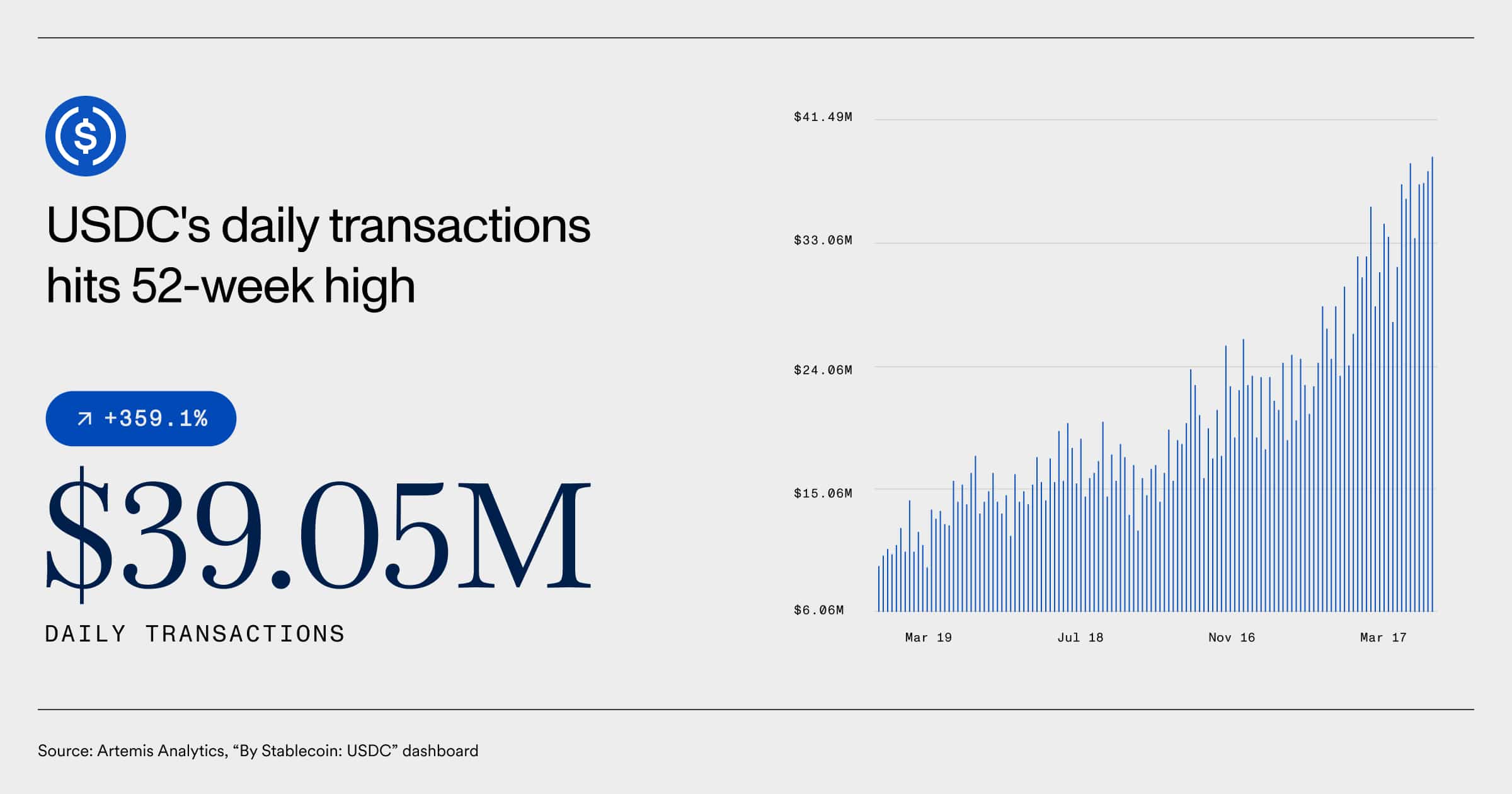

Резкий рост ежедневных транзакций

Токенизация сильно зависит от стейблкоинов.

Для контекста: ежедневные транзакции USD Coin [USDC] достигли 52-недельного максимума в 39,05 миллиона долларов. Это эквивалентно росту на 359% с марта 2019 года.

Однако рост рынка стейблкоинов в австралийских долларах несопоставим с ростом стейблкоинов, обеспеченных USD. Следовательно, токенизация может стимулировать рост стейблкоинов, обеспеченных AUD, и реальных активов (RWA) в стране.

Итоговое резюме

- RBA переходит от вопроса о том, будет ли происходить токенизация, к вопросу о том, как ее реализовать.

- Рыночная капитализация стейблкоинов, обеспеченных AUD, оставалась относительно низкой, но регулирование может изменить эту тенденцию.