Луммис предупреждает, что криптовалютное регулирование в США по-прежнему несовершенно, поскольку борьба за принятие закона CLARITY зашла в тупик

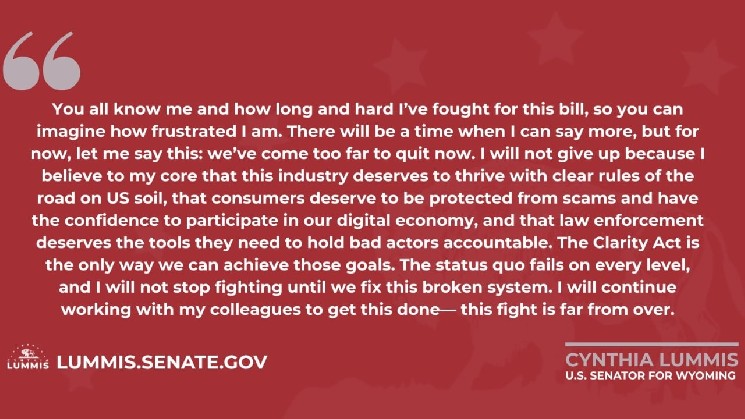

Сенатор США Синтия Луммис выразила разочарование из-за застоя в рассмотрении законопроекта CLARITY Act, который призван создать комплексную систему регулирования криптовалют в США. Она подчеркнула, что законодатели проделали большую работу и не намерены сдаваться, так как отрасли необходимы четкие федеральные правила для ведения бизнеса, а потребителям — защита от мошенничества на цифровых рынках.

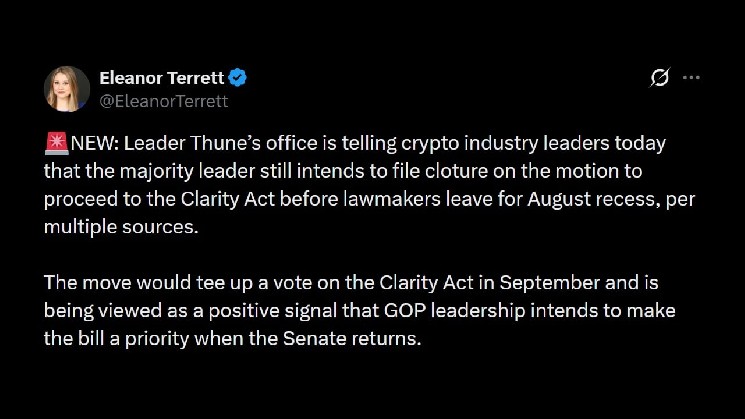

Луммис, являясь ключевой фигурой в продвижении этого закона, ожидала голосования до августовских каникул, но оно было отложено до сентября. Она отмечает, что законопроект предусматривает важные меры, такие как защита активов клиентов в случае банкротства бирж.

Несмотря на двухпартийный прогресс и одобрение Банковским комитетом Сената, дальнейшая судьба законопроекта зависит от действий Сената. Луммис предупреждает, что если закон не будет принят в текущем периоде, процесс может затянуться до 2030 года. Обновленный текст законопроекта был опубликован в июле, и теперь внимание сосредоточено на возможности добиться более широкой поддержки в Конгрессе после возвращения сенаторов к работе в сентябре. Луммис пообещала продолжать борьбу за принятие закона.

cryptonews.ruВчера 14:59