После более чем двух месяцев колебаний Биткоин наконец показал признаки пробоя.

Возглавляет атаку Биткоина старый друг Майкл Сейлор, и на этот раз он задействовал новое оружие: STRC.

Если пролистать последние твиты Сейлора, можно заметить, что он практически ежедневно создает контент, продвигающий STRC. Бассейны тропических курортов, женщины с коктейлями — подобные низкокачественные промо-видео, сгенерированные ИИ, посылают четкий сигнал: мужчина, вознесший MSTR на вершину Nasdaq, направил ту же маркетинговую мощь на STRC.

Почему он это делает? Потому что STRC — это практически единственный инструмент Strategy на данный момент, который может преобразовать деньги рынка в покупательский спрос на BTC. За последние три месяца каждое крупное объявление Strategy о наращивании запасов BTC указывало на STRC как на источник финансирования.

Что такое STRC

STRC — это аббревиатура от Variable Rate Series A Perpetual Stretch Preferred Stock, бессрочный привилегированный акционерный капитал, выпущенный Strategy и размещенный на Nasdaq в ноябре прошлого года.

Его механизм работы大致如下:

Вы платите около 100 долларов за одну акцию STRC. Strategy ежемесячно выплачивает дивиденды наличными с годовой доходностью 11,5%, что составляет примерно 96 центов на акцию в месяц. Он не имеет срока погашения, и Strategy не нужно возвращать основную сумму.

Цена акции привязывается к номиналу в 100 долларов посредством ежемесячной корректировки дивидендной ставки: если цена падает ниже 100, ставка дивидендов повышается, чтобы привлечь покупателей; если поднимается выше 100, ставка понижается, позволяя цене вернуться к номиналу. Верхний предел ежемесячной корректировки дивидендной ставки составляет 25 базисных пунктов.

Strategy может выпускать новые акции по номинальной стоимости для привлечения средств только тогда, когда цена STRC находится выше 100 долларов — это前提 всего механизма. Большая часть выручки от размещения, за вычетом резерва на дивиденды, направляется на покупку BTC.

Сейлор называет этот продукт «краткосрочным высокодоходным кредитом» или «фондом денежного рынка, обеспеченным Биткоином». При текущей доходности казначейских облигаций США около 3,5% STRC предлагает доходность, эквивалентную трём таким yield.

Маховик

Распространенное заблуждение о Сейлоре заключается в том, что он печатает бесконечные деньги для покупки BTC.

Он не может этого сделать. Сейлор не может печатать деньги из воздуха, он должен ждать, пока рынок не передаст ему деньги. Каждая новая выпущенная акция STRC предполагает, что есть реальный маржинальный покупатель, готовый купить её по цене 100 долларов.

Покупатели STRC, по сути, совершают кредитную «сделку», где дополнительные 8% доходности по сравнению с гособлигациями являются компенсацией за «кредитный риск Strategy».

Однако многие покупатели STRC не знают, что их средства, вложенные в STRC, будут косвенно усилены в три раза и направлены в BTC.

У Strategy есть публичная финансовая цель: коэффициент leverage 33%.

Среди всех источников финансирования компании на долю таких бессрочных привилегированных акций, как STRC, STRF, STRK, приходится около одной трети, остальные две трети — от обыкновенных акций MSTR. Сейлор называет этот принцип «intelligent leverage» (умное leverage). Это означает, что каждый раз, когда Strategy привлекает 1 доллар через STRC, чтобы удержаться на отметке leverage в 33%, они должны дополнительно выпустить примерно 2 доллара MSTR и также направить их в BTC. 1 доллар STRC + 2 доллара MSTR = 3 доллара покупательского спроса на BTC.

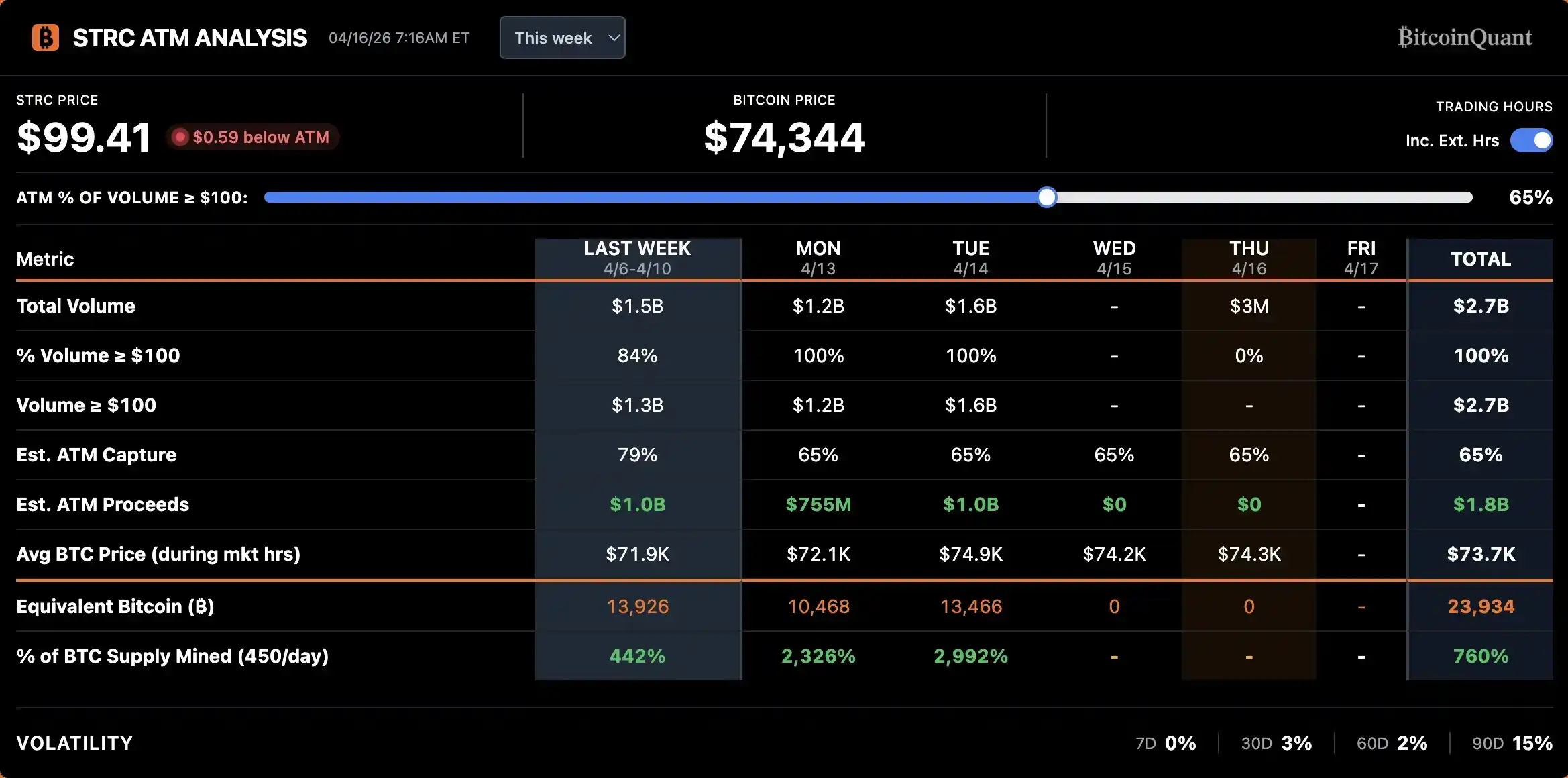

14 апреля Strategy привлекла через STRC около 1 миллиарда долларов за один день. При усилении в 3 раза это соответствует покупательскому спросу на BTC примерно на 3 миллиарда долларов, что точно совпадает с масштабом накопления BTC за первые две недели апреля до экс-дивидендной даты.

Когда BTC падает, залог обесценивается, кредитный риск STRC возрастает, и Strategy должна повышать дивидендную ставку, чтобы компенсировать новый уровень риска. Но чем выше ставка, тем больше давление на денежный поток и выше вероятность дефолта. Это нестабильная обратная связь. В период с октября прошлого года, когда BTC рухнул со 120 000 до 60 000 долларов, дивидендная ставка STRC выросла с 7% до 11,5%, чтобы едва вернуть покупателей.

И наоборот, когда BTC стабилизируется и растет, залог укрепляется, качество кредита улучшается, и STRC становится более привлекательным при той же дивидендной ставке, что further放大 спрос. BlackRock's Preferred and Income Securities ETF в апреле включил привилегированные акции Strategy в число своих крупнейших холдингов, заняв второе место, с ростом рыночной стоимости с примерно 200 миллионов в марте до 344 миллионов долларов, что является прямой поддержкой кредитного качества Strategy со стороны институциональных инвесторов в fixed income.

Маховик Strategy перешел в положительную фазу: больше денег покупают STRC → Strategy усиливает в 3 раза и покупает BTC → цена BTC получает поддержку → залогововая база STRC укрепляется, кредитный спред сужается → STRC становится более привлекательным при той же дивидендной ставке → больше денег покупает STRC.

Арбитраж на экс-дивидендную дату

Механизм выплаты дивидендов по привилегированным акциям отличается от облигаций. По облигациям проценты начисляются ежедневно, вы получаете проценты за каждый день владения; привилегированные акции выплачиваются единовременно в фиксированную дату. Для STRC, если вы владеете акцией на момент закрытия торгов за день до экс-дивидендной даты, вы получаете полные ежемесячные дивиденды в 96 центов.

Это создает очевидное арбитражное окно: купить за несколько дней до экс-дивидендной даты, получить дивиденды и продать на следующий день. Данные за последние месяцы показывают, что среднее падение STRC после экс-дивидендной даты составляет около 20 центов, что значительно меньше самих дивидендов в 96 центов. Чистая прибыль от однократного арбитража на одну акцию может составить от 40 до 50 центов.

Арбитражеры не упустят такую возможность.

Как показано на графике, объем торгов начинает расти за неделю до экс-дивидендной даты, достигает пика в день экс-дивидендной даты или накануне, а затем быстро затихает после нее. В апрельском раунде всплеск объема был значительно круче, чем в марте, что указывает на то, что все больше средств участвует в арбитраже на дивиденды по STRC.

Однако такой арбитраж может быть не совсем好事.

Для самого продукта STRC две-три недели после экс-дивидендной даты становятся «мертвой зоной» — ликвидность сокращается, спреды между ценой и продажей расширяются, цена акции долгое время остается ниже номинала в 100 долларов. Такое repeated расхождение с якорем подрывает позиционирование STRC как «продукта денежного рынка», приближая его к форме, более похожей на облигацию с месячной волатильностью.

Для Сейлора его покупки BTC легко могут быть front-run арбитражными деньгами. Размещение STRC сосредоточено за две недели до экс-дивидендной даты, что означает, что его действия по покупке BTC также сосредоточены в эти две недели.

Теперь арбитражные трейдеры ежемесячно в одно и то же время устремляются покупать STRC, зная, что Сейлор вот-вот возьмет эти деньги и пойдет скупать BTC на спотовом рынке, поэтому они могут заранее купить BTC, дождаться, пока Сейлор поднимет цену, а затем продать, повышая thus стоимость покупки для Сейлора.

За последние две недели премия спота Coinbase вокруг экс-дивидендной даты STRC значительно выросла

Есть два возможных решения: изменить частоту выплаты дивидендов, например, с ежемесячной на еженедельную, распределив thus арбитражную прибыль; или выпустить более初级ный, более frequently выплачивающий дивиденды производный продукт, чтобы рассредоточить concentrated арбитражные сделки.

И果然, Сейлор быстро acted, объявив в субботу, что Strategy подала доверенность, предлагающую изменить частоту выплаты дивидендов по STRC с ежемесячной на раз в две недели. Годовые дивидендные обязательства и дивидендная ставка остаются неизменными.

Если предложение будет одобрено, первые полумесячные дивиденды будут выплачены 15 июля.

Советник Bitwise Джефф Парк指出, что в настоящее время на рынке нет корпоративных облигаций с полумесячным机制 выплаты дивидендов, а предпочтение розничных инвесторов к более частым выплатам подтверждается успехом таких продуктов, как ETF с еженедельными дивидендами.

На более глубоком уровне Джефф Парк рассматривает это как знаковый шаг проникновения видения «потоковых платежей» индустрии криптовалют на традиционные рынки капитала: частота выплаты процентов по своей сути отражает эффективность преобразования денежного потенциала в кинетическую энергию, и эпоха цифровых денег должна打破 искусственные временные周期 ограничения.

Он считает, что STRC задает новый стандарт для традиционных компаний и с нетерпением ждет будущей эволюции от полумесячной к ежедневной и даже мгновенной выплате.

Новая нарратика для DeFi

Появление STRC принесло свежую струю в бледный рынок DeFi.

За последний год доходность стейблкоинов в DeFi неуклонно снижалась. Годовая ставка по депозитам стейблкоинов на Aave составляет около 2%, USDe от Ethena и USDS от Sky находятся ниже 4%, даже PT по мейнстримным стейблкоинам на Pendle с трудом突破 6%. Такой уровень доходности при риске exposure смарт-контрактов в эпоху ИИ уже отпугнул многих ветеранов DeFi.

DeFi нуждается в надежном, достаточно крупном источнике дохода, который мог бы вернуть деньги TradFi в ончейн, и STRC как раз предоставляет такую возможность.

Два проекта пытаются упаковать доходность STRC в ончейн:

Apyx Protocol использует двухтокенную модель. apxUSD — это базовый стейблкоин, обеспеченный с избытком привилегированными акциями, такими как STRC, SATA, и гособлигациями; apyUSD — это стейкинговая версия, которая получает дивиденды и процентный доход от базовых активов, текущая годовая доходность составляет около 12,78%. Объем供应 уже достиг 130 миллионов долларов, и на Pendle и Morpho уже есть соответствующие продукты для дохода и leverage.

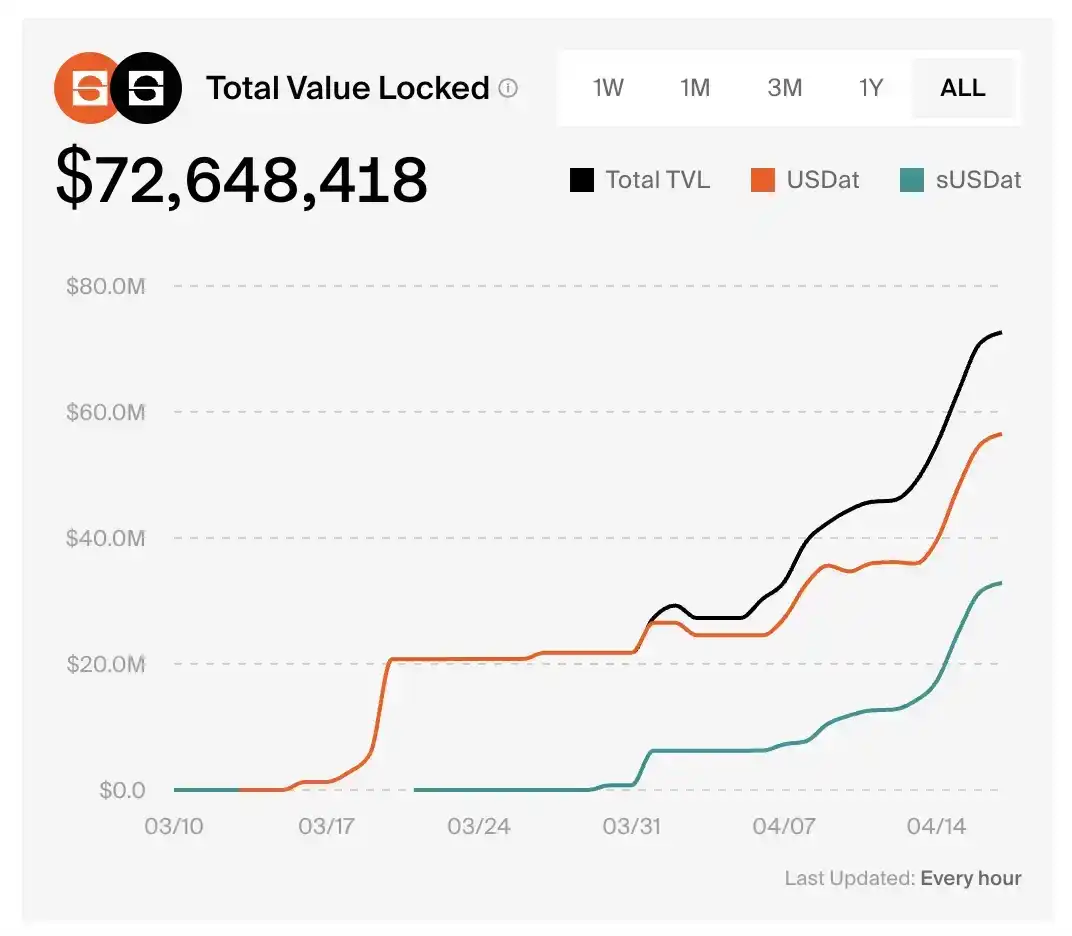

sUSDat от Saturn Credit — это стейкинговый стейблкоин, приносящий доход, который получает доходность от STRC, TVL протокола выросло с нуля до 72,6 миллиона долларов за чуть более месяца.

Согласно данным рынка Pendle, текущая годовая доходность PT-sUSDat составляет 9,2%.

Взлет и падение

Чем успешнее работает эта精心 сконструированная Сейлором финансовая машина, тем сложнее избежать одного вопроса.

На данный момент Strategy владеет почти 3,5% от общего количества BTC и продолжает наращивать их с скоростью в миллиарды долларов в месяц.

Каково было первоначальное ценностное предложение BTC? Децентрализованный monetary актив, не зависящий от какого-либо одного субъекта, который никто не может unilateral манипулировать.

Когда бессрочные привилегированные акции одной публичной компании становятся основным маржинальным покупателем для BTC — децентрализованного monetary актива, не зависящего от какого-либо одного субъекта, который никто не может unilateral манипулировать, не отходит ли Биткоин от своей первоначальной формы?