Author: Chloe, ChainCatcher

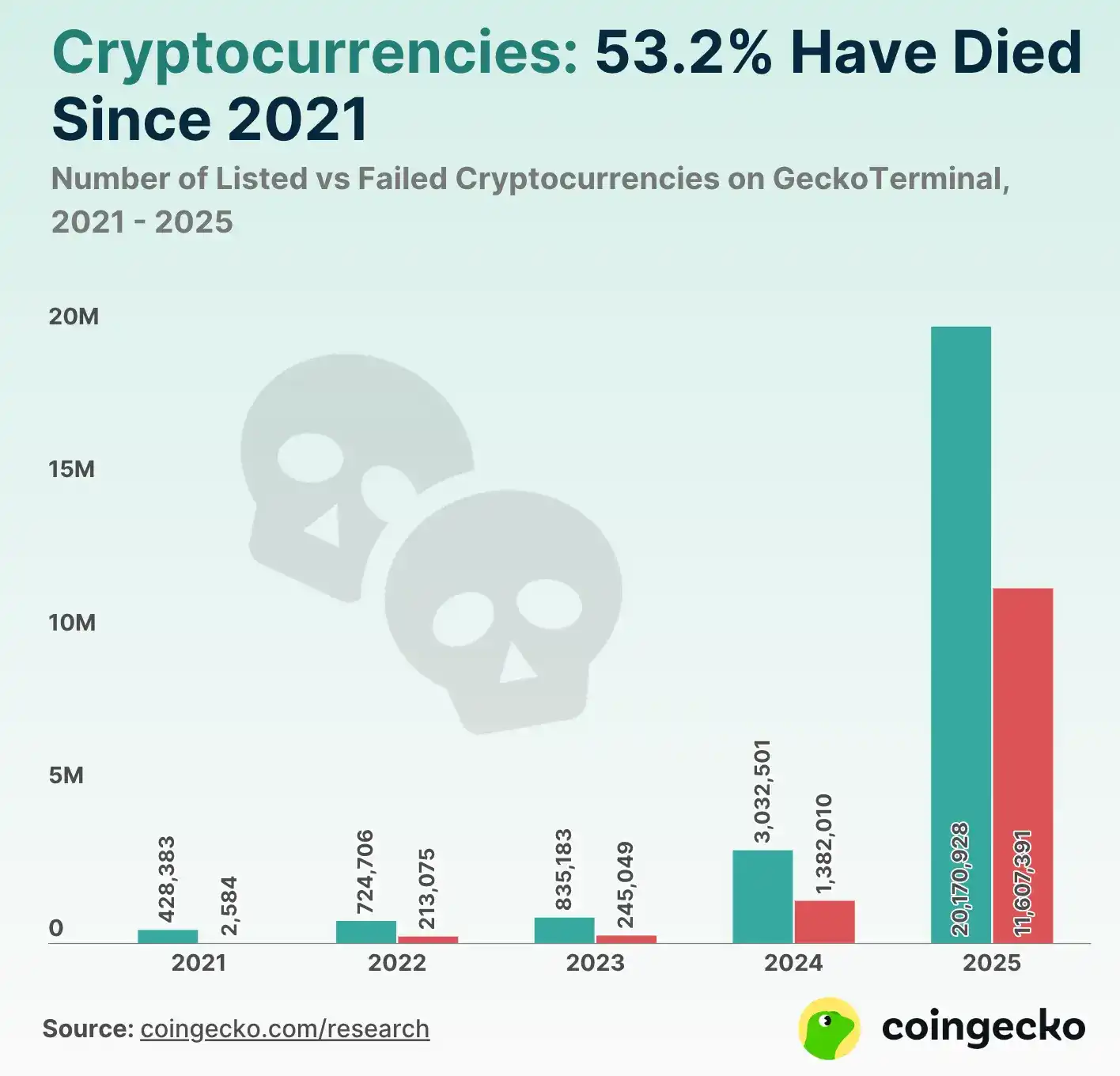

The crypto market in 2025 witnessed an extreme industry contradiction: according to GeckoTerminal statistics, while the total number of token-launching projects surpassed the 20 million mark, over 57% of them met their demise. Amid this brutal elimination race, a more insidious type of "zombie project" is spreading. They boast backing from top-tier capital and leading exchanges, frequently pivot their narratives to chase hot trends, yet are nearly stagnant in terms of actual product delivery, technological development, and ecosystem building.

This article will deeply analyze疑似 zombie-fying projects like Sleepless AI, Hooked Protocol, Saga, and Dymension, examining their operational characteristics. In 2026, the ability to see through narrative fog and identify signs of zombification has become a essential survival skill for investors.

Launching a Token Means "Job Done"? Project Decline and Zombification Phenomenon

In the early stages of blockchain development, the definition of "Zombie Coins" was relatively straightforward: long-term dormancy, loss of trading liquidity, vanished development teams, lack of community participation, etc. However, with the maturation of capital markets and the deep involvement of venture capital, a more隐蔽 absurd phenomenon has emerged in recent years.

Data shows that in 2021, the number of token-launching projects on GeckoTerminal was only 428,000, but by the end of 2025, this number had skyrocketed to 20.17 million. Behind this explosive growth, a staggering 53% of projects met their end. Simultaneously, hidden within this high turnover, high淘汰 rate are大量 "zombified" projects. They trade on exchanges, post social media announcements daily, but there exists a huge gap in actual product delivery, on-chain activity, and ecosystem development.

Sleepless AI: Parasitizing the AI Narrative? R&D and Delivery Disconnect

Sleepless AI was once a market darling, not only selected as a standout in Binance Labs' sixth season incubation program but also debuted gloriously on Binance Launchpool's 42nd edition under the光环 of "Web3+AI Virtual Companion." However, entering 2026, its market performance has diverged sharply from its initial热度: the token price has retreated from its historical high of $2.46 to around $0.024, a drop of 99%.

1. Technical Transparency and R&D Progress Disconnect: Although the project touts the use of AIGC and large language models (LLM) to create a deep emotional support experience, its technical transparency is lacking. Observing through public channels, the project almost lacks trackable code update records or iterative versions of core algorithms. More concerning for investors is that the Web Dapp originally scheduled for Q2 2025 has an unclear progress status至今.

2. Inefficient Execution of Mobile Strategy: In the "mobile-first" application era, Sleepless AI's product落地 process appears relatively lagging. Its flagship product "HIM" as of early 2026 still hasn't successfully launched on the iOS App Store or Google Play Store; the official website still only offers Android APK downloads. For a project aiming for mass adoption, this development efficiency severely limits user growth and market trust.

3. Narrative Rebranding and Insider Doubts: Accompanying the product stagnation are deep market doubts about the project's本质. Market observers have put forward the view that the project is疑似 a "narrative rebranding" of an old Web2 game, meaning it repackaged itself with AI concepts and leveraged capital connections to强行 latch onto the AI trend's热度 to secure Binance Labs' investment and Launchpool's流量红利. Although such claims are often anonymous, combined with its weak technical delivery and token price collapse, this phenomenon of "narrative parasitism" has become an important reference indicator for investors in 2026 to identify疑似 zombie projects.

Hooked Protocol: Ecological Dilemma After Incentives Dry Up

Hooked Protocol once emerged rapidly in the Web3 social learning track with its Learn-to-Earn model, securing investment from Binance Labs and Sequoia China, and launching as Binance's 29th Launchpad project. However, as token distribution entered its mid-to-late stages and subsidy红利 gradually faded, the project now faces severe tests of "real user retention" and "ecological substance".

1. From Learn-to-Earn to Incentive Dependency Dilemma: Hooked Protocol's initial success relied heavily on the流量 effect of Binance Launchpad and a strong token subsidy mechanism. This model can quickly换取 huge user numbers initially, but when the HOOK token price fell nearly 99% from its high, the growth game sustained by subsidies loses its appeal. History has repeatedly shown: after TGE, when incentives disappear, "massive user numbers" lacking rigid demand often rapidly shrink.

2. "Marketing-Oriented" Tendency in Narrative Transformation: Entering 2025, Hooked attempted to transform into an "AI-driven learning ecosystem" and "educational infrastructure." Although officially stated to be co-developing courses with 3-7 top universities and launching the Hooked Coursera Hub in August 2025 in collaboration with over 74 Web3 projects, these moves seem more like "brand endorsements" at the marketing level. Compared to the impressive list of partners, its substantive breakthroughs at the technical底层 appear lackluster.

Hooked Protocol's current state reveals a core challenge for Web3 application projects to a certain extent: if a project's vitality relies on token incentives and cannot transform into原生 demand with business resilience, it will struggle to escape the fate of大幅 token price decline, even zombification. The current low币价 and potentially shrinking ecological activity are the negative feedback after subsidy-driven prosperity.

Saga: Dual Blows of Lack of Market Demand and Security Vulnerabilities

Saga represents another path to zombification: the shovel seller can't find miners. With the grand vision of "one-click chain launch," Saga successfully attracted over $1000 in financing from top institutions like Placeholder, GSR, and Samsung Next, and also successfully launched as the 51st project on Binance Launchpool. However, this powerful automated chain-launching tool seems somewhat misplaced when tested against real market demand.

1. Frequent "Pivoting" Exposes Ecological Anxiety: Over the past two years, Saga has shown极高的 narrative flexibility, but also暴露出其生态核心缺陷. From initially promoting itself as a gaming-specific chain with over 350 partner projects, to later pivoting to an AI infrastructure narrative, this frequent narrative shifting essentially reflects the growth anxiety arising from the lack of落地 applications in its old ecosystem.

If its core technology "Chainlet" had genuine market demand, it should theoretically drive token buybacks through developers' continuous renewals. However, the reality is that Saga's partner list, though long,始终 lacks blockbuster project support. Most partners remain in the early exploration stage, unable to contribute substantial economic driving force to the protocol.

2. Fatal Blow to Security Credibility: For infrastructure, technical security is its bottom line. SagaEVM suffered a $7 million vulnerability attack in January this year, with the stablecoin $D depegging to $0.75, and TVL evaporating from approximately $37 million to $12 million. This is undoubtedly a severe blow for a project positioning itself as infrastructure.

When grand narratives fail to translate into ecological data, and technical security is flawed, the market's feedback is often merciless. The native token SAGA price has fallen from its 2024 high of $6 to around $0.032 currently.

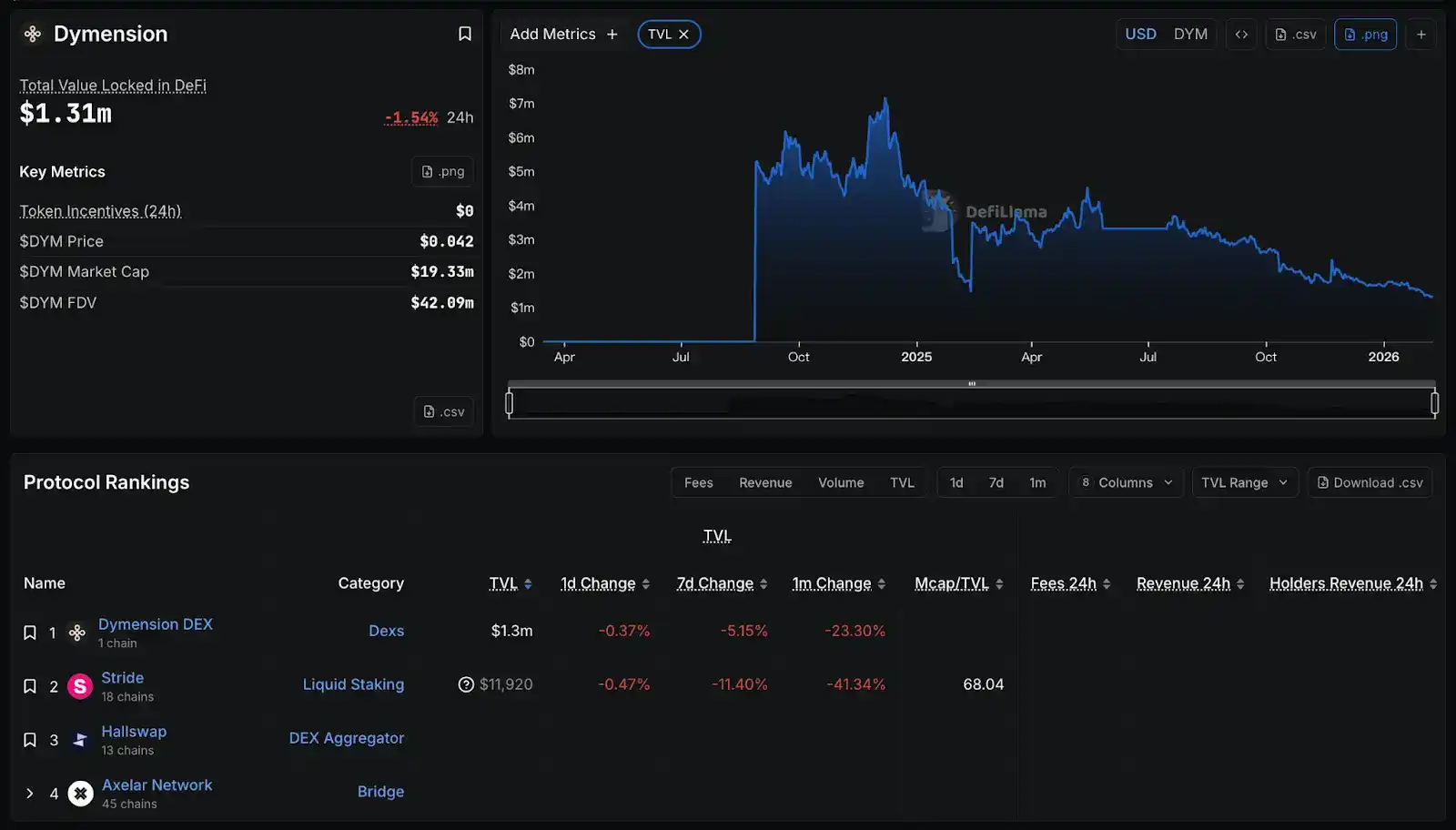

Dymension: Data Ghost Town Under a Grand Architecture

Dymension's script is highly similar to Saga's. Its proposed RollApp concept is quite attractive in theoretical architecture, but in the face of actual data in 2026, it更像是一座宏伟的鬼城 (a grand ghost town). Although Dymension attempts to establish a benchmark for a modular settlement layer, the real vitality of its ecosystem falls far short of expectations.

1. RollApp Network Activity Disconnect: Dymension once claimed to have deployed over 10,000 RollApps within its ecosystem. However, this data prosperity essentially stems from the lowered barriers to "issuing tokens and launching chains." The vast majority of deployed RollApps have no sustained on-chain transactions or substantial output beyond the initial token issuance, and many have even disappeared.

2. Dysfunctional Economic Function of Infrastructure: When Launchpad and development kits fail to transform into a thriving digital economy, the infrastructure itself falls into value exhaustion. Dymension's main DEX projects and ecosystem TVL performance are both unsatisfactory. The current overall TVL is only $1.3M, forming a stark contrast with the market's initial expectation of it being a "modular leader" at token launch.

When the infrastructure primarily runs zombie applications and the overall ecosystem performance is拉垮 (lacking), the native token DYM price is inevitably corrected by the market. The current FDV is $45M, and the token price has fallen 99% from its high of $6, now只剩 (only remaining at) $0.042.

Why Are "Zombie" Projects Proliferating?

The reason these projects can maintain a superficial "vitality" stems from deep-seated structural issues within the Web3 industry.

1. Capitalized Listing Power Structure: In recent years, the listing path for many projects has not originated from substantial technological breakthroughs but has highly relied on "capital, vested interests, and narrative packaging." Pushed forward by the combined force of VCs and internal executives, these projects enter top exchanges through精美 packaging and刷出来的 (fabricated) testnet data. Once the token unlock is complete, teams often lose motivation for further development.

2.模糊的团队背景 (Ambiguous Team Backgrounds): A common characteristic among some zombie projects is that the background of the core operators and technical leaders is extremely模糊 (ambiguous). This "black box" operational model not only allows the project team to avoid credible accountability when encountering technical bottlenecks or security vulnerabilities but also provides them with very low exit costs. It enables the operating team to quickly rebrand, discreetly reposition in a new narrative after one project stalls, and repeatedly消耗 (consume) market credit.

3. Narrative Parasitism Capability: Zombie projects often possess a strong ability for "narrative parasitism." Whenever market热点 (hot topics) shift, these projects with little substantive progress often conduct "announcement-style pivots" to align with the new narrative. This not only increases the identification cost for investors but also分散 (disperses) scarce liquidity into unproductive shells, from which they can蹭热度 (ride the hype) and attract speculative capital.

Conclusion: Investors Should Seek the True Bottom Line of Value in 2026

Facing a prosperous market woven from twenty million token-launching projects, investors' core logic must change. In 2026, identifying zombie projects is no longer just a bonus skill but a defensive necessity. Below are three core indicators to help readers identify them:

First, the verifiability of the team and technical delivery: Avoid projects with unclear team information, no GitHub commit history, low roadmap fulfillment rates, and slow product distribution. Second, the substance of the data: Distinguish between "subsidy-driven activity" and "organic demand." Check if users show retention willingness after token subsidies are removed. Finally, be wary of projects that change their core focus every three months. Genuine innovation requires deep cultivation; frequent narrative switches usually掩盖 (mask) the failure of the old business.

As the crypto market matures, the industry needs projects that consistently deliver both before and after token launches, genuinely bring value to the industry, and solve market pain points.