Автор: Dovey Wan, основатель и управляющий партнёр Primitive Ventures

Компиляция: Dayu

К 2025 году индустрия криптовалют достигла почти всех ожидаемых целей. Структурно это должен был быть блестящий год.

Но почему он ощущается... таким безжизненным?

Дело не только в том, что «цена не выросла», и всё кончено. Биткоин обновил исторический максимум. Но атмосфера, настроения, внутреннее подтверждение, подхват других криптовалют и энтузиазм розничных инвесторов — всё изменилось. Возможно, больше всего беспокоит то, что бывший «лидер горячих денег» теперь потерял свою привлекательность как с точки зрения эффекта богатства, так и волатильности.

Связанные криптоактивы больше не синхронизируются с Биткоином и Эфириумом, как в предыдущих циклах:

1. Мемкоины были на первом месте с четвертого квартала 2024 года по первый квартал 2025 года, а запуск токена Трампа поднял этот тренд до апогея.

2. Крипто-акции достигли пика вокруг IPO Circle и начали снижаться в период с мая по август 2025 года.

3. Большинство альткоинов так и не сформировали устойчивого тренда. В росте присутствовала асимметрия, а падение полностью контролировалось всеми участниками.

При ближайшем рассмотрении ситуация выглядит ещё страннее.

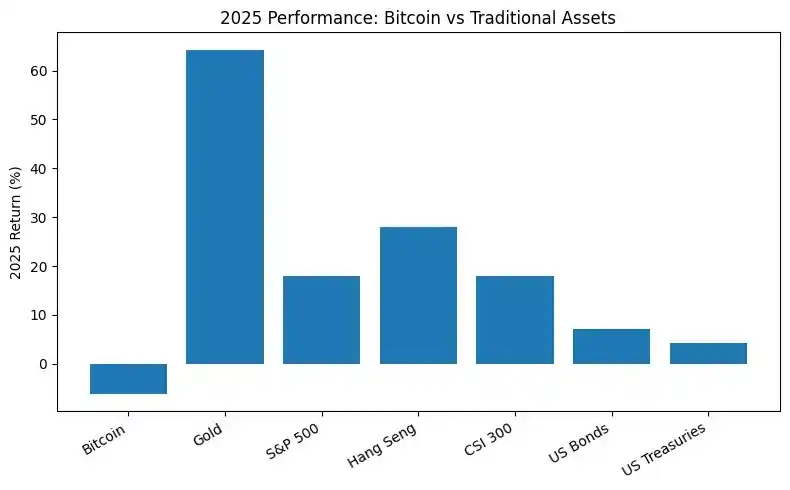

Несмотря на благоприятную политическую среду, Биткоин в 2025 году показал худшие результаты почти по сравнению со всеми основными традиционными финансовыми активами, включая золото, американские акции, гонконгские акции, акции A-shares и даже некоторые эталонные индексы облигаций.

(Сравнение Биткоина с другими активами, крайне слабая производительность)

Это первый раз, когда производительность Биткоина отключилась от всех других классов активов.

Это расхождение крайне важно: цена обновляет максимумы, но внутреннего подтверждения нет, а другие рынки показывают лучшие результаты. Это раскрывает простой, но тревожный факт: в цепочке поставок ликвидности Биткоина произошли значительные изменения, его первоначальный четырёхлетний цикл расчётов был изменён более крупными силами на других рынках.

Поэтому мы углубимся в изучение того, кто покупал наверху, кто вышел с рынка и где находится дно цены.

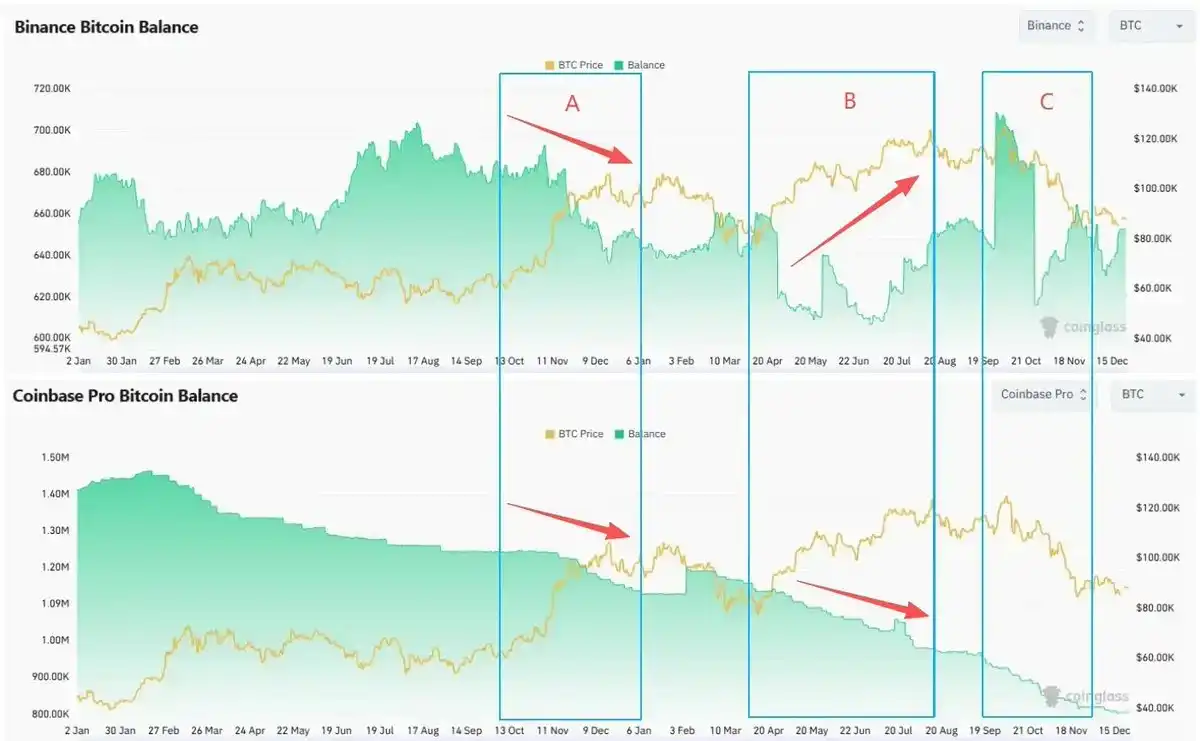

Огромный разрыв: Оншорные и офшорные операции

В этом цикле мы прошли через три截然 разных этапа —

-

Этап A (ноябрь 2024 г. – январь 2025 г.): Победа Трампа на выборах и более дружелюбная регуляторная среда вызвали общую FOMO среди инвесторов внутри страны и за рубежом. Цена Биткоина впервые превысила отметку в 100 000 долларов.

-

Этап B (апрель 2025 г. – середина августа 2025 г.): После распродаж, вызванных снижением杠杆 (делевериджа), BTC восстановил восходящий импульс и пробил уровень в 120 000 долларов.

-

Этап C (начало октября 2025 г.): BTC достиг текущего локального исторического максимума в начале октября, затем столкнулся с флэш-крэшем 10 октября и вошёл в период коррекции.

На каждом этапе мы наблюдали огромную разницу между покупками в США и продажами за рубежом —

Спот: Оншорные покупки на пробоях, офшорные продажи на росте.

-

Премия Coinbase оставалась положительной на этапах A, B и C. Высокий уровень покупательского спроса в основном исходил от оншорных спотовых средств.

-

Баланс BTC на Coinbase снижался на протяжении всего цикла. Запасы, доступные для продажи на американской стороне, сократились.

-

С отскоком цены на этапах B и C, балансы на Binance значительно выросли. Офшорные спотовые держатели пополняли запасы, увеличивая потенциальное давление продаж.

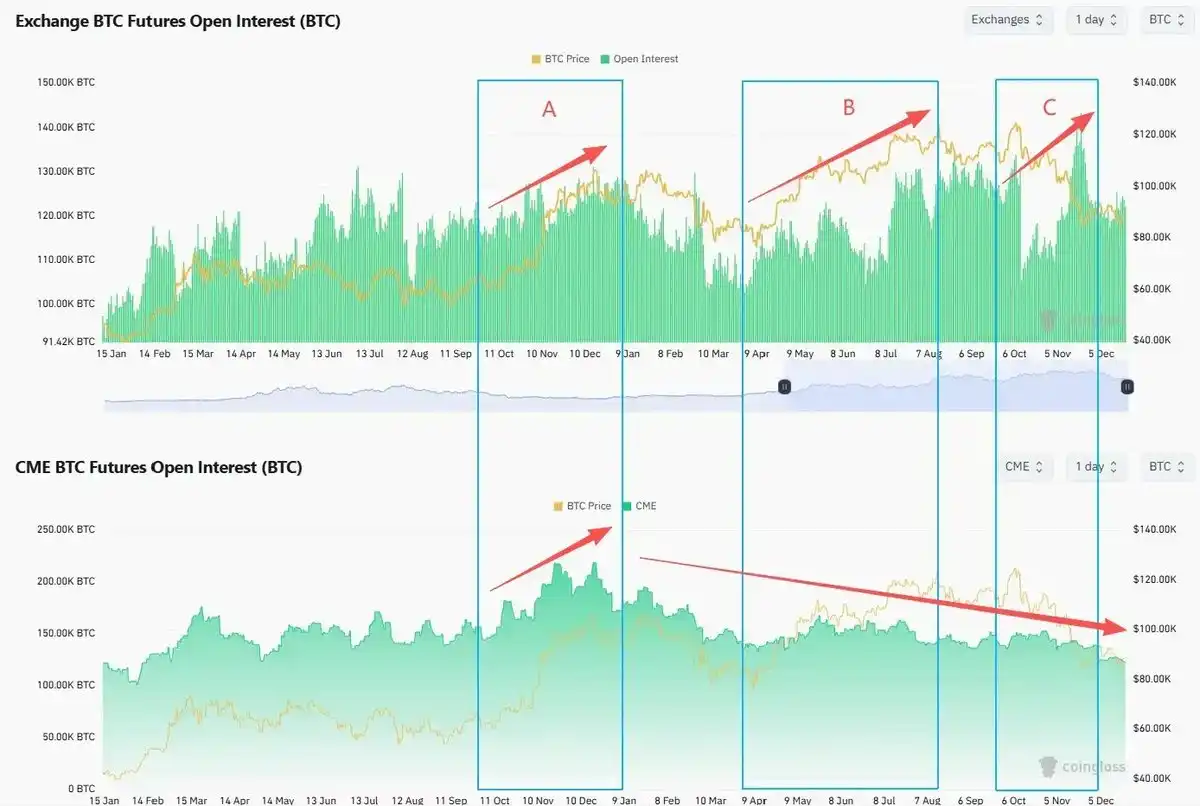

Фьючерсы: Рост офшорного杠杆 (левериджа), снижение оншорных позиций

Объём открытых офшорных позиций (Binance и другие офшорные площадки) пережил рост на этапах B и C. Леверидж увеличился. Даже после 10 октября леверидж быстро восстановился и вернулся к предыдущим пикам или превысил их.

С начала 2025 года оншорный объём открытых позиций (CME) имеет тенденцию к снижению. Институциональные инвесторы не увеличивали своё рисковое exposure (вложение) по мере обновления максимумов по контрактам.

В то же время, волатильность Биткоина разошлась с ценовым движением.

В августе 2025 года, когда цена Биткоина впервые пробила 120 000 долларов, DVOL находился near локальных минимумов. Рынок опционов не давал адекватной компенсации за сохраняющиеся риски.

Каждая «вершина», казалось, отражала разногласия между оншорными и офшорными трейдерами. Когда оншорные спотовые средства толкали цену вверх на пробоях, офшорные спотовые трейдеры использовали возможность для продажи. Когда офшорный杠杆ный (leveraged) капитал гнался за ростом, оншорные фьючерсные и опционные трейдеры сокращали позиции и оставались в стороне.

Где маржинальный покупатель? Кто ещё может принять эстафету?

По оценкам Glassnode, количество биткоинов, хранящихся в корпоративных инструментах и инструментах типа DAT, увеличилось с примерно 197 000 в начале 2023 года до примерно 1,08 миллиона к концу 2025 года, с чистым приростом примерно на 890 000 за два года. DAT стал одним из крупнейших структурных инвестиционных инструментов в системе Биткоина.

Другая часто misunderstood область — это ETF. К концу 2025 года американские спотовые Bitcoin ETF хранили около 1,36 миллиона BTC, что примерно на 23% больше, чем годом ранее, и составляет около 6,8% от circulating supply.

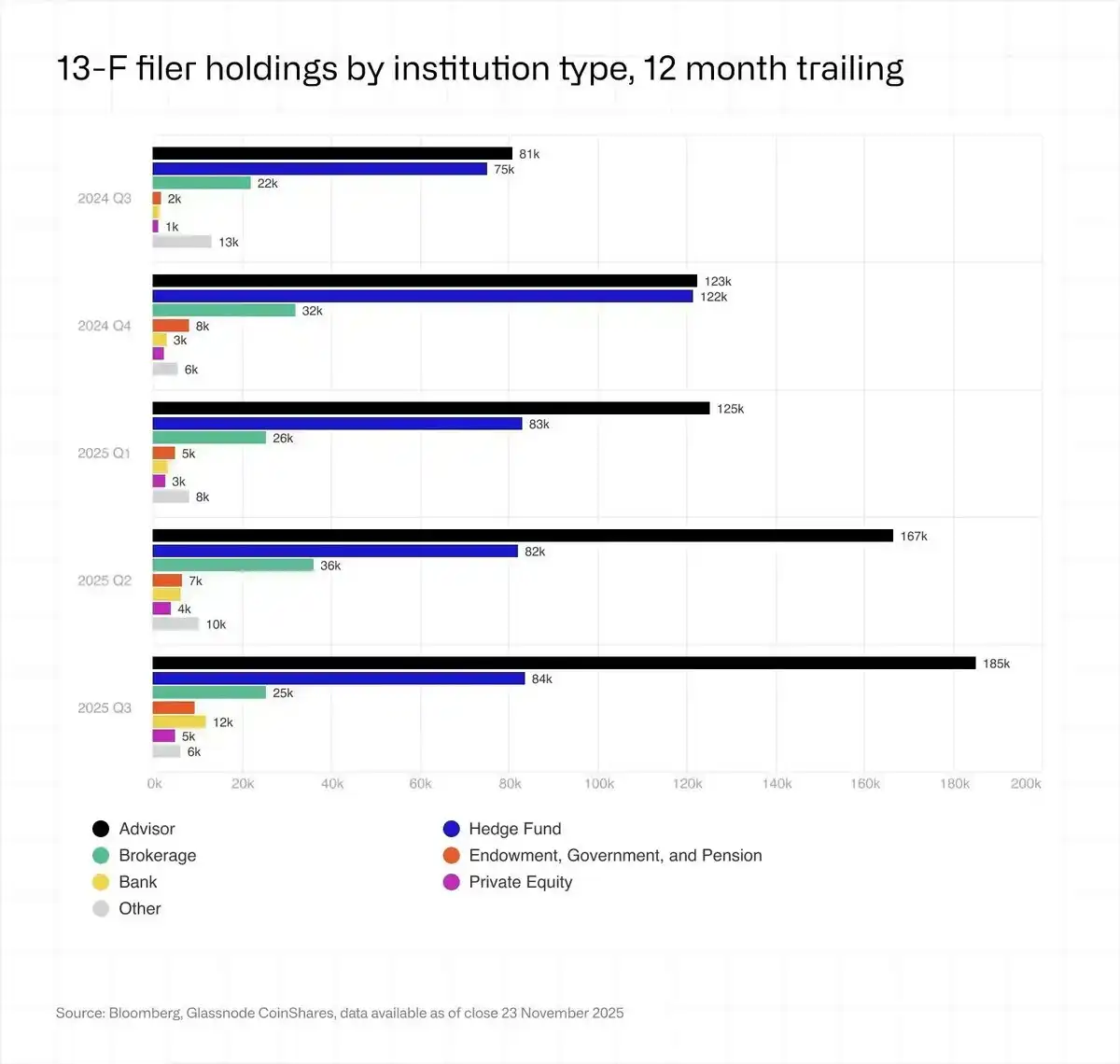

Институциональные инвесторы (заявители 13F) владеют менее четверти от общего количества ETF, и большинство из них — хедж-фонды и инвестиционные советники, явно не те «алмазные руки» из семейных офисов, которых мы знаем.

Смерть розничного инвестора

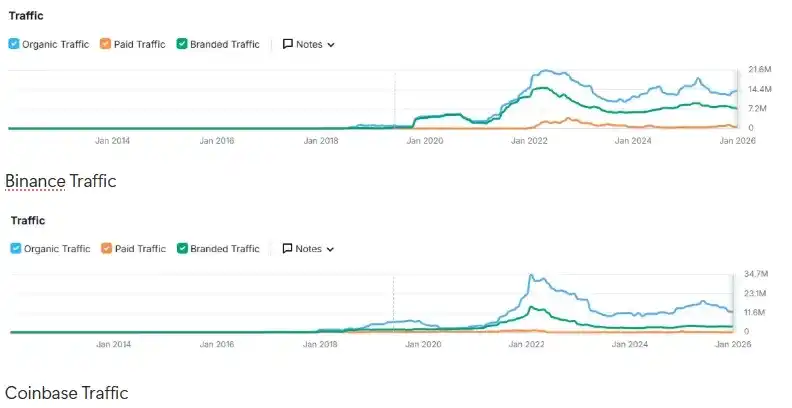

С начала 2025 года данные о трафике на Binance, Coinbase и других топовых биржах чётко указывают на сохраняющуюся слабость розничных инвесторов после того, как Трамп продал свои «мемкоины».

Кроме того, общие социальные настроения розничных инвесторов с начала 2024 года фактически были медвежьими.

Общий трафик на веб-сайты имеет тенденцию к снижению с пика 2021 года.

Обновление максимумов цены Биткоина не вернуло количество посещений к предыдущим уровням.

Вы можете прочитать больше на эту тему в нашей прошлогодней статье. «Кто является маржинальным покупателем?»

Стратегия бирж также адаптировалась. Столкнувшись с высокими затратами на привлечение клиентов и низкой активностью существующих пользователей, биржи перешли от «стремления к росту» к «удержанию существующего капитала с помощью продуктов, приносящих доход, и торговли multi-asset (активное листингование американских акций, золота и forex)».

В других местах повсюду бычий рынок

Настоящий «эффект богатства» в 2025 году проявился не в криптовалютном пространстве: S&P 500 (+18%), Nasdaq (+22%), Nikkei (+27%), Hang Seng (+30%), KOSPI (+75%), и даже A-shares выросли на 19%, показав强劲ный рост. Золото (+70%) и серебро (+144%) также значительно выросли, что делает «цифровое золото» несколько滑稽 (смехотворным) в сравнении.

Акции AI, 0DTE (с нулевым days to expiry) и товары, такие как золото и серебро, further eroded его привлекательность.

Деньги спекулянтов не rotated в альтернативные инвестиции. Многие полностью вышли, вернувшись на рынок волатильности акций, а новые спекулянты с удовольствием зарабатывали прибыль на американском фондовом рынке или на рынках акций своих стран.

Даже корейские розничные инвесторы продавали на Upbit, чтобы сделать ставку на индекс KOSPI и американские акции: среднедневной объём торгов на Upbit в 2025 году упал примерно на 80% по сравнению с 2024 годом. За тот же период индекс KOSPI вырос более чем на 75%. Корейские розничные инвесторы чисто купили американских акций на сумму около 31 миллиарда долларов.

Кто самые большие продавцы?

В каждом цикле кто-то продаёт на локальных максимумах, но интересно, что время продаж продавцов в этом цикле совпало с точками расхождения RS.

Биткоин ранее closely correlated с движением американских tech-акций, пока примерно в августе 2025 года он не начал заметно отставать от ARKK и Nvidia, после чего столкнулся с обвалом 10 октября и до сих пор не弥补 (восполнил) предыдущий разрыв.

Как раз перед этим расхождением, в конце июля, Galaxy в своих earnings report и медиа-брифингах раскрыла, что она executed ордер на продажу более 80 000 BTC от имени established держателя. Эта сделка вывела phenomenon «выхода китов эпохи Сатоши в прибыль» на公众ный (public)视野.

Майнеры продают для AI CAPEX

С халвинга Биткоина в 2024 года до конца 2025 года, miner reserves пережили самое устойчивое снижение с 2021 года. К концу года резервы составляли около 1,806 миллиона BTC. Хешрейт同比下降 примерно на 15%.

-

Согласно «Плану оттока в AI», майнеры перевели биткоины на сумму около 5,6 миллиардов долларов на биржи для финансирования строительства дата-центров AI.

-

Bitfarms, Hut 8, Cipher, Iren и другие компании преобразуют площадки в кампусы для AI и высокопроизводительных вычислений, подписывая 10-15-летние контракты на вычисления, рассматривая электроэнергию и землю как «золото эпохи AI».

-

Riot, являющаяся представителем HODL, в апреле 2025 года объявила, что начнёт продавать все ежемесячно добытые монеты.

По оценкам, к концу 2027 года около 20% майнинговых энергомощностей может быть перераспределено на workloads AI.

Китай принял более жёсткие меры. В декабре 2025 года Синьцзян снова стал целью Народного банка Китая и различных министерств. Около 400 000 ASIC-майнеров были принудительно отключены, что привело к падению глобального хешрейта на 8-10% за несколько дней.

Серые киты: Похмелье от чёрного Биткоина

Подобно тому, как афера PlusToken оказала значительное влияние на цикл 2021 года, несколько крупных случаев мошенничества и азартных игр, произошедших в 2025 году, включая финансовую пирамиду/культовую сеть Цянь Чжиминь и дело камбоджийской Prince Group / Чэнь Чжи, likely были major драйверами behind движением цены Биткоина.

Оба дела involved конфискацию десятков тысяч BTC, в общей сложности достигая или превышая уровень в 100 000 чёрных монет.

Это также может увеличить потенциальное давление продаж со стороны правительства, а также оказать significant сдерживающее воздействие на крупные серые рынки long-term держателей Биткоина, что может создать давление продаж в среднесрочной перспективе, но в целом является положительным в долгосрочной перспективе.

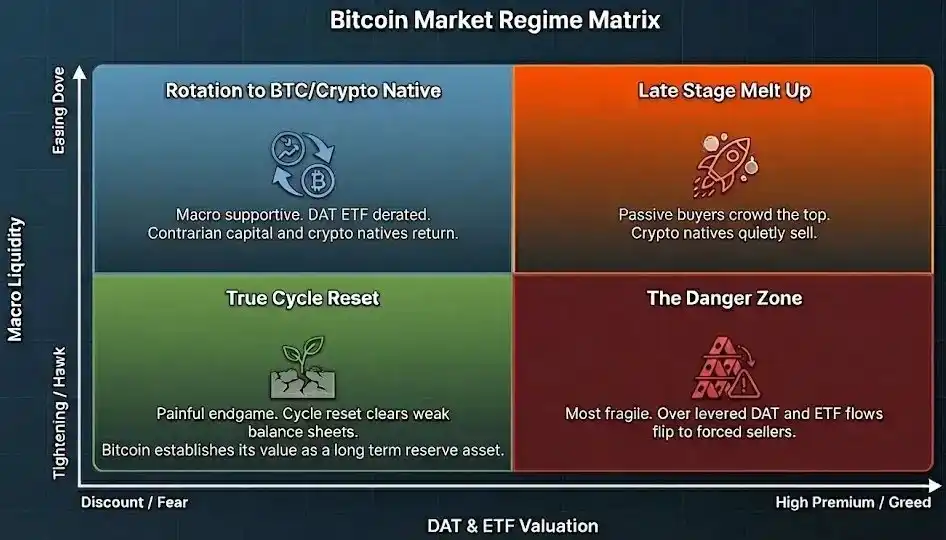

Взгляд на 2026 год

В этой новой структуре первоначальный «четырёхлетний цикл халвинга» больше не является жизнеспособным self-fulfilling путём.

Следующая фаза режима в основном driven двумя осями.

-

Вертикаль: Макро ликвидность и кредитные условия, процентные ставки, фискальная позиция, цикл инвестиций в AI.

-

Горизонталь: Оценка и уровень премии DAT, ETF и других альтернативных активов Биткоина.

Ранние победители Биткоина, включая OGs, майнеров и азиатских серых китов, распределяют монеты среди пассивных держателей ETF, структур DAT и долгосрочного государственного капитала.

Траектория Биткоина, по-видимому, похожа на траекторию FAANG в период с 2013 по 2020 год: рынок медленно переходит от стратегии инвестирования с high beta,主导ствуемой ранними розничными инвесторами и фондами роста, к пассивной аллокационной стратегии,主导ствуемой индексными фондами, пенсионными фондами и sovereign wealth фондами.

Биткоин теперь — это криптоактив, которым легко владеть, не прикасаясь к криптовалюте. Вы можете купить его через брокерский счёт, хранить как ETF, чётко вести accounting и объяснить это инвестиционному комитету трейдера в пяти предложениях.

В то время как оценка большинства других криптоактивов не stems от их actual utility или легитимности в实体ном (physical) рынке и Уолл-стрит.

Мы всегда ждём нового бычьего рынка, но было бы здорово, если бы на этот раз бычий рынок был не просто ростом цены, а ростом utility, способным преобразовать легитимность эпохи ETF в ончейн-спрос, превратить пассивное хранение в активное использование и принести реальную отдачу, а не постоянно меняющиеся narrative.

Если это произойдёт, сегодняшние «игроки, оставшиеся с мешком» (bagholders), будут выглядеть не как пойманные в ловушку одного цикла, а как первые инвесторы нового цикла.

Биткоин в конечном итоге становится государственным резервным активом

Код поглощает банки

Криптовалюте ещё предстоит развиться в новый инструмент цивилизации.