Author: Mohit Pandit

Compiled by: TechFlow Deep Tide

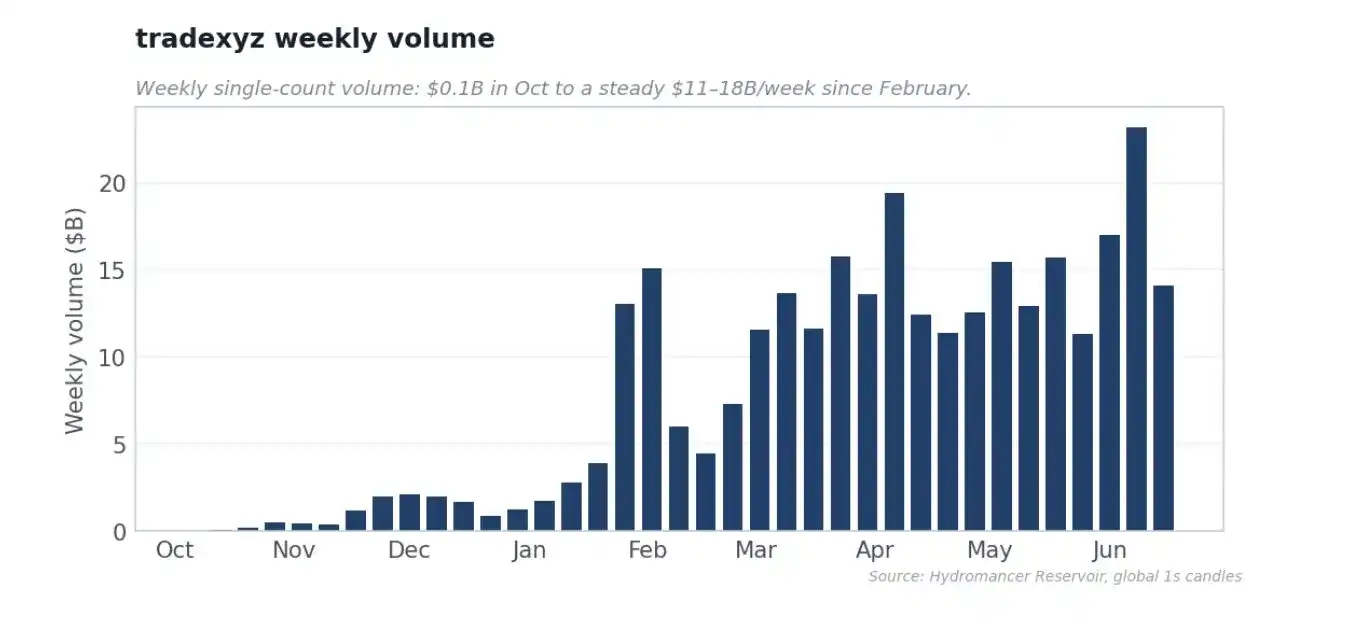

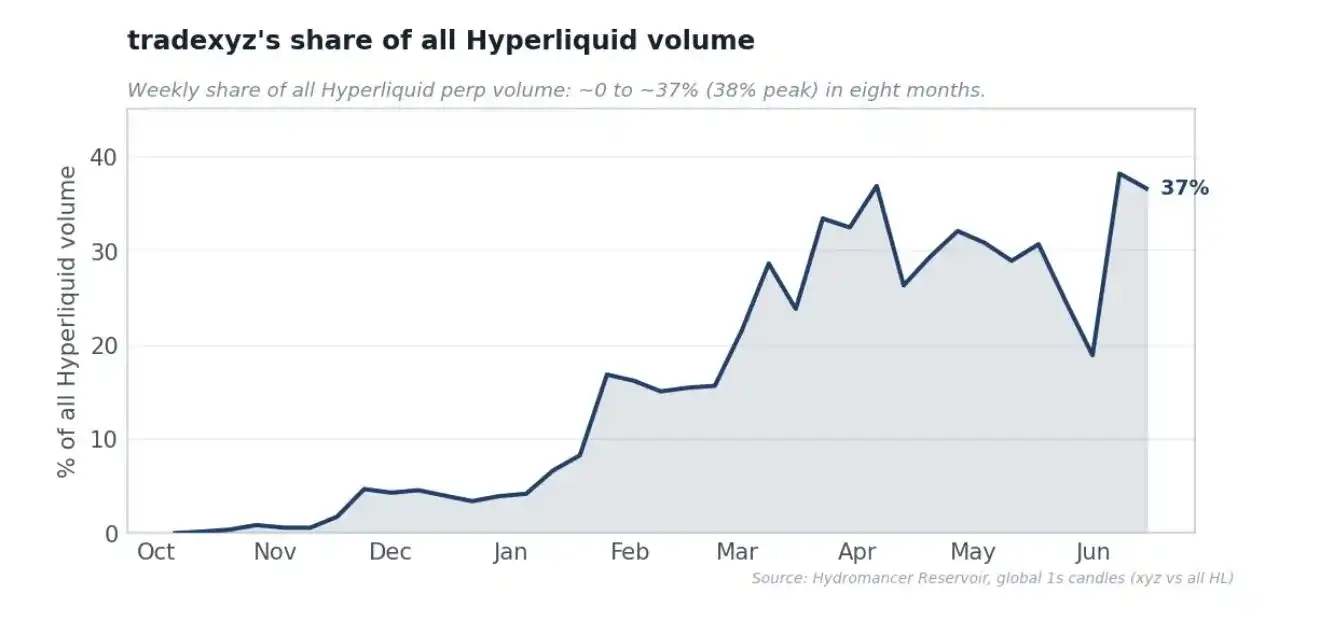

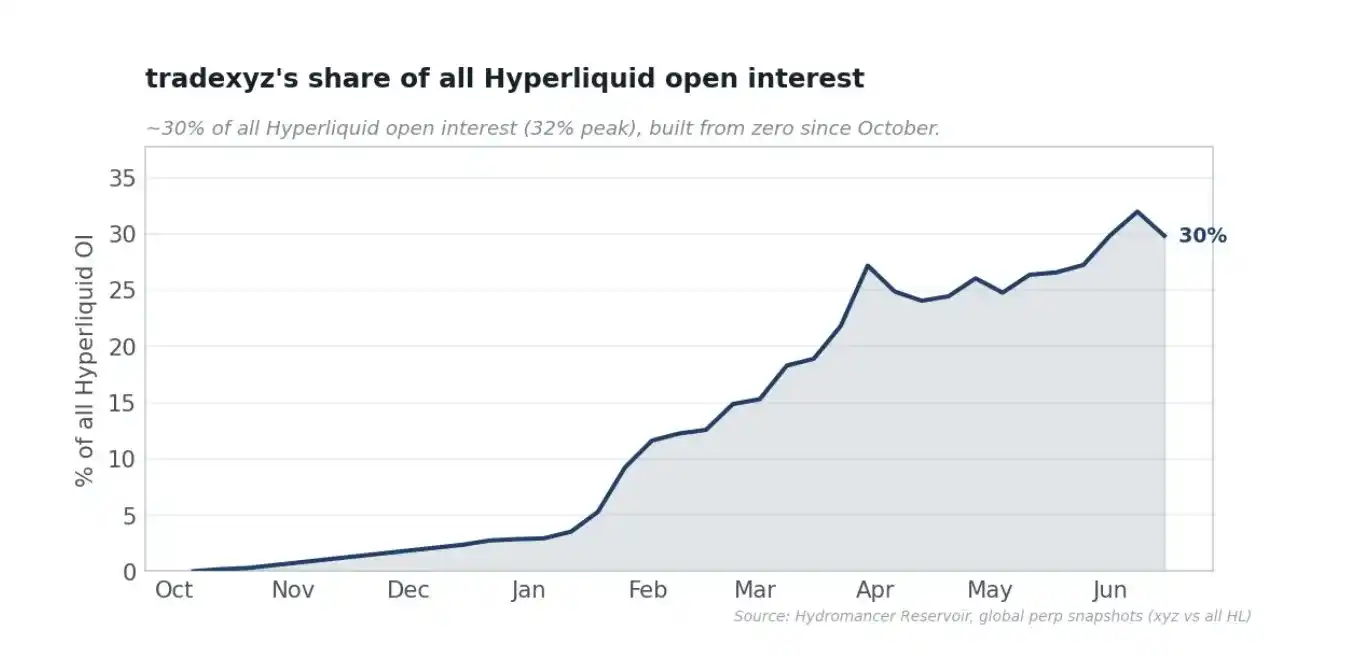

TechFlow Deep Tide Guide: Trade[XYZ] has achieved 98% of HIP-3 trading volume on Hyperliquid, leading many to worry it might overshadow its host. But data shows that Trade[XYZ] built an institutional-grade stock perpetual market in 8 months, brought 300,000 users to Hyperliquid, with 97% of trades occurring through the Hyperliquid frontend, and both sides split fees 50/50—this isn't a threat but a successful validation of Hyperliquid's strategy of "open infrastructure, letting professional teams compete, and letting liquidity decide the winner."

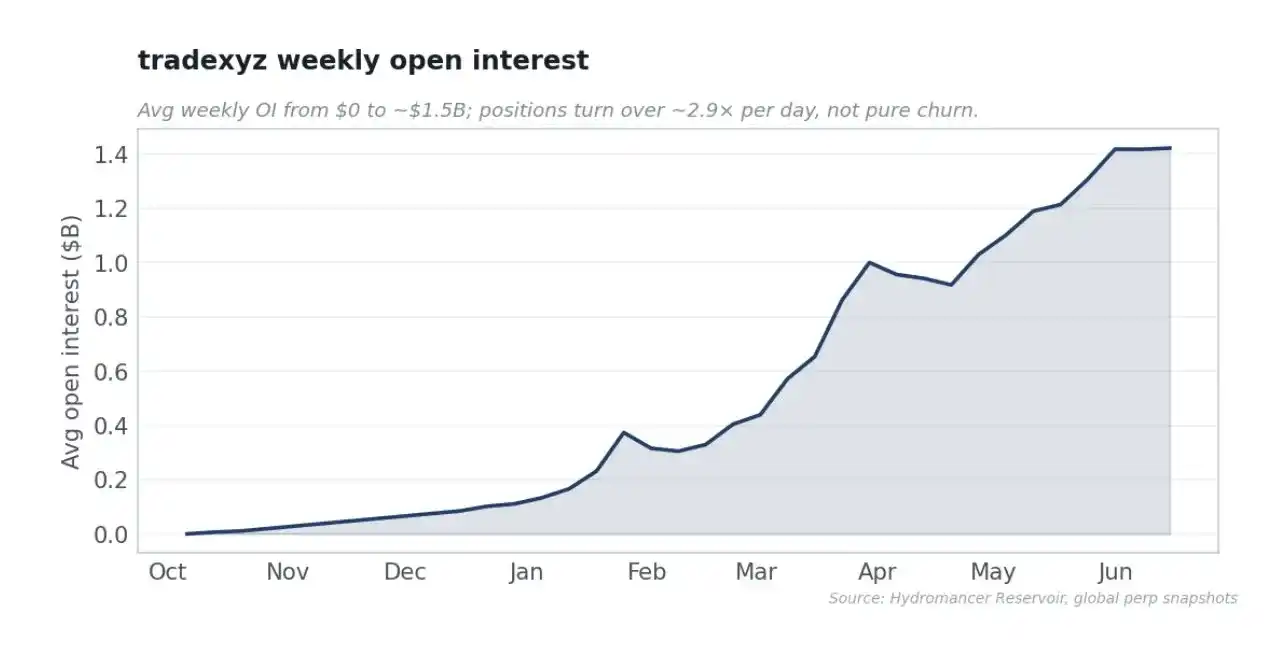

(Data as of June 2026) With each rise in HIP-3 open interest, each basis point jump in trading volume share, each new pre-IPO asset listing, every tweet about Hyperliquid leading price discovery for the world's largest, most watched assets, the voice in everyone's mind grows louder.

Is Trade[XYZ] an existential threat to Hyperliquid? Has Hyperliquid handed over the keys to the kingdom? If Trade[XYZ] issues a token, is HYPE finished?

I intend to use data and first principles to argue why I believe Trade[XYZ] is value-additive to Hyperliquid, and thus to HYPE.

The conventional argument is narrow: Trade[XYZ] locks HYPE, lists and operates new markets, generates trading fees, and recycles fees back to HYPE for buybacks. This is indeed true, but in my view, it underestimates the relationship between Hyperliquid and deployers, specifically @tradexyz here. The reality is, Trade[XYZ] spent 8 months building the hardest thing in this category: a truly liquid market for stock, index, commodity, and FX perpetual contracts, proving HIP-3 can host a professionally built, institutionally liquid non-crypto perpetual vertical, while Hyperliquid retains users, matching engine activity, fee splits, auction demand, and ecosystem narrative without directly taking on listing or regulatory responsibility.

Two Paths to Build a Large Derivatives Exchange

The vertical path is to build all markets yourself, source assets, run oracles, recruit market makers, bear risk, and keep all rewards; Lighter and Ostium (pure RWA) are vertically integrated products. The horizontal path is to provide the base layer and let permissionless deployers build markets on top, sharing fees; this is Hyperliquid's HIP-3, and @tradexyz is one such deployer. But thinking of HIP-3 as horizontal for horizontality's sake is wrong. The right way to understand it is: it's an access application.

Hyperliquid's belief is that the lasting advantage of on-chain finance lies in core infrastructure—L1, clearinghouse, matching engine—and the core team spends almost all its energy here. The bet is: the best operators will choose to build on this infrastructure, and to attract the best operators, it needs to continuously evolve towards high performance and neutrality. There is only one CME, one NYSE, one Hong Kong Exchange in the world. Liquidity attracts liquidity; a category without a single deep liquidity winner has effectively already lost. Hyperliquid's ambition is to become the home for all finance, the neutral substrate on which winners in each category build, and HIP-3 is the mechanism to achieve that. It doesn't anoint winners; it opens the track, invites the best operators to compete in building the deepest markets, and lets liquidity itself decide. The eventual winner returns immense value to Hyperliquid: fees, buybacks, users, while also keeping real rewards for themselves. In this view, concentration is not a failure of the model; it's the model working as finance always has.

However, there are many objections to this model, and I think they should be heard fairly.

The first is that Hyperliquid is giving up future value, letting deployers keep about half the fees and own the franchise, foregoing revenue it could have captured by building stock perpetuals itself. The second is sharper: HIP-3 is vertical integration in disguise. One deployer does about 98% of HIP-3 volume, raising allegations of favoritism (often pointing to Trade[XYZ]'s connection to the Unit ecosystem), while Hyperliquid still takes 50% of the fees.

My take is that this greatly underestimates how difficult it is to build an institutional-grade real-world asset market. The entire goal of this report is to present a data-backed, first-principles analysis: is this current model even a little successful?

What It Takes to Build a Stock Perpetuals Market

"Just list the assets" is the most common misread of this business. Listing is the easy part; the hard part and the moat is making newly listed markets tradeable at scale. Trade[XYZ]'s data points to three clear hurdles: 1. Listing fast enough to capture demand 2. Acquiring market makers that create depth 3. Keeping liquidity economically real and day-to-day operations of these markets

Listing Speed

A perpetual market is only valuable if it exists by the time a trader thinks of it. Measuring from the precise on-chain registration of each asset to the first trade, Trade[XYZ]'s median time-to-launch is only 3.3 days, 65% of markets launch within a week, 47% within three days.

Tradable Markets Are the Real Moat

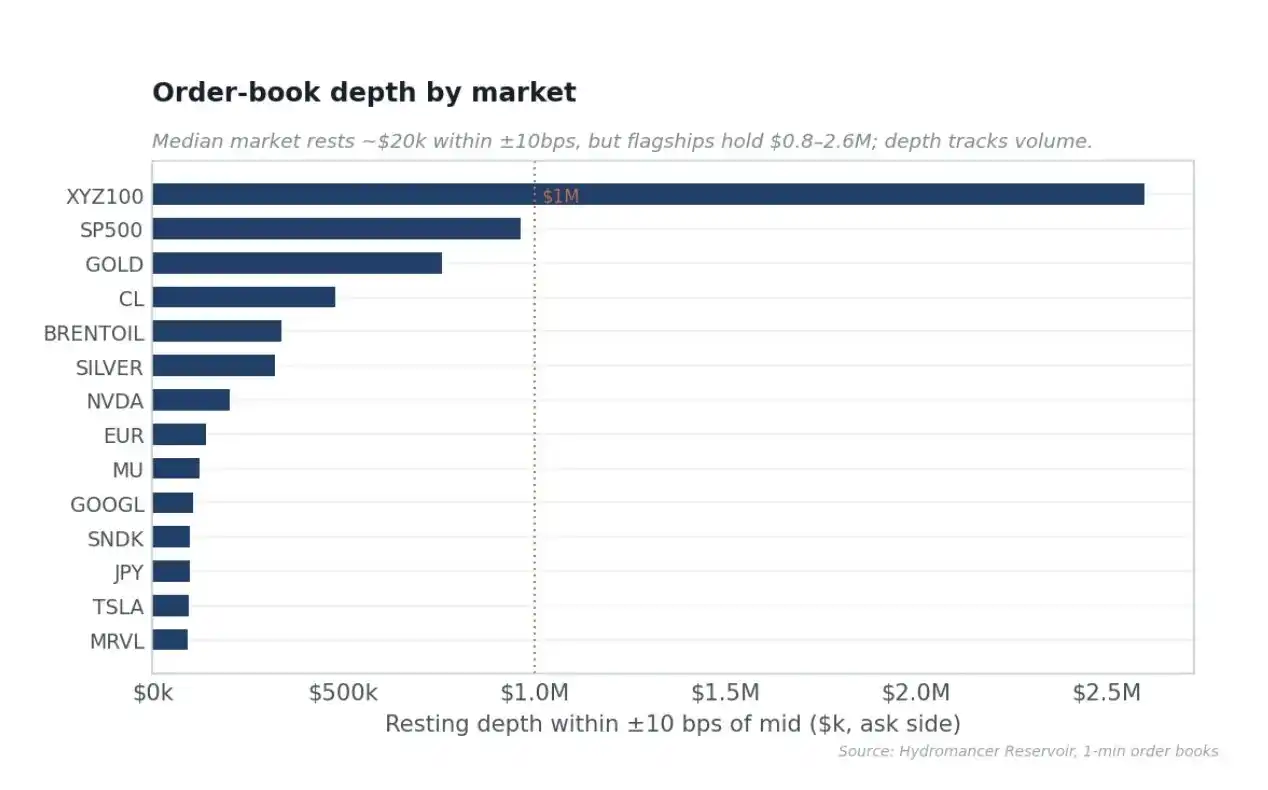

Trade[XYZ]'s depth is both deep and rationally allocated. The flagship index and commodity markets have institutional-level limit order depth, with XYZ100 having $2.6 million within 10 bps of mid-price, S&P 500 market $964k, Gold $759k, while single stocks like Nvidia and Tesla also have enough volume for comfortable trading. In contrast, the median market only posts about $20k within 10 bps. This is how rational market makers allocate capital.

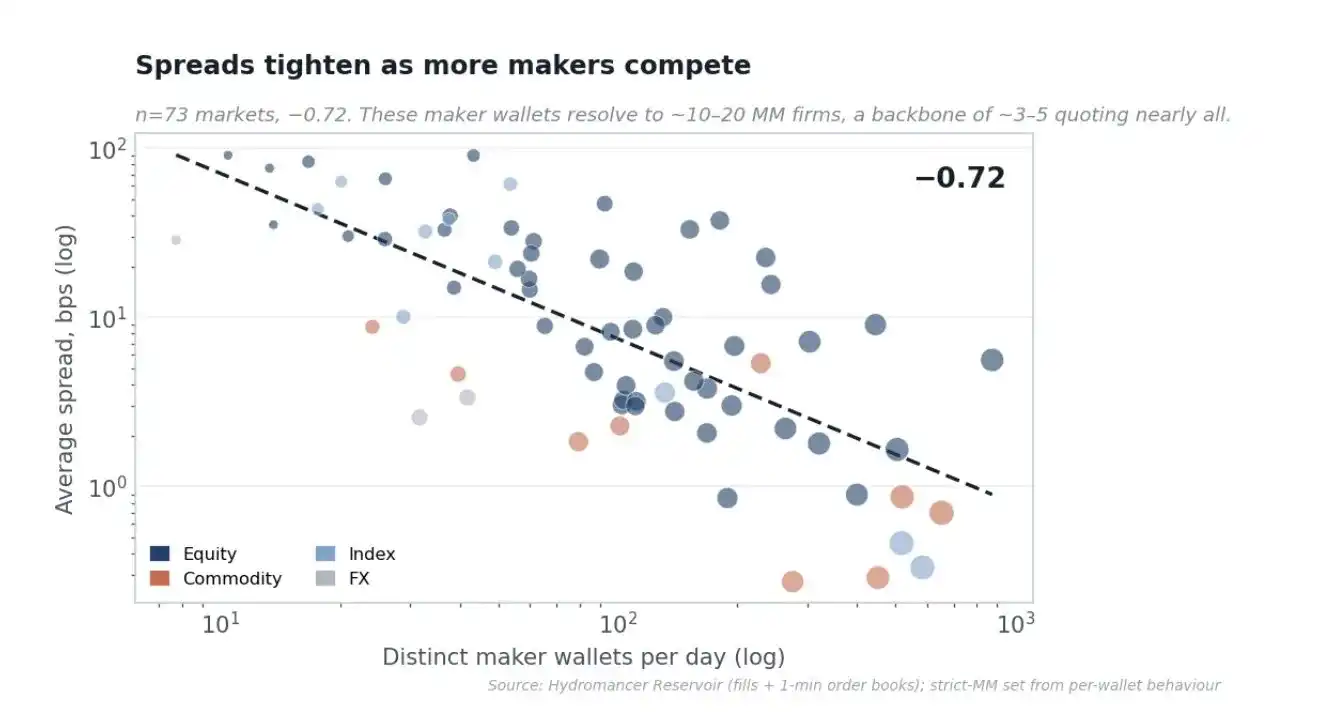

Acquiring market makers is the real skill, and their presence is what tightens markets. Across 73 markets with sufficient data, daily unique market maker wallet count correlates with spreads at -0.72, volume with spreads at -0.82, volume with open interest at +0.96. The full-book volume-weighted average spread is 2.33 bps, daily turnover is about 2.9x open interest. Trade[XYZ]'s edge is the BD work and capital work to acquire market makers, and this work produces tight, deep markets.

It's worth asking from first principles why acquiring this liquidity is a hurdle, and why only one deployer has successfully scaled these markets. Market makers earn spreads, but can only survive by managing what each trade leaves on the book. Simply, market makers need ways to hedge. The primary risk is pure inventory risk: each trade leaves the desk long or short, an unhedged trending position is a big red flag. For stocks, the key is hedging. Crypto perpetuals can be hedged 24/7 on another crypto exchange, but the only real hedge for a stock perpetual is the underlying stock, ETF, or futures, which only trade when the spot market is open. During regular hours, a desk can hedge its TSLA perpetual inventory with TSLA stock, capturing the spread with almost no risk, so it can quote tight, deep prices. But as soon as the market closes, it's holding naked inventory, and the rational response is to widen spreads, reduce depth, or stop quoting. Pre-IPO there is no hedge at all, which is why those order books are thin before listing. Add adverse selection (a larger share of post-market flow is informed), funding rates and carry (funding must tether the perpetual to the index without making hedging uneconomic), and oracle or gap risk (perpetuals settle against an oracle, and stale, manipulable, or gappy marks are an uncontrollable liquidation risk that prevents quoting a book at size).

Discovery Bounds cap the mark price to within plus or minus one over the max leverage of the reference price (20x leverage ~5%), re-anchoring in discrete, per-market-capped steps, as a hard cap until external pricing resumes, paired with liquidation protection that prevents positions from being liquidated when the liquidation price is outside the active bound. Simply, there's a "known ceiling" on how far price can move in a single go, and the exchange won't liquidate desks within that ceiling, so unhedgeable overnight inventory's worst case is bounded and quantifiable, not open-ended. Finally, per-market funding rate multipliers scale the standard funding rate by 0.5 (roughly 5.5% annualized baseline), but drop to 0.005 for pre-IPO names. Funding rates tether the perpetual to fair value without bleeding market makers dry, and for pre-IPO names where there's no stock to arbitrage, it's almost fully off, so holding a position itself is not unprofitable. These together are a toolkit to make markets that, by first principles, should become unmakable once hedging vanishes.

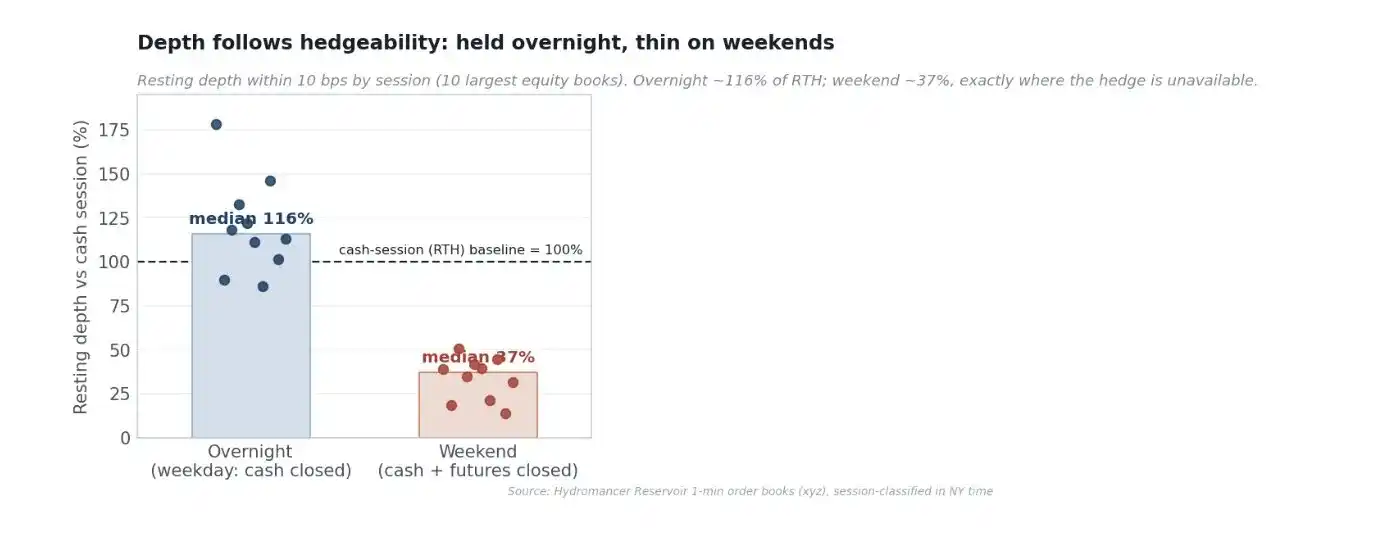

Measuring the top ten stock order book depth by session, overnight depth holds at about 116% of spot-session levels, and single stocks like Nvidia and Tesla actually deepen because the perpetual is the only active price once the spot market closes, concentrating quotes there. On weekends, when even index futures close and hedging vanishes for a full two days, depth shrinks to about 37%. A boundary should be honestly stated: this makes Trade[XYZ]'s post-market books resilient, but not magically superior. The enduring differentiators remain its intraday depth, order flow, and breadth across truly hard-to-make markets. What the data supports is that Trade[XYZ]'s risk mechanics let market makers retain depth overnight where first principles predict collapse, which is itself non-trivial engineering that makes these markets makable.

Trade[XYZ] Is Not a List-and-Leave Business

Trade[XYZ] does not list and walk away. Across the recent ~300 on-chain operation windows, it executed 294 distinct risk management actions. 54 open interest cap changes, 35 growth mode toggles, 34 funding multiplier adjustments, 28 trading suspensions, and 11 margin mode changes, plus per-asset annotations. This is ongoing, per-market risk management across 92 underlying assets, handling real trading hours, halts, and funding rates—a full-time market operations business.

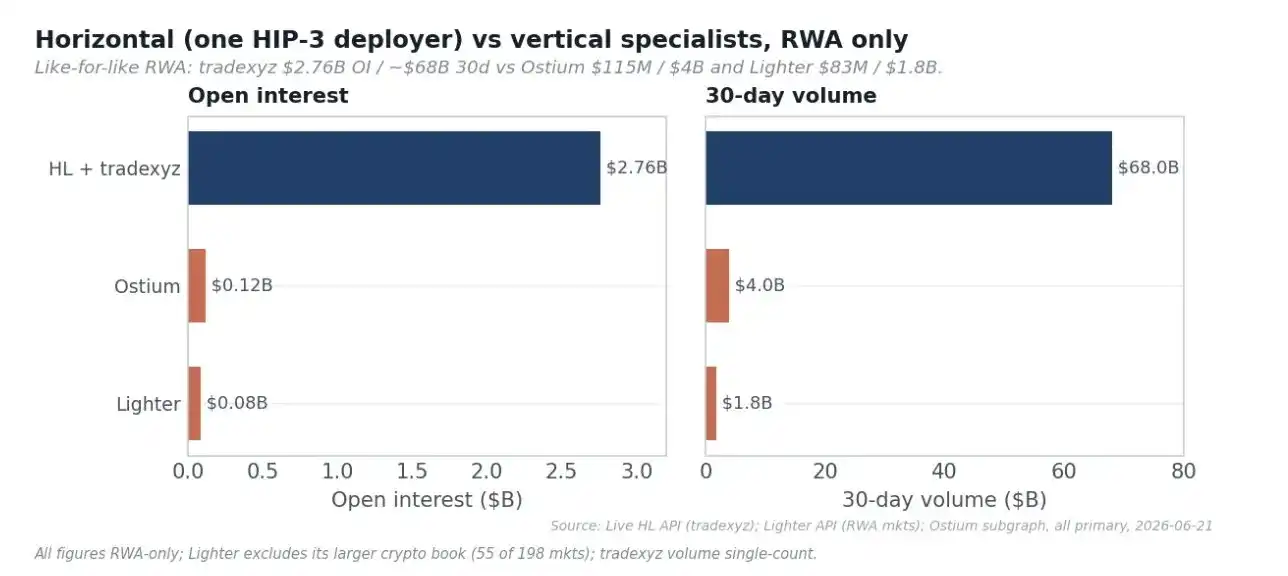

It's best understood by comparison. Tokenized spot stocks (xStocks) on Solana represent over $25B in cumulative volume, but actual DEX volume is only about $517M. Ostium is a dedicated, funded RWA perpetual DEX with ~$59B in cumulative volume, but open interest is only ~$115M, 1/24th of Trade[XYZ]'s. Newer entrants like Variational don't even attempt to build native depth, instead aggregating liquidity from Hyperliquid, Lighter, and CEXs via RFQ, routing to Hyperliquid for the very liquidity being discussed. The leader in on-chain stock perpetuals, by a wide margin, is Trade[XYZ] on Hyperliquid.

Trade[XYZ] Markets Expand Hyperliquid's User Base, Hyperliquid Benefits from Its Network Effects

The natural assumption is that deployers own users through their own frontends. The truth is the opposite. Tagging each fill with the frontend (builder) code that generated it, measured on the taker side—the party choosing the frontend—shows about 97% of Trade[XYZ] market volume trades through Hyperliquid's own app and API, all third-party frontends combined account for ~3%, with Trade[XYZ]'s own frontend just a sliver of that. In other words, nearly every trade on Trade[XYZ]'s product happens on Hyperliquid's interface.

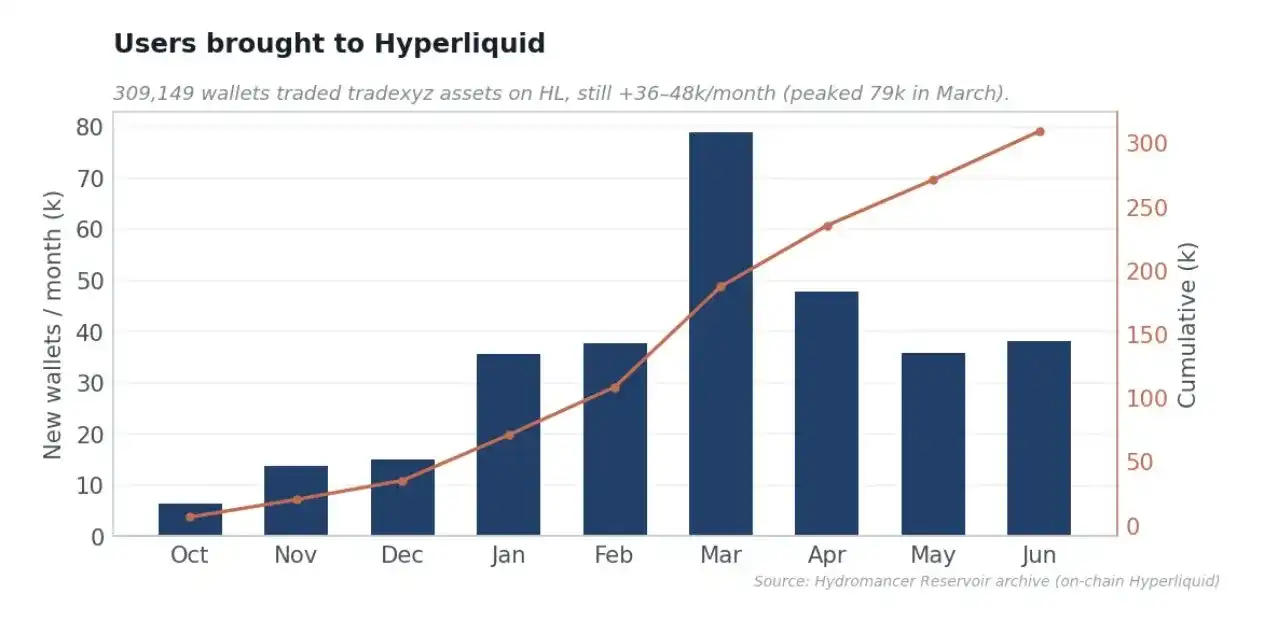

The customer acquisition this represents is material and ongoing. Trade[XYZ] has cumulatively brought ~300k+ distinct wallets to Hyperliquid, still adding 36k to 48k monthly, peaking near 79k in March during the SpaceX listing surge. Stock and RWA perpetuals as top-of-funnel customer acquisition: assets are the bait, Hyperliquid is the landing, trading, and staying place for users that come from it. This is real attention and user acquisition value that never shows up on a fee table.

Incentives Are Aligned Correctly at the Protocol Level

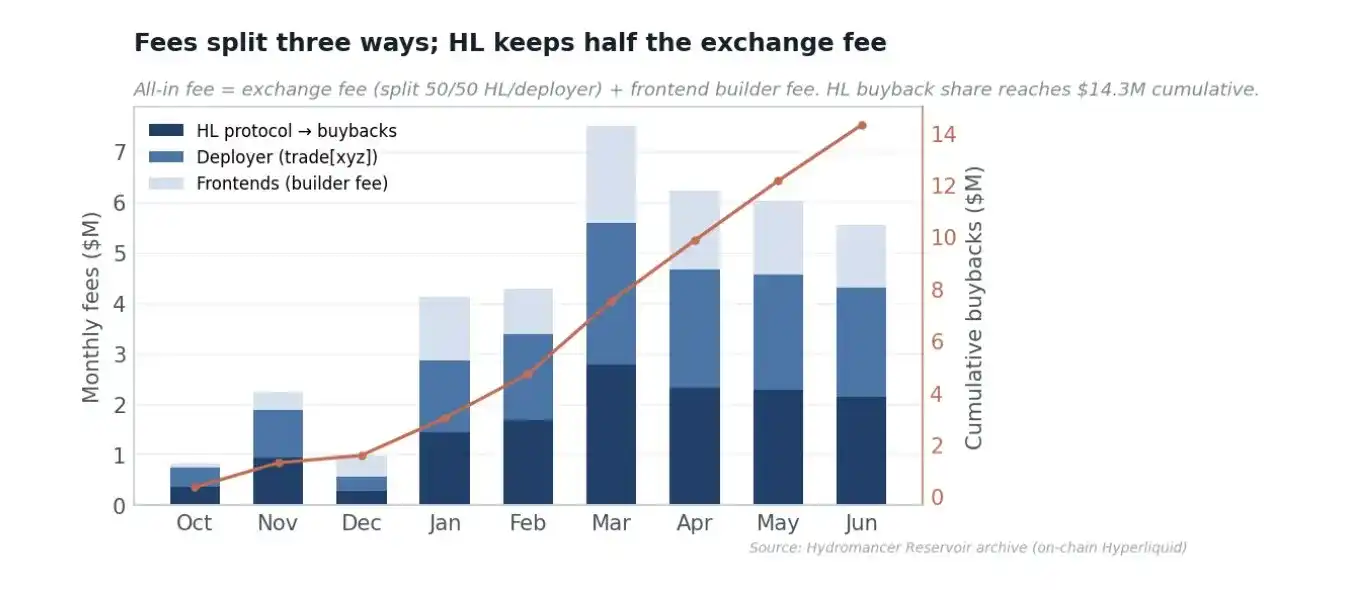

Total taker fees for HIP-3 are ~$37.9M, split three ways. About $9.2M in builder code fees go to third-party frontends, not the deployer's; the remaining exchange fees are split 50/50 between Hyperliquid and the deployer. So Hyperliquid's protocol share, directed to HYPE buybacks, is ~$14.3M, and the deployer's accrued share is ~$14.3M. HIP-3 caps the deployer share; Hyperliquid's protocol fees match any deployer share above 100%, so the deployer never gets more than half. Cheap, deep markets attract the volume that generates fees itself.

My Take on Growth Mode

HIP-3 deployers choose a fee model per market: standard mode charges takers 9 bps and makers 3 bps, while growth mode charges 0.9 bps and 0.3 bps, a ~90% reduction. Growth mode is restricted to non-crypto real-world assets, explicitly excluding crypto wrappers like MSTR, and notably also excluding GOLD because it overlaps with the existing PAXG-USDC market. This exclusion provides a clear natural experiment.

Today, eligible growth-mode order books have fees near 0.86 bps, while excluded names have fees near 7 bps, an 8x gap on the same matching engine. RWA perpetuals compete with traditional finance on total cost. A 9 bps fee cannot compete with CME index futures or spot stock commissions, while 0.9 bps is competitive and offers 24/7 trading with leverage. Cheap, deep markets are how to win share, and depth and market maker base form from it. In a category that tends toward a single winner, maximizing volume, open interest, users, and reference price status has value.

Yet, growth mode is not the reason volume exists, as three datapoints prove. First is the on-chain control: six of the other seven HIP-3 deployers have the same fee tools but have near-zero volume; the second-largest deployer (dreamcash) even quotes narrower spreads but remains ~30x smaller; if low fees drove volume, dreamcash should be close. Second is the GOLD experiment: GOLD pays ~8x the fees of growth books, but it is the single largest fee market, top three by volume and open interest. Traders are willing to pay full fees for GOLD because liquidity is there.

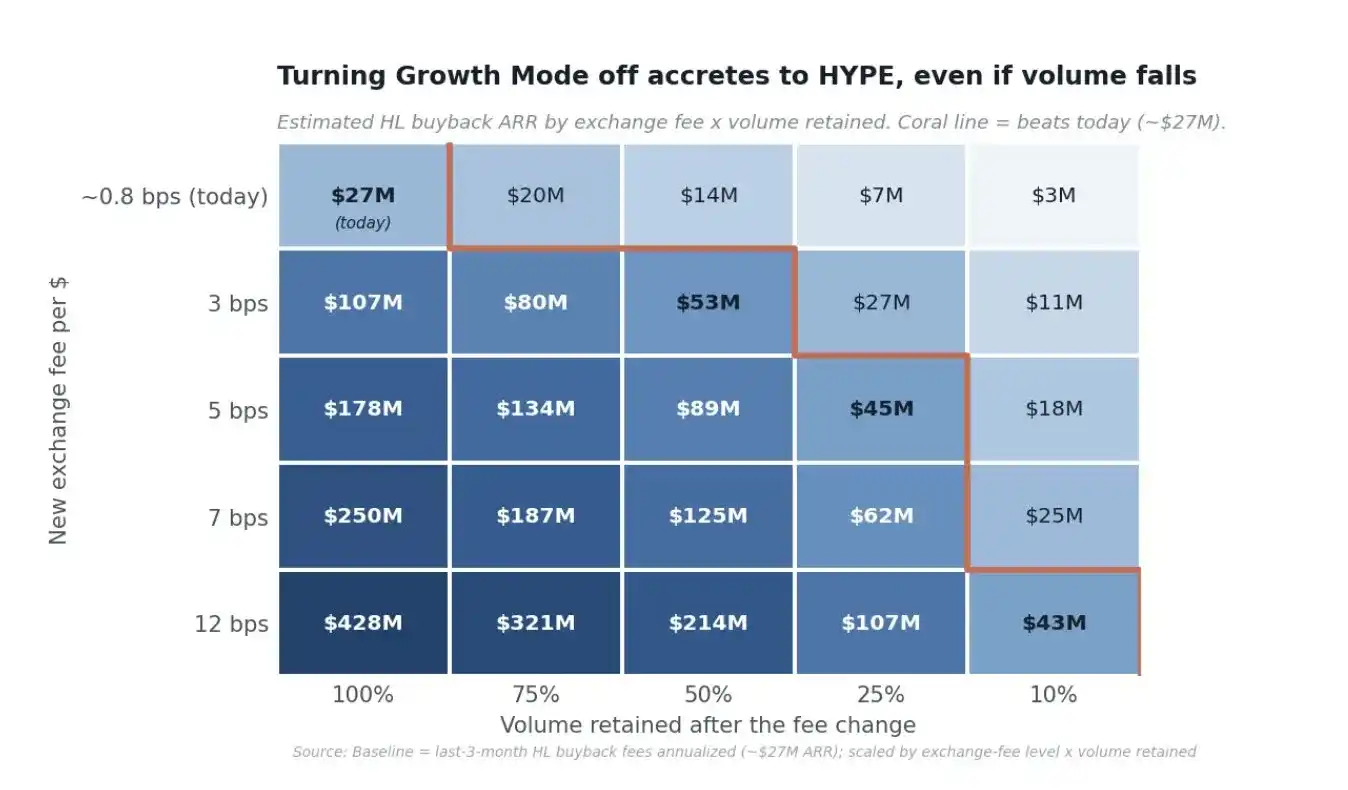

That's why turning it off wouldn't kill volume; it would direct more value to HYPE. Because exchange fees are split 50/50 in both modes, raising fees would boost HYPE's value ~9x to 15x (from ~0.9 bps in growth to ~9-12 bps in standard), so even with a substantial volume drop, Hyperliquid's buyback share would rise unless volume collapsed more than ~85%.

At the 7 bps observed for GOLD, tradexyz would need only ~11% of today's volume to match today's buyback (at 5 bps ~15%, at 3 bps ~25%). A realistic monetization path would be adjusting mature markets to 5-7 bps, capturing half to three-quarters of volume given the moat, directing ~$90M-$185M annually to buybacks, 3-5x current levels. This isn't hypothetical: GOLD already operates at standard rates, converting 4.3% of volume into 23% of all buybacks. The turn-off-growth-mode scenario is observed in real-time on a single market and proves deep RWA markets keep trading at standard fees, making a >85% collapse unlikely. The two phases are a strategy, build moat cheaply now, monetize later, both delivering value to HYPE: users, volume, OI, reference price status first, then fees.

Market-by-Market Dynamics

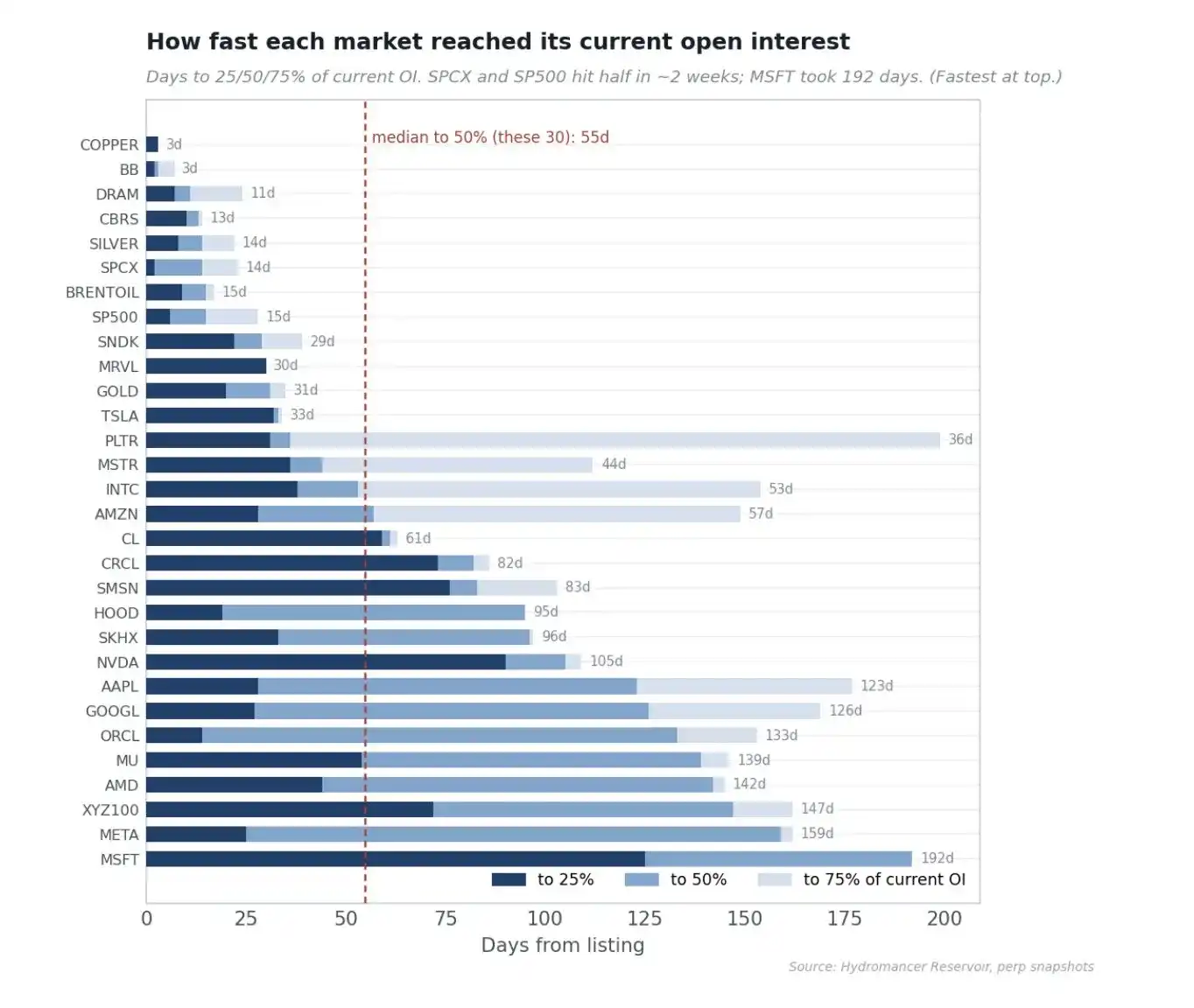

The top 30 markets hold ~95% of open interest, led by S&P 500, XYZ100 index, Brent Crude, and WTI. More interesting than the levels is the speed each market reached them. Measuring days from listing to reaching 25%, 50%, and 75% of current OI, the median market hits a quarter of its final size in 9 days, half in 15, three-quarters in 30, but spreads are huge and telling. The fastest markets reach half their current OI in about two weeks (SpaceX 14 days, S&P 500 and Silver ~15 days), while the earliest single stocks listed when the venue's liquidity infrastructure was nascent, taking five to six months (Microsoft 192 days, Meta 159 days). This spread is the deployer learning curve made concrete: recent listings grow far faster than early batches because market maker relationships and tools exist on day one now.

Proof of Market Quality

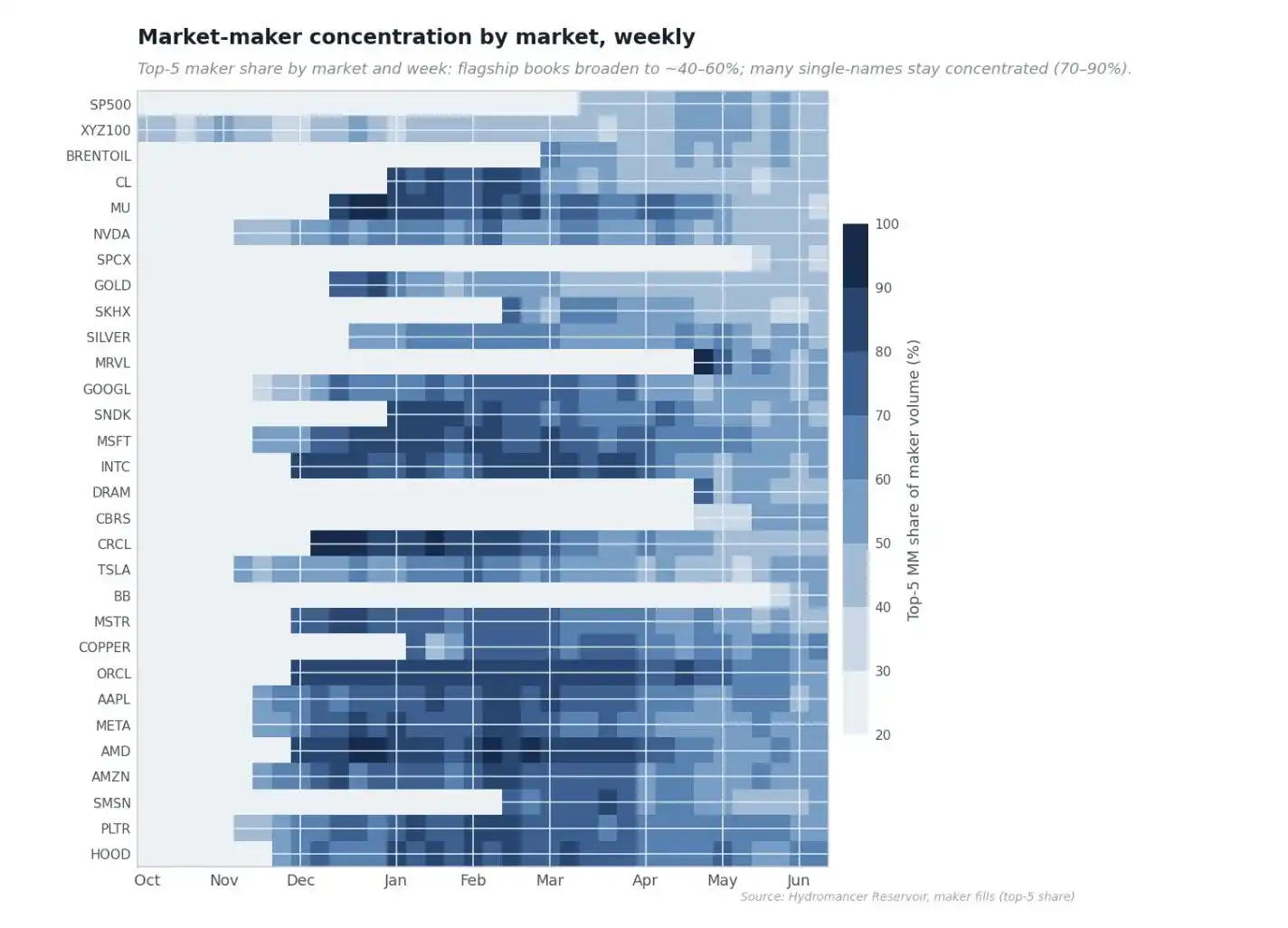

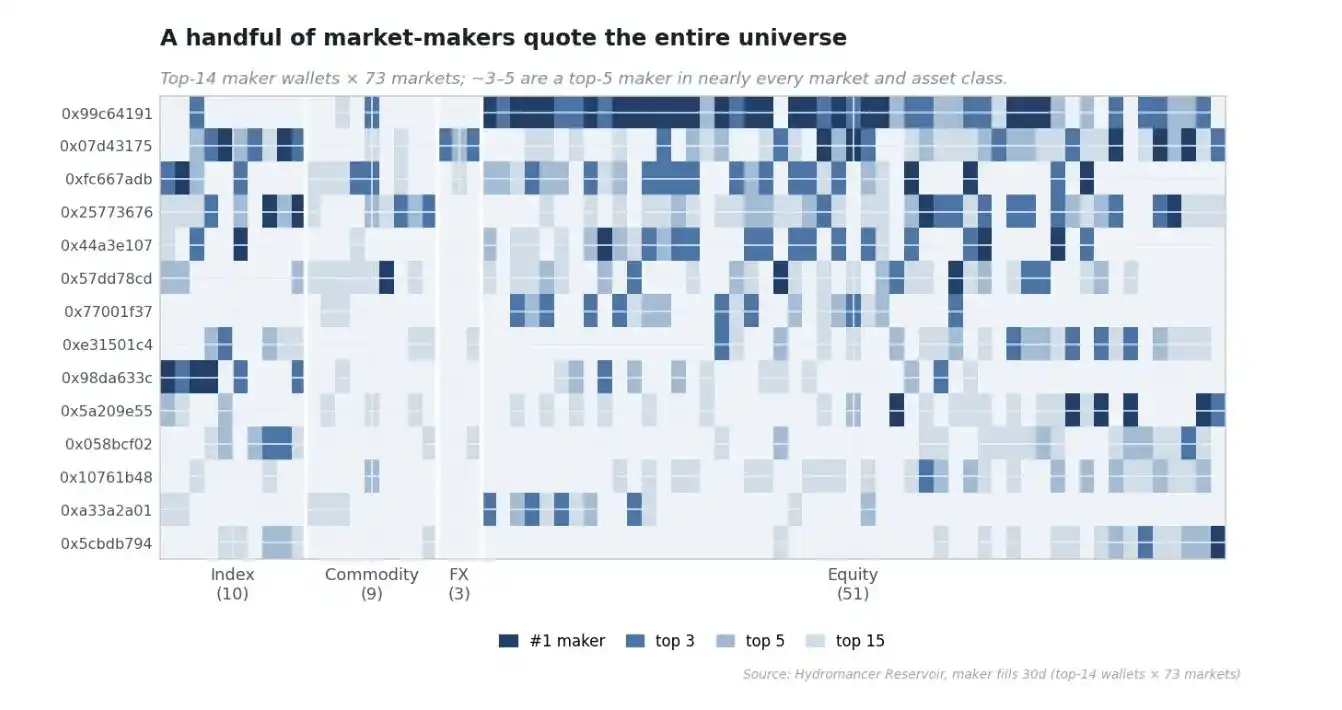

A. Market Maker Concentration Per Market Over Time

As Tradexyz matures, liquidity provision has broadened. The heatmap below shows, for each market and week, the share of its maker volume captured by its top five market makers. Early markets are deep blue; in the first months, a handful of market makers provided almost all passive liquidity (top five share >90%). Over time, the largest, most liquid markets lighten as more market makers compete to quote, while many single stocks remain concentrated. More concentrated order books aren't bad per se—it's how markets bootstrap—but flagship markets becoming competitive is a healthy sign that liquidity provision on tradexyz is now a contested business at the top of the book, not the grace of one or two market makers.

B. Market Maker Anchors

A natural question is whether a handful of firms quote the whole market or each market attracts its own specialists. Ranking the top makers per market over a 30-day window and asking which wallets recur at the top across markets reveals a clear anchor set. The single largest anchor wallet is a top-five maker in 47 of 73 markets, #1 in 22; the top three anchor wallets combined are top-three makers in 57 of 73 markets. Several of these wallets simultaneously quote across all four asset classes: stocks, commodities, FX, and indices, all with textbook market maker signatures: directionality within a percent, realized PnL within rounding error of zero.

Sources of Fees

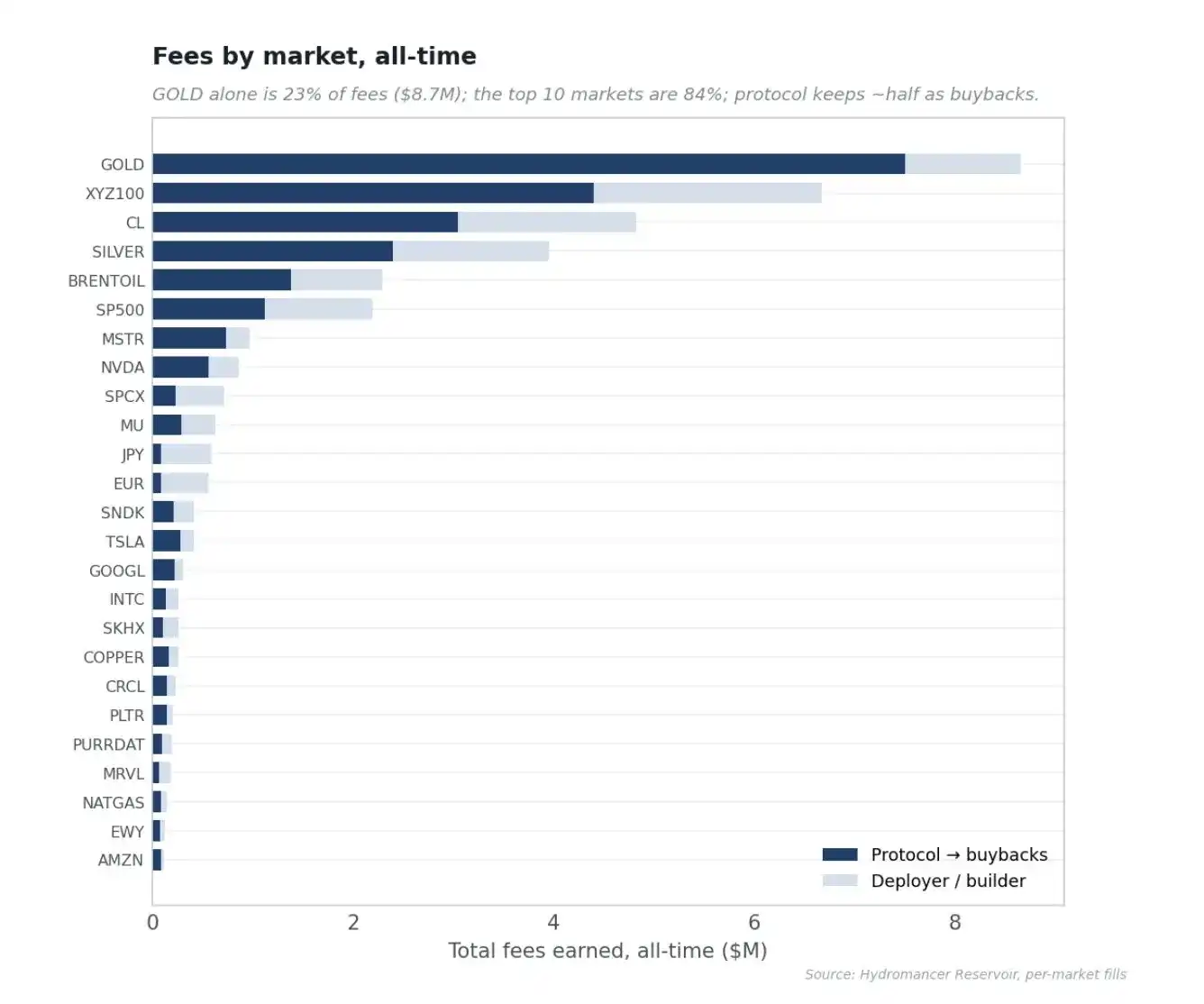

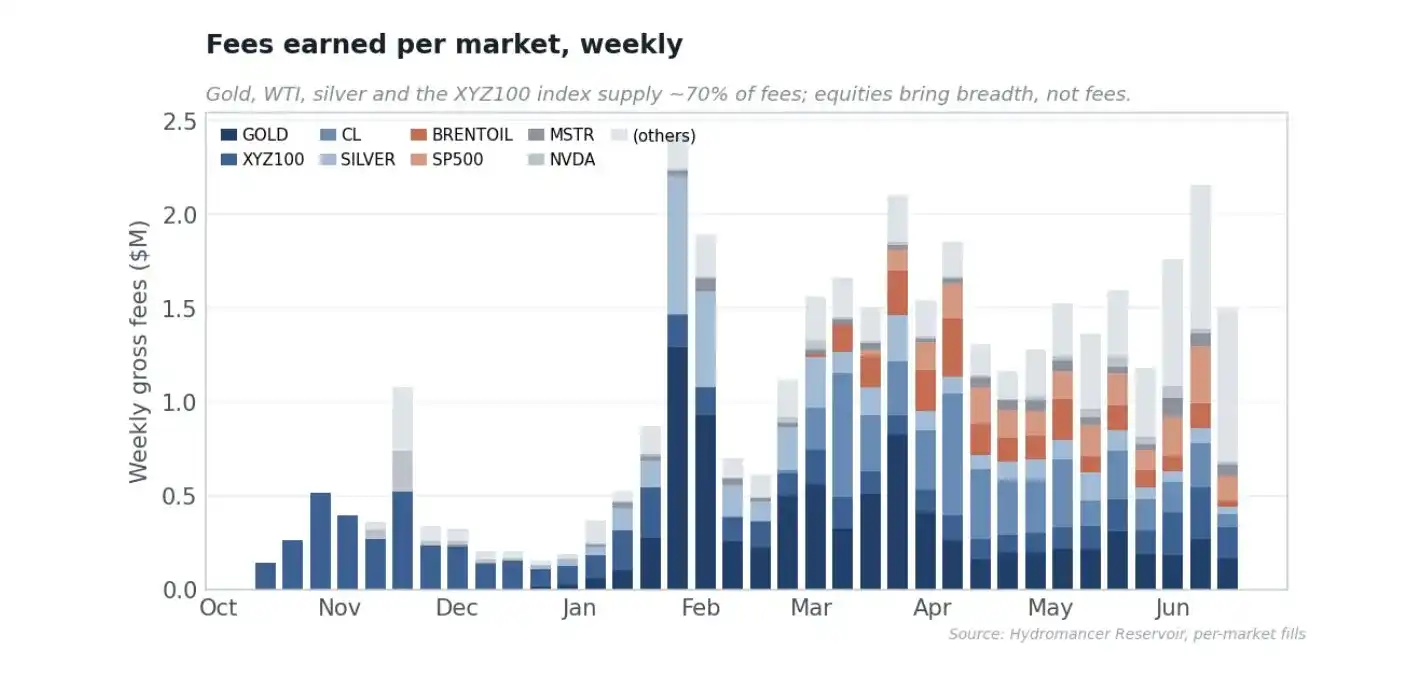

The fee base is driven by commodities and indices. Commodities alone account for 54% of all fees earned, indices 24%, and the entire long tail of single stocks and FX is 22%, despite stocks being the bulk of listings. Gold is the single largest contributor at 23% of fees ($8.7M), followed by XYZ100 index (18%), WTI crude (13%), and Silver (10%); the top ten markets generate 84% of all fees.

A nuance forced by GOLD's exclusion is that fee rank is not volume rank, because fee models differ by market, circling back to growth mode. GOLD is the only large market excluded from growth mode, so it pays ~7 bps while the rest of the book pays ~1 bps, making it the #1 fee market on that alone: it accounts for just 4.3% of volume but 23% of all fees. By trading activity, GOLD is a minor market; by buyback fuel, it's massive.

Could the Core Team Have Done This Themselves?

My assessment is they couldn't, and more importantly, they shouldn't. The strongest reason is regulation. Listing NVIDIA, TSLA, and pre-IPO SpaceX perpetuals sits squarely in the securities derivatives arena, and HIP-3 deliberately externalizes that responsibility to deployers. If the core team listed stocks themselves, it would bring the protocol, foundation, and HYPE directly into regulators' crosshairs. Keeping listings at arm's length isn't a missed opportunity; it's by design.

The rest of the reasons compound this. Hyperliquid's value is being credibly neutral infrastructure; core team picking assets would undermine the permissionless argument and the deployment auction fee market HIP-3 aims to monetize. Operating 92 stock, FX, and commodity markets, sourcing oracles, handling market hours and halts, cultivating market makers, and executing the hundreds of on-chain visible risk actions is a full operational business orthogonal to building a high-performance exchange. BD-ing for top-tier market makers for niche RWA perpetuals is relationship and capital work, not protocol engineering, and it's here even funded specialists have moved slowly. The empirical record settles the question: if this were easy or could be done in-house, one would expect the core team to have done it, or many strong deployers to exist. Instead, the second-largest deployer is 46x smaller, dedicated standalone RWA venues are 24x to 33x shallower, and new entrants route liquidity back to Hyperliquid. Scarcity is proof of difficulty.

I want to end with the analogy that struck me most. What Tether did for global dollar access, is being done for global equity access. All data in the article was provided by the elite folks at @hydromancerxyz.