Автор: Клод, Shenchao TechFlow

Обзор Shenchao: Долгосрочные облигации развитых стран коллективно теряют поддержку. Рынок переоценивает уже не фискальные сюрпризы отдельной страны, а реальность длительного сосуществования высокого госдолга, высокого дефицита и еще более высоких процентных ставок. Когда рост долга устойчиво опережает экономический рост, энергетический шок вновь разжигает инфляцию, а пространство для снижения ставок центральными банками сжимается, «модель рефинансирования по низким ставкам», поддерживавшая финансирование развитых стран последние десять с лишним лет, дает трещины.

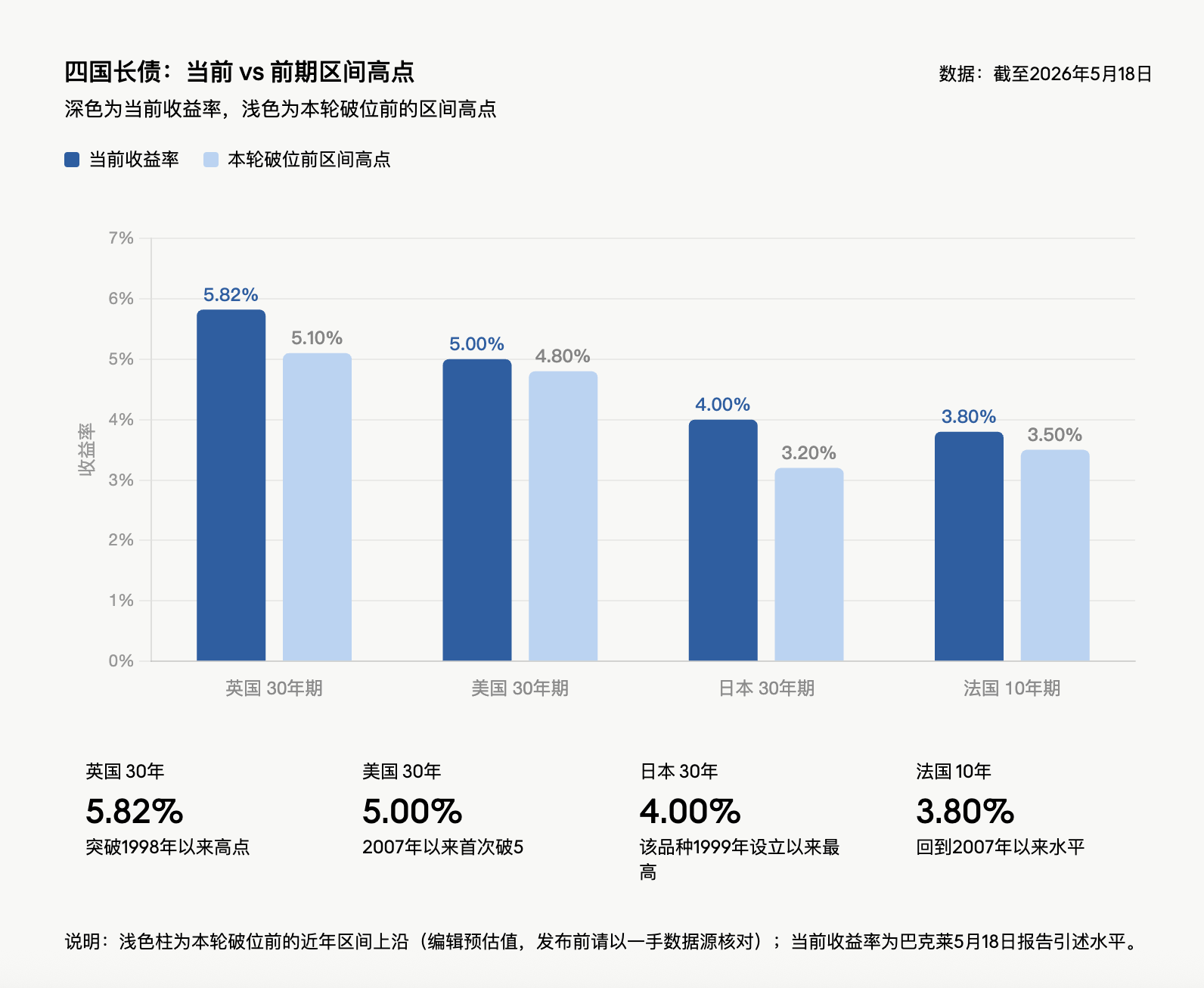

За последнюю неделю доходность 30-летних британских гособлигаций выросла до 5,82%, достигнув максимума с 1998 года; доходность 30-летних японских гособлигаций достигла 4%, что является наивысшим показателем с момента запуска этого инструмента в 1999 году; доходность 30-летних казначейских облигаций США впервые с 2007 года превысила 5%; доходность 10-летних французских гособлигаций достигла 3,8%, также вернувшись к уровням 2007 года. Эта распродажа уже оказала давление на глобальные фондовые рынки, и на этой неделе министры финансов стран G7 на своем совещании специально обсудят эту волну продаж облигаций.

Как отмечает Аджай Раджадхьякша из отдела исследований фиксированного дохода, валют и сырьевых товаров Barclays в отчете от 18 мая: «Долгосрочные облигации не просто продавались на прошлой неделе, они повсеместно прорываются за пределы диапазонов». Его ключевой вывод: рост долга опережает рост экономики, траектория инфляции ухудшается, а политическая воля к фискальным реформам отсутствует. Даже несмотря на падение долгосрочных облигаций, нет достаточных оснований для увеличения дюрации.

Прия Мисра, управляющий портфелем JPMorgan Asset Management, высказывает аналогичное предупреждение: «Синхронный рост долгосрочных ставок по всему миру имеет тенденцию взаимно усиливаться, а ожидания повышения ставок ФРС также входят в рыночную повестку».

Синхронный прорыв уровней на рынках облигаций многих стран: коллективное проявление «фискальной пирамиды»

Падение рынка облигаций отдельной страны обычно можно объяснить локальной инфляцией, фискальной политикой, политической ситуацией или коммуникацией центрального банка. Но на этот раз Великобритания, Япония, США и Франция практически одновременно прорвали уровни, что указывает на то, что рынок торгует уже не только локальными рисками.

Общие черты очевидны: основные развитые экономики имеют уровень госдолга, как правило, выше 100% ВВП, и их бюджетный дефицит не покрывается номинальным ростом. Дефицит США составляет около 2 трлн долларов, что эквивалентно 6,5% ВВП, при номинальном росте около 4,5-5%; номинальный ВВП Франции в годовом выражении за квартал, закончившийся в марте 2026 года, вырос на 2,2%, а дефицит составляет около 5%; дефицит Великобритании превышает 4%.

Именно в этом заключается ключевое противоречие, на которое указывает «фискальная пирамида»: правительства постоянно полагаются на новые заимствования и рефинансирование для поддержания расходов, но скорость роста долга превышает темпы экономического роста, а стоимость обслуживания долга вновь растет. Пока эта комбинация не изменится, долгосрочным облигациям потребуется более высокая доходность, чтобы привлекать покупателей.

Новые расходы продолжают увеличивать давление. НАТО в прошлом году в Гааге согласилась увеличить цель по оборонным расходам до 5% ВВП к 2035 году; расходы на оборону в Европе в прошлом году уже продемонстрировали двузначный рост в процентном выражении и могут сохраняться в течение десятилетия; правительство США запросило у Конгресса ассигнования на оборону в размере 1,5 трлн долларов на следующий финансовый год. Эти расходы не компенсируются соответствующими сокращениями.

Блокада Ормузского пролива: нефтяной шок поджигает инфляцию

Долг и дефицит уже были уязвимы, а шок цен на энергоносители еще больше сужает пространство для политики. Блокада Ормузского пролива стала непосредственным триггером текущей турбулентности на рынке облигаций. Препятствия на этом важнейшем в мире нефтяном транспортном пути постоянно поднимают цены на нефть и вновь разжигают инфляционные ожидания.

Базовый сценарий Barclays предполагает, что средняя цена на нефть Brent в 2026 году достигнет 100 долларов, что на 50% выше средней цены 2025 года. Это напрямую ухудшит инфляционные перспективы, сократит пространство для снижения ставок центральными банками и даже может вынудить их повысить ставки. Более высокие ставки означают дальнейший рост расходов на обслуживание существующего долга, а рост процентных расходов, в свою очередь, усложняет сокращение дефицита. Это больше похоже на фискальный храповик: с каждым щелчком вперед у правительства остается меньше пространства для маневра, а компенсация, требуемая инвесторами в облигации, становится выше.

Прия Мисра, управляющий директор JPMorgan, прямо заявляет: «Если пролив не будет вновь открыт, диапазон ставок в целом сместился вверх».

Если смотреть на краткосрочные данные: доходность 2-летних американских казначейских облигаций в какой-то момент выросла до 4,09%, что является максимумом с февраля 2025 года; доходность 10-летних облигаций составила 4,58%, достигнув максимума за почти год; совокупная доходность американских гособлигаций с начала года стала отрицательной, тогда как в конце февраля годовая доходность приближалась к 2%.

Инфляционная повестка доминирует на рынках, премия за срок переоценивается

Судя по оценке Карен Манны, инвестиционного стратега и управляющего портфелем фиксированного дохода Federated Hermes: «Мы видим мир, который действительно сталкивается с новым витком инфляции».

Кевин Флэнаган, глава инвестиционной стратегии WisdomTree, ожидает, что следующий отчет об индексе потребительских цен может показать годовую инфляцию на уровне 4%, что станет наивысшим уровнем с 2023 года. Он прямо указывает на рыночную логику: «Инфляционная повестка доминирует на рынках, и рынок облигаций требует более высокой премии в качестве компенсации за владение вновь выпущенными гособлигациями».

Аукционы гособлигаций на прошлой неделе подтвердили такое ценообразование: ставка на аукционе 30-летних облигаций достигла 5%, что стало первым случаем с 2007 года, но спрос инвесторов был вялым; спрос инвесторов на аукционах 3-летних и 10-летних облигаций также был не очень активным. Даже то, что доходность долгосрочных облигаций выросла до максимумов с начала года, само по себе не является достаточным основанием для покупки долгосрочных инструментов.

Полный разворот пути ФРС: ставки меняются с двух снижений на повышение в марте

Инфляционная буря перекраивает ожидания относительно политики ФРС. Среда, с которой столкнется вступающий в должность председатель ФРС Кевин Варш, уже далеко не та «траектория смягчения», которую рисовал рынок в начале года.

Трейдеры в настоящее время считают повышение ставки в марте следующего года наиболее вероятным сценарием, вероятность повышения к декабрю составляет около трех четвертей; тогда как в конце февраля рынок все еще ожидал двух снижений ставки в 2026 году. Доходность американских казначейских облигаций в целом примерно на 50 базисных пунктов или выше уровня конца февраля.

Заявления официальных лиц еще больше укрепляют ястребиное ценообразование. Председатель Федерального резервного банка Чикаго Остан Гулдсби на прошлой неделе заявил, что широкомасштабное ценовое давление может даже указывать на перегрев экономики; член совета управляющих ФРС Майкл Барр назвал инфляцию «подавляющим» риском для экономики. В среду будут опубликованы протоколы апрельского заседания ФРС, и рынок пристально следит за тем, какую поддержку среди чиновников получили члены, голосовавшие против решения.

Последний опрос инвесторов в американские гособлигации, проведенный JPMorgan, показывает, что короткие позиции по казначейским облигациям достигли наивысшего уровня за 13 недель, а ставки на дальнейшее падение рынка облигаций явно усилились.

Система низких ставок Японии переоценивается

Доходность 30-летних японских гособлигаций на уровне 4% для США или Великобритании не является экстремальной, но для японского рынка она имеет иное значение. В течение последних 20 лет долгосрочные ставки в Японии были близки к нулю, и структура активов и пассивов пенсионных фондов, страховых компаний и местных банков строилась вокруг этой среды.

Ключевая ставка Банка Японии в настоящее время составляет 0,75%. На апрельском заседании по денежно-кредитной политике 3 из 9 членов совета выступили против текущей позиции; рыночное ценообразование показывает 77%-ную вероятность повышения ставки в июне. Даже если Банк Японии поднимет ставку до 1%, реальные ставки все равно будут заметно отрицательными.

Рост доходности долгосрочных японских облигаций можно объяснить нормализацией денежно-кредитной политики: конец дефляции, рост реальной заработной платы, возвращение экономики к более нормальному состоянию. Но проблема в том, что нормализация ставок в экономике с размером долга, превышающим двукратный объем ВВП, может оказаться не такой уж мягкой. 4% по 30-летним японским облигациям — это не просто изменение цифры доходности, а переоценка всей финансовой системы низких ставок.

Великобритания, Франция: политическая структура делает сокращение дефицита почти невозможным

Правительство лейбористов Великобритании имеет рабочее большинство более чем в 150 мест в парламенте из 650, теоретически обладая возможностью для фискальной корректировки. Но прошлым летом экономия всего в 1,4 млрд фунтов стерлингов, связанная с субсидиями на зимнее топливо, вызвала бунт среди парламентской фракции лейбористов.

Политическое давление нарастает. 97 депутатов от лейбористов требуют отставки премьер-министра или установления сроков ухода; главный претендент Энди Бёрнем ранее выступал за то, чтобы фискальная политика не подчинялась рынку облигаций, а затем уточнил, что не будет полностью игнорировать инвесторов. За последние четыре года в Великобритании сменились четыре премьер-министра и пять министров финансов. Рыночное ценообразование по облигациям показывает, что к концу года у Банка Англии все еще есть пространство для повышения ставки более чем на 60 базисных пунктов, хотя председатель Бэйли, возможно, предпочел бы выжидательную позицию.

Проблемы Франции не так заметны, как с британскими гособлигациями, но фискальная структура同样棘手. За менее чем три года Франция сменила пять премьер-министров. Нынешнее правительство, чтобы продвинуть бюджет с целевым уровнем дефицита в 5% ВВП, уже пережило два вотума недоверия. Реформа 2023 года о повышении пенсионного возраста до 64 лет подвергается атакам, хотя 64 года все еще ниже, чем в большинстве западных экономик. Дефицит Франции уже заметно превышает темпы роста номинального ВВП, избиратели будут сурово наказывать за попытки ужесточения, а конституционные нормы также облегчают парламенту блокирование сокращения расходов. Все знают, что дефицит должен снижаться, но никто не хочет нести политическую цену за его снижение.

Структура покупателей в США изменилась: иностранные центральные банки переключаются на золото, частные инвесторы требуют более высокой цены

Превышение доходности 30-летних американских казначейских облигаций уровня 5% произошло впервые с 2007 года. Прямой причиной является рост инфляции, фискальное расширение, высокий дефицит, но это не новость. Более глубокое изменение заключается в том, что меняются маржинальные покупатели.

Федеральный дефицит США составляет около 2 трлн долларов. Бюджетно-контрольное управление Конгресса прогнозирует, что доля федерального долга, находящегося в руках общественности, вырастет с нынешних более 100% ВВП до 120% к 2036 году. Но этот прогноз может все еще быть оптимистичным. Ключевой переменной являются таможенные доходы: эффективная тарифная ставка США снизилась с пика в 12% до 7-8%, что ниже предполагаемых Бюджетно-контрольным управлением 15%. Даже если в конечном итоге она вырастет до 10%, таможенные доходы за следующее десятилетие составят лишь около 60% от предполагаемого размера сокращения дефицита в 3 трлн долларов. Предположения относительно оборонных расходов и стоимости обслуживания долга также могут быть занижены.

Статус доллара как резервной валюты остается структурным преимуществом США, позволяя им финансироваться под ставки, недоступные для стран с аналогичным уровнем долга. Но это не означает, что дефицит в 6,5% является устойчивым. Иностранные центральные банки раньше были стабильными покупателями долгосрочных активов, но после замораживания Западом резервов России центробанки переключились на золото. В прошлом году доля золота в резервах центробанков превысила долю американских гособлигаций. Япония как крупнейший держатель американских гособлигаций теперь находит ставки на внутреннем рынке более привлекательными. ФРС все еще находится в режиме сокращения баланса. Покупателями долгосрочных облигаций становятся частные инвесторы, более чувствительные к цене и требующие более высокой премии за срок.

ФРС не является «предохранителем» для долгосрочных облигаций

Органы управления долгом за последние годы уже относительно сократили выпуск долгосрочных облигаций и в будущем могут продолжить корректировать структуру выпуска, но это может лишь смягчить давление со стороны предложения, а не изменить фискальное и инфляционное направление.

На рынке обсуждается вопрос, будет ли ФРС вынуждена возобновить масштабные покупки активов, чтобы предотвратить дальнейший рост долгосрочных ставок. Но ранее Варш высказывался о балансе ФРС следующим образом: «Раздутый баланс может быть значительно сокращен» — это не формулировка, готовящая введение американского контроля кривой доходности.

Столкнувшись с продолжающимися распродажами, некоторые инвесторы предпочитают оставаться в стороне. Аналитик WisdomTree Кевин Флэнаган заявляет, что в настоящее время придерживается плавающих векселей и сохраняет низкую подверженность процентным ставкам: «Лучше купить позже, чем слишком рано». Он считает, что уровень доходности 10-летних облигаций в 4,5% «скорее является психологическим барьером», и если ситуация на Ближнем Востоке вновь обострится, подняв цены на нефть, доходность может вновь протестировать прошлогодний максимум в 4,62%. Хэнк Смит, глава инвестиционной стратегии Haverford Trust, придерживается более осторожной позиции. Он заявляет, что остается открытым вопрос: является ли рост потребительских и производительских цен временным «или он продолжится до 2027 года».

Силы, движущие распродажами, — ухудшение фискальной ситуации, увеличение оборонных расходов, устойчивость инфляции, ограниченность центробанков — никуда не исчезнут в течение одной-двух недель. Пока экономические данные не покажут явного ослабления или не появятся достоверные изменения в фискальной траектории, долгосрочные облигации развитых стран все еще торгуются вокруг одной и той же проблемы: модель финансирования по низким ставкам в эпоху высокого долга переоценивается рынком.