Источник: DeFi Report

Автор: Michael Nadeau

Компиляция и редактирование: BitpushNews

Оглядываясь на 2021 год, розничные транзакции составляли 88% от общего дохода Coinbase. К прошлому году (2025) эта доля снизилась до 48% по мере диверсификации компании в области подписок, услуг и институциональной инфраструктуры.

В этой статье анализируется текущая трансформация Coinbase и то, что это означает для её прибыльности, конкурентного положения и долгосрочной оценки.

Давайте начнём.

Финансовые показатели за 2021 – 2025 годы

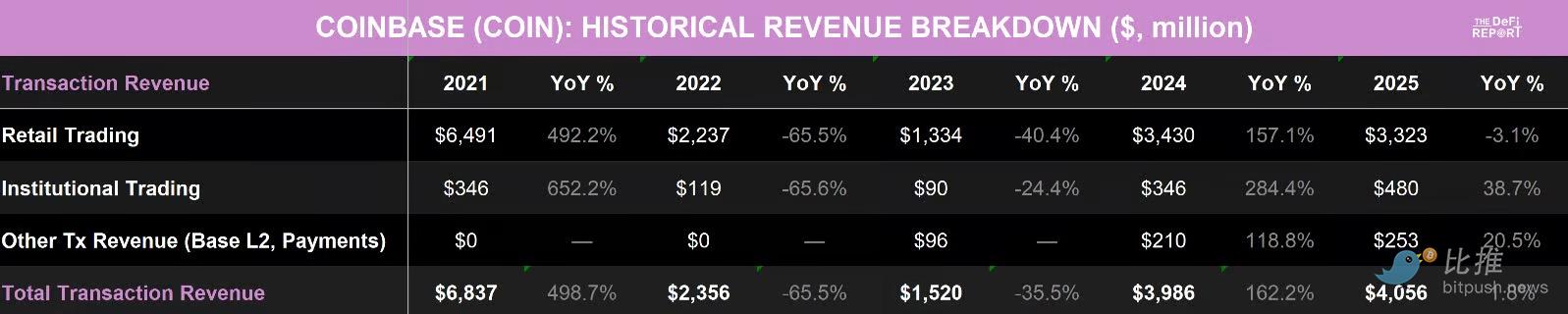

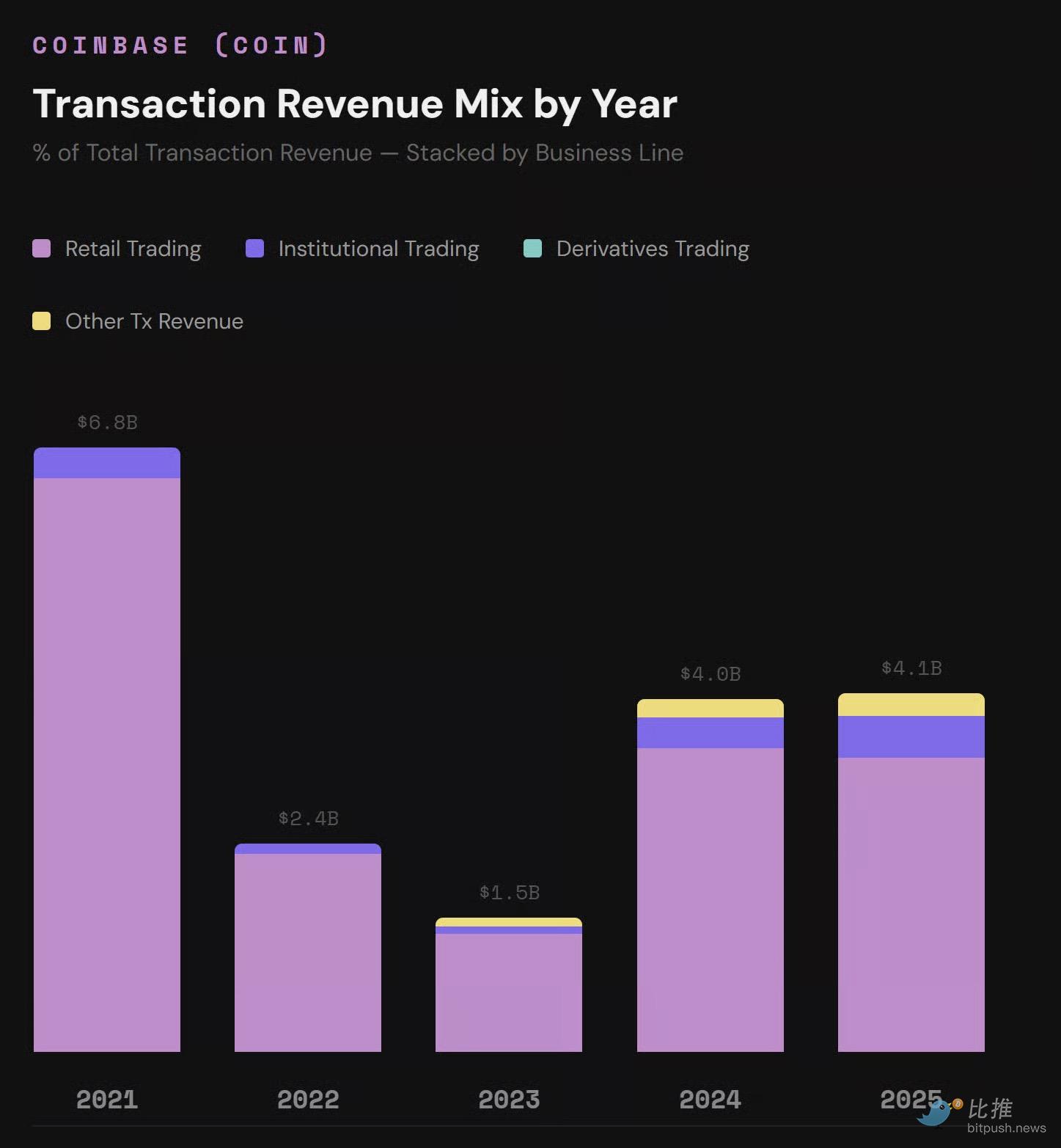

Доход от транзакций

Визуализация структуры дохода:

(На основе данных Coinbase 10k и SEC)

Ключевые выводы по доходу от транзакций:

-

Доминирование розничных операций медленно ослабевает: В 2021 году розничные транзакции составляли 95% дохода от транзакций и 88% общего дохода. К 2025 году эти доли снизились до 82% дохода от транзакций и 48% общего дохода соответственно.

-

Доля институциональных транзакций растёт: В 2025 году институциональные транзакции составили 12% общего дохода от транзакций по сравнению с 5% в 2021 году.

-

Прочий доход от транзакций: В настоящее время составляет 6.2% общего дохода от транзакций. Это в основном доход от сборов секвенсора L2 Base и платёжных поступлений — совершенно новая статья, которой не существовало до 2023 года.

-

Более устойчивая структура дохода: Когда в 2022 году объёмы розничных транзакций замедлились, Coinbase почти лишилась всего дохода. Сегодня доход поддерживается тремя направлениями, а не одним источником, что помогает сглаживать циклические колебания дохода в периоды медвежьего рынка.

-

Пик ещё не достигнут: Несмотря на прогресс, доход от транзакций всё ещё не вернулся к уровню 2021 года. Фактически, в 2025 году доход от транзакций снизился на 40% по сравнению с 2021 годом (в основном из-за падения розничного торгового дохода на 48%).

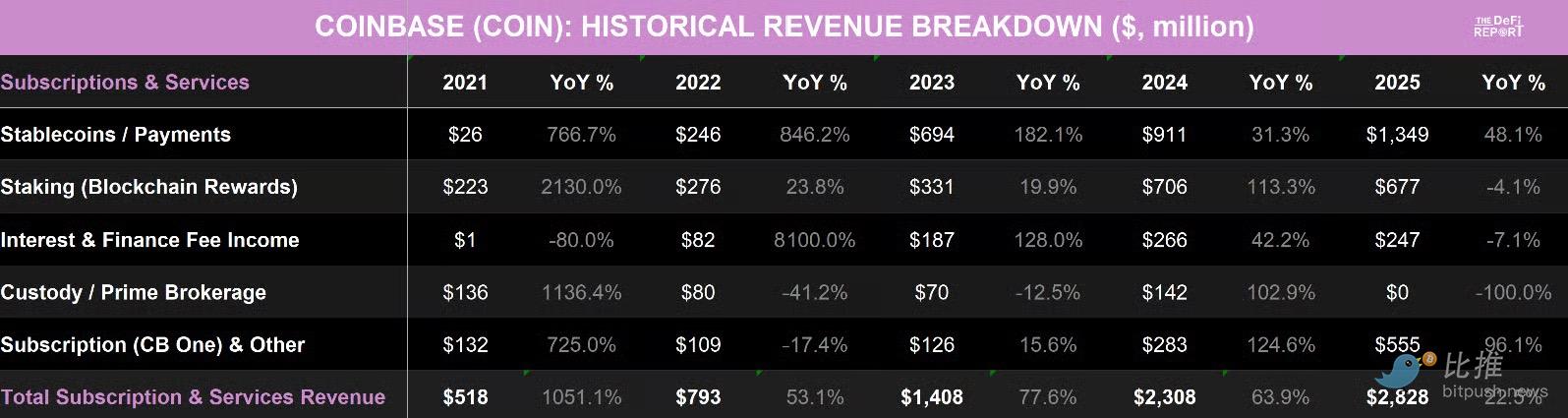

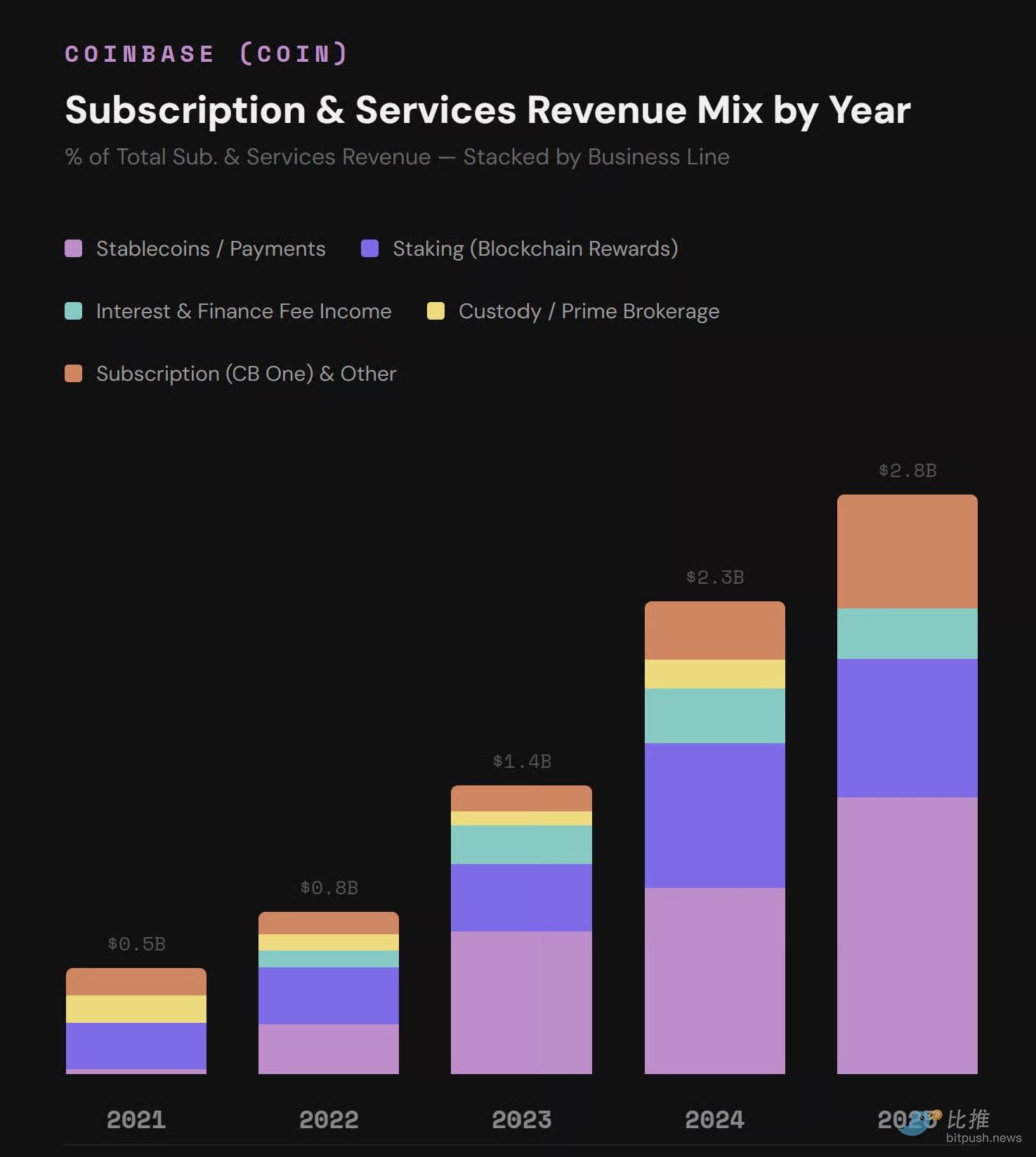

Доход от подписок и услуг

Визуализация структуры дохода:

(На основе данных Coinbase 10k и SEC)

Ключевые выводы по доходу от подписок и услуг:

-

Общий сильный рост: Этот сегмент вырос в 5.5 раз за последние 4 года, при среднегодовом темпе роста (CAGR) 53%. Что наиболее примечательно, даже во время медвежьего рынка 2022 года этот бизнес рос каждый год.

-

Стейблкоины стали основой: Стейблкоины стали крупнейшим единым источником дохода в этом сегменте, выросшим до 1.35 миллиарда долларов в 2025 году (в 52 раза по сравнению с 2021 годом) и составившим 19% от общего дохода за 2025 год. Этот доход получен благодаря партнёрству с Circle (USDC): Coinbase получает 100% всего дохода USDC, генерируемого на её платформе (биржа, Prime для институциональных услуг, кастодиальные услуги), и 50% всех оставшихся доходов от резервов USDC вне платформы (другие биржи, DeFi, кошельки и т.д.). Фактически, Coinbase получает по этому соглашению больше дохода, чем половина дохода Circle.

-

Стейкинг (Staking): Доход достиг пика в 706 миллионов долларов в 2024 году и снизился на 4% в 2025 году. Мы считаем, что это в основном связано с ростом DeFi и значительным снижением вознаграждений за стейкинг ETH.

-

Доход от подписок (Coinbase One): В 2025 году вырос на 96%, составив 7.7% общего дохода. Coinbase One в настоящее время насчитывает более 1 миллиона подписчиков и генерирует регулярный доход, подобный SaaS. Обратите внимание, что с 2025 года доход от кастодиальных сборов был объединён с этой статьёй.

-

Доля в доходе: Подписки и услуги в настоящее время составляют 41% общего дохода. Эти доходы носят регулярный характер, менее волатильны и постоянно растут, что хорошо компенсирует снижающийся и волатильный доход от розничных транзакций.

В целом: Общий доход Coinbase в 2025 году вырос на 9.4%, но всё ещё на 6.4% ниже пикового значения 2021 года.

Операционные расходы за 2021 – 2025 годы

Источник данных: Coinbase 10k, документы SECВизуализация структуры расходов:

(На основе данных Coinbase 10k и SEC)

Ключевые выводы по операционным расходам:

-

Были на грани банкротства: В 2022 году операционные расходы Coinbase составили 5.9 миллиарда долларов, в то время как выручка была всего 3.2 миллиарда долларов. В то время компания сжигала деньги с угрожающей скоростью, только на технологии и разработку было потрачено 2.3 миллиарда долларов, а на общие и административные расходы (G&A) — 1.6 миллиарда долларов.

-

Структурная перестройка: Это было исправлено в 2023 году. Путем реструктуризации рабочей силы (сокращение 950 человек), оптимизации процесса найма и перефокусировки на основных продуктах компания сократила операционные расходы на 45%.

-

Проявился операционный рычаг: Хотя текущие операционные расходы вернулись к уровню 2022 года, бизнес стал вдвое больше, чем тогда, и успешно превратил операционный дефицит в операционный рычаг. В 2025 году операционная рентабельность Coinbase составила 21%.

-

Распределение расходов: 17.7% расходов связаны с транзакциями (переменные затраты, изменяющиеся с масштабом бизнеса); 18.4% идут на продажи и маркетинг (эта статья продолжает расти, в основном用于USDC вознаграждения, спонсорство NBA и привлечение клиентов Coinbase One).

-

Управление и R&D: Оставшиеся 57.3% приходятся на технологии и разработку (рост на 13.8% в 2025 году) и общие и административные расходы (рост на 24.6%). Учитывая, что выручка в 2026 году, вероятно, снизится, мы считаем, что Coinbase может снова сократить штат, чтобы снизить фиксированные затраты в период медвежьего рынка.

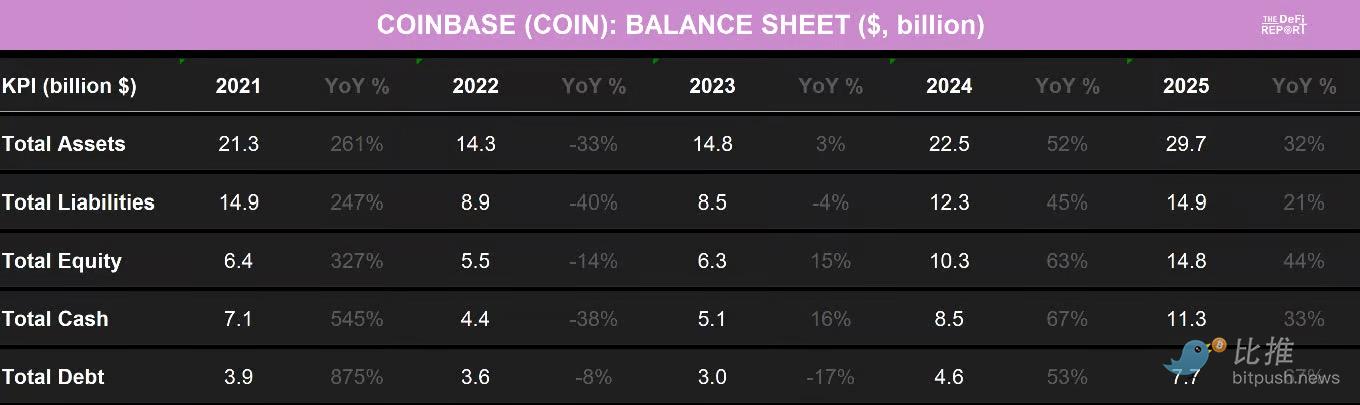

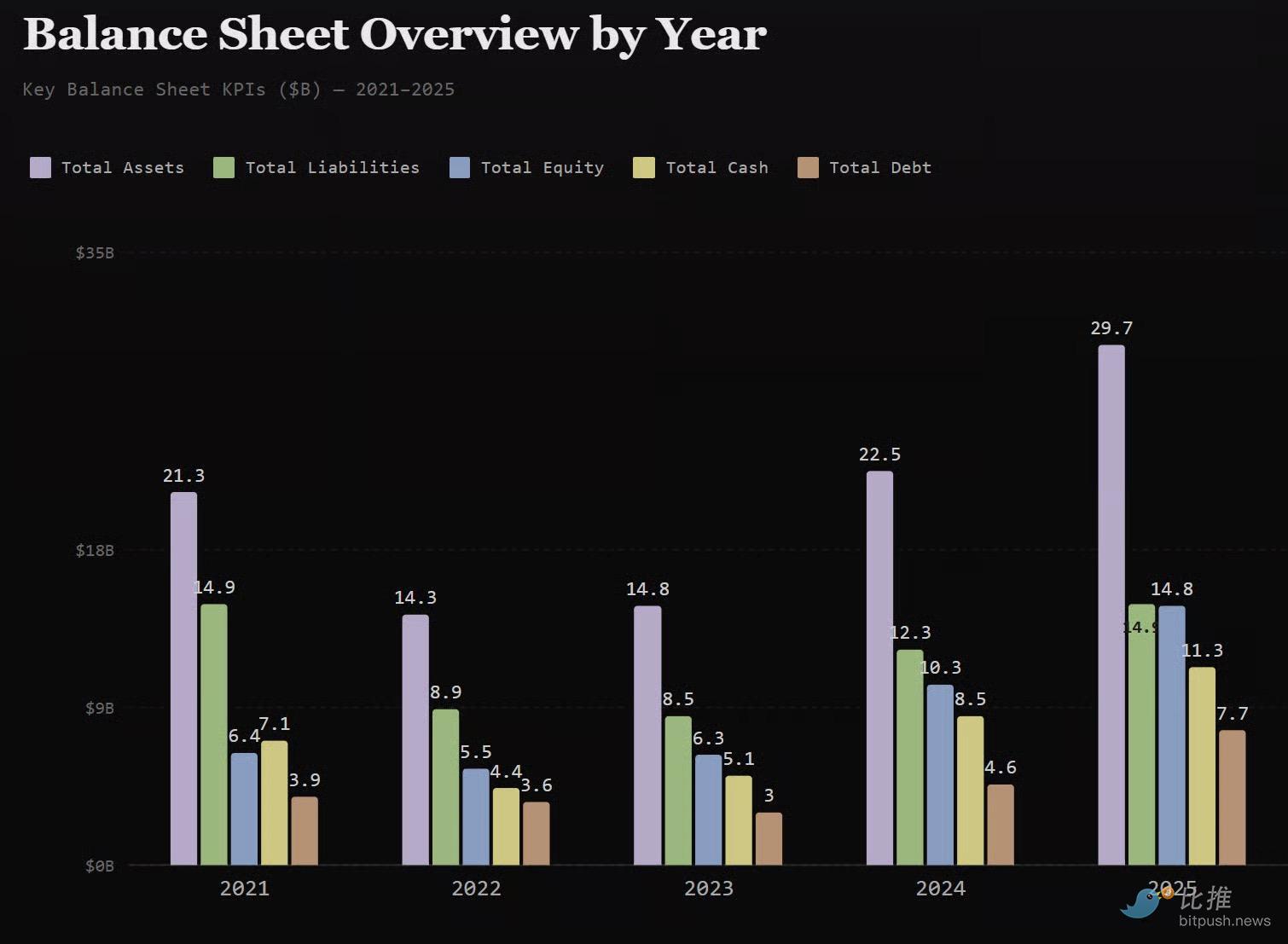

Баланс за 2021 – 2025 годы

Визуализация баланса:

(На основе данных Coinbase 10k и SEC)

Ключевые выводы:

-

Долговые обязательства: Долг на сумму 1.27 миллиарда долларов подлежит погашению в июне этого года. Из общего долга в 7.7 миллиарда долларов около 40% составляют конвертируемые облигации с процентной ставкой 0%; ещё 1.26 миллиарда долларов подлежат погашению в 2030 году с процентной ставкой всего 0.25%. Текущие годовые денежные процентные расходы по существующему долгу составляют около 65 миллионов долларов (совокупная ставка ниже 1%). Для сравнения, только в 2025 году Coinbase получила 297 миллионов долларов процентного и прочего дохода, что в 4.5 раза превышает процентные расходы.

-

Структура обязательств: Из общих обязательств в 7.2 миллиарда долларов 6.2 миллиарда долларов составляют «сквозные статьи», которые хеджируются активами на другой стороне баланса (обязательства по кастодиальным средствам клиентов и обязательства по возврату обеспечения). Оставшиеся 1.0 миллиард долларов — это краткосрочные обязательства, связанные с кредиторской задолженностью и операционной деятельностью.

-

Структура активов: Помимо денежных средств (исторический максимум), Coinbase имеет гудвил в размере 4.2 миллиарда долларов, связанный с приобретением Deribit, 2.0 миллиарда долларов криптоактивов (BTC и ETH), 623 миллиона долларов стратегических инвестиций (включая долю в Circle) и 310 миллионов долларов в торгуемых инвестициях. Ещё 3.3 миллиарда долларов составляют операционные активы (дебиторская задолженность, займы, оборудование).

-

Значительные изменения: Наиболее заметное изменение в 2025 году произошло в результате приобретения Deribit (ведущей биржи деривативов). Гудвил вырос с 1.1 миллиарда долларов до 4.2 миллиарда долларов, а нематериальные активы в результате этой сделки увеличились с 47 миллионов долларов до 1.4 миллиарда долларов.

Общая оценка: Баланс Coinbase находится в самом здоровом состоянии за всю историю. Чистая денежная позиция в размере 3.6 миллиарда долларов (без учёта 2.9 миллиарда долларов криптоактивов и стратегических активов) означает, что у неё достаточно возможностей, чтобы пережить трудные времена, совершать стратегические приобретения и инвестировать в новые продуктовые линейки. Кроме того, её долговая структура чрезвычайно дёшева.

Конкурентная среда

COIN vs HOOD

Говоря о конкуренции для Coinbase, мы фокусируемся на Robinhood. Обе компании управляются основателями, были созданы примерно в одно время (Coinbase в 2012 году, Robinhood в 2013 году), обслуживают поколения миллениалов и Zетов и строят финансовые рельсы на основе криптографии.

Мы считаем, что у обеих компаний есть возможность достичь оценки в 1 триллион долларов и стать ведущими финансовыми институтами будущего.

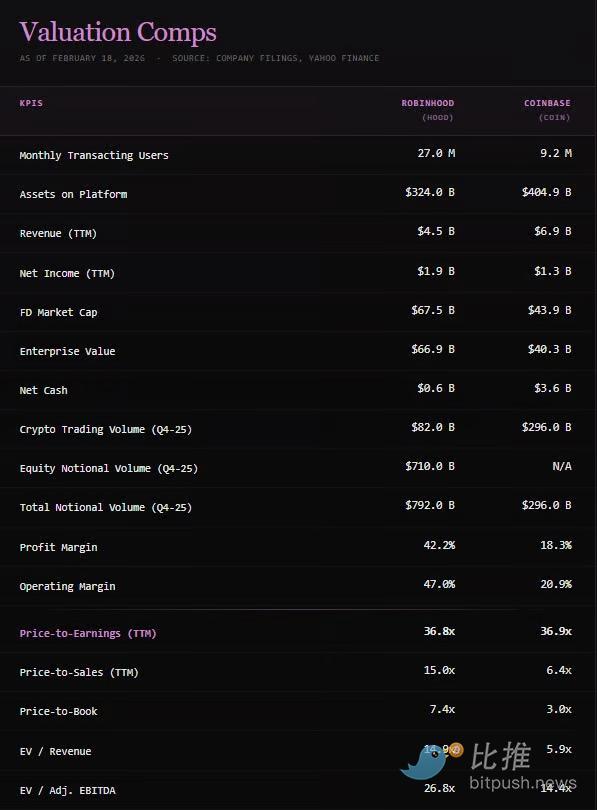

Сравнение оценки с HOOD

Источник данных: Coinbase 10k, документы SEC

Ключевые выводы:

-

Расхождение в оценке: Хотя скользящее P/E (цена/прибыль) обеих компаний почти одинаково и составляет 37x, во почти всех других показателях COIN оценивается лишь в половину от HOOD. Это говорит о том, что рынок более оптимистично оценивает качество прибыли и траекторию роста Robinhood по сравнению с Coinbase.

-

Причина в рентабельности: Операционная рентабельность Robinhood в 47% и чистая рентабельность в 42% более чем вдвое превышают показатели Coinbase (21% и 18% соответственно). Это привело к тому, что при выручке на 35% меньше, операционная прибыль Robinhood反而 на 45% выше (2.09 миллиарда против 1.44 миллиарда).

-

Два момента, требующих внимания:

-

Операционные расходы Coinbase за 2025 год включают 345 миллионов долларов на утечку данных и затраты на интеграцию Deribit, которые являются разовыми расходами.

-

Robinhood имеет лучший контроль над затратами и более стройные операции. Мы считаем, что это связано с фокусом: Robinhood фокусируется на розничных клиентах, в то время как Coinbase пытается охватить как институциональные, так и розничные сегменты, что приводит к слишком широкой продуктовой линейке и более высоким операционным затратам.

Денежный поток: Coinbase имеет 11.3 миллиарда долларов денежных средств (почти в три раза больше, чем 4.3 миллиарда у Robinhood), а вместе с криптоактивами и стратегическими инвестициями — 14.1 миллиарда долларов доступных ресурсов, что обеспечивает более сильный буфер для выживания.

Характер долга: Подавляющая часть долга Robinhood (11.8 миллиарда) — это операционный брокерский долг (хеджирование securities lending и т.д.), её долгосрочных корпоративных облигаций почти нет. У Coinbase же есть 7.7 миллиарда долларов корпоративного долга, но с очень низкими процентными ставками.

Выкуп акций и продажа инсайдерами: Robinhood агрессивно выкупает акции с Q3 2024 года (выкуплено 910 миллионов долларов). Coinbase начала выкуп в 2025 году (408 миллионов долларов) и заявила, что будет искать возможности в период медвежьего рынка. В то же время продажа акций CEO Брайаном Армстронгом вызвала негативное внимание (продано примерно на 550 миллионов долларов с апреля 2025 по январь 2026). Хотя это выглядит плохо, мы считаем, что рынок среагировал чрезмерно, поскольку это часть обычного запланированного плана продаж руководителей и составляет лишь 3.3% его доли.

Факторы риска

-

Усиление конкуренции: Традиционные брокеры (Schwab, Fidelity) расширяют криптовалютные услуги; Binance по-прежнему велик на международных рынках; BlackRock и Fidelity строят конкурирующую инфраструктуру для институциональных клиентов.

-

Регулирование: Coinbase играет роль в переговорах по Clarity Act. Если новые правила будут благоприятствовать традиционным институтам, это серьёзно ударит по нативным крипто-сервисам.

-

Цикличность: Несмотря на диверсификацию дохода, 59% дохода по-прежнему напрямую связаны с ценами на криптовалюты и рыночными настроениями.

-

Процентный риск: Стейблкоины составляют 19% общего дохода. Если ФРС значительно снизит ставки, это напрямую повлияет на этот доход. Coinbase уже предупредила в руководстве на Q1 2026 года, что доход может снизиться на 100–150 миллионов долларов из-за этого.

-

Риск безопасности: Утечка данных в мае 2025 года обошлась в 345 миллионов долларов и нанесла ущерб репутации.

-

Риск концентрации с Circle: Часто недооцениваемый риск заключается в том, что закон GENIUS может сделать их партнёрство незаконным. Юридический вопрос: является ли Coinbase, как кастодиан USDC пользователей, «держателем», которому закон запрещает выплачивать проценты. Хотя мы считаем, что нет, инвесторам следует следить за этим.

Заключение

Несмотря на сложный четвёртый квартал, базовая бизнес-структура Coinbase сильнее, чем в любом предыдущем цикле. Компания имеет резерв денежных средств в размере 11.3 миллиарда долларов, базу дохода от подписок и услуг в 2.8 миллиарда долларов (41% от общего дохода) и лидирующие позиции в области институционального кастодиана и инфраструктуры стейблкоинов.

В настоящее время COIN оценивается примерно в половину от Robinhood по показателям P/S (цена/выручка), P/B (цена/балансовая стоимость) и EV/EBITDA. Учитывая её более сильный баланс, мы считаем, что для инвесторов, уверенных в долгосрочном росте рынков крипто-капитала, COIN предлагает очень привлекательное соотношение риска и доходности.

Мы вышли из большей части наших позиций в COIN в третьем/четвёртом квартале прошлого года (с прибылью 270%), но до сих пор держим позицию со средней ценой входа 99.58 доллара и ищем возможности для увеличения доли.

Twitter:https://twitter.com/BitpushNewsCN

Группа в TG比推:https://t.me/BitPushCommunity

Подписка в TG比推: https://t.me/bitpush