Автор: 0xBrooker

Снижение ставок ФРС и высвобождение ликвидности подняли дно цены BTC на этой неделе; отчеты AI-акций технологического сектора, не соответствующие ожиданиям, продолжили сжимать оценку высокобетативных активов, ограничивая восходящее пространство BTC. В итоге BTC после тестирования максимумов прошлой недели продолжил сохранять среднесрочную тенденцию «поиска дна».

ETH, который упал сильнее ранее, также отскочил более энергично, но в конечном итоге также отступил вместе с общей тенденцией.

Под воздействием снижения ставок и некоторого улучшения краткосрочной ликвидности, оба актива на этой неделе пытались пробить нисходящую линию тренда, но в конечном итоге безуспешно, вновь откатившись внутрь к верхней границе нисходящего тренда.

В целом BTC сохранял синхронность роста и падения с Nasdaq, ожидая публикации данных по CPI и занятости за ноябрь на следующей неделе, чтобы предоставить ориентиры для рынка, испытывающего недостаток точек для торговли, а также готовясь к воздействию повышения ставок в Японии на следующей неделе.

Политика, макрофинансы и экономические данные

Пережившее катящиеся как американские горки и нанесшее удар по росту BTC ноябрьское заседание ФРС по установлению ставок, как и ожидалось, снизило ставки на 25 базисных пунктов до 3,50%~3,75%. В заявлении ФРС подчеркивалось: в «взвешивании рисков двойного мандата» риски снижения на стороне занятости возросли, в то время как инфляция «все еще немного завышена»; последующие шаги будут зависеть от данных, перспектив и баланса рисков для определения «объема и времени дальнейших корректировок». Это означает, что в рамках двойного мандата ФРС в настоящее время немного сместилась в сторону занятости.

Это несколько более голубиное заявление было разбавлено внутренним разногласием в ФРС — 9/12 «за», 3 «против» (1 выступал за снижение на 50 б.п.; 2主张主张ли за сохранение ставок).

Точечный график на 2026~2028 годы明显 более рассредоточен, что говорит о不一致ности в взвешивании «вязкости инфляции vs замедления занятости»; точки справа «Longer run» сконцентрированы около 3% и slightly выше, указывая на политическое значение potentially более высокой долгосрочной нейтральной ставки по сравнению с допандемийным периодом. Это снизило ожидаемый объем снижения ставок в 2026 году до 1-2 раз, всего на 50 б.п. Это нейтральный ориентир, который может somewhat помочь занятости, но в current состоянии недостаточен для поддержки высокобетативных активов.

В ответ на напряженность краткосрочной ликвидности ФРС возобновила покупку краткосрочных казначейских облигаций, на пресс-конференции объяснив, что для поддержания «достаточных резервов» будет проводиться RMP, в первый месяц около $40 млрд, и подчеркнув, что RMP не означает изменения monetary policy stance. Первая покупка уже завершена.

После более чем месяца снижения оценок, представители высокобетативных активов — AI-акции — не стабилизировались. Отчеты Oracle и Broadcom, опубликованные на этой неделе, вновь ударили по доверию рынка.

После роста акций в Q3 на фоне expansion расходов, рынок сейчас больше关注ит проблемы долга AI-акций и whether высокие инвестиции быстро принесут рост прибыли. Публикация отчетов двух компаний нанесла «двойной удар», рынок начал переоценивать «цикл окупаемости AI», что привело к тому, что весовые AI-акции потянули вниз appetite к риску Nasdaq и общего рынка. Nvidia и BTC потеряли gains от отскока, вернувшись к исходной точке недели.

Доходность 10-летних казначейских облигаций США сохраняется на уровне около 4.18%, оказывая давление на активы с высокой дюрацией.

Хотя ФРС начала покупки облигаций, счет Казначейства TGA также начал снижаться due to расходов, SOFR вернулся внутрь диапазона联邦ной ставки, краткосрочная ликвидность постепенно выходит из состояния напряженности, но все еще не изобильна. На фоне сомнений в долге AI-акций и окупаемости прибыли, есть признаки перетока средств на美股 в потребительские и циклические акции. Индексы Dow Jones и Russell 2000均 на этой неделе обновили исторические максимумы.

На фоне неясности снижения ставок в 2026 году, в叠加 с тем, что новый председатель ФРС еще не утвержден, высокобетативные активы, включая AI-акции и BTC, все еще не пользуются青睐нием资金. Самый оптимистичный прогноз заключается в том, что рынок, возможно, откроет «рождественское ралли» только после повышения ставок в Японии на следующей неделе и публикации данных по занятости и инфляции в США.

Крипторынок

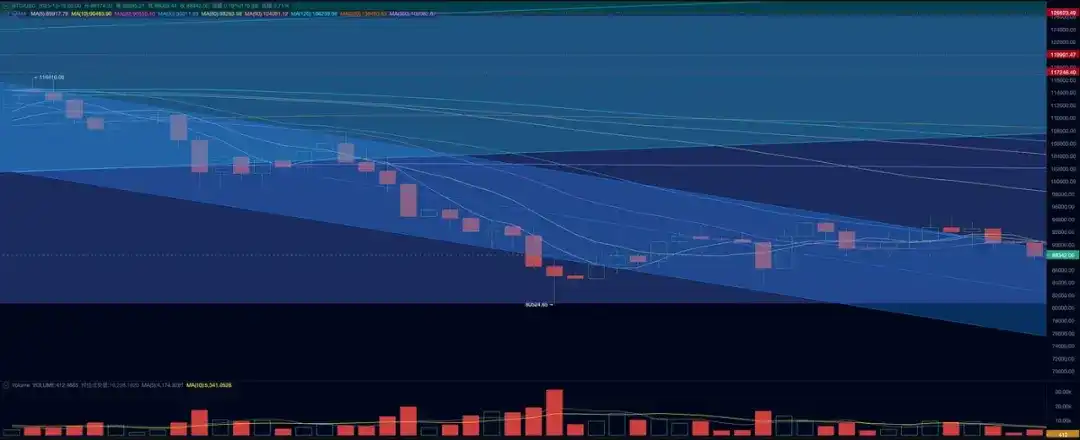

На этой неделе BTC открылся на отметке $90402.30, закрылся на $88171.61, снизившись на 2.47%, с амплитудой 7.83%, объем торгов slightly сократился. Технически, BTC一度 пробил нисходящий канал до снижения ставок, но затем, под ударом отчетов AI-акций, полностью отыграл обратно.

График цены BTC (дневной)

В настоящее время BTC все еще находится на стадии консолидации после резкого падения, и то, пойдет ли он дальше вверх вместе с美股 в «новом цикле», или после консолидации вновь рухнет и продолжит падение, закрепив «старый цикл», все еще зависит от叠加内外因素 и реакции различных сторон рынка.

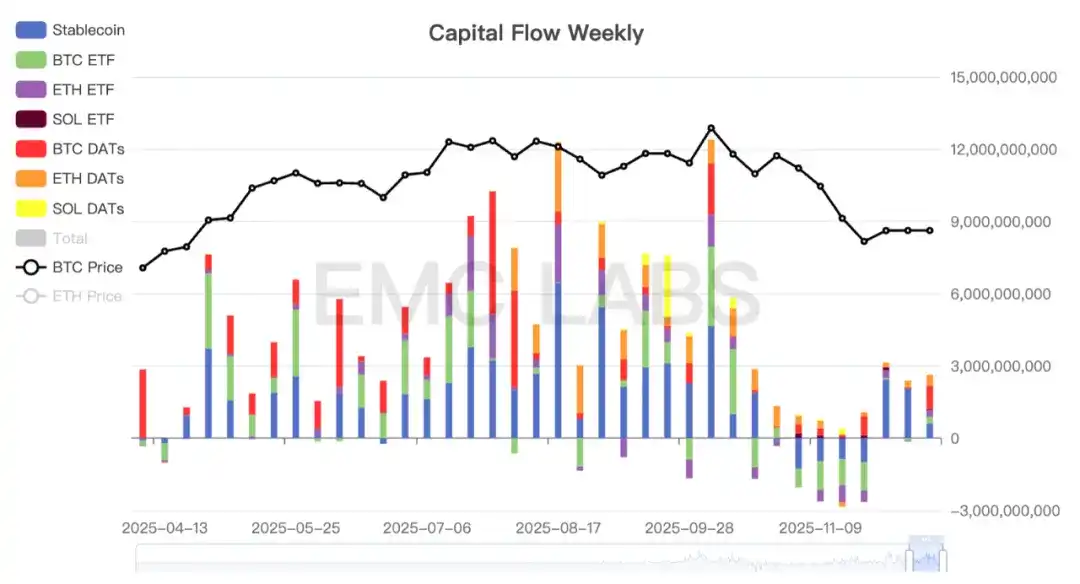

С точки зрения资金, ситуация相对 оптимистична. По имеющимся данным, приток средств на этой неделе не significantly изменился, но на прошлой неделе Strategy провела дополнительную покупку BTC на сумму超过 $900 млн, Bitmine также значительно увеличила долю ETH, что, несомненно, значительно подстегнуло доверие рынка.

Статистика притока и оттока средств на крипторынке (неделя)

Среди них, каналы BTC ETF и ETH ETF, обладающие значительной定价权 на加密资产, также зафиксировали чистый приток, в сумме超过 $500 млн.

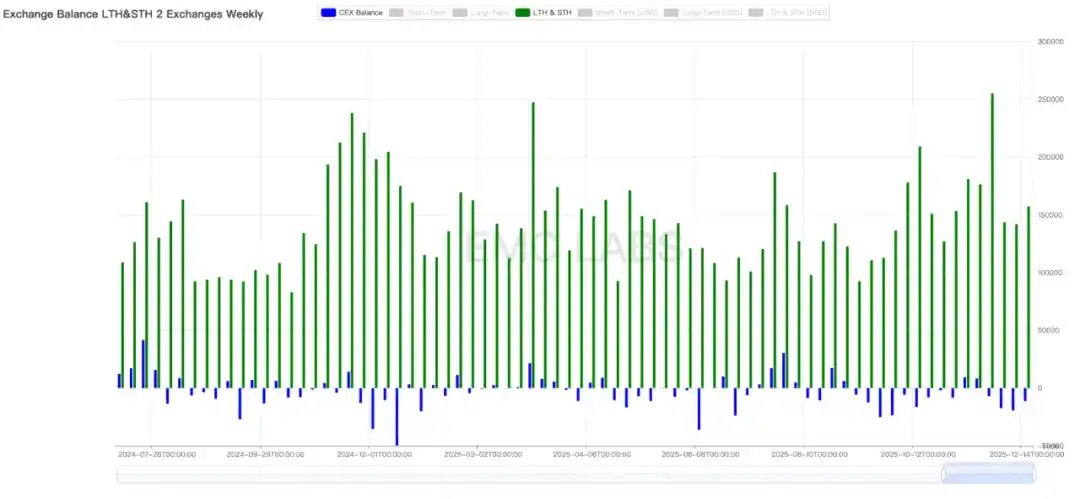

С точки зрения продаж, ситуация稍微 пессимистична. На прошлой неделе длинные и короткие руки в сумме продали超过 157k монет, что超过 масштабы двух предыдущих недель. И с ростом продаж, масштабы outflow с бирж также slightly снизились.

Статистика продаж и inflow/outflow на биржах (неделя)

И группа длинных рук продолжает продавать. Историческое проклятие циклов все еще глубоко влияет на эту группу. Если они не вернутся к状态 накопления, цена BTC вряд ли стабилизируется.

На отраслевом уровне также есть позитивное推进. CFTC объявило о запуске пилотной программы для цифровых активов, разрешающей регулируемым衍бычным рынкам использовать BTC, ETH и USDC в качестве collateral, с配套 более строгих механизмов мониторинга и отчетности. Прорыв加密资产 в качестве гарантий для сценарных производных инструментов способствует слиянию DeFi и CeFi, увеличивает应用场景 Crypto, что является долгосрочным позитивом для Crypto. Кроме того,备受瞩目的 «структурное предложение» также, по сообщениям СМИ, добилось определенного推进, и получило поддержку как Democrats, так и Republicans. Окончательное принятие этого законопроекта будет способствовать дальнейшему развитию加密产业 в США и подтолкнет институциональные организации к дальнейшей allocation加密资产.

Циклические индикаторы

Согласно eMerge Engine, индикатор EMC BTC Cycle Metrics составляет 0, войдя в «нисходящую фазу» (медвежий рынок).