Автор: Zhou, ChainCatcher

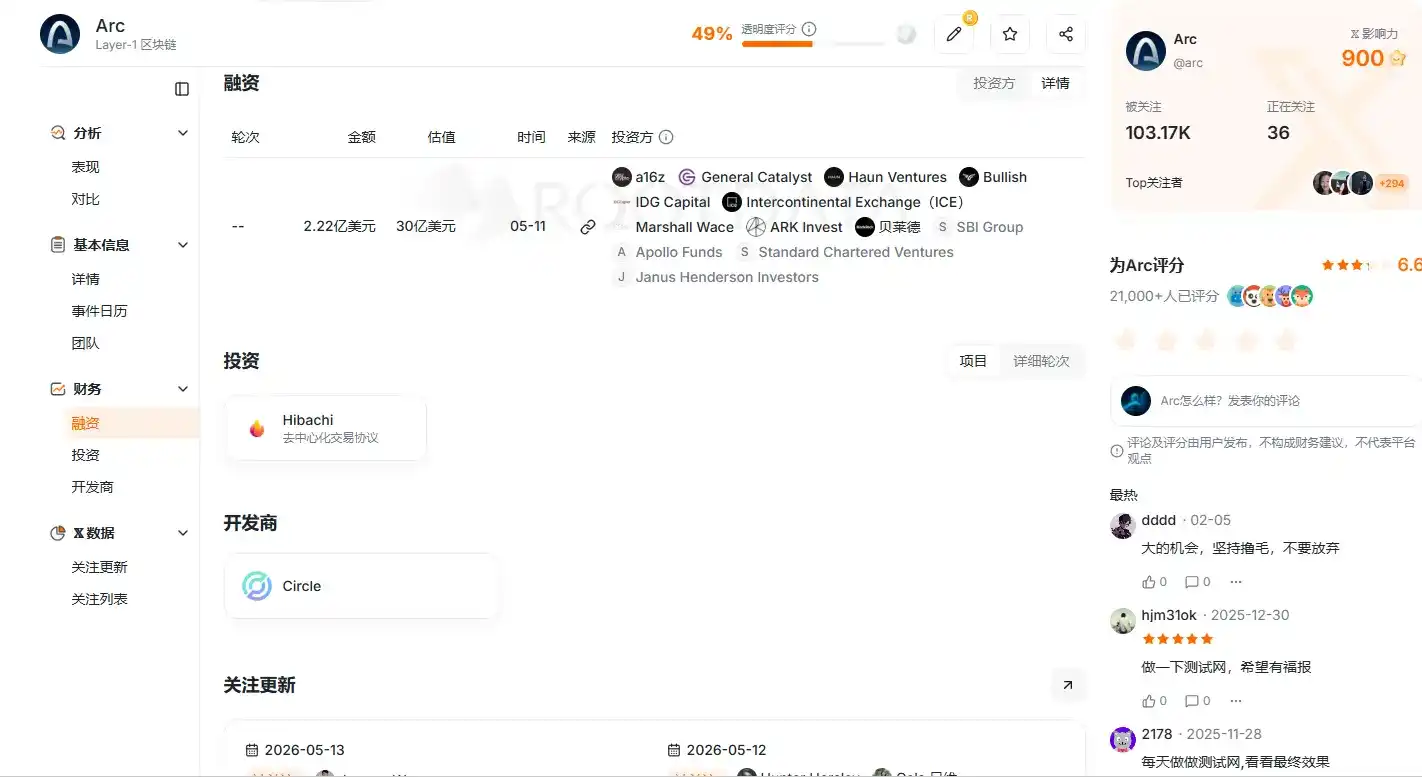

11 мая Circle одновременно с публикацией отчетности за первый квартал 2026 года объявила о завершении предпродажи нативного токена ARC для своей публичной блокчейн-сети Arc на сумму 222 миллиона долларов. Полностью разводненная стоимость сети оценивается в 3 миллиарда долларов.

В раунде ведущим инвестором выступила a16z crypto с инвестицией в 75 миллионов долларов, последовали другие ведущие институты, такие как BlackRock, Apollo, материнская компания Нью-Йоркской фондовой биржи ICE, SBI Group, Standard Chartered Ventures, ARK Invest и другие.

Акции CRCL в тот же день выросли почти на 16%, а рыночная капитализация вернулась к уровню выше 30 миллиардов долларов.

Источник изображения:RootData

В связи с этим на рынке возникает ключевой вопрос: Circle уже является публичной компанией, если верить в ее будущее, можно просто держать акции CRCL, зачем же выпускать токен ARC? Оба инструмента захватывают стоимость сети Arc, но что же стоит за каждым из них?

I. Почему Circle строит Arc самостоятельно

Почему Circle не продолжает выпускать и использовать USDC на Ethereum или Solana, а тратит огромные ресурсы на создание собственного публичного блокчейна?

a16z Crypto объясняет это так: по мере того, как глобальные финансы постепенно переходят на блокчейн, в будущем лишь немногие публичные блокчейны смогут выступить в качестве "основы для экономической системы в сети".

Объем транзакций стейблкоинов в прошлом году приблизился к 9 триллионам долларов, что сопоставимо с такими глобальными платежными сетями, как Visa и PayPal.Кросс-граничные платежи, расчеты B2B и валютные операции становятся основными сценариями использования стейблкоинов, которые уже превратились в ключевой слой глобальной финансовой инфраструктуры.

Однако существующая блокчейн-инфраструктура по-прежнему ориентирована в основном на крипто-нативных пользователей и индивидуальных разработчиков и не обеспечивает изначальной поддержки потребностей крупных институциональных игроков.

По мнению специалистов отрасли, институты сталкиваются с несколькими ключевыми проблемами при ведении бизнеса в сети, включая необходимость полного замыкания прав собственности на выпуск и погашение активов между ончейн и офчейн, детерминированный финалитет платежей, предустановленные возможности соответствия требованиям, настраиваемая защита конфиденциальности, а также возможность использования USDC для предсказуемых затрат на газ и т.д.

Эти потребности сложно удовлетворить изначально на существующих публичных блокчейнах, таких как Ethereum и Solana.

Для Circle в прошлом компания в основном получала прибыль за счет процентов по резервам USDC.В первом квартале объем обращения USDC достиг 77 миллиардов долларов, что на 28% больше, чем годом ранее.По мере постоянного расширения масштабов бизнеса зависимость от существующих публичных блокчейнов уже не может полностью соответствовать глубоким потребностям институциональных клиентов.

Поэтому Circle запускает Arc, одна из ключевых целей которой — заполнить этот пробел. Тот факт, что стейблкоин обращается в чужой цепочке, не означает, что стейблкоин-финансы принадлежат ему самому — это и есть глубинная логика решения Circle построить L1 самостоятельно.

Источник изображения:X пользователь @vanisaxxm

II. USDC решает проблему транзакций, ARC — проблему координации

Раз USDC уже является газовым токеном для Arc, зачем выпускать еще и токен ARC?

USDC уже хорошо решает проблему стабильности на уровне транзакций. Институты могут использовать доллар США в качестве прямой основы для расчета комиссий, затраты предсказуемы и могут быть учтены в бухгалтерии, избегая проблем, которые волатильность криптоактивов создает для финансовых отделов.

Однако для долгосрочного здорового функционирования сети недостаточно решить только проблему транзакций, необходимо также решить проблему координации.

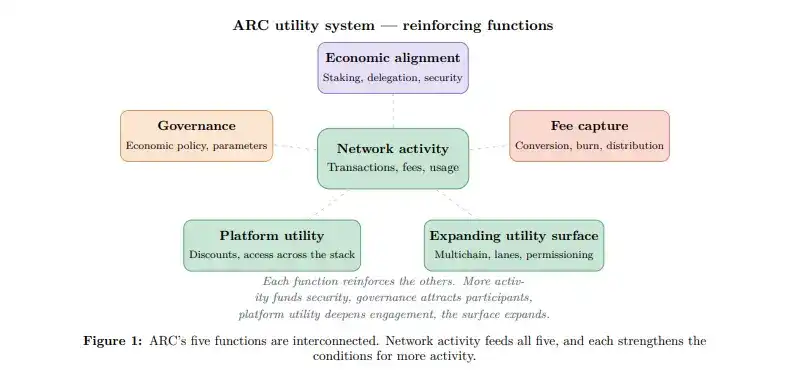

Согласно официальному техническому документу, Arc постепенно перейдет от текущего PoA к PoS. Валидаторам необходимо будет стейкать активы для обеспечения безопасности сети. Суть стейкинга заключается в привязке поведения нод к экономическим интересам: в случае злонамеренных действий они столкнутся с слэшингом (конфискацией). Поскольку стоимость USDC привязана к 1 доллару, она не может по-настоящему привязать ноды к успеху или провалу сети.Только нативный токен ARC может обеспечить такие динамические экономические стимулы.

Уровень управления также требует привязки интересов. Ключевые решения, такие как ставки комиссий, параметры инфляции, пропорции сжигания, требуют от участников долгосрочной перспективы. Если голосование осуществляется только с помощью USDC, держателям может не хватать постоянной мотивации, они могут проголосовать и уйти. Стоимость активов держателей ARC напрямую связана с результатами работы сети, что дает им больше мотивации делать выбор в пользу долгосрочного развития сети.

Технический документ также четко указывает, что права управления ARC имеют поэтапные границы. Экономические параметры определяются голосованием держателей токенов, но такие важные вопросы, как обновления протокола, обработка инцидентов безопасности, проверка квалификации валидаторов, изначально остаются под контролем Circle и будут постепенно передаваться по мере созревания механизмов управления.

Проще говоря, USDC — это кровь сети Arc, отвечающая за эффективное ежедневное движение; ARC — это доля в сети, отвечающая за долгосрочную привязку интересов различных сторон. Такая двойная токенная модель также частично превращает затраты на построение экосистемы из фиксированных денежных расходов Circle в стимулирующие механизмы, привязанные к успеху или провалу сети.

III. Какую часть пирога получают CRCL и ARC

Таким образом, у Circle одновременно есть акции публичной компании CRCL и нативный сетевой токен ARC, оба захватывают стоимость одной и той же сети Arc. Так какую же часть пирога получает каждый из них?

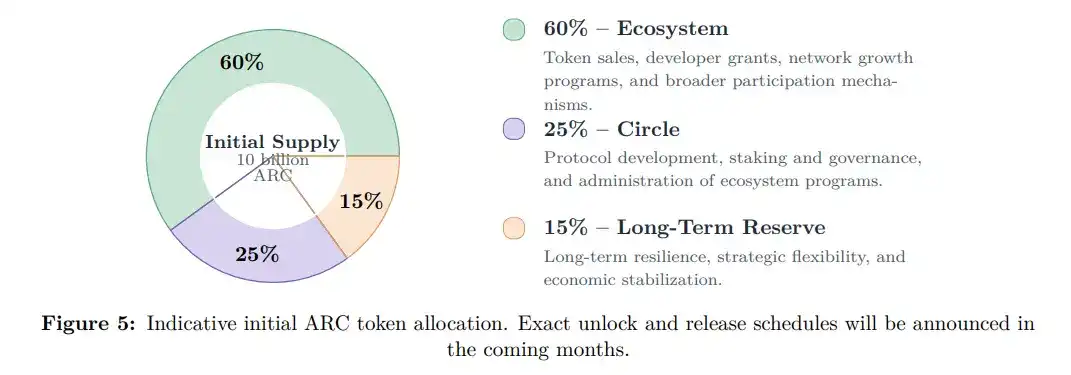

Согласно техническому документу, общее предложение токенов ARC составляет 10 миллиардов единиц, с четким распределением: 60% на экосистему, включая стимулы для разработчиков, планы роста сети и вознаграждения за участие пользователей; 25% принадлежат компании Circle для операций с нодами валидаторов, стейкинга и управления; 15% зарезервированы на долгосрочную перспективу для стабильности сети и стратегической гибкости.

Что касается механизма комиссий, все сетевые комиссии в Arc, независимо от того, каким активом пользователь платит, на уровне протокола будут полностью конвертированы в ARC, часть будет сожжена навсегда, а часть распределена среди стейкеров и валидаторов. Чем активнее сеть, тем сильнее ценностный захват ARC.

Акционеры CRCL в основном получают выгоду через корпоративный уровень Circle. Компания продолжает получать проценты по резервам USDC — основной источник дохода, а также выгоду от роста других бизнесов, таких как платежная сеть CPN. При этом Circle владеет 25% ARC, что также позволяет ей косвенно получать долю от сетевых вознаграждений.

Криптоаналитик BTCdayu предлагает трехмерную оценочную модель для понимания CRCL: первое измерение — это доход от процентов по резервам, который на данный момент является наиболее стабильным денежным потоком и формирует базовый уровень оценки; второе измерение — это доход от платежной сети, который по мере роста CPN может приблизиться к модели сетевых комиссий типа Visa; третье измерение — это сетевая опционная стоимость, которую приносит Arc, то есть рыночные ожидания трансформации Circle из эмитента стейблкоинов в платформу финансовой инфраструктуры.

Проще говоря, CRCL захватывает стабильный денежный поток компании в целом и рост существующего бизнеса, в то время как ARC захватывает эластичность роста на сетевом уровне, включая преобразование комиссий за газ, расширение экосистемы и долгосрочные сетевые эффекты.

Два инструмента образуют четкую двухуровневую структуру. Чем успешнее сеть Arc, тем больше объем использования USDC и сильнее синергия бизнеса, что выгодно для компании Circle; в то же время стоимость токена ARC растет, и принадлежащая Circle доля в 25% также растет в цене, что в конечном итоге передается акционерам CRCL.

Однако на юридическом уровне эти два инструмента полностью независимы.Официально заявлено, что ARC не представляет собой долю в капитале Circle и не дает никаких прав на доходы, прибыль, активы Circle или акции CRCL. Это означает, что держатели ARC не имеют защиты фидуциарной ответственности, присущей акционерам публичных компаний, и их доход полностью зависит от фактического внедрения сети и дизайна токеномики.

IV. Как обычные пользователи могут участвовать в "аирдропе"

После понимания распределения стоимости CRCL и ARC возникает практический вопрос: кому же в конечном итоге продаются токены ARC? И как обычные пользователи могут участвовать с низкими затратами?

Первый тип покупателей — это стратегические институциональные инвесторы. Они входят в проект через предпродажу на сумму 222 миллиона долларов по цене 0,3 доллара за токен, с периодом блокировки от 1 до 4 лет. Эти институты не только предоставляют капитал, но и в большинстве своем являются потенциальными пользователями и строителями Arc. Например, BlackRock уже тестирует расчеты с токенизированными активами в тестовой сети, ICE, как материнская компания Нью-Йоркской фондовой биржи, и SBI Group, как крупнейшая финансовая группа Японии, заранее готовятся к ведению бизнеса на Arc в будущем.

Второй тип — это строители экосистемы и долгосрочные держатели. Разработчики, поставщики ликвидности получают вознаграждение ARC за свой вклад, для этого предназначены 60% распределения на экосистему. Они больше заинтересованы в долгосрочном росте сети, подобно ранним сотрудникам, владеющим долей в компании.

Третий тип — розничные спекулянты и участники. Они обращают внимание на возможности, связанные с ранними нарративами, и стимулы в экосистеме, ожидая волатильности цен после запуска основной сети.

Для обычных пользователей, не имеющих права на предпродажу, Arc предлагает несколько путей участия с низкими затратами.

Arc Testnet запущен в октябре 2025 года, и на данный момент обработано более 244 миллионов тестовых транзакций. Запуск основной сети ожидается летом 2026 года. Пользователи могут бесплатно получить тестовые токены для совершения обменов (Swap), мостовых операций (Bridge), развертывания контрактов и других действий, знакомясь с сетевым взаимодействием.

Сообщество Arc House является основным входом для обычных пользователей. Пользователи могут накапливать баллы, регистрируясь в сообществе, оставаясь активными, публикуя посты, читая контент, участвуя в вопросах и ответах. За принятые ответы также начисляются дополнительные баллы.

Более продвинутые способы включают создание контента, обмен видео, организацию мероприятий и даже проведение офлайн-встреч. Кроме того, пользователи с командами или продуктами могут подать заявку на гранты для разработчиков Circle (Circle Developer Grants).

Следует отметить, что баллы Arc House являются лишь признанием вклада в сообщество, не имеют денежной стоимости и не гарантируют какого-либо конкретного распределения прав. Конкретные правила следует уточнять в последних официальных объявлениях.

Заключение

В настоящее время конкуренция в сегменте блокчейнов для институтов ожесточенная, Arc не является единоличным лидером.

Digital Asset, к которой принадлежит Canton Network, в настоящее время завершает новый раунд финансирования с оценкой около 2 миллиардов долларов под руководством a16z crypto; Plasma позиционируется как нативный расчетный блокчейн для стейблкоинов, ее оценка относительно более привлекательна; Visa уже в апреле включила такие проекты, как Arc, Canton, Plasma, Base, Tempo, в качестве тестовых точек для расчетов стейблкоинов. Это говорит о том, что данный сегмент все еще находится на этапе параллельного развития нескольких игроков и конкуренции.

На этом фоне полностью разводненная стоимость (FDV) предпродажи Arc в 3 миллиарда долларов находится на относительно высоком уровне. Розничным инвесторам, участвующим на вторичном рынке, необходимо тщательно оценить потенциал нарратива проекта и конкурентную среду внутри сегмента.

В долгосрочной перспективе для удержания ARC с ежегодной инфляцией от 2% до 3% необходимо, чтобы сеть генерировала достаточное количество реальных комиссий, чтобы компенсировать давление от эмиссии, и тогда можно будет добиться роста стоимости. В то же время CRCL, опираясь на проценты по резервам USDC и доход от платежной сети, имеет относительно четкую поддержку в виде денежного потока. Эти два инструмента сталкиваются с разными профилями риска и доходности.

В краткосрочной перспективе рыночные настроения часто имеют свою собственную логику. В период перед запуском основной сети и сразу после него, когда нарративы достигают пика, могут возникать возможности для краткосрочных операций. В этот период стоимость принадлежащих Circle 25% ARC также будет расти, и акционеры CRCL смогут извлечь из этого выгоду.

На уровне регулирования принятие закона GENIUS Act укрепило конкурентное преимущество Circle, а новая версия законопроекта CLARITY Act уже опубликована и в настоящее время продвигается в Конгрессе, что может обеспечить более четкую нормативную определенность для экосистемы цифровых активов и является важным положительным фактором для Circle.

В целом, Arc является на данный момент важной стратегической инициативой Circle. Как указано в техническом документе, "глобальная экономическая операционная система не может координироваться одним субъектом; она превращает участников Arc в тех, кто поддерживает Arc". Реализация этого видения в конечном итоге зависит от того, сможет ли сеть после запуска привлечь достаточно масштабные реальные институциональные транзакции и экономическую активность.

Пока все данные не станут реальностью, все нарративы остаются всего лишь нарративами.