Recently, Bitcoin's price has experienced a pullback, while assets like gold and silver have also shown significant volatility. Macroeconomic uncertainty has notably increased, putting overall pressure on risk assets. Against this backdrop, market sentiment has turned cautious, with discussions around crypto assets gradually shifting from growth expectations to survival capabilities. Among these, the operational status of miners has become a focal point, and the concept of the "miner shutdown price" is frequently mentioned.

This concern is not unfounded. Under the dual pressures of price declines and tightening macro liquidity, the profitability of the mining industry indeed faces periodic challenges. The market attempts to use the "shutdown price" as an indicator to assess whether miners might be forced to exit on a large scale, thereby affecting network security and asset prospects. This attention itself reflects market participation. However, if this concept alone is used as the core basis for judging industry risks, it often overlooks key differences and self-regulating characteristics within Bitcoin's mining operation mechanism. In practice, the "shutdown price" is not a simple, uniform price threshold.

Shutdown Price is Often Misunderstood

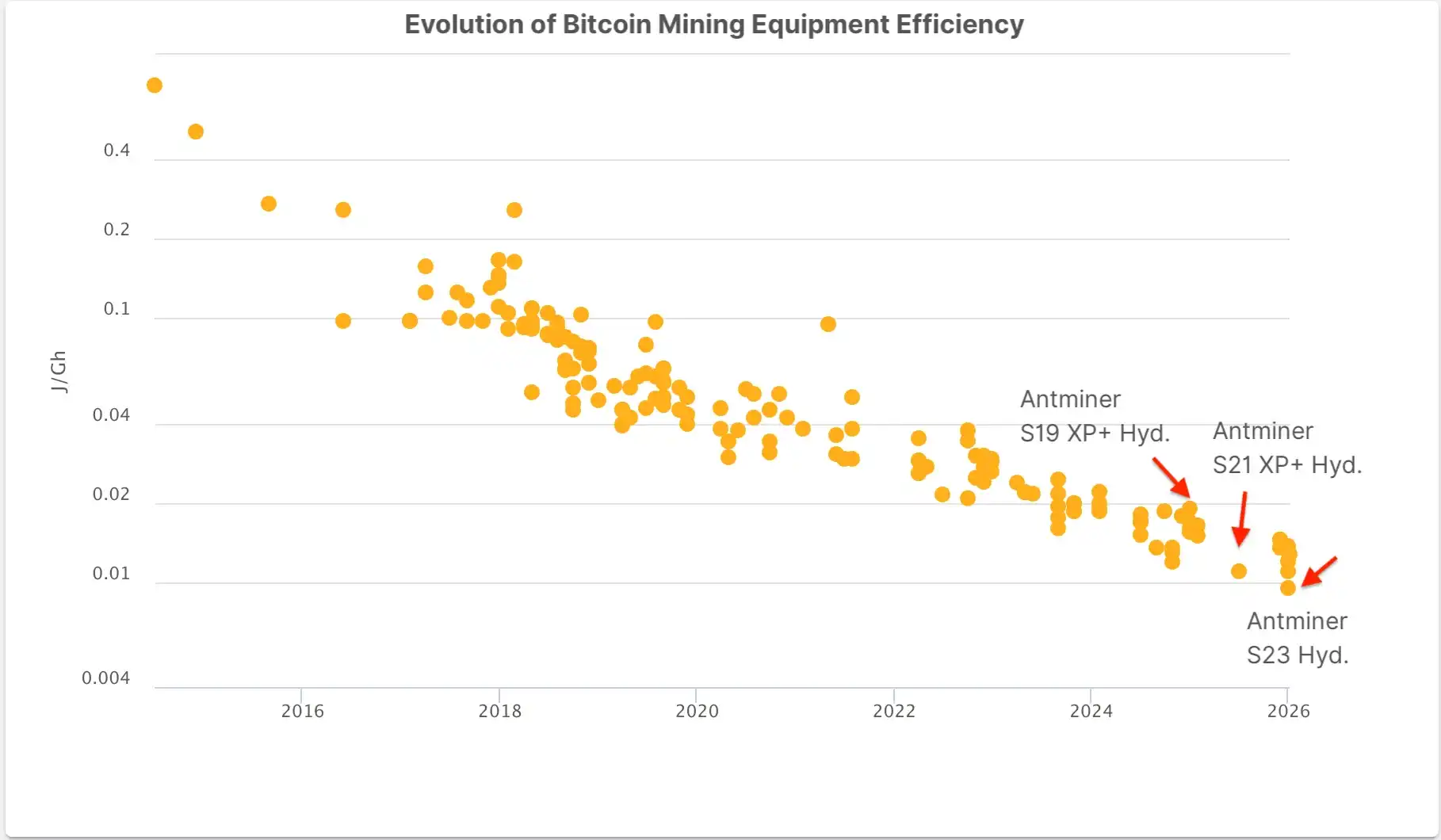

From an industry perspective, there is no single "miner shutdown price" that applies to all miners. The so-called "shutdown price" is more of a theoretical result derived from model calculations under specific assumed conditions, typically assuming uniform electricity costs, equipment efficiency, and operational cost structures. However, in reality, the cost structure of the mining industry is highly fragmented. Different miner models exhibit significant differences in energy efficiency performance; the unit hash rate cost of new-generation high-efficiency miners is not comparable to that of older equipment. For example, among current mainstream models, the Antminer S23 Hyd (approx. 580 TH/s, 5510W) has an efficiency of about 9.5 J/T, the Antminer S21 (approx. 480 TH/s, 5280W) about 11 J/T, and the Canaan Avalon A16XP-300T about 12.8 J/T. Every 1–2 J/T improvement in unit efficiency significantly changes the breakeven range at the same electricity price.

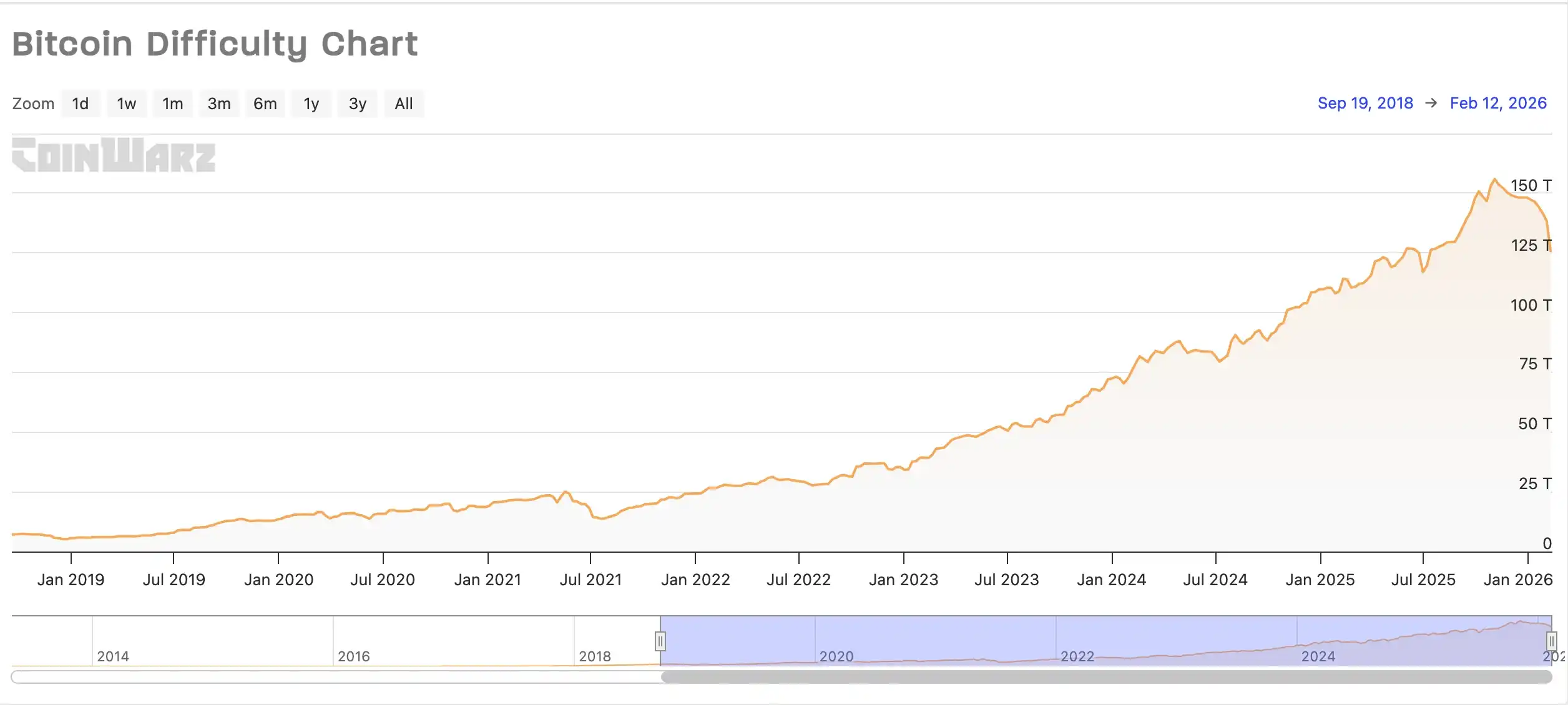

Source: Cambridge Bitcoin Electricity Consumption Index (CBECI), Cambridge Centre for Alternative Finance (CCAF), accessed February 12, 2026

Energy environments and contracted electricity prices also vary significantly between mining facilities, from hydropower and wind power to thermal power. Different energy mixes directly determine marginal cost levels. Large mining farms in regions abundant with hydropower resources, such as parts of North America, can secure long-term contract rates as low as $0.03–0.05/kWh, while commercial electricity prices in some regions with higher energy costs can reach $0.08–0.12/kWh. The operational pressure for the same miner model therefore differs significantly across different electricity price environments. Additionally, differences in operational efficiency, management costs, capital structure, and risk management strategies among miners also affect their ability to withstand price fluctuations.

Precisely because of these variations in miner models, electricity cost structures, and operational efficiencies, there is no uniform "miner shutdown price" across the industry. The actual situation depends on the mining facility conditions and equipment configuration. Treating a model result based on average assumptions as the industry's "survival line" itself tends to amplify market sentiment.

When the Bitcoin price gradually approaches some cost ranges amid fluctuations, the real change occurring in the industry is often more akin to a structural adjustment rather than a concentrated outbreak of systemic risk. During phases of price pressure and relatively high mining difficulty, the overall profit margin of the industry narrows. Adjustment first appears in marginal hash rate with higher costs and lower efficiency. Some smaller-scale miners, those with higher energy costs, or those using older equipment may choose to gradually shut down equipment, reduce hash rate, or adjust their asset structure to alleviate operational pressure.

This process is often reflected in macro data as a periodic decline in the network's total hash rate. A drop in hash rate does not mean network security is compromised; it more reflects natural clearing and metabolism within the industry. In fact, such cyclical changes often accelerate the concentration of hash rate towards entities with scaled operations and cost advantages, thereby improving the overall operational efficiency of the industry.

Market Screening and Self-Adaptation

At a deeper level, the "shutdown price" is not an absolute price floor but更像是一个动态调节中的参考区间 (more like a reference range in dynamic adjustment). During market volatility, miners with high costs and low energy efficiency may choose to temporarily shut down equipment or adjust their operational strategies. The Bitcoin network itself possesses mature self-adjusting mechanisms. When some hash power exits, the network's mining difficulty subsequently adjusts downward. The remaining, more efficient hash power then gains a larger share of rewards, pushing the network gradually towards a new equilibrium. It is this self-regulating capability that allows the Bitcoin mining ecosystem to continue operating through multiple cycles and brings improved unit hash rate output and operational environment for the efficient miners who remain running.

Extending the timeline makes this pattern clearer. In past cycles, the industry has experienced phases where the price fell below the production cost range for some miners. In periods like 2019 and 2022, the Bitcoin price也曾低于当时大部分矿机的生产成本区间 (also fell below the production cost range of most miners at the time). However, following adjustments in hash rate, changes in difficulty, and market repair, it gradually converged towards new equilibrium ranges. Each cyclical adjustment pushes the industry towards lower energy costs, higher hash rate efficiency, and a more professionalized and scaled direction. Clearing out outdated capacity is itself an important sign of industry maturation.

How to Move Forward Amid Volatility

Returning to the enterprise level, the key to coping with industry volatility lies not in short-term price judgments but in long-term preparation and operational resilience. Taking BitFuFu as an example, the company has long focused on mining infrastructure construction and operational efficiency optimization, continuously deploying new generations of high-efficiency miners. Through scaled operations and refined energy cost management, it constantly improves overall hash rate quality. The company has also deployed diversified energy cooperation, building a competitive electricity cost structure. Benefiting from comprehensive advantages in equipment efficiency, energy structure, and operational systems, its current hash rate remains stable, enabling the company to maintain relatively stable output performance and a healthy asset structure during industry adjustment phases.

Short-term market volatility is inevitable, but what the Bitcoin network and mining industry have demonstrated through cycles is strong self-adaptive capability and continuous evolutionary progress. Behind the discussion of the "shutdown price," what is truly worth attention is how the industry completes efficiency leaps amidst volatility, and those enterprises that consistently focus on long-term development and continuously build moats of cost and efficiency.

Winter screens vitality, cycles temper true value. The industry is experiencing not an exit, but a deeper consolidation and upgrade. We are always here, focused, steady, moving forward together with the network.