Страх рыночных участников перед рисками падения практически исчез, ключевой механизм ценообразования на рынке опционов перестает работать.

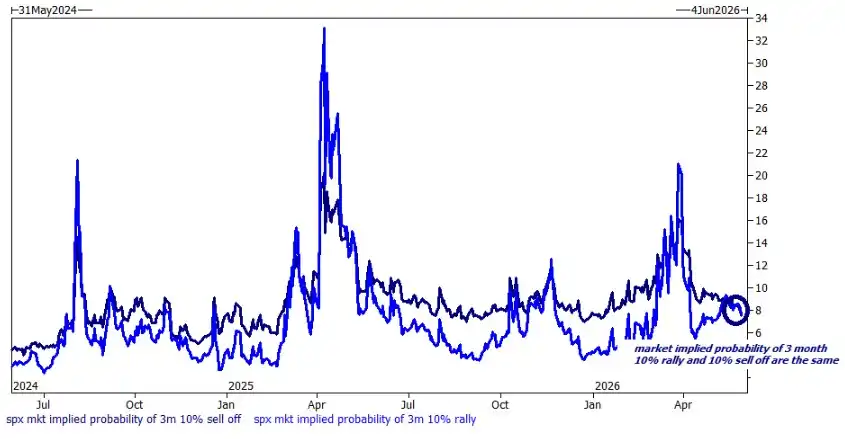

Стратег по деривативам Goldman Sachs Брайан Гарретт в своем свежем отчете на выходных отметил, что перекос волатильности (Skew) по опционам на индекс S&P 500 упал до минимума за 18 месяцев. Рынок оценивает вероятность падения на 10% и роста на 10% почти одинаково — примерно в 8%. Это явление команда по волатильности Goldman Sachs напрямую охарактеризовала как «отказ Skew».

В то же время индекс паники Goldman Sachs опустился до однозначных цифр, достигнув двухлетнего минимума, что свидетельствует о крайне низком уровне спроса на хеджирование рисков экстремальных событий (хвостовых рисков).

Этот сигнал появился на фоне непрерывного стремительного роста американского фондового рынка. С начала года индекс S&P 500 обновляет исторические максимумы в среднем каждые пять торговых сессий, а акции Micron в воскресенье после закрытия торгов впервые преодолели отметку в 1000 долларов.

Гарретт признался, что обсуждения внутри его команды эволюционировали с марта от «остановите это» до мая «оно все еще растет?». Однако его собственная позиция меняется от осторожного оптимизма к все большему пессимизму, и он четко перечислил несколько причин для медвежьего настроя.

Появляются три сигнала медвежьего рынка, наметился разрыв между настроениями рынка и фундаментальными показателями

Гарретт перечислил три основные скрытые опасности на текущем рынке.

Во-первых, чрезвычайная узость лидерства роста рынка. На десять крупнейших по весу акций в индексе S&P 500 сейчас приходится 40% веса индекса, а последние четыре обновления исторических максимумов происходили при отрицательной общей ширине рынка — ранее такое явление никогда не наблюдалось.

Во-вторых, высокая концентрация на тематике. С начала года индекс S&P 500, исключающий акции, связанные с ИИ, отстает от общего индекса на 700 базисных пунктов.

В-третьих, динамика цен в высокой степени повторяет историю. Гарретт отметил, что динамика 2026 года в высокой степени соответствует ценовым паттернам конца 1998 — 1999 годов.

Хотя медвежьи настроения заполонили заголовки СМИ и соцсети, Гарретт подчеркивает, что эти опасения не нашли отражения в ценообразовании на опционном рынке — по крайней мере, страх перед рисками падения практически незаметен.

Отказ Skew: стоимость хеджирования падения упала до исторического минимума

Команда по волатильности Goldman Sachs дала три ключевых наблюдения с точки зрения опционного рынка.

Первое: перекос волатильности (Skew) по S&P 500 упал до минимума за 18 месяцев, что обусловлено действием двух сил: опционы пут (put wing) аномально дешевы, в то время как опционы колл (call wing) относительно дороги.

Второе: индекс паники Goldman Sachs (GS Panic Index) в прошлую пятницу закрылся на однозначном уровне, достигнув двухлетнего минимума. Этот индекс представляет собой сводный рейтинг процентилей за два года по VVIX, VIX, Skew и волатильности «при деньгах» (at-the-money).

Третье и самое важное: рынок оценивает вероятность падения на 10% и вероятность роста на 10% совершенно одинаково — примерно в 8%. Это означает, что опционный рынок больше не назначает дополнительную премию за риск падения, и защитная функция Skew фактически перестала работать.

Гарретт отмечает, что прямое значение указанных явлений заключается в следующем: для инвесторов, желающих застраховаться от корреляционных рисков, текущая стоимость хеджирования чрезвычайно низка.

Низкозатратное хеджирование в сочетании со ставкой на правый хвост распределения

Основываясь на приведенных выводах, Гарретт дал ряд конкретных торговых рекомендаций.

Для инвесторов, ожидающих смены рыночного стиля и верящих, что движение рынка пойдет от концентрации к диверсификации, Goldman Sachs рекомендует покупать опционы на опережение RSP (ETF Invesco S&P 500 Equal Weight) относительно SPX, стоимость 1-месячного опциона на 100% опережение составляет около 145 базисных пунктов. Также рекомендуется покупать опционы колл на VIX в качестве хеджирующего инструмента, отмечая, что кривая форвардов для августа и более поздних сроков крайне плоская, а VVIX закрылся на уровне 86.

Для инвесторов, ищущих простую защиту от падения, Гарретт советует напрямую покупать опционы пут на S&P 500 — учитывая, что текущий перекос для опционов пут крайне низок, структура выплат выглядит весьма привлекательно.

Кроме того, Goldman Sachs рекомендует покупать волатильность биткоин-ETF с нейтральным хеджированием по дельте. Гарретт отметил, что исторически биткоин вел себя как «рычаговая версия Nasdaq», но его текущая оценка находится на двухлетнем минимуме и примерно на 10 пунктов волатильности ниже, чем у SMH.

Движение капитала: хедж-фонды две недели подряд чистые покупатели, объем ETF на отдельные акции удвоился

Согласно последним данным Goldman Sachs Prime Brokerage, хедж-фонды две недели подряд были чистыми покупателями, причем с самой высокой скоростью за год, что в основном выражалось в увеличении длинных позиций и закрытии коротких макропозиций.

На отраслевом уровне наблюдается явная ротация: акции финансового сектора (с начала года падение на 6%) были объектом чистых покупок, тогда как акции промышленного сектора (с начала года рост на 11,5%) стали объектом чистых продаж.

На фьючерсном рынке позиции конечных пользователей вернулись почти к уровням максимумов 2024 года. Команда Goldman Sachs особо отмечает, что ETF с использованием заемных средств (рычаговые ETF) механистически увеличивают масштабы своих балансов. Стратегии CTA (управляемых фьючерсных счетов) в настоящее время близки к нейтральным, но системные стратегии демонстрируют явную асимметрию в отношении левого хвоста распределения: при сценарии «без изменений за 1 месяц» происходит покупка примерно на 12 миллиардов долларов, а при сценарии «падение за 1 месяц» — продажа примерно на 100 миллиардов долларов.

Заслуживает внимания то, что глобльный объем активов под управлением рычаговых и обратных ETF на отдельные акции превысил 60 миллиардов долларов, удвоившись за два месяца — масштабы этого сегмента рынка уже нельзя игнорировать.