ETF на Dogecoin продолжают фиксировать низкий спрос с момента их запуска в прошлом месяце, что свидетельствует об отсутствии интереса со стороны институциональных инвесторов к мемной монете. Примечательно, что DOGE также показала самый низкий спрос через эти ETF среди ведущих монет по рыночной капитализации.

ETF на Dogecoin фиксируют сокращение объемов и притоков

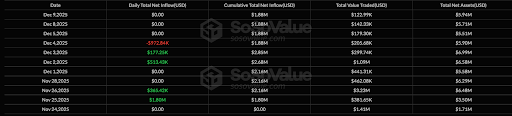

Данные SoSoValue показывают, что ETF на Dogecoin продолжают демонстрировать снижение дневного объема и притоков с момента их запуска в прошлом месяце. 10 декабря ETF на DOGE от Grayscale и Bitwise зафиксировали торговый объем в $125 100. Между тем, эти фонды в совокупности показали общий чистый приток в $171 920 за день.

Дальнейшие данные от SoSo Value показывают, что торговый объем ETF на Dogecoin снижается с 2 декабря, когда был зафиксирован дневной торговый объем в $1,09 миллиона. Эти фонды показали всего три дня с семизначным торговым объемом из 12 торговых дней с 24 ноября, когда запустился фонд Grayscale на Dogecoin.

Это относительно низкий показатель и свидетельствует о слабом спросе на ETF на DOGE среди институциональных инвесторов. Для контекста, ETF на Chainlink от Grayscale, единственный фонд на LINK на данный момент, показал лучшие результаты, чем ETF на Dogecoin, несмотря на запуск в начале этого месяца. Чистые активы ETF на LINK от Grayscale составляют $77,71 миллиона, в то время как у ETF на DOGE общие чистые активы составляют $6,01 миллиона.

Чистые потоки также подчеркивают неудовлетворительные результаты этих ETF на Dogecoin. С момента запуска фонд Bitwise на DOGE зафиксировал чистый отток в размере $972 840. Между тем, фонд Grayscale привлек чуть более $3 миллионов. Фонды в целом зафиксировали чистые притоки в пять из 12 торговых дней.

Возможная причина неудовлетворительных результатов

Аналитик Bloomberg Эрик Балчунас предупреждал ранее, что крипто-ETF, такие как ETF на Dogecoin, будут привлекать меньше активов из-за их отдаленности от Биткойна с точки зрения рыночной капитализации. «Чем дальше вы отходите от BTC, тем меньше будет активов», — сказал он. Примечательно, что фонды на DOGE имеют самые низкие чистые активы среди топ-10 криптовалют по рыночной капитализации, имеющих ETF-оболочку.

ETF на Solana и XRP, которые также были запущены в прошлом месяце, показали лучшие результаты, чем ETF на Dogecoin, хотя фондов, предлагающих SOL и XRP, больше. Между тем, теория Балчунаса не применима к ETF на LINK, так как он превзошел фонды на DOGE, несмотря на то, что рыночная капитализация Chainlink ниже, чем у Dogecoin.

Кроме того, ETF на Hedera и Litecoin также имеют более крупные чистые активы, чем ETF на Dogecoin, что указывает на то, что институциональные инвесторы просто не настроены бычье на DOGE, возможно, из-за ее статуса мемной монеты и отсутствия полезности. DOGE — пока что единственная мемная монета с ETF-оболочкой.

На момент написания цена DOGE торгуется на уровне около $0,138, снизившись более чем на 6% за последние 24 часа, согласно данным от CoinMarketCap.