On January 26, The Federal Open Market Committee, a committee within the Federal Reserve System issued a statement that it would end tapering in early March, and then start raising interest rates and reducing the size of the Fed's balance sheet. This reflects a complete turnaround and a likely end to the loose monetary policies of the past two years. Both the US stock market and the crypto market fell slightly in response to this statement, indicating that it was in line with market expectations. However, markets still ended up disappointed. What’s the reason behind this? Let's take a look at the Fed statement more closely.

First, as the Fed noted in its original text: With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds.

Why does the article emphasize inflation and the labor market? You should understand the Fed's monetary policy framework first.

According to the Federal Reserve Act, the Fed's monetary policy was designed to "maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of (1) maximum employment, (2) stable prices, and (3) moderate long-term interest rates".

To realize the monetary policy goals above, the Taylor rule proposed by Taylor in 1993 plays an important role. Taylor's rule is expressed as follows:

Where FFRt stands for the policy interest rate of the Federal Reserve, rt* stands for the equilibrium real interest rate; πt is the rate of inflation; πt* represents the target inflation rate, and (π-πt*) represents the inflation gap; Y is economic output, yt* represents potential economic output, and (y-yt*) represents output gap; Two parameters a and b represent the response of the policy interest rate to the two types of gap respectively. This formula implies that central banks should tighten monetary policies when inflation is above the target number; when output is below potential economic output, the policies should be loosened as a response.

After 2014, based on the previous Taylor rule, the Federal Reserve developed optimal control policies to minimize divergence of the unemployment rate and the inflation rate from their respective targets. The latest monetary policy framework is still consistent with the core logic of the Taylor Rule. Specifically, since 2012, the Federal Reserve has achieved a relatively stable long-term goal over an eight year time frame: maintaining 2% inflation in the long run.

Back to the FOMC statement in January, "Inflation is well above 2% and the labor market is active." Under the Taylor rule, increasing interest rates in the future is inevitable. That's why the Fed's statement was consistent with market expectations.

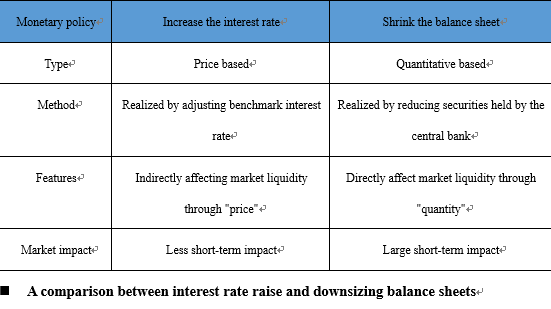

In addition, it should be noted that the Fed's statement clearly stated "significantly reducing the size of the Federal Reserve's balance sheet".

We know that interest rate hikes are a pricing tool, while reducing size of the balance sheet is a quantitative tool. An interest rate increase refers to the positive adjustment of the federal funds target rate: Federal Reserve adjusts the federal funds rate closer to the target rate through open market operations, thus changing short-term borrowing costs, moderating liquidity and economic growth. Reducing the balance sheet means that the Federal Reserve reduces its holdings of securities, either through direct active selling or passive management, which means holding those assets until maturity.

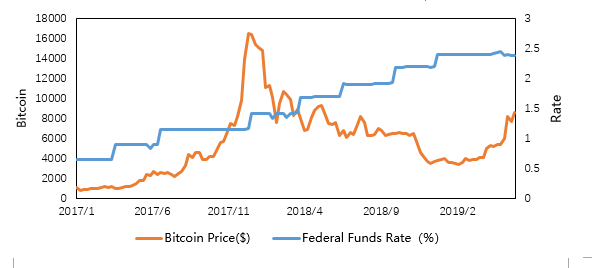

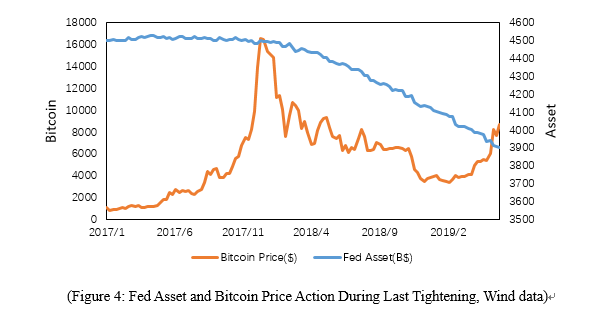

Compared with raising interest rates, reducing the balance sheet reflects a direct withdrawal of liquidity from the market, which has a greater impact on the economy in the short term. A vivid example is that, when a user takes a loan, if the bank increases the rate, the user is likely to pay a higher rate to obtain a loan, but if the bank directly reduces the loan amount, then the user will have no choice. From historical data, during the Fed tightening period from 2015 to 2018, although the Fed began to raise rates since 2016, the price of Bitcoin still rose and saw a big bull run in 2017. But shortly after reducing the balance sheet in October 2017, Bitcoin entered into a bear market. Therefore, we should pay more attention to the impact of the Fed reducing its balance sheet, rather than raising rates in 2022.

(Figure 3: Fed Rate and Bitcoin Price Action During Last Tightening, Wind data)

At the same time, we can also see the Fed reiterating “changes in the target range for the federal funds rate as its primary means of adjusting the stance of monetary policy”. Its purpose is to reduce the influence of monetary policy changes on the economy in the short run.

Furthermore, after the Fed's previous rounds of loose monetary policies, the market each time was flooded with liquidity; raising rates this time around may lead to a flattening of the interest rate curve, or even trigger an inverted economic recession signal. To control the flattening of the interest rate curve and reduce risks to financial stability, tools to reducing the balance sheet must be deployed. As a result, Fed determined the policy framework of “raising interest rates first, reducing the balance sheet later" and clearly stated that “significantly reducing the size of the Federal Reserve's balance sheet”. In order to prevent market panic for reducing balance sheet, at the same time, the Fed emphasized “a predictable manner primarily by adjusting the amounts reinvested of principal payments received from securities held in the System Open Market Account (SOMA)”.

To summarize, the Federal Reserve statement was basically in line with market expectations, and interest rates will be raised as early as March. However, the extent of future interest rate increases, and the schedule and size of balance sheet reductions have yet to be unveiled, which should be the focus of the Fed’s next steps.