Author: Gino Matos

Compiler: Chopper, Foresight News

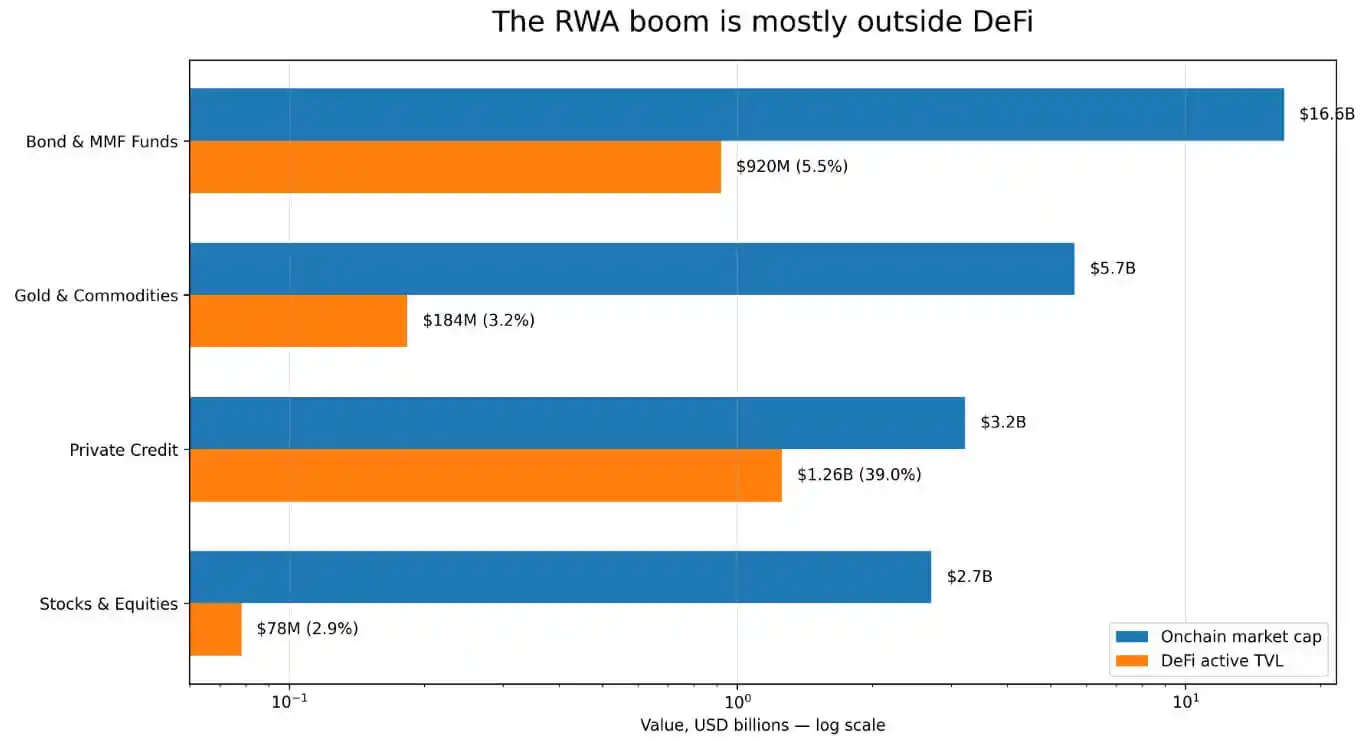

Data from DeFiLlama shows that the on-chain tokenized real-world asset (RWA) scale has approached $30 billion. However, only $2.47 billion is shown as the active DeFi Total Value Locked (TVL), which is the actual amount of funds deposited into third-party DeFi platform liquidity pools and participating in the ecosystem's operation.

The vast majority of other RWA assets remain outside of scenarios such as lending markets and collateral vaults, which enable free combination and interaction of crypto assets. Bonds and money market funds are the largest RWA category by scale, with an on-chain total exceeding $16.6 billion. Yet, the effective TVL flowing into the DeFi ecosystem is only $920 million. The on-chain scale of gold and commodity assets is $5.7 billion, with only $183.6 million effectively circulating in DeFi. Equity assets have an on-chain scale of $2.7 billion, but the funds that have entered the DeFi market are a mere $78.27 million.

Only the private credit sector stands out: its on-chain scale is $3.226 billion, with a DeFi effective TVL of $1.257 billion, achieving an ecosystem penetration rate of 39%. The reason behind this is that projects like Maple Finance and Centrifuge were designed from the outset as lending financial instruments, making them naturally suited for DeFi application scenarios.

In contrast, tokenized products like US Treasury bond funds, gold assets, and stock assets are designed by their issuers to cater more to institutional custody needs, with their overall architecture aligning with the operational models of traditional compliant funds.

Distribution of On-Chain Market Value and DeFi Active TVL Across Four RWA Categories

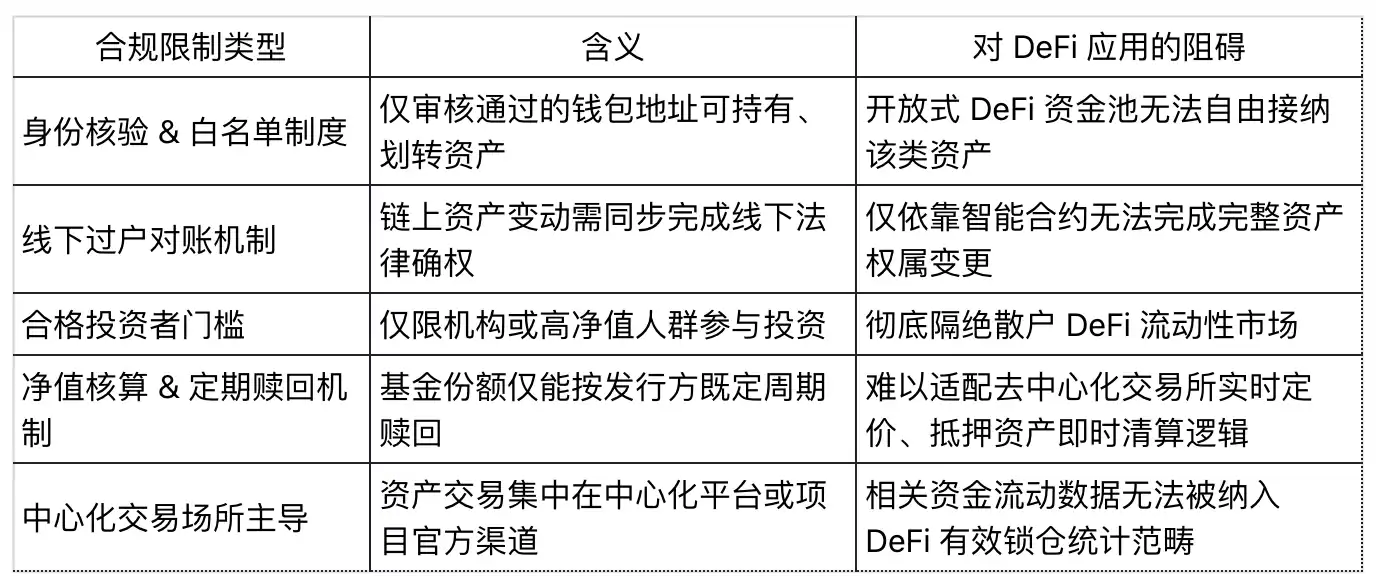

Permissioned Architecture Becomes the Biggest Barrier to DeFi Composability

DeFiLlama categorizes the money market fund product BUIDL by BlackRock as a permissioned fund. Its effective TVL within the DeFi ecosystem is only $18.9 million.

The International Organization of Securities Commissions (IOSCO) pointed out in its final report on financial asset tokenization released in November 2025 that BUIDL created a permissioned system on a public blockchain for issuance, custody, secondary trading among qualified investors, dividend distribution, and redemption.

Potential investors must pass the whitelist review on the Securitize platform. Furthermore, on-chain asset transfer actions only attain full legal validity after information verification and confirmation by an offline transfer agent.

This means that BUIDL is essentially a compliant custody infrastructure built atop blockchain channels, primarily serving institutional asset custody and offline account reconciliation needs. Its smart contracts only support interactions from whitelisted addresses. Without using a compliant wrapping layer as an intermediary, they cannot be directly deposited into permissionless, open DeFi protocols like Aave or Uniswap.

In February 2026, BlackRock completed the integration of BUIDL with Uniswap, enabling partial assets to enter trading pools. However, asset access permissions are still controlled by Securitize, limited to qualified investment institutions with a net asset value of no less than $5 million; ordinary market participants still cannot participate.

IOSCO found that the vast majority of tokenized money market funds on the market currently adopt similar operational models. These assets have so far failed to deliver the high secondary market liquidity value previously anticipated by the industry.

RedStone stated bluntly in its tokenization industry report released in March 2026 that the most challenging part of asset tokenization implementation is coordinating a series of complex rules across different jurisdictions and public chain ecosystems, including compliance review, identity verification, trading permission restrictions, risk control sanctions screening, and corporate rights distribution. Looking at the current market, Morpho and Aave Horizon are among the few genuine case studies successfully implementing RWA assets in DeFi applications.

In short, each compliance and access restriction set by project parties further raises the barrier for assets to enter the DeFi ecosystem. Products like US Treasury token bonds and money market funds are themselves designed to meet the regulatory requirements of licensed institutional investors, actively incorporating various permission constraints.

Gold and commodity assets face another practical issue. CoinGecko data shows that in Q1 2026, spot trading volume for tokenized gold reached $90.7 billion, surpassing the total for the entire year of 2025. However, the vast majority of this trading occurs on centralized exchanges. The aforementioned DeFi effective TVL of $183.6 million only represents a tiny fraction circulating within the ecosystem. The enormous trading volume in centralized markets is completely outside the scope of DeFiLlama's data statistics.

Positive Outlook: Highly Compatible Products Have Set Examples

In early 2026, the TVL of Ondo's USDY exceeded $1 billion and has now achieved full coverage across nine public chain ecosystems. The Ondo Global Markets segment, launched in September 2025, focuses on tokenized US stocks and ETF assets for overseas investors. It was designed from the start to support free asset transfer and direct use as DeFi collateral. Currently, the TVL for corresponding assets is $650 million, with cumulative trading volume exceeding $12 billion.

According to RedStone statistics, the RWA deposit scale on the Morpho platform exceeds $620 million, and the total RWA-related asset scale on Aave Horizon is $423.5 million. Both lending protocols have successfully implemented mature RWA collateralized lending models.

These implementation cases fully prove that as long as the design philosophy of permissionless free circulation is upheld from the asset issuance stage, RWA assets can fully achieve composability within the DeFi ecosystem.

During an industry roundtable hosted by DWF Labs in April 2026, projects including Centrifuge, Falcon Finance, and xStocks jointly proposed the view that the RWA sector has now diverged into two major development tracks. The first prioritizes compliance with asset ownership regulations, adhering to a strictly permissioned and controlled path. The second balances compliant issuance standards while enabling secondary market circulation properties, with ecosystem composability as the core design orientation.

Graham Nelson, the person in charge of the Centrifuge project, stated that stringent whitelist access mechanisms mean each participant in a liquidity pool needs to undergo separate qualification reviews, directly blocking the path for assets to enter open DeFi.

The DeRWA solution launched by Centrifuge bypasses this barrier by wrapping the underlying primary issuance assets in a compliant manner while relaxing restrictions on secondary market asset circulation. Artem Tolkachev from Falcon Finance also mentioned that ecosystem composability and flexible exit mechanisms are the key bridges connecting real-world assets with crypto market liquidity.

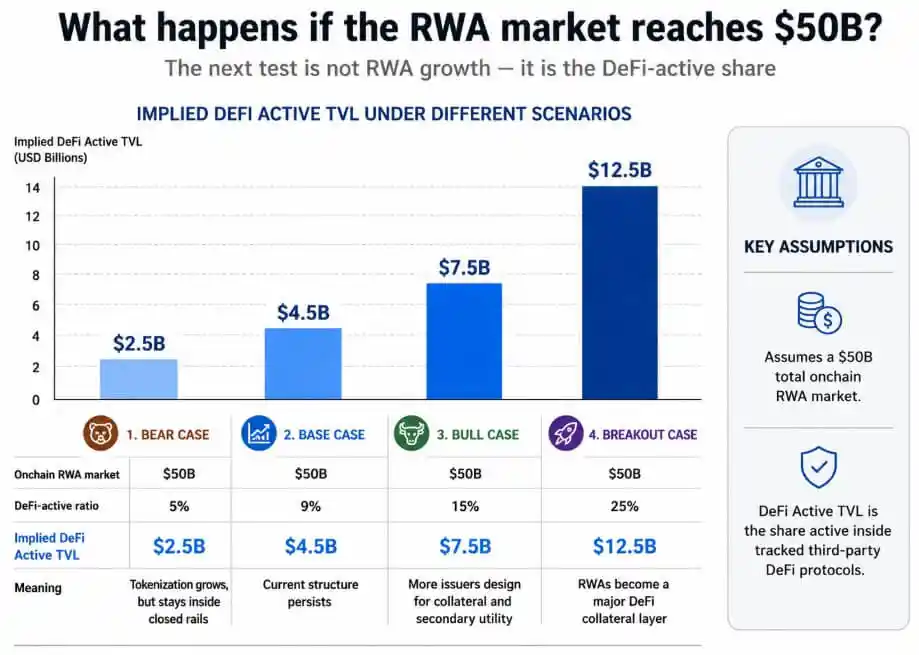

The industry is optimistic that as the overall on-chain RWA asset scale approaches $50 billion, if most projects within the sector shift towards designs compatible with DeFi, the penetration rate of RWA assets in the DeFi ecosystem is expected to break through the current low level of 9%.

Negative Reality: Industry Growth May Be Confined to the Traditional Financial System

Standard Chartered Bank predicts that the global tokenized asset scale will reach $2 trillion by 2028, but it simultaneously warns that this industry boom is likely to be confined within the traditional banking and financial system, with limited growth benefits for the open crypto market.

IOSCO's research in November 2025 also corroborates this point. Constrained by the inherent access barriers and liquidity shortcomings of distributed ledger technology, the current distribution, circulation, and secondary market trading of tokenized assets still heavily rely on traditional financial infrastructure.

The European Central Bank further pointed out in its tokenization industry research report released in April 2026 that the absence of unified global standards for asset tokenization is highly prone to creating isolated asset silos. Different asset systems have their own compliance rules, settlement layers, and access mechanisms, ultimately leading to high concentration of liquidity within closed circles, making interconnection and circulation difficult.

The DeFi penetration rates of 5.5% for bonds and money funds, 3.2% for gold and commodities, and 2.9% for equities directly reflect this fragmented ecosystem pattern.

Most US Treasury tokens and money fund products on the market commonly set minimum investment thresholds, mandatory identity verification, offline asset reconciliation cycles, and fixed redemption windows tied to net asset value. These underlying rules inherently conflict with the operational logic of decentralized exchanges' real-time pricing and permissionless collateral vaults. These constraints are mandatory requirements from the regulatory level and an inevitable choice for asset issuers to adapt to the compliant environment.

Two Markets, One Industry Label

The total on-chain RWA scale of $30 billion and the effective DeFi circulation scale of $2.47 billion, while seemingly belonging to the same RWA sector, actually correspond to two completely separate markets:

- Compliant On-Chain Financial Market: Primarily consisting of money market funds, US Treasury funds, and institutionally custodied assets. Asset transfer relies on offline transfer agent reconciliation and confirmation, following traditional financial regulations throughout.

- DeFi Composability Ecosystem Market: Assets can be freely deposited into lending protocols, used as permissionless collateral, and integrated into various automated yield strategies for free circulation.

The chart above predicts the implied DeFi Active TVL under four scenarios in a $50 billion RWA market, ranging from 5% to 25%

The achievement of over $620 million in RWA deposits on Morpho and the circulation of USDY across 9 blockchains is sufficient proof that the second type of market possesses genuine development potential.

To drive the DeFi penetration rate of RWA assets beyond 9%, asset issuers must abandon the 'compliance-system-first' design approach exemplified by BlackRock's BUIDL. Instead, they should adopt underlying architectures that natively support permissionless free circulation.

Currently, $28.56 billion of on-chain RWA assets belong to the permissioned control track. This also means that most current tokenized real-world assets are, in essence, more akin to compliant on-chain traditional financial products, rather than general-purpose collateral assets suitable for open DeFi ecosystems.