Samsung Leverages Technology Cycles, SK Hynix Relies on HBM, What Enabled Micron to Win a Trillion-Dollar Market Cap?

Micron Technology, the Idaho-based memory chip maker, recently saw its market cap surpass $1 trillion, securing its position as one of the top three DRAM manufacturers alongside Samsung and SK Hynix. Its survival and growth story is marked by a unique combination of political maneuvering and hard-won manufacturing efficiency, but also strategic missteps that now challenge its future.

Founded in 1978 in Boise without significant government or capital backing, Micron repeatedly turned to Washington for survival during critical junctures. In the 1980s, it filed anti-dumping complaints against Japanese firms, leading to the U.S.-Japan Semiconductor Agreement. Ironically, this created an opening for Samsung, which Micron had earlier licensed its 64K DRAM technology to. In 2002, Micron avoided heavy fines in a price-fixing investigation by acting as a whistleblower against its competitors, cementing its reputation as a "political opportunist."

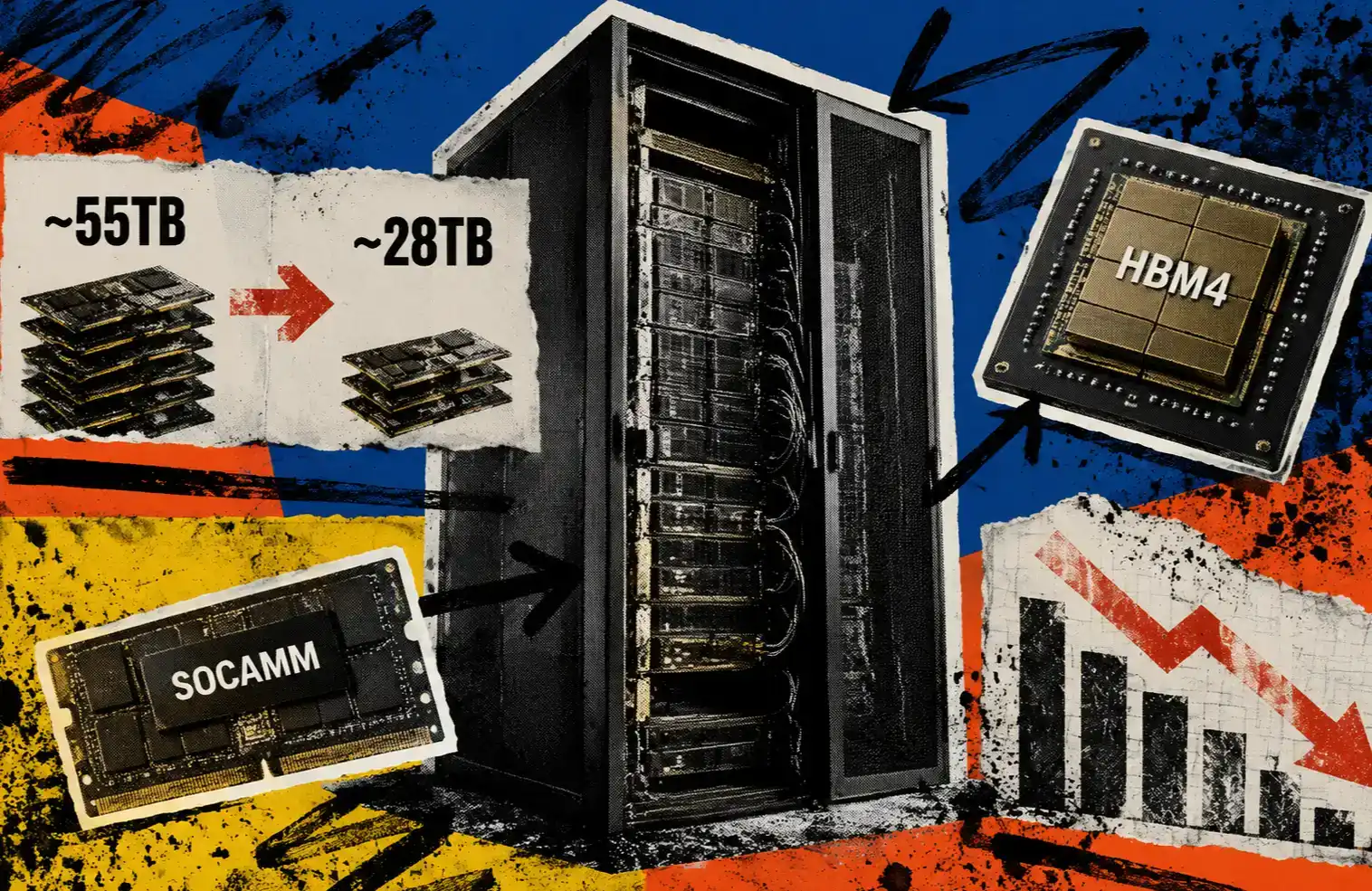

A major strategic error occurred in 2013 with its $2.5 billion acquisition of bankrupt Japanese firm Elpida. This deal burdened Micron with integrating incompatible manufacturing processes just as the industry was pivoting toward HBM (High Bandwidth Memory), a critical technology for AI. SK Hynix had launched its first HBM chip that same year. By the time AI demand exploded with ChatGPT in 2022, SK Hynix commanded about 85% of the HBM3 market, while Micron, playing catch-up, held only around 3%.

In 2017, Micron employed similar tactics against a new competitor, Chinese startup Fujian Jinhua, by alleging intellectual property theft, which led to U.S. sanctions effectively crippling the firm. However, this strategy backfired in 2023 when China banned Micron's products from its critical infrastructure, causing its revenue share from China to plummet from 14% in FY2023 to just 7.1% by FY2025.

Today, Micron faces a triple squeeze: it lags in the high-margin HBM race, faces pricing pressure in low-end DRAM from Chinese manufacturers like CXMT, and has lost crucial access to the booming Chinese AI server market.

Despite its political strategies, Micron's core strength is its exceptional manufacturing cost control, achieved through decades of engineering. Its DRAM chips have a smaller cell area than its rivals, yielding more chips per wafer. This efficiency has been vital for weathering industry downturns. However, this advantage cannot compensate for the decade lost in HBM development.

Micron is now racing to ramp up production of its HBM3E, certified by NVIDIA, and develop HBM4. Its future hinges on whether it can close this technological "time debt" through relentless R&D and execution, in a marathon where its competitors, having started earlier, are not slowing down.

marsbit05/28 07:28