Author: a16z New Media

Compiled by: Deep Tide TechFlow

Deep Tide Intro: This week's a16z Chart covers four topics: Super platforms recorded unusually high 'Other Income' from private investments in Q1; AI-generated eBooks are flooding the market, but the volume of quality content is also growing; Employment in Filipino call centers is rising against the trend, as voice AI costs still haven't caught up with human labor; Mobile AI app downloads, revenue, and usage time have all doubled, with Codex's single-day installs surpassing Claude Code. Four charts, four counter-intuitive signals.

'Other Income': The VC Business of Tech Giants

Profit growth in the public markets is already exaggerated, and Wall Street expects it to be even higher this year.

But beneath the profit figures lies an uncommon detail: not all of the super platforms' income comes from their main businesses. In Q1, 'Other Income' accounted for a surprisingly large portion of net profit.

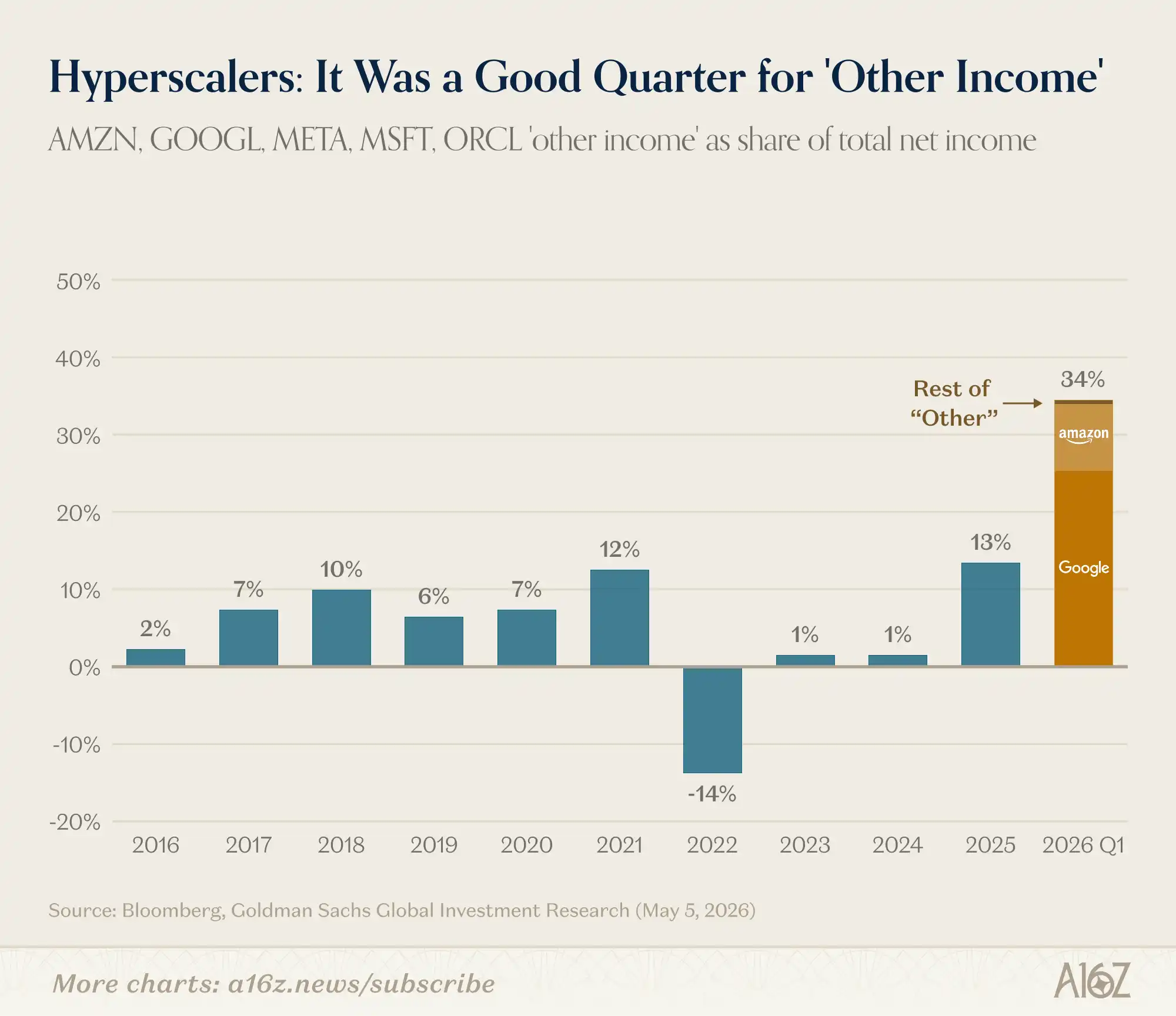

Chart Note: Super platforms' 'Other Income' as a percentage of net profit, exceeding one-third in Q1, historically around 5%-10%.

In Q1, 'Other Income' accounted for over one-third of net profit, historically this figure has been around 5% to 10%.

Where does this money come from? Primarily from private investment returns of Amazon and Google, totaling about $53 billion. Alphabet's CFO stated on the earnings call that 'other income and expense was $37.7 billion, primarily from unrealized gains on non-marketable equity investments'; Amazon disclosed a $15.6 billion net gain from its Anthropic investment in its 10-Q.

In a nutshell: Super platforms are doing pretty well as venture capitalists.

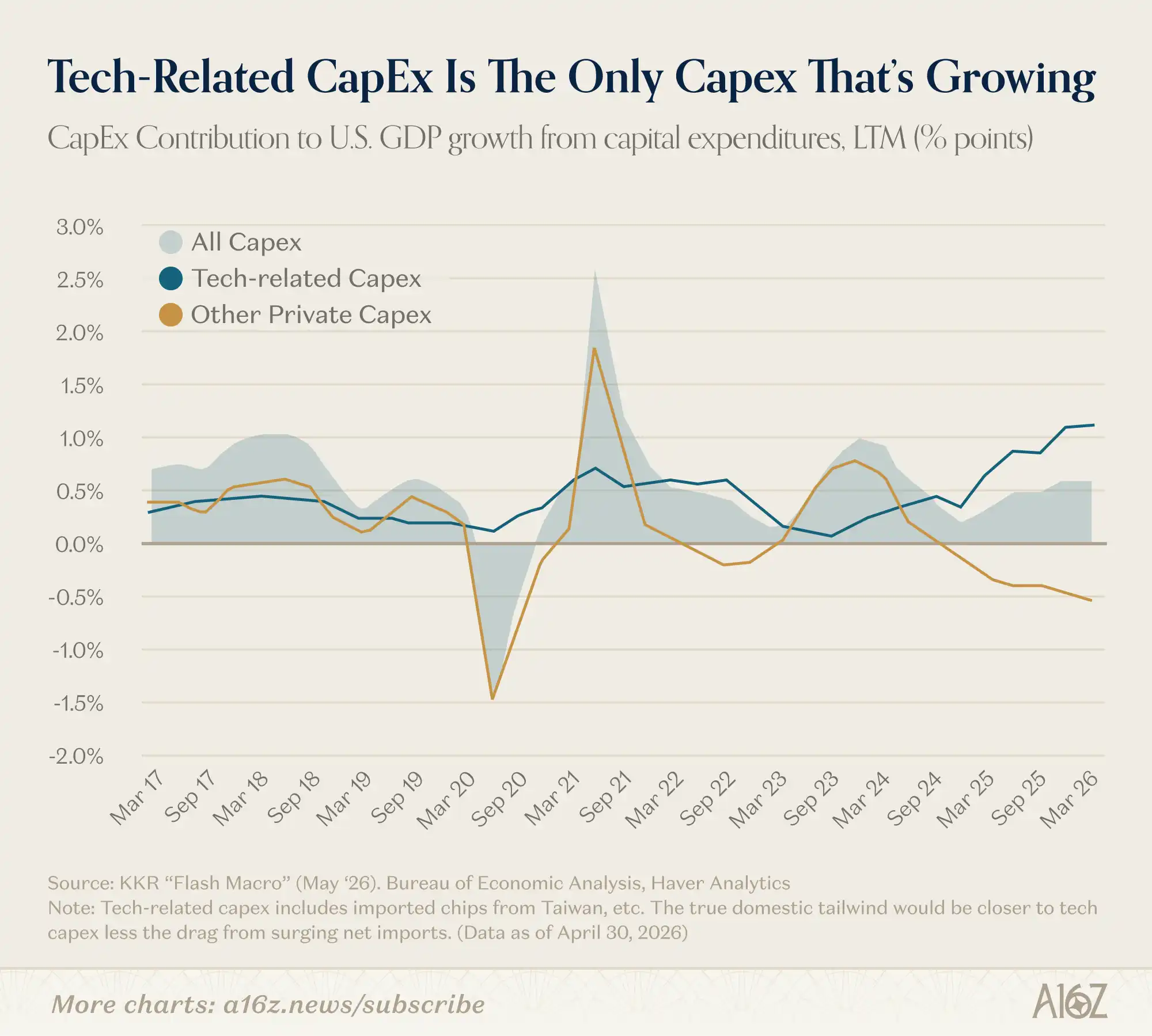

But tech investing is no longer just a game for giants. KKR estimates show that tech-related capital expenditure is currently the only category of capital expenditure driving GDP growth:

Chart Note: Of the 2% growth in US GDP in Q1, tech capital expenditure contributed 1.9%, accounting for almost all of it.

US GDP grew by 2% in Q1, with tech capital expenditure contributing 1.9%. Meaning, without tech investment, GDP would have basically stagnated.

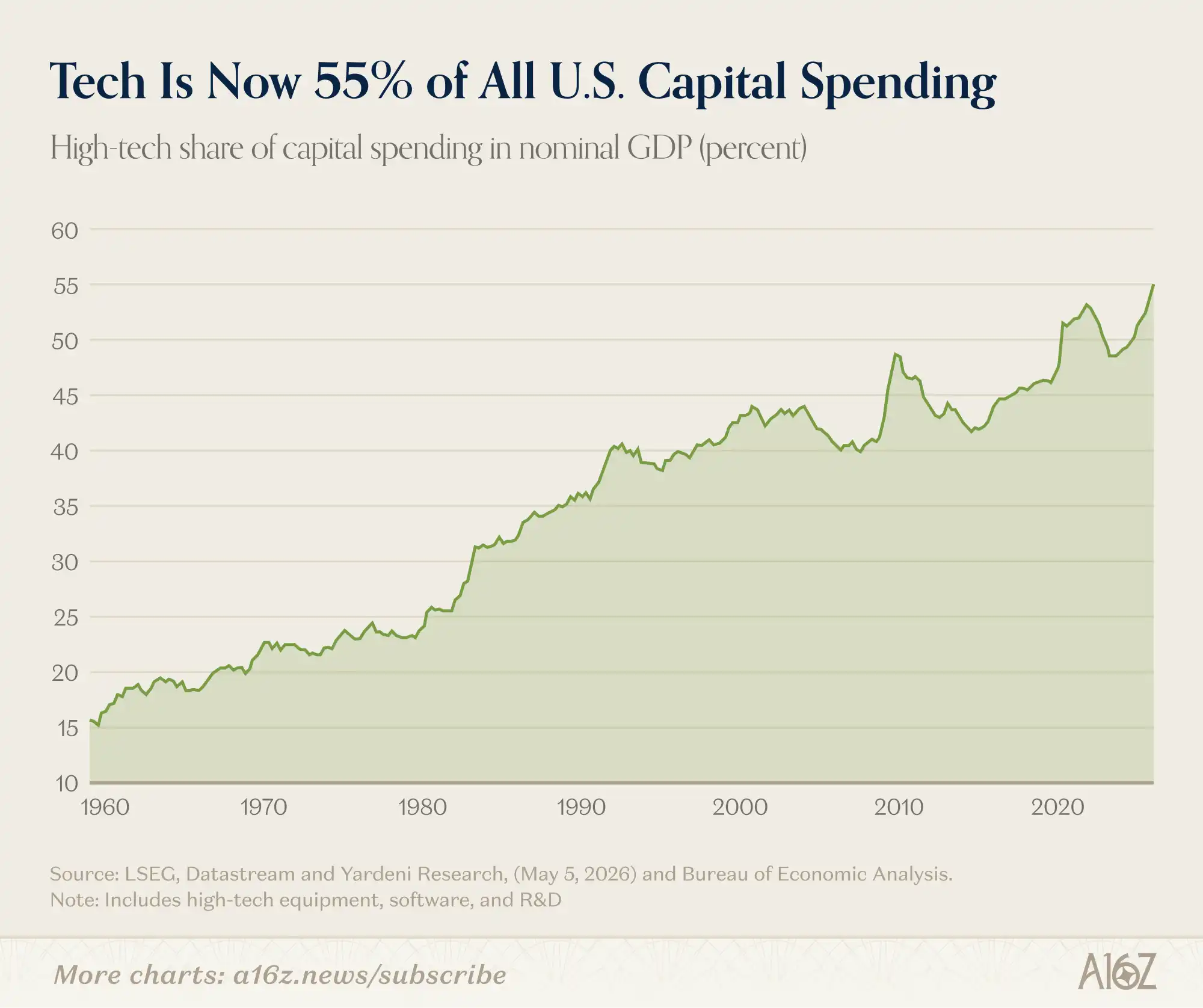

Taking a broader perspective, according to the Bureau of Economic Analysis (BEA) statistics on total business capital expenditure (including R&D and software), tech now accounts for 55% of all US business investment:

Chart Note: The share of technology in total US business capital expenditure has been climbing steadily and now stands at 55%.

This proportion has been climbing for a long time, and AI might accelerate this trend. Yardeni Research proposes an interesting framework: economics textbooks list three factors of production—land, labor, and capital. Now a fourth should be added: data. AI makes data more useful, and the more useful data becomes, the greater the demand for tools to invest in and process data.

Amazon and Google doing well as VCs is one thing. The bigger reality is: everyone is a tech investor now.

AI Junk Books Are Flooding the Market, But Quality Content Is Also Increasing

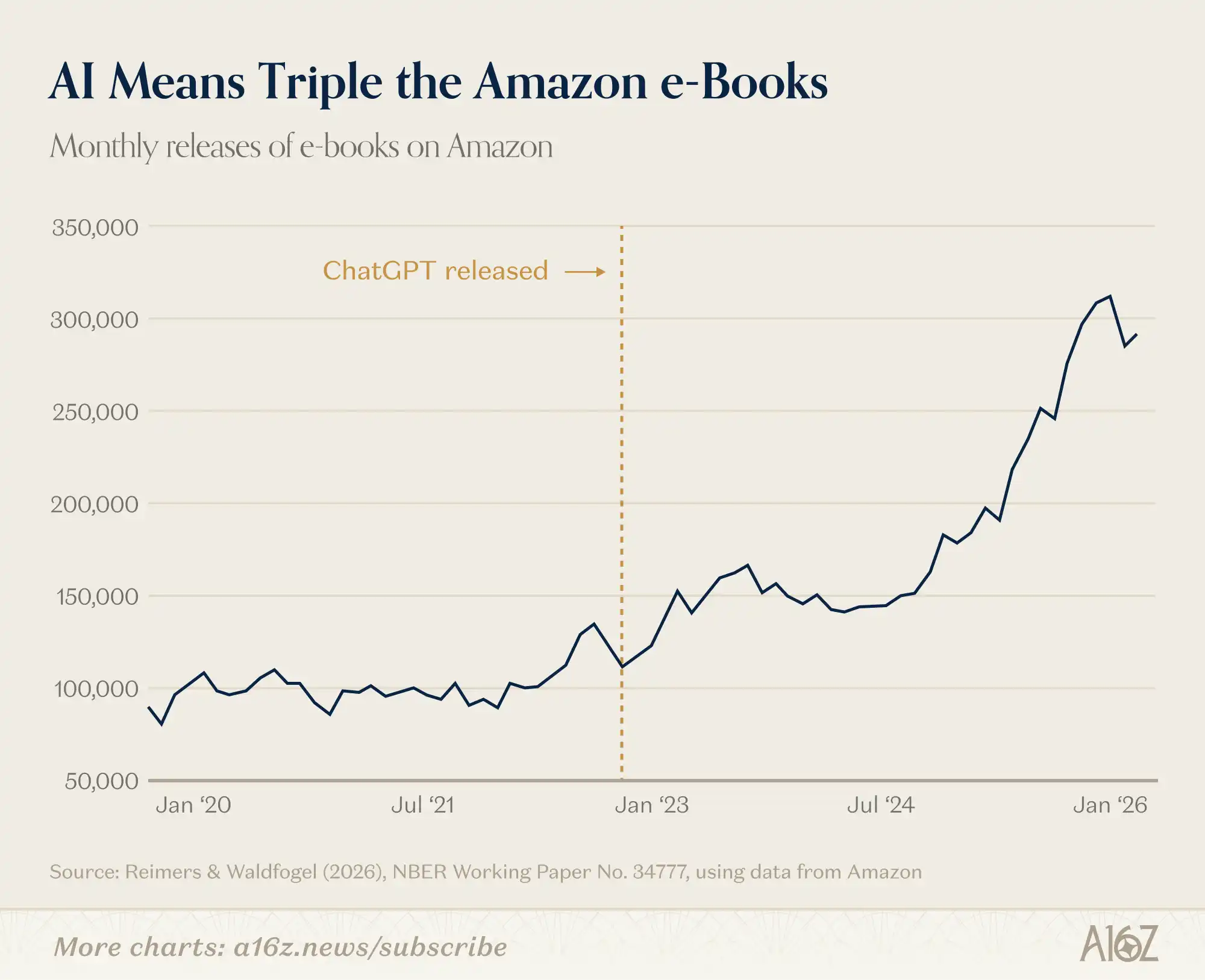

Good news: There are far more eBooks on Amazon than before. Bad news: The increase is mostly AI-generated junk.

Chart Note: Monthly eBook releases on Amazon have tripled since ChatGPT's launch, exceeding 300,000 per month by late 2025.

Since ChatGPT's launch, monthly eBook releases on Amazon have increased from about 100,000 to over 300,000.

There are two ways to read this chart.

The first is intuitive: AI arrived, a tsunami of junk content followed, and Amazon is flooded with machine-generated low-quality books.

The second is more thought-provoking: Junk has indeed increased, but there are also more 'decent' books than before. A recent NBER paper by professors from Cornell and Minnesota quantified this—using a nested Logit demand model, they estimated the 2025 eBook selection set provided about 7% more consumer surplus compared to a counterfactual baseline of purely human creation. Readers in 2023 gained almost nothing, but by 2025, the gains were perceptible.

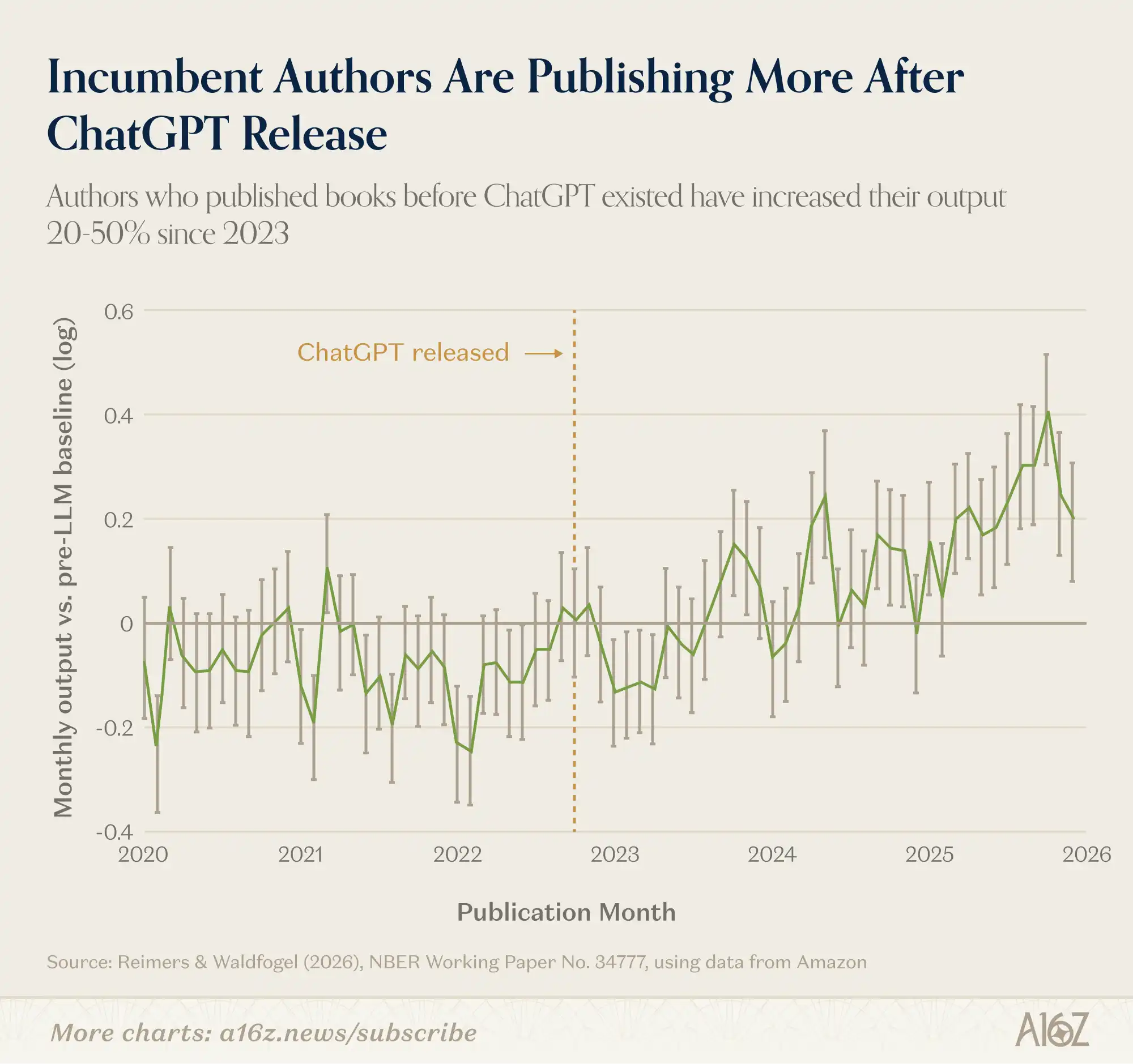

Another finding is even more interesting: AI helps 'old authors' (those publishing before LLMs) the most.

Chart Note: After 2023, output by 'old authors' (those published before LLMs) increased significantly; AI boosted their productivity.

AI didn't just create a bunch of robot authors; it also made human authors more productive.

Marc Andreessen predicted years ago on David Perell's podcast: writing is becoming too easy, so low-quality content will flood the market; but at the same time, with tools this powerful, high-quality content should also experience explosive growth. The junk is real, but the surplus value is also real. Good writers are now writing more.

Call Centers Aren't Dead, Voice AI Is Still Too Expensive

David George just wrote an article arguing that AI replacing jobs is a myth. He distinguishes between 'substitution' and 'augmentation'—customer service is the prime candidate for substitution; AI can answer all questions and has infinite patience.

The logic is sound. But the data doesn't agree.

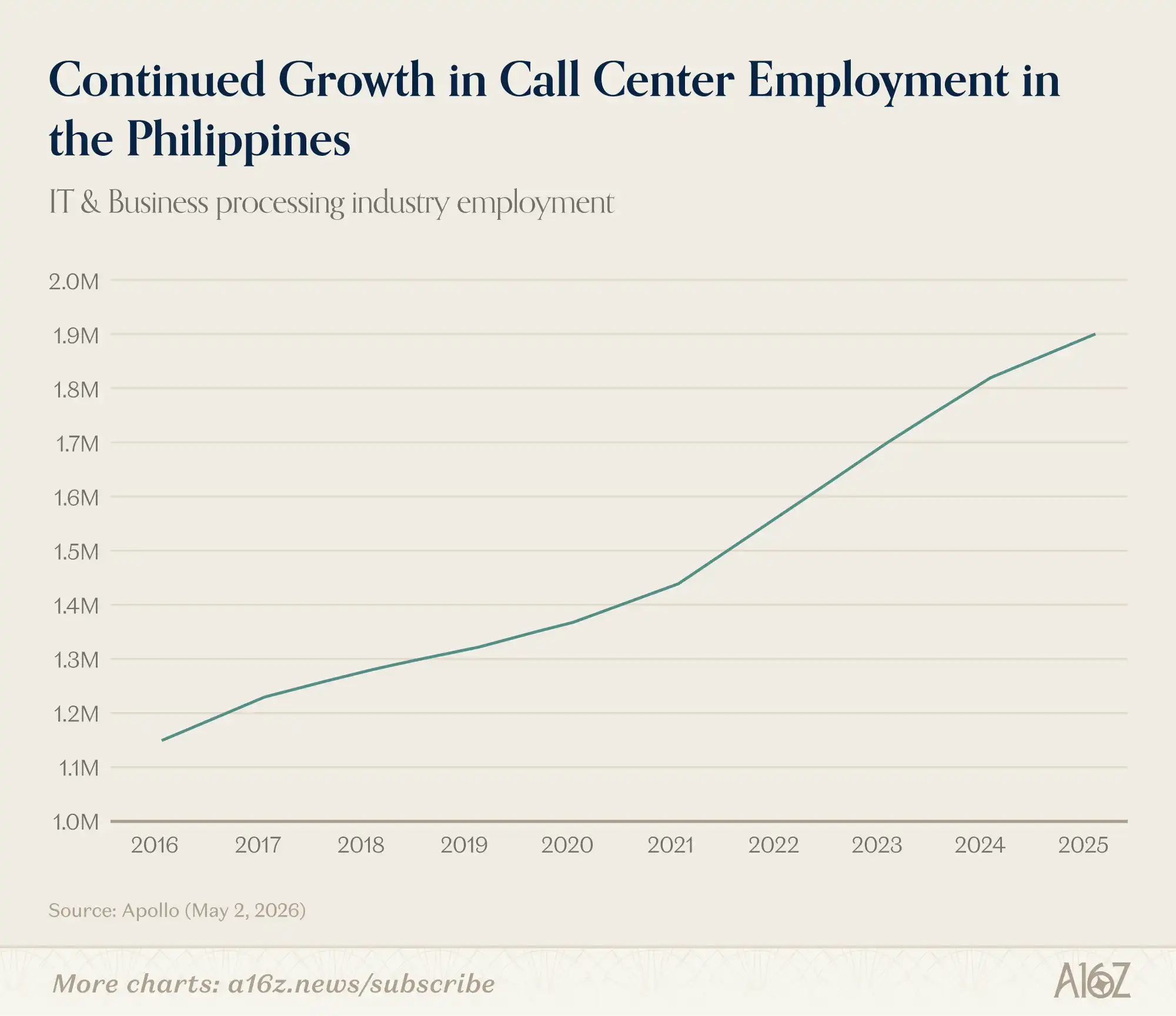

Chart Note: Employment in the Philippines IT and business process outsourcing industry grew from 1.15 million in 2016 to 1.9 million in 2025, spanning every major AI capability leap.

The Philippines is the call center capital of the world. Apollo data shows employment in the IT and business process outsourcing industry grew from 1.15 million in 2016 to 1.9 million in 2025—spanning every major AI upgrade. The industry association projects an additional 70,000 jobs in 2026, a 3.7% year-on-year increase.

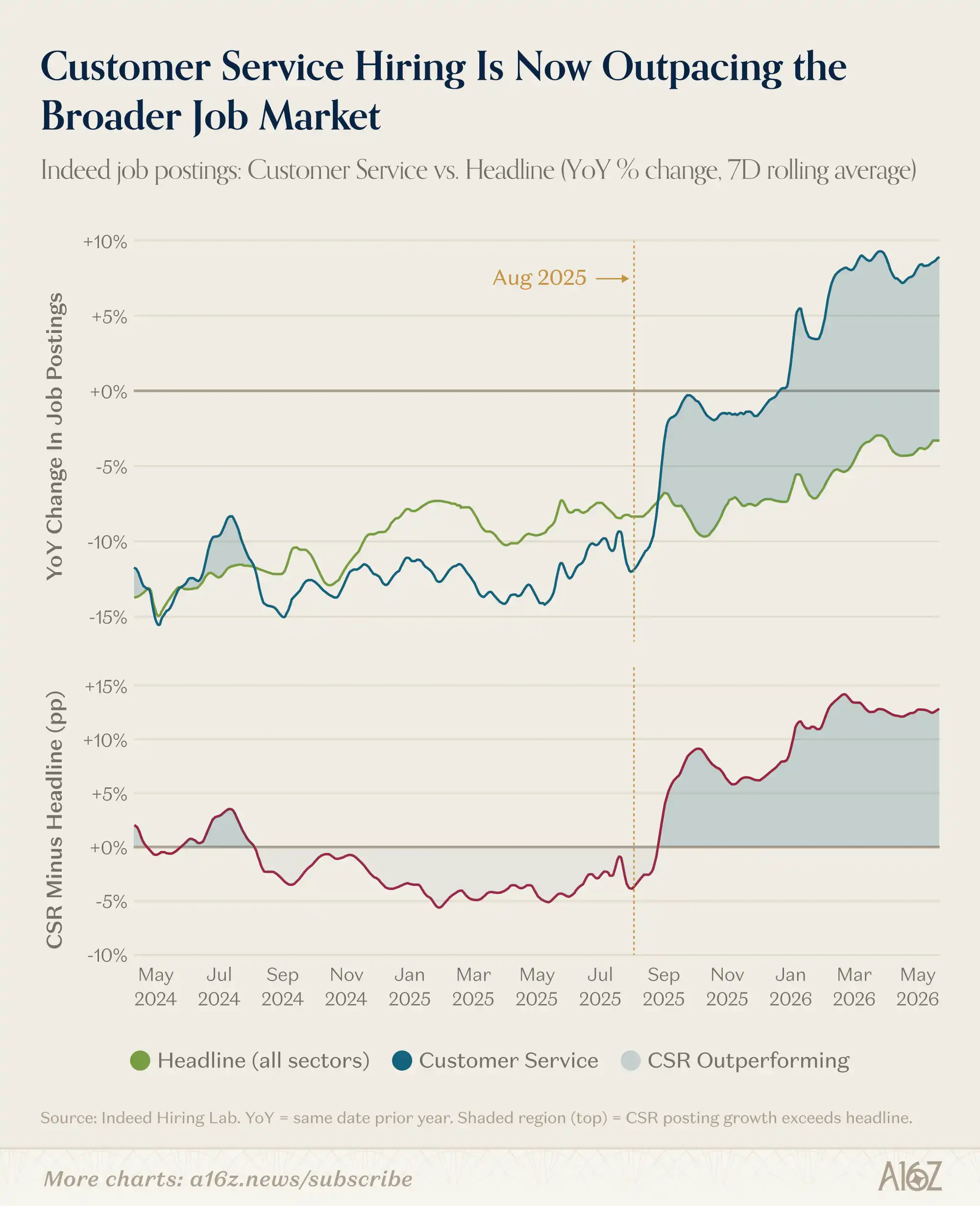

The situation in the US is similar. Indeed data shows that customer service job postings haven't decreased; they're actually outperforming the broader market:

Chart Note: Indeed data shows customer service job postings' year-on-year growth rate is about 10 percentage points higher than overall hiring; the flip happened in August 2025.

The year-on-year growth rate for customer service hiring is about 10 percentage points higher than the overall job market. And this flip only happened recently, in August 2025.

Does this mean AI is actually a boon for the customer service industry? Probably not.

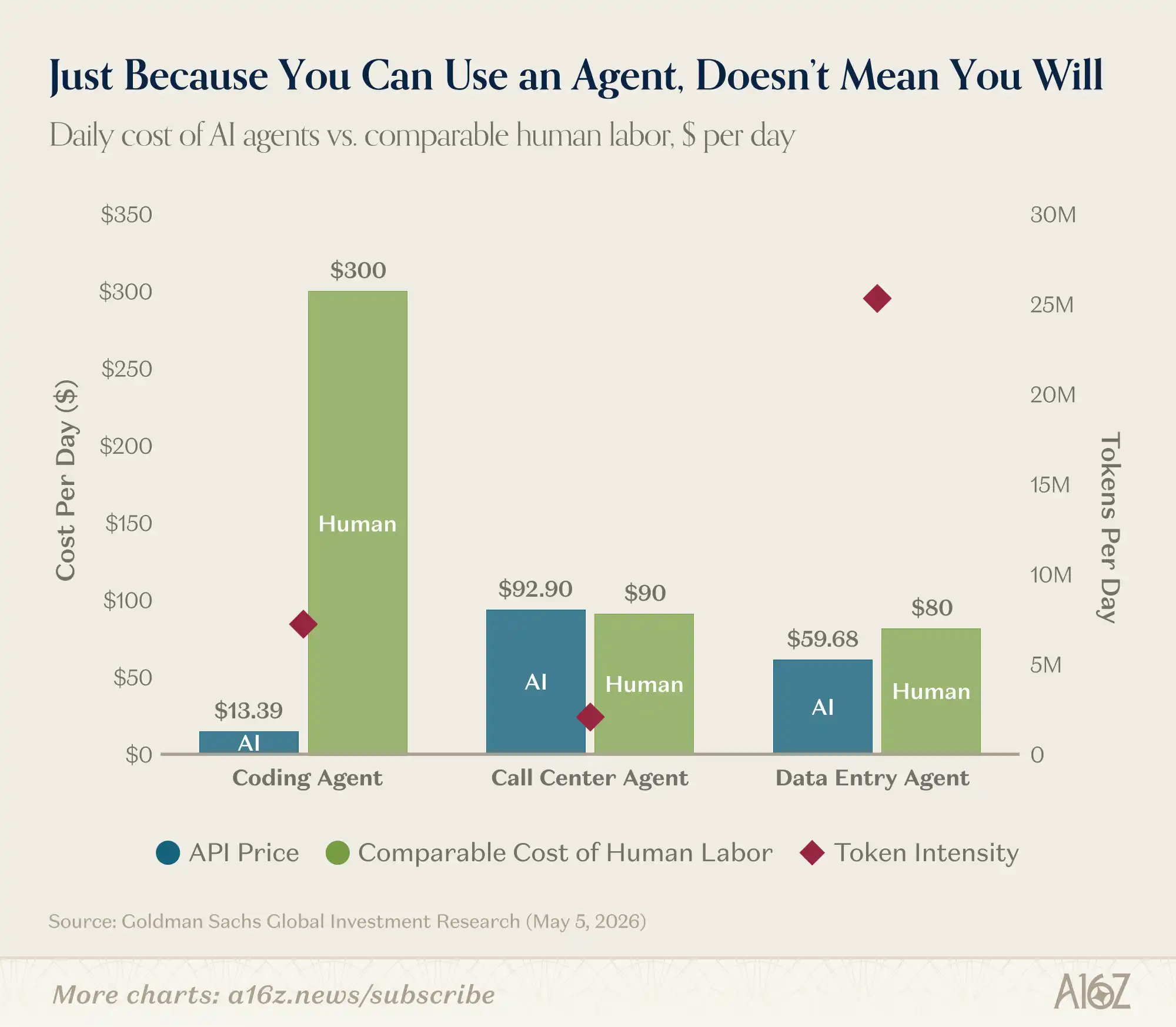

The core reason is cost. Text LLM output is cheap, but voice AI is still expensive. Goldman Sachs conducted an internal test comparing the total cost of AI customer service agents versus human agents:

Chart Note: Goldman Sachs estimates the all-in cost of an AI agent is about $92/day, vs. a human agent at about $90/day, roughly equal.

The all-in cost for an AI agent is about $92/day, versus about $90/day for a human agent. Roughly equal. Compare this to coding agents—pure text output, costs are orders of magnitude lower than human labor. The difference between code and customer service is that the potential demand for code far exceeds that for customer service, so the leverage from cost reductions is completely different.

The Klarna story is the best footnote. In early 2024, Klarna announced replacing 700 customer service agents with AI, with the CEO saying AI was doing everyone's job. This became a benchmark case for 'AI replacing humans.' By May 2025, the CEO backtracked, starting to rehire—service quality declined, and users received cookie-cutter responses.

This situation won't last forever. API costs are falling rapidly, companies like Decagon are growing fast, and the cost comparison might look completely different in 18 months.

Great AI Products Explode Rapidly

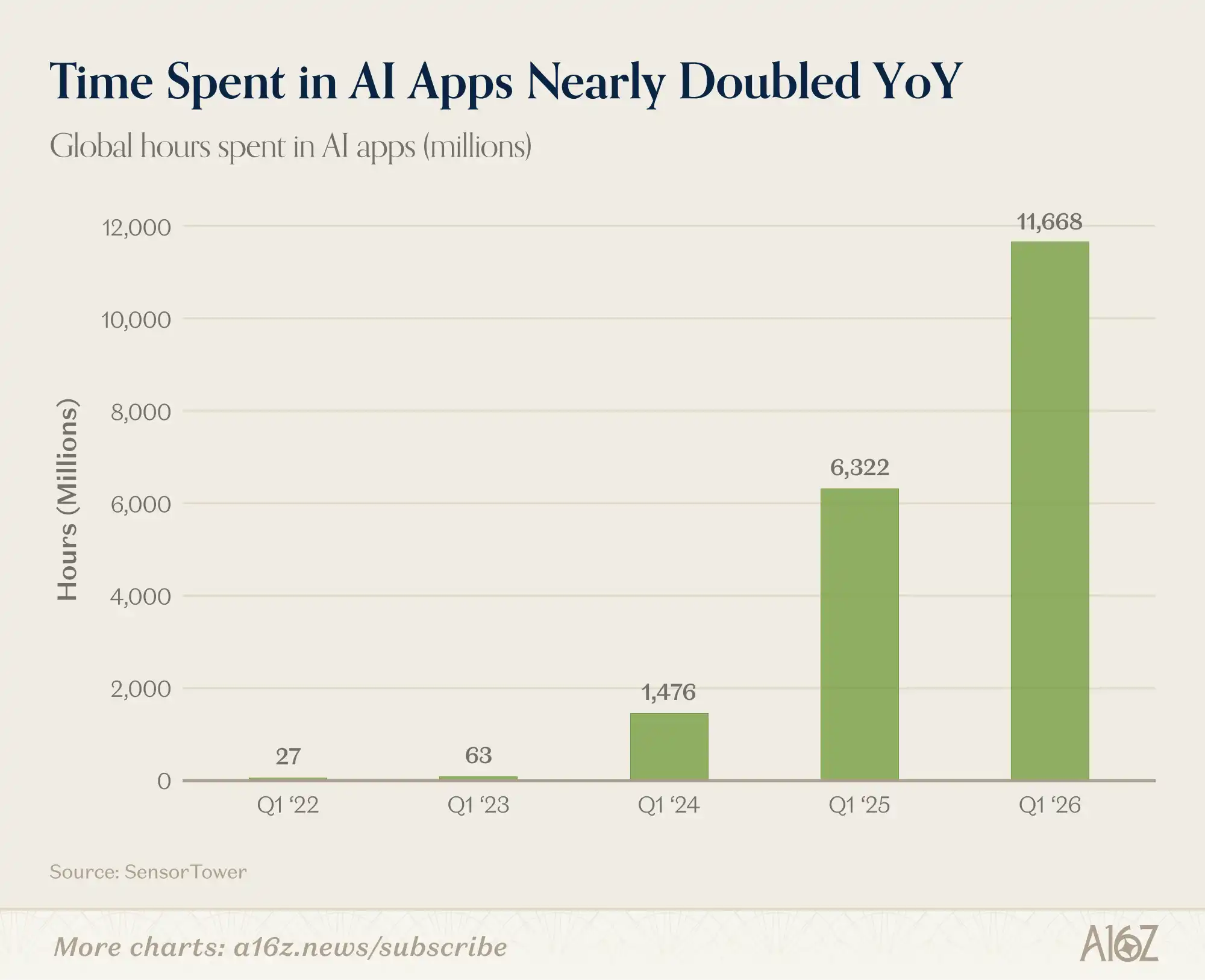

The penetration speed of AI on mobile is astonishing:

Chart Note: Q1 data for AI app mobile downloads, revenue, and usage time.

Chart Note: Monetization and usage time for AI apps nearly doubled year-on-year in Q1.

Downloads, monetization, and usage time all turned upward in Q1, with monetization and usage time nearly doubling year-on-year.

Maybe people are spending less time on social media because they're vibe coding with AI on their phones? Not necessarily a bad thing.

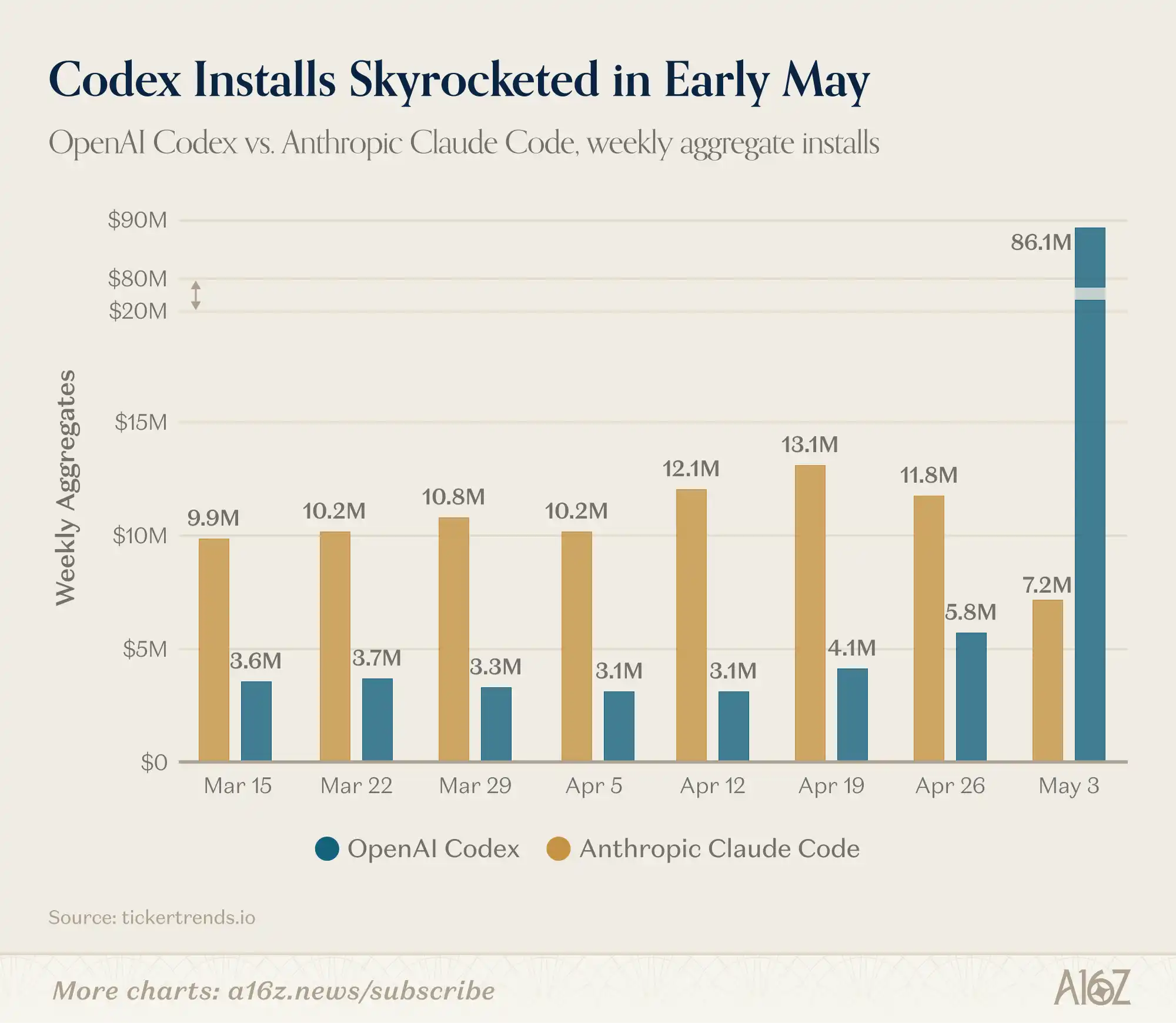

Speaking of vibe coding, a new contender has arrived:

Chart Note: Codex's daily installs surged in May, exceeding Claude Code in a single day—the latter had been the king of code tools for the past year.

Codex's daily installs surged in May, surpassing Claude Code in a single day. Of course, this is just single-day data, and the base is lower, but it illustrates a point: great products spread extremely fast.

Jeff Bezos said something in 2012: You used to be able to sell a mediocre product with marketing, but that's getting harder and harder. A great product will get users to spread the word for you.

In the AI field, this logic is taken to the extreme. Signals propagate quickly, users are highly willing to switch, and no one feels loyalty to a platform or model.

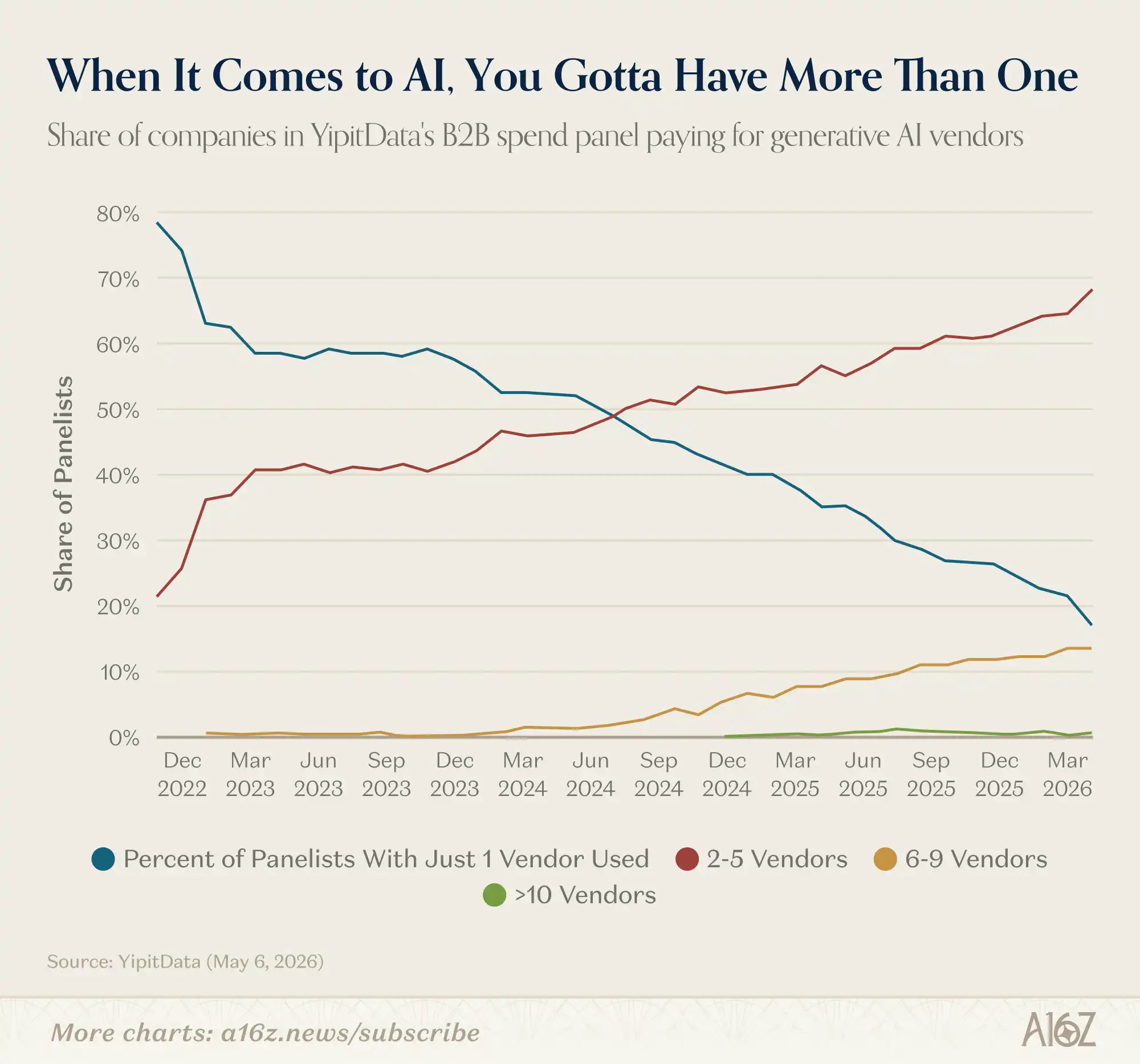

The same holds true in the B2B realm:

Chart Note: YipitData shows the proportion of enterprises using 2-5 and 6-9 AI vendors is rising steadily, with less than 20% using just one.

The proportion of enterprises using multiple AI vendors continues to rise, with those using just one now below 20%. The B2B AI market has no winner-take-all dynamics, for now.