Editor's Note: The core judgment of this article is straightforward: the flow of capital itself is the moat. Looking back through business history, many of the most powerful companies didn't win by simply selling products; they positioned themselves in the middle of a "value flow," continuously taking a cut from every shipment, payment, transaction, ad conversion, compute call, or order flow. Railroads made money from the movement of goods, Visa charged fees from the payment network, Google and Meta captured the entry point where attention converts into commercial transactions, and AWS positioned itself at the center of compute flow. As long as value continues to flow through the network, the network itself becomes stronger.

Crypto natively gives this model to startups for the first time. Blockchains provide open ledgers and programmable settlement, stablecoins allow capital to flow globally at internet speed, and token mechanisms align users, developers, and network growth. For Crypto entrepreneurs, the real opportunity isn't just building a new application, but finding the most expensive, inefficient, and profit-extracting value channels in the old system, compressing them, reconstructing them, and positioning themselves in the new capital flow.

The article emphasizes that the most profit-extracting and inefficient parts of traditional financial services—payments, custody, lending, forex, clearing, market making, etc.—will become entry points for crypto entrepreneurs to reconstruct: compressing costs, increasing speed, and redistributing value. This type of "capital flow business" (taking a revenue share based on volume in the value flow channel) will not stop at finance; it could extend to future markets like GPU markets, AI training data, energy, robotics, space, and rare earth metals.

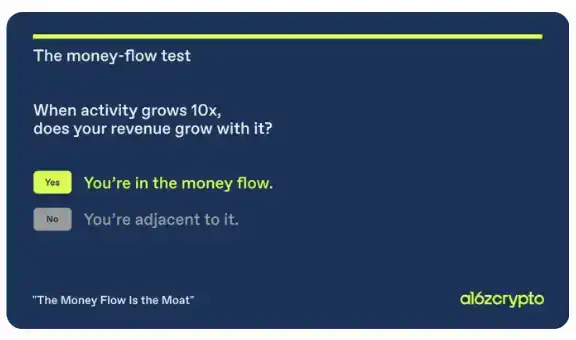

For founders, the most crucial questions are: Is your product already positioned in a value flow? When network activity scales 10x, does your revenue scale proportionally? Opportunities often hide where old infrastructure is least efficient but profit extraction is highest. Whoever compresses old costs and positions themselves in the new flow has the chance to turn the capital flow into their own moat.

Here is the original text:

Many of history's greatest businesses have been built by putting themselves in the "flow of capital"—they facilitate the creation and transfer of value in a network and take a portion of it. The more value that flows through the network, the larger such businesses tend to grow.

Crypto is the first modern technology that is native to this. If your startup isn't designing its product and business model around these principles, you're missing the opportunity. Especially with stablecoins, capital and value can now flow at internet speed: global settlement, running 24/7, with end-to-end programmability. The underlying rails are open, the unit economics are public, and the addressable market for capital flows is nearly every dollar moving globally.

This Model

Blockchains are network businesses by nature. Every transaction settles on a shared ledger; every new participant reinforces the same underlying infrastructure that later participants can use. As more people use and build on it, the network becomes more valuable for all its users.

Most companies spend years artificially manufacturing network effects on top of traditional infrastructure. Crypto entrepreneurs inherit this network effect from day one.

Network tokens amplify this further. A well-designed token can align users, developers, suppliers, validators, and the protocol itself to the same goal: growing the network and distributing rewards based on each participant's contribution. Protocol revenue belongs to the people actually using it. No co-op rebates, no side deals, just a positive feedback loop: value flows through the system while also flowing back to those who build and drive its growth.

This isn't a new model. Crypto just makes it easier and at a larger scale for startups to use it.

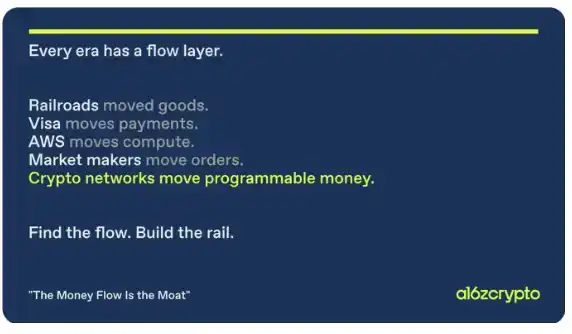

Railroads didn't make money selling locomotives; they made money on every ton of grain, coal, and steel that moved over their tracks. Standard Oil, U.S. Steel, and AT&T were companies in the flow of capital. Google and Meta didn't replace print and TV because the ads were better; they captured the crucial node where attention converts into commerce, taking a cut from trillions in commercial intent. AWS positioned itself at the center of compute flow.

The model is consistent: Find where value flows, then put yourself in the middle.

Financial markets make this pattern even clearer. Visa processed $15.7 trillion in payment volume in fiscal 2024, recording $35.9 billion in net revenue. Jane Street had $20.5 billion in net trading revenue last year, surpassing Citi and Bank of America. The top five U.S. market makers handle 87% of payment for order flow: they aren't predicting the market; they're in the middle of every order flow, earning more as trading volume grows.

These businesses share another trait: network effects. Visa becomes more useful to merchants as more cards are issued; more useful to cardholders as more merchants accept Visa. The same with order flow: each added broker narrows spreads, attracting more brokers, which attracts more order flow.

Capital flow plus network effects is one of the most durable structures in business history.

Your Margin is My Opportunity

Jeff Bezos once said, "Your margin is my opportunity." He was talking about retail, but it applies even more to traditional financial services—the world's largest pool of profit extraction. Payments, custody, lending, forex, securitization, settlement, market making—it's all true. Visa and Mastercard charge 2% to 3% interchange on a network designed in the 1960s; cross-border remittance corridors charge 6% to 9%; prime brokers and custodians take a cut of every securities transaction. Even with the U.S. moving to T+1 settlement in 2024, capital still sits idle overnight, a structural cost borne by all participants.

These profit margins are targets. Compress costs, increase velocity, and potentially expand the entire market. Stripe and Square have proven this in payments.

Crypto entrepreneurs have the chance to build the next version: programmable, instant, global, and natively in the flow of capital.

And this frontier extends far beyond financial services. Compute and GPU markets, memory chips, AI training data, energy, robotics, space, rare earth metals—each could see massive global flows of value, and existing infrastructure isn't built to handle that scale.

Each is an open market where capital flow businesses can be built on programmable infrastructure from day one. No legacy rails, no entrenched intermediaries, no old profits to defend.

As a founder, you should ask yourself:

1. Are you in the flow of capital today?

2. When activity value on your product grows 10x, does your revenue grow proportionally?

3. If you're building a new product, where in your target market does the highest profit extraction exist relative to the value created?

The opportunity is there. Compress it, step into the new value flow, and let the network compound from there.