Author: Melee

Compiled by: AididiaoJP, Foresight News

In July 2017, Hayden Adams was laid off by his employer Siemens, where he worked as a mechanical engineer. His college roommate Karl Floersch was working at the Ethereum Foundation at the time and often told him about smart contracts. Adams had previously paid no attention. Now unemployed and looking for something to do, he decided to listen.

The Birth of the Automated Market Maker (AMM)

Floersch recommended a blog post by Vitalik Buterin about running an on-chain exchange using a mathematical formula instead of an order book. The principle was not to match buyers and sellers, but to allow traders to exchange with a pool of assets, with the price automatically set based on the ratio of tokens in the pool. No working version existed at the time. Adams took it on as a learning project, received a $65,000 grant from the Ethereum Foundation, and launched Uniswap in November 2018.

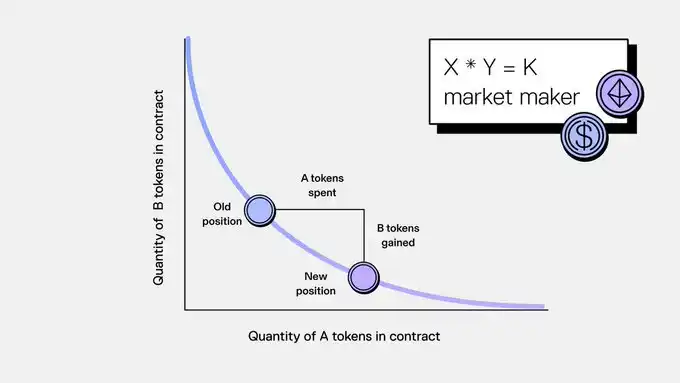

Its formula was deceptively simple: x * y = k.

Two tokens are placed in a pool, and the product of their quantities remains constant. When someone buys one token, they must deposit the other token, changing the ratio within the pool and adjusting the price accordingly. No order book, no matching engine, no professional market makers needed. Anyone can deposit tokens into the pool and earn fees from every transaction.

The automated market maker thus became the cornerstone of decentralized finance. Uniswap, Curve, Balancer, and dozens of other protocols handle billions of dollars in trading volume. On-chain order books are slow and expensive, and traditional market makers have no interest in tokens with only two hundred holders. Automated market makers allow anyone to create a liquid market for any asset at any time. Before AMMs, listing a new asset required permission and infrastructure. After AMMs, all you need is a liquidity pool.

The benefits were obvious. So, prediction markets naturally tried to adopt them too.

Automated Market Makers and Prediction Markets

Prediction markets face the same cold-start problem as token markets. You need liquidity before people are willing to trade, and you need traders before people are willing to provide liquidity. Little known is that Robin Hanson had proposed an automated market making solution for prediction markets years earlier in his 2002 Logarithmic Market Scoring Rule.

He thought he had theoretically solved the cold-start problem. However, in practice, the solution suffered from the same fundamental issue that every subsequent attempt to automate liquidity for prediction markets encountered: the formula couldn't distinguish between perpetually fluctuating tokens and equity certificates that expire.

Prediction market outcomes are binary. They ultimately settle to one or zero. In a token swap pool, both assets can fluctuate indefinitely, and the AMM formula works precisely because neither token is designed to go to zero.

Early Polymarket used an AMM based on the logarithmic market scoring rule. Augur also experimented with similar schemes. If automated liquidity pools worked for token swaps, they should, in theory, work for election betting too.

They didn't.

Why AMMs Fail in Prediction Markets

When a prediction market event settles, one side is worth one dollar, the other zero. For anyone providing liquidity to the pool, the mathematical outcome is nearly brutal. As the market moves towards settlement, the pool automatically rebalances towards the losing side.

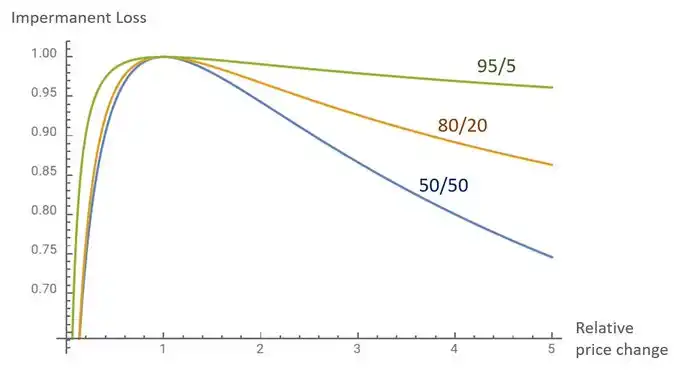

Impermanent Loss

What decentralized finance traders call "impermanent loss" becomes completely "permanent" here. Every market settles, and every pool will eventually hold a pile of worthless shares.

In regular DeFi pools, trading fees can offset impermanent loss over time.

But in prediction markets, the loss is a structural certainty. The only question is how much the liquidity provider loses. Protocols have tried to persuade users to deposit assets into these pools through liquidity mining, reward programs, and various incentive structures. All of these are just different ways to subsidize users to lose money at a slower rate.

Price Discovery

Then there is the issue of price discovery. AMMs price assets based on the pool ratio and a fixed formula. For tokens, the "correct price" is a moving target, and a formula-driven approximation is sufficient. Prediction market prices are supposed to represent probabilities. The slippage introduced by the constant product curve distorts the signal, especially in low-liquidity markets, where a single trade can swing the implied probability by several basis points.

Is the Central Limit Order Book (CLOB) Better Than AMMs?

Polymarket realized this early on. In late 2022, the platform migrated from a logarithmic market scoring rule-based AMM to a central limit order book. AMMs were designed for continuous token swaps across a price range. Prediction markets require precise probability pricing on binary outcomes with known terminal values. They are entirely different problems.

The characteristics that made AMMs revolutionary for tokens—permissionless market creation, instant liquidity bootstrapping, no reliance on professional market makers—are exactly what prediction markets desperately need. The problem is that the specific mechanism, the constant function formula built for token swaps, breaks down when faced with the reality of binary outcomes and inevitable settlement.

The challenge for prediction markets is to replicate these effects with infrastructure that reflects how these markets actually settle.