In this wave of tech IPO frenzy, everyone wants to 'get on board,' including Polymarket.

The soonest SpaceX could list on Nasdaq is in 23 days, an IPO poised to break all records in human IPO history.

OpenAI's last round valuation was $5 trillion, Anthropic is rumored to be worth $4 trillion, and SpaceX $17.5 trillion. Globally, there are 1,600 unicorn companies with a cumulative valuation of $5 trillion. The returns from this sector have historically been available only to institutions and accredited investors. Directly buying shares in these companies requires a six-figure minimum, a one-year lock-up period, accredited investor certification, and a network of connections. Ordinary people have no access.

Furthermore, private companies are not obligated to disclose their valuations. Funding round valuations are lagging, secondary market quotes are scattered, and the actual transaction prices of employee stock are highly sensitive internal information. This, precisely, is the perfect entry point for prediction markets.

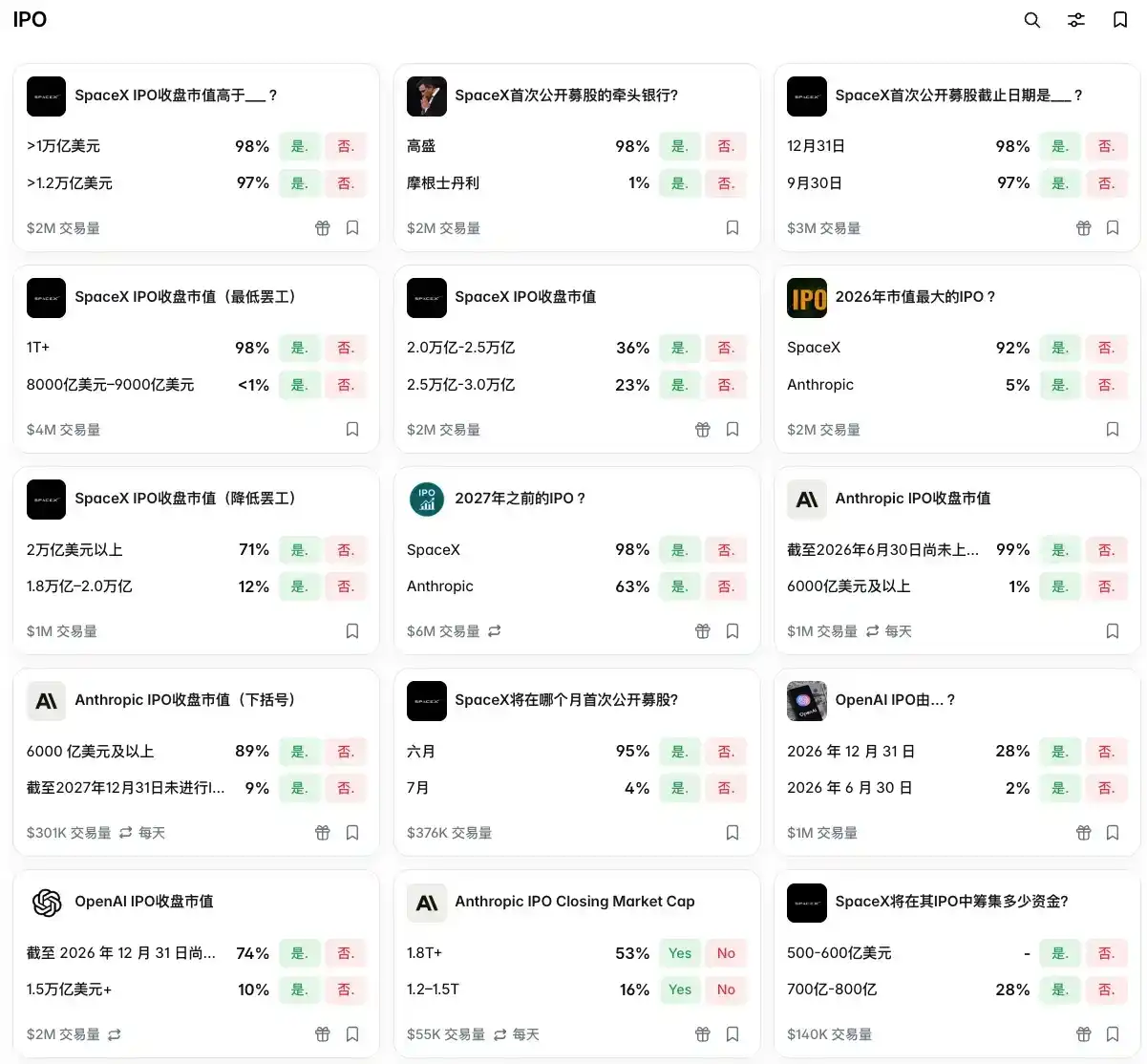

On May 19th, just before this critical timing, Polymarket announced an exclusive partnership with NASDAQ, launching a batch of prediction contracts targeting the market valuations of pre-IPO companies. Users can bet on whether OpenAI's valuation will break through $10 trillion by year-end, whether Anthropic will reach $11 trillion by December 31st, and if SpaceX can touch $15 trillion before June 30th. NASDAQ, as the data source, is responsible for the final settlement of the contracts.

Polymarket previously had a market on OpenAI's closing market cap on its first day. Bloomberg reported that it accumulated $1.6 million in trading volume since last September. On Kalshi, existing IPO contracts are even more concentrated: Cerebras Systems' probability of an IPO before 2027 is priced at 95%, Kraken at 83%, Databricks at 70%, Discord at 70%. OpenAI and Anthropic also have contracts.

Both competing platforms are placing significant emphasis on this wave of pre-IPO frenzy.

Polymarket's Comeback Fight

Over the past eight months, Polymarket has been surpassed by Kalshi on nearly every visible metric.

In April, Kalshi's monthly trading volume was $14.8 billion, a 13% increase month-over-month. Polymarket's global volume plus the US App volume totaled $10.2 billion, a month-over-month decline of 8.9%. Active traders dropped from 733,000 in March to 643,000 in April, a 12% decrease. In valuation, Kalshi's latest round is $22 billion, while Polymarket is reportedly in talks for $15 billion.

A Bank of America report in April noted that among US-based prediction markets, Kalshi has captured approximately 89% of the market share.

Kalshi's journey over the past few years has been smoother than Polymarket's. In 2020, the CFTC granted it a Designated Contract Market (DCM) license, the first in the US and still the only one specifically issued to an event contract platform. This means Kalshi can accept USD, issue 1099 tax forms, integrate SDKs with platforms like Robinhood, and have its probability data cited by CNN and CNBC. In February of this year, Kalshi was selected by TIME for its TIME100 Most Influential Companies list, and its App Store ranking once approached that of ChatGPT.

Polymarket, fined $1.4 million by the CFTC in 2022, withdrew from the US market. It wasn't until July 2025 that the CFTC and the Department of Justice concluded a new round of investigations against it, allowing it to acquire a compliant trading license through the acquisition of QCEX.

However, Polymarket's partnership with NASDAQ this time is likely a signal of a counteroffensive.

The specific partner for Polymarket is Nasdaq Private Market (referred to as NPM), a company incubated by NASDAQ that specializes in serving private companies. Its main businesses are two-fold:

First, organizing secondary market liquidity programs for employee stock. Employees of companies like OpenAI, SpaceX, and Anthropic hold a large number of options or restricted stock units. Since the companies are not public, they cannot sell on the open market. NPM helps companies organize tender offers, allowing employees to sell their shares to approved external investors. NPM itself has disclosed facilitating nearly $80 billion in such transactions, covering over 1,000 company-sponsored liquidity programs and serving more than 200,000 employee shareholders.

Second, building a valuation database for private companies. NPM daily sees the transaction prices of employee stock for companies like OpenAI, Anthropic, and SpaceX on the secondary market. This data was previously sold only to institutional clients for a hefty annual fee.

The key step in this partnership is NPM's agreement to, for the first time, provide these valuation data to Polymarket for use.

Rodolfo Sanchez, NPM's Data Vice President, made a crucial statement in the press release: "The data flows in both directions." NPM provides data to Polymarket for contract settlement, while Polymarket's contract price curves become, in turn, "institutional signals" available to NPM's clients. Institutional clients buying NPM data also receive a probability curve priced in real-time by hundreds of thousands of retail traders.

Selling Data, Seizing Authority, Capturing Retail

This is not Polymarket's first time selling its data.

In October 2025, ICE announced an investment of up to $2 billion at an $8 billion pre-money valuation. The significance of this deal wasn't just the valuation, but the terms. ICE secured global exclusive distribution rights for Polymarket's data. The sales channels of the parent company of NYSE began selling Polymarket's probability data to global institutional clients.

In January 2026, an exclusive partnership with Dow Jones. Polymarket's prediction data was integrated into The Wall Street Journal, Barron's, MarketWatch, and Investor's Business Daily. The financial media matrix under News Corp began embedding Polymarket's probability signals as standard modules in their layouts, similar to the Dow Jones Index or VIX.

In February 2026, ICE formally launched the 'Polymarket Signals and Sentiment' product. Real-time quotes from thousands of contracts on Polymarket were standardized into structured data streams and distributed to institutional clients via the ICE Consolidated Feed, flowing through the same pipeline as NYSE stock data, bond prices, and corporate announcements. ICE President Ben Jackson mentioned this product alongside Reddit and Dow Jones in the Q1 earnings call, calling it one of the three pillars of ICE's alternative data services.

And this new partnership is about seizing the authority to determine valuations in this year's hottest private market.

We speculate Kalshi won't sit idle; its next move will likely involve partnering with a private market data provider to implement a similar structure. However, mainstream private data providers like Forge and PitchBook have smaller scales and cover fewer companies compared to NPM. NPM has already been exclusively secured by Polymarket. The cost for Kalshi to enter this track will be higher.