Author: Michael Saylor

Compiled by: Deep Tide TechFlow

Deep Tide Insight: MicroStrategy founder Saylor presents a "Digital Asset Stack" theory, positioning Bitcoin as the foundational digital capital layer, upon which are built digital credit, digital currency, digital yield, and digital equity. The core argument is that Bitcoin itself does not require staking, inflation, or protocol changes; its benefits are generated through the capital structures built on top of it. This framework supports the strategy behind STRC and MSTR and serves as a direct response to debates like "should stablecoins pay interest?" and "should Bitcoin emulate Ethereum?"

The Modern Digital Asset Stack

Bitcoin is digital capital.

This is the foundation of the entire modern digital economy.

Bitcoin is scarce, globally liquid, highly tradeable, programmable, divisible, and auditable, accessible to anyone with an internet connection. It is not issued by a government, not controlled by a corporation, has no tenants, no maintenance costs, no borders, no physical address, no board of directors, and no central bank can dilute it.

It is the foundational layer of digital value.

But capital itself is just the starting point.

The next stage for Bitcoin is not merely holding BTC, but building an entire digital capital stack on top of it: Digital Capital, Digital Credit, Digital Currency, Digital Yield, and Digital Equity.

This is how Bitcoin evolves from a single asset into a global financial architecture.

Bitcoin remains Bitcoin. The world builds on top of it.

The Stack Has Five Layers

The modern digital asset stack consists of five layers.

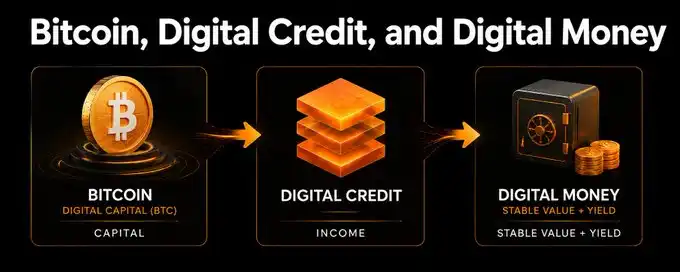

Layer One: Digital Capital, which is BTC—the pure, scarce, high-energy capital asset.

Layer Two: Digital Credit, instruments like STRC, yield-generating instruments backed by Bitcoin, designed to dampen volatility and provide yield.

Layer Three: Digital Currency, a stable-value, interest-bearing instrument. It is pegged to a currency like the US dollar and can take the form of tokens, funds, preferred securities, accounts, or other wrappers, fundamentally a combination of digital credit and fiat cash equivalents.

Layer Four: Digital Yield, leveraged or structured yield products. For investors willing to accept more risk, leverage, volatility, or illiquidity.

Layer Five: Digital Equity, like the residual equity of MSTR. It is the junior tranche that absorbs volatility, supports the entire credit structure, and captures the residual upside.

This is not a protocol change, not staking, not monetary inflation, and not another new token pretending to be Bitcoin. This is capital markets built on Bitcoin.

Layer One: Digital Capital - BTC

At the bottom of the stack is BTC.

BTC is the digital equivalent of gold, landmark real estate, and sovereign reserve assets, but with superior liquidity, divisibility, scarcity, and global settlement capabilities. It is the highest-energy asset in this system.

High energy leads to volatility. Bitcoin can swing dramatically precisely because it is pure digital capital: scarce, liquid, global, and traded 24/7. This volatility is not a bug; it is the raw material for building digital capital markets.

But not every investor can hold raw BTC directly. Family offices want capital appreciation, corporations want treasury reserves, banks want collateral, insurers want yield, retirees want interest, payment companies want stable settlement, crypto exchanges want a dollar-like asset that truly pays interest to users, and savers in emerging markets want dollars, liquidity, and yield.

A 40% volatility asset is perfect for some investors and completely unsuitable for others.

The answer is not to change Bitcoin, but to build products on top of it that match the needs of each type of capital.

Layer Two: Digital Credit - Bitcoin-Backed Yield

Digital Credit transforms high-volatility digital capital into lower-volatility yield.

STRC is an example: a senior, high-yield, short-duration yield instrument issued by a Bitcoin-backed company. BTC provides the long-term capital foundation, Digital Equity absorbs residual volatility, and Digital Credit sits above equity, paying a yield to investors who want income without directly bearing BTC's volatility.

The key is not that Digital Credit always has a fixed, single-digit volatility. It doesn't.

Credit instruments have low volatility in normal markets and higher volatility in stressed markets. Spreads widen, liquidity changes, rates move, issuer perception shifts, and market structures evolve.

A more accurate description is: Digital Credit is designed to dampen the volatility of Digital Capital.

It achieves this through capital structure, seniority, yield, par mechanisms, liquidity support, and a layer of junior equity cushion. The goal is to convert the raw, high-volatility capital energy of BTC into a more stable stream of yield suitable for credit investors.

Finance professionals have long understood this logic. A mortgage is not a house, a municipal bond is not a city, a corporate bond is not common stock, and a preferred security is not the equity beneath it. An asset can be volatile, while the credit layer can be far less so.

The purpose of Digital Credit is not to eliminate risk, but to allocate it intelligently. Equity holders accept residual volatility and upside, credit holders take yield and a more senior claim, and digital currency holders achieve another layer of stability and liquidity. Each investor picks the risk tranche matching their mandate.

Bitcoin itself does not need to generate yield. No staking, no inflation, no protocol changes, no need to become Ethereum. Yield is created by the capital structure on top of Bitcoin, not by degrading Bitcoin.

This distinction is crucial.

Layer Three: Digital Currency - Stable-Value Money Built on Digital Credit

Digital Currency is the next layer.

It is a stable-value, daily redeemable instrument that functions like money while paying a meaningful yield. Depending on jurisdiction, distribution channel, and investor type, it can be structured as a token, fund, preferred security, account, or other regulated wrapper.

The concept is simple: combine Digital Credit with fiat cash equivalents. Digital Credit serves as the yield engine, fiat cash equivalents provide liquidity and stability, the structure itself manages duration, redemptions, credit exposure, reserves, and market risk, and the holder gets a stable-value asset that yields interest.

For example, a product might hold Bitcoin-backed Digital Credit yielding around 10%-12%, combined with Treasury bills, money market funds, repos, or bank reserves. After deducting for liquidity reserves, fees, and risk buffers, the target yield for this Digital Currency instrument might land in the 6%-8% range.

This is the breakthrough. Digital Capital becomes Digital Credit, Digital Credit combined with fiat liquidity becomes Digital Currency.

This is how a Bitcoin-backed, stable-value instrument can pay interest. It's not magic; it's structured finance.

BTC is the capital asset, Digital Equity is the first-loss and upside layer, Digital Credit is the yield layer, and Digital Currency is the stable-value liquidity layer. The entire stack transforms Bitcoin's raw volatility into useful financial products without touching Bitcoin itself.

Stable-Value Does Not Equal Risk-Free

This distinction is important.

Digital Currency should not be described as risk-free or sold as an unconditional guarantee. It should be described as: designed to maintain stable value through reserves, liquidity, credit structure, transparency, and risk management.

A well-designed Digital Currency product should be scrutinized with the same questions finance professionals use to evaluate any money market, stablecoin, or short-duration credit product: What are the underlying assets? What is the credit exposure? How much liquidity reserve is there? What is the duration? How does redemption work? What is the seniority? What is the collateral? What is the transparency? Who bears the first loss? How does it perform under stress?

This scrutiny is healthy.

Digital Currency does not eliminate risk; it packages, discloses, manages, and prices risk into a form useful for savers, businesses, payment networks, exchanges, and institutions.

Why Digital Currency Pegs to Fiat

Many Bitcoin believers will ask: Why should Digital Currency peg to the dollar or another fiat currency?

Because the world's debts are still denominated in fiat.

Salaries are calculated in dollars, euros, yen, pesos, and local currencies. Invoices are in fiat. Taxes are in fiat. Mortgages are in fiat. Credit card bills are in fiat. Corporate accounting is in fiat. The banking system, insurance contracts, payroll systems, and financial statements are all fiat-denominated.

Most people do not want their checking account to swing 5% in a day. They want a stable unit of account.

This is why stablecoins found product-market fit. The world wants digital dollars because the dollar remains the dominant unit of account in global commerce.

But the current stablecoin model is incomplete. Stablecoins provide digital liquidity, but holders often do not receive the full economic benefit of the reserve yield. Bank deposits are convenient but typically offer little yield. Money market funds yield but lack native, 24/7 digital transferability. Staked assets yield but require users to accept crypto price volatility and protocol risk.

Digital Currency can combine the best attributes: stable value, digital transferability, daily liquidity, transparent reserves, meaningful yield, and a Bitcoin-backed capital structure.

The fiat peg solves the unit of account problem; Bitcoin solves the capital preservation problem. The dollar is the measuring stick; Bitcoin is the power source.

The Ideal Monetary Experience

Good money should fulfill three functions: medium of exchange, store of value, and unit of account.

BTC is the strongest long-term store of value, but for most of the world, it is not yet a unit of account. Digital Currency solves this bridge problem.

A dollar-pegged, Bitcoin-backed, interest-bearing Digital Currency instrument can act as a medium of exchange because it is stable and transferable; act as a store of value for those measuring in fiat because it yields rather than sitting idle; and function as a unit of account because it is denominated in the currency people already use to price salaries, bills, taxes, and debt.

This is not a rejection of Bitcoin; it is a bridge from the fiat world to the Bitcoin world.

This is Bitcoin's Killer Use Case

Bitcoin's killer use case is not just payments.

The true killer use case is rebuilding the world's currency, credit, and capital markets on a foundation of digital capital.

Bitcoin is the superior asset, but the world does not consist of only one type of investor. Some want raw BTC, some want yield, some want stable value, some want collateral, some want leverage, some want payments, some want growth equity, some want treasury reserves, and some want a dollar balance they can transfer instantly that also pays interest.

The Digital Asset Stack allows Bitcoin to serve all of them. BTC serves capital allocators, Digital Credit serves yield investors, Digital Currency serves savers and payment users, Digital Yield serves return-seeking investors, and Digital Equity serves growth investors. The same Bitcoin foundation supports every layer.

This is how Bitcoin expands from a trillion-dollar asset into a global financial system.

Bitcoin does not need to replace all fiat currencies directly tomorrow. It can back the tools the world already uses today: dollars, credit, accounts, funds, securities, payment assets, treasury products. This is the bridge.

Why This Makes Sense to Finance Professionals

For finance professionals, this framework should look familiar.

The innovation is not that risk disappears, but that Bitcoin becomes the foundational collateral and capital asset for a modern, layered financial system.

Traditional finance has long layered risk: common equity, preferred equity, senior debt, secured credit, money market instruments, levered funds, structured products, bank deposits, payment balances. The Digital Asset Stack applies the same logic to Bitcoin.

The key variables are all standard: seniority, collateralization ratio, liquidity, duration, yield, credit spreads, redemption rights, market depth, disclosure, regulatory treatment, accounting treatment, tax treatment, counterparty exposure.

Bitcoin introduces a superior foundational asset, and capital markets transform that asset into products tailored to different mandates.

This is not anti-finance; it's better finance.

Why This Makes Sense to Bitcoin Investors

For Bitcoin investors, the most important principle is simple: Bitcoin remains Bitcoin.

No protocol changes, no base-layer yield, no staking, no inflation, no touching the 21 million supply cap, no one is forced to abandon self-custody.

Those who want pure BTC can hold pure BTC. Those who want to run nodes can run nodes. Those who want self-custody can self-custody.

The Digital Asset Stack does not compromise Bitcoin's core principles; it merely extends its reach. This is disciplined expansion. The base layer should remain sacred; most innovation should happen on top of it: custody, applications, securities, credit instruments, payment systems, wallets, exchanges, funds, capital markets.

This is how Bitcoin serves billions without forcing everyone into a single, narrow adoption model. It can be a personal self-custodied money, a corporate digital capital, a bank's collateral, a nation's reserve, a family's property, a market's infrastructure, and hope for anyone in economic hardship.

The world builds on Bitcoin because Bitcoin deserves to be built upon.

Why This Makes Sense to MSTR Investors

For MSTR investors, the Digital Asset Stack explains the role of Digital Equity.

Digital Equity is the junior tranche. It absorbs volatility, supports the credit structure, benefits from BTC appreciation, captures residual upside after senior debt is satisfied, and provides the capital structure that makes Digital Credit and Digital Currency possible.

An equity like MSTR is not BTC, is not STRC, is not Digital Currency. Each has a different role.

BTC is Digital Capital, an STRC-like security is Digital Credit, Digital Currency is stable-value yield, Digital Yield is amplified yield, and MSTR-like common stock is Digital Equity.

Equity is more volatile because it is a residual claim; credit is less volatile because it is senior; currency is designed to be more stable because it combines credit with liquidity reserves. This is the logic of a capital stack.

Digital Equity makes the upper layers possible because someone must always bear the residual risk and earn the residual return.

Why This Makes Sense to Crypto Innovators

For crypto innovators, Digital Currency is a major opportunity.

Stablecoins proved the world wants digital fiat. DeFi proved users want yield. Exchanges proved global markets want 24/7 liquidity. Wallets proved value can move at internet speed. Bitcoin proved digital scarcity can be secure, decentralized, and global.

The next step is to combine these breakthroughs into a better product.

A Bitcoin-backed, interest-bearing, stable-value dollar instrument could become the native asset for wallets, exchanges, payment networks, fintech apps, DeFi protocols, treasury platforms, and global commerce.

It can compete with stablecoins that pay users almost no interest, with bank deposits that pocket the spread, with money market funds that yield but lack native digital transferability, and with staked assets that require users to accept token volatility to earn yield.

This is constructive competition. Crypto does not need more speculation for speculation's sake. It needs useful, durable, transparent, yield-bearing financial products that solve real problems for real users. Digital Currency is one of those.

Digital Yield: Not Money, But Useful

Above Digital Currency is Digital Yield.

Digital Yield is not money; it is an investment product.

It can be structured using leveraged digital credit, leveraged digital currency, structured funds, private vehicles, or other instruments, targeting investors seeking higher returns who are willing to accept higher risk, leverage, volatility, or illiquidity.

A leveraged digital currency strategy might target returns significantly higher than its unleveraged counterpart. But that is not a checking account, not a stablecoin, not a savings product for everyone. That is Digital Yield.

This distinction is important. Digital Currency is for stability, liquidity, payments, savings, and working capital. Digital Yield is for sophisticated investors seeking amplified returns. Digital Equity is for investors seeking residual upside. The power of the stack lies in the clarity of each product's role.

The Three-Layer Breakthrough

The key innovation is this three-layer transformation.

Digital Capital: High-volatility, high-energy BTC.

Digital Credit: Bitcoin-backed yield, designed through seniority, structure, yield, and equity support to dampen a significant portion of BTC's volatility.

Digital Currency: Combining Digital Credit with fiat cash equivalents and liquidity reserves to create a stable-value, interest-bearing instrument.

This is the breakthrough. Bitcoin gives us the world's strongest digital capital asset, capital markets transform that asset into credit, and credit plus liquidity reserves transforms that yield into currency.

The world doesn't need everyone to price coffee in satoshis tomorrow. The world today needs better money: money that moves at internet speed, remains stable in the user's unit of account, pays meaningful yield, and is ultimately powered by the strongest digital capital asset ever created.

That is Digital Currency.

Why This is Good for BTC

Digital Currency increases the utility of BTC.

Every dollar of Digital Currency built on Bitcoin-backed credit creates incremental demand for Bitcoin-backed capital structures, creating new reasons to hold BTC, finance BTC, custody BTC, audit BTC, insure BTC, and build services around BTC.

It also brings Bitcoin exposure to investors who cannot handle the volatility of raw Bitcoin. Retirees may not want raw BTC volatility, corporations may not, banks may not, payment companies may not. But they may want a stable-value dollar asset yielding 6%-8% and backed by Bitcoin-backed digital credit.

This brings new capital into the Bitcoin ecosystem. More capital means more adoption, more adoption means more liquidity, more liquidity means greater resilience, and greater resilience means a stronger Bitcoin.

Why This is Good for the Crypto Industry

The crypto industry needs a better monetary foundation.

Many crypto users want dollars, many crypto investors want yield, many crypto builders want programmable assets, many crypto platforms want liquid collateral, and many crypto applications need a stable unit of account.

Digital Currency built on Bitcoin-backed credit gives the industry a better foundational product: a stable-value, interest-bearing digital dollar powered by Bitcoin.

It can live on exchanges, in wallets, in funds, in accounts, on payment networks, and eventually wherever digital value flows. It doesn't force users to choose between zero-yield stablecoins and volatile staked tokens; it gives them another option: stable-value, yield-bearing digital currency built on Bitcoin-backed capital. This is good for crypto.

Why This is Good for Investors

Investors should not be forced into a single risk tranche.

The Digital Asset Stack gives every investor a choice. Want digital capital? Hold BTC. Want digital credit? Hold STRC-like instruments. Want digital currency? Hold stable-value, yield-bearing instruments. Want digital yield? Hold leveraged or structured products. Want digital equity? Hold MSTR-like common stock.

It's a full menu. Savers can hold digital currency, yield investors can hold digital credit, growth investors can hold digital equity, long-term believers can hold BTC, and sophisticated investors can hold digital yield. The same Bitcoin foundation supports everyone. This is how Bitcoin becomes accessible to every mandate.

Why This is Good for the World

The world needs better money.

Billions want dollars because they are liquid, familiar, and widely accepted. But they also want yield, transparency, liquidity, and protection from debasement erosion.

Today, many are forced to choose between unstable local currencies, low-yield bank deposits, zero-yield stablecoins, volatile crypto assets, or financial products they cannot access.

Digital Currency can improve this. It can offer stable value, digital liquidity, daily redemptions, and meaningful yield. It can help savers, businesses, payment companies, emerging markets, exchanges, institutions, and anyone who wants better money but doesn't want the volatility of raw BTC.

The analog world built its economy on gold, real estate, banks, deposits, credit, equity, funds, and payment networks. The digital world will be built on BTC, digital credit, digital currency, digital yield, and digital equity.

Bitcoin is digital capital. Digital credit transforms it into yield. Digital currency transforms it into daily utility. Digital yield amplifies it. Digital equity finances it.

The foundation layer remains sacred; the capital stack remains open.

This is the modern Digital Asset Stack. This is how Bitcoin becomes the foundation for a better financial system.