Author:Ben Harvey

Compilation: TechFlow

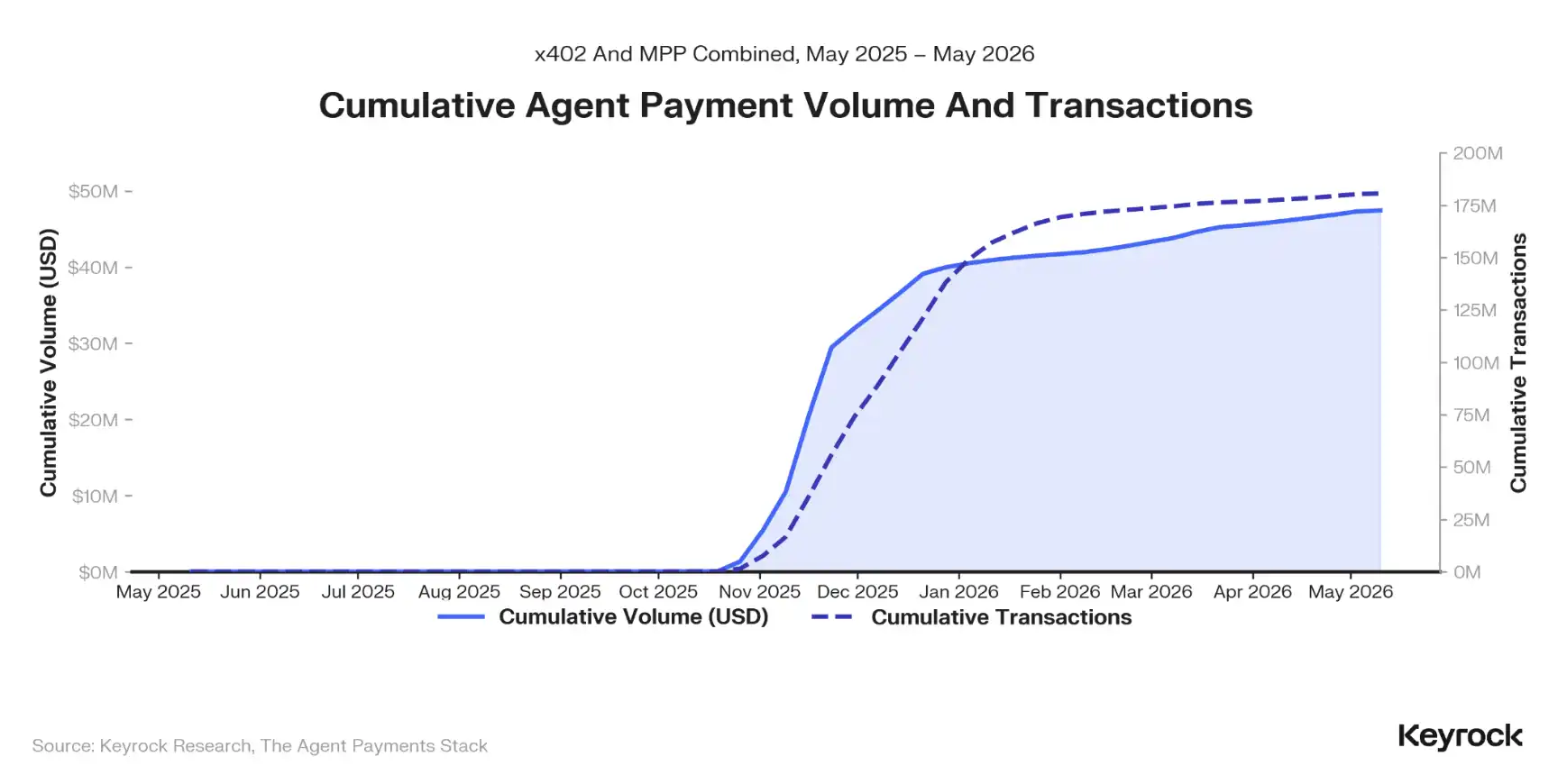

TechFlow Introduction: A year ago, machine-to-machine payments were just a concept. Now, Coinbase, Stripe, Google, and Visa have deployed four competing architectures. AI Agents have already completed 176 million transactions and settled $73 million. Traditional giants have spent over $8 billion on acquisitions to secure their position. This is not a future narrative but an ongoing restructuring of payment infrastructure—whoever controls the most layers will capture the most value.

A year ago, machine-to-machine payments were just a concept. Now four competing payment architectures are live, backed by Coinbase, Stripe, Google, Visa, and American Express. AI Agents have settled over $73 million across 176 million transactions. Traditional giants have invested over $8 billion in acquisitions to stake their claim in this new payment stack.

This report, produced in collaboration with Keyrock, Coinbase, and Tempo, examines how this payment stack is being assembled, whether the economic model works, and the obstacles it faces.

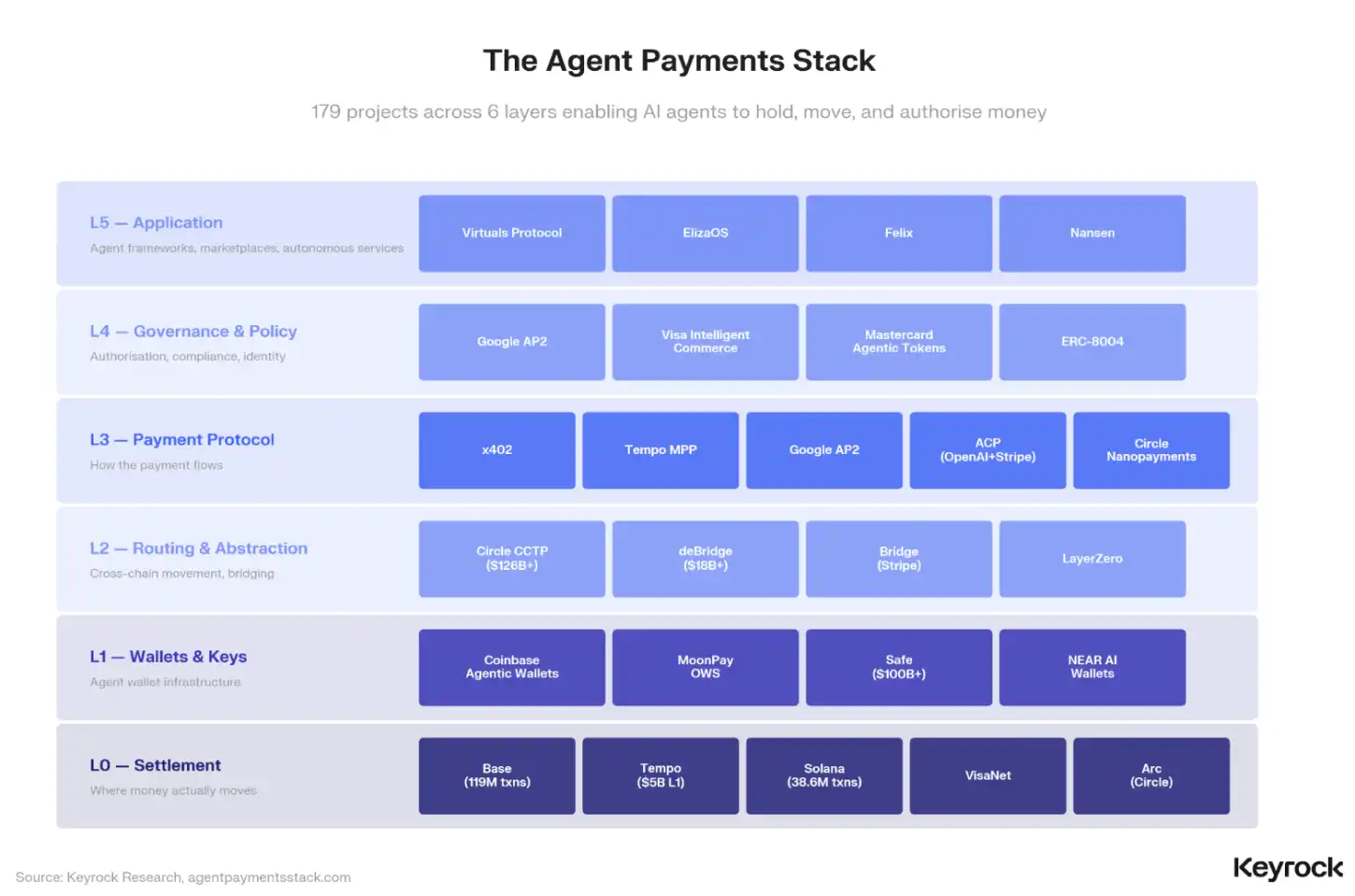

Protocols Aren't Competing, They're Stacking

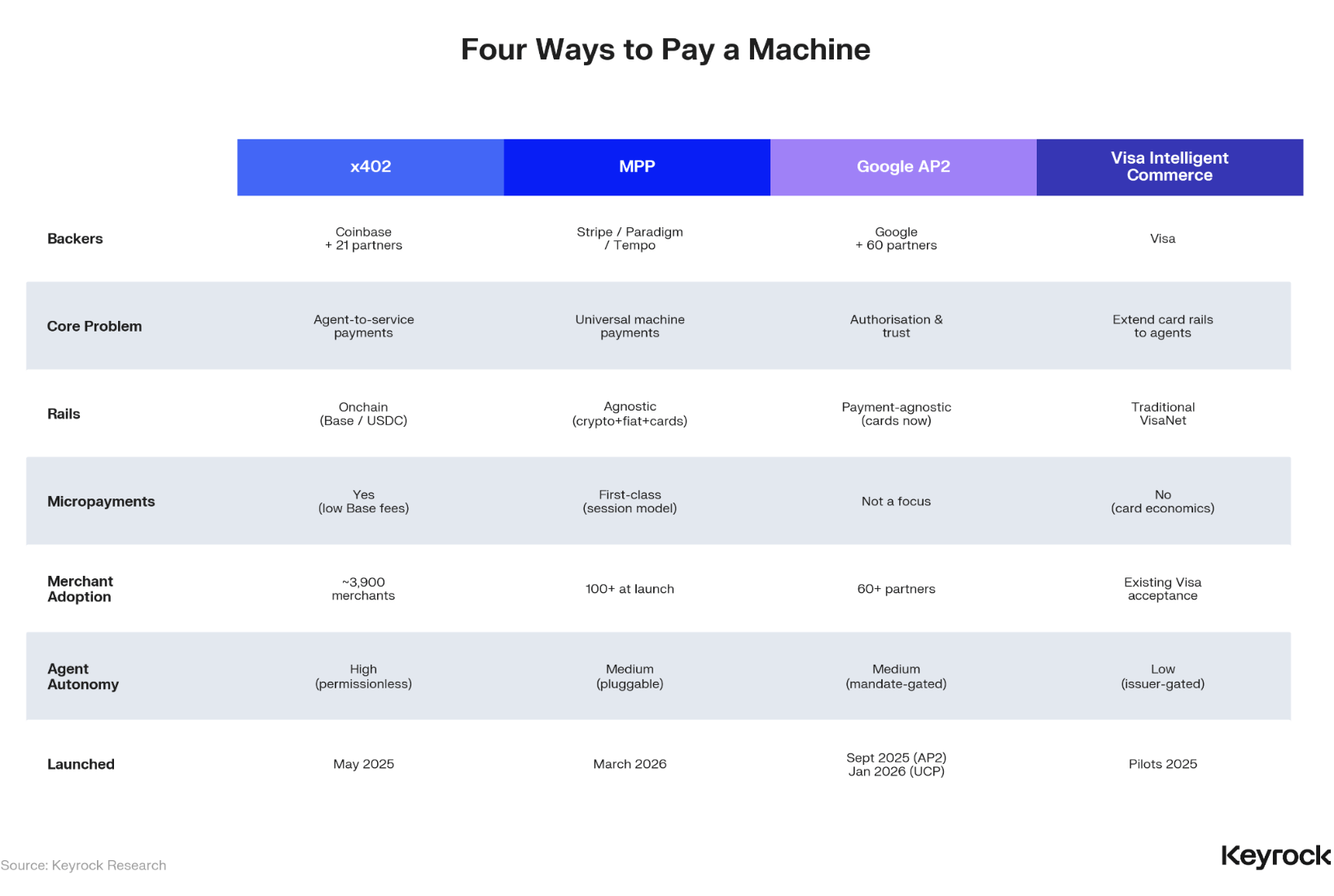

In September 2024, if you wanted an AI Agent to pay for something, there was essentially one insecure option. Twelve months later, four architectures exist, backed by some of tech's biggest companies.

Coinbase built x402, a crypto-native protocol that turns stablecoin wallets into a universal API key. Stripe and Tempo launched MPP, a payment-method-agnostic standard handling bank cards, cryptocurrency, and Lightning through a single HTTP flow. Google assembled AP2, an authorization layer allowing users to delegate payment permissions to Agents via cryptographic signatures. Visa expanded its existing card rails to provide AI-ready tokenized credentials.

What most coverage misses is that these four proposals are not purely competitive. Protocol layers do overlap, but the more important dynamic is that they are assembling into a payment stack. The right question isn't "which protocol will win?" but "which companies control the most layers and thus capture the most value?"

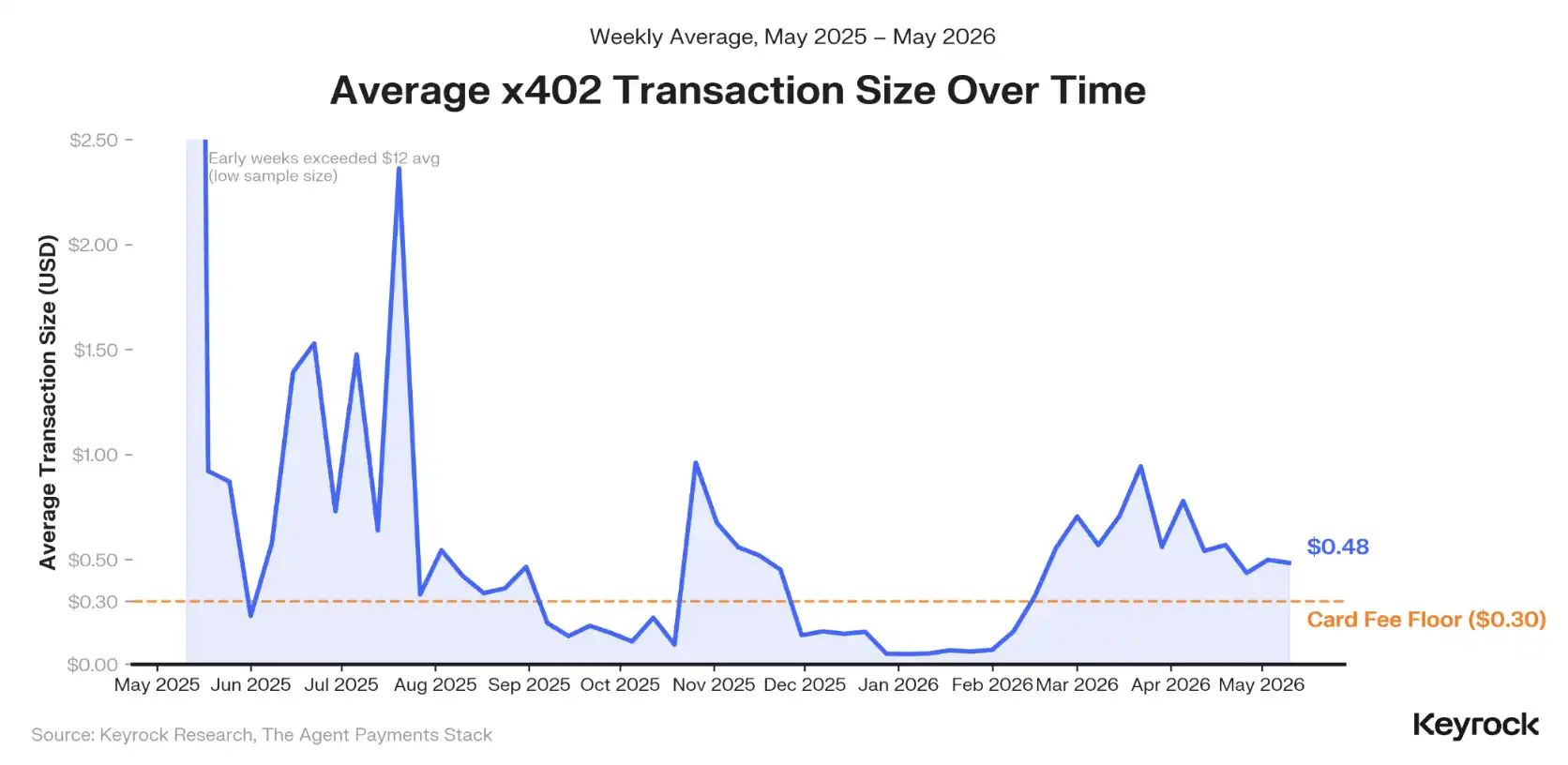

The $0.30 Wall

Among the 176 million x402 payments processed so far, the median transaction amount falls between $0.01 and $0.10. 76% of the activity is below the $0.30 baseline card processing fee. This figure almost single-handedly explains why traditional payment rails cannot serve this market. A fixed processing fee of approximately $0.30 per transaction renders micropayments unprofitable. An Agent cannot route a 3-cent payment for a weather API call through Visa.

Layer 2 stablecoin settlement costs $0.0001. For Agents, this means blockchain rails are a necessity.

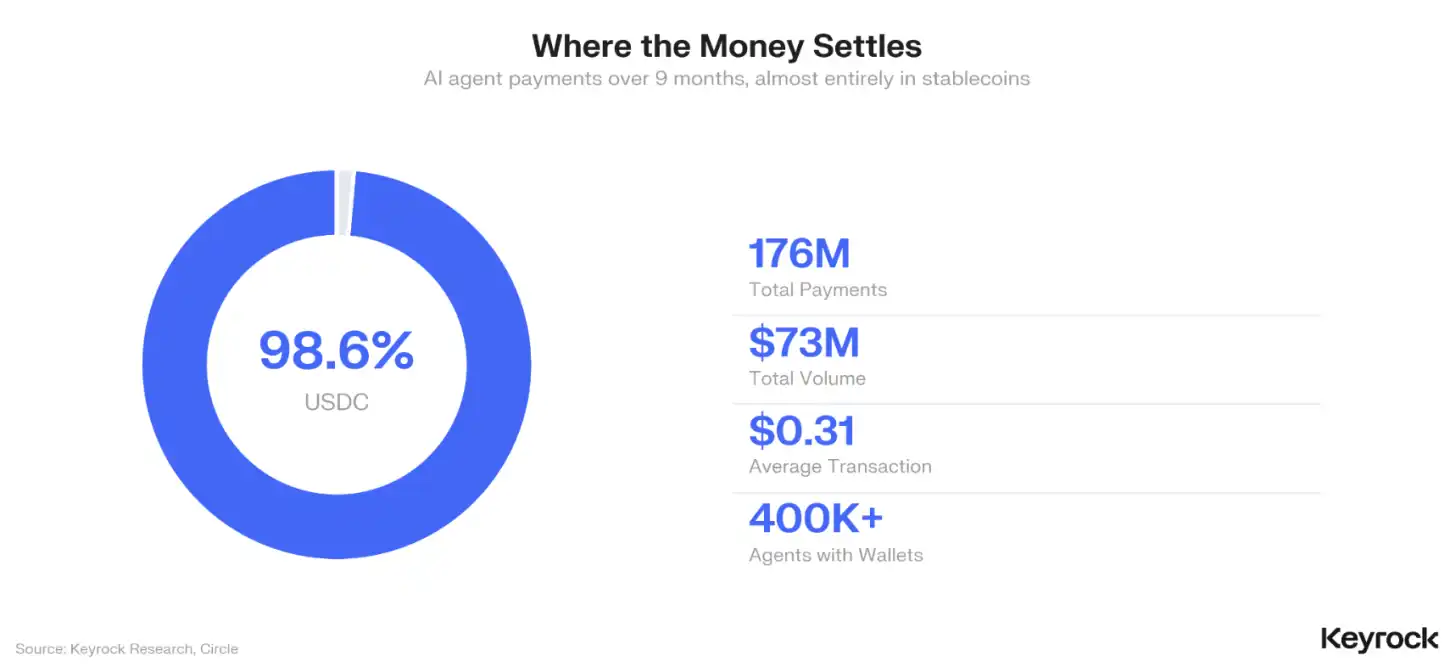

Single Stablecoin Dominance

Of those 176 million payments, 98.6% were settled in USDC. Stablecoins have all but defaulted to winning the settlement layer for machine commerce; they are the only instruments that can process small-value transactions without the economic model collapsing.

This concentration is both validation and a vulnerability. It validates Circle's position as the default settlement asset, but it also means the entire Agent payments ecosystem depends on a single stablecoin issuer's reserve management, regulatory standing, and technical infrastructure. No one in the industry is discussing this publicly. We think they should.

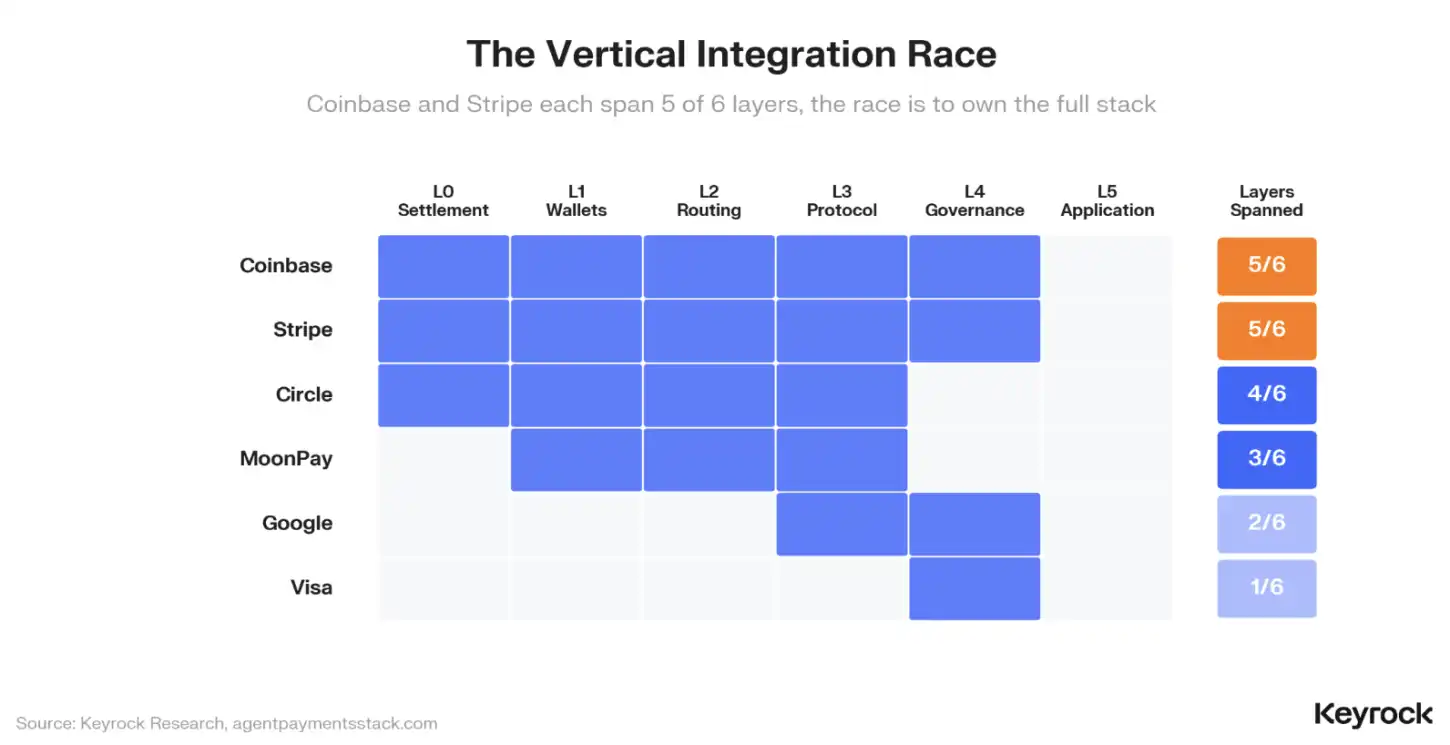

The Race for Vertical Integration

Coinbase and Stripe each cover five of the six layers in the emerging payment stack. Coinbase controls the settlement layer (Base), wallets (Agentic Wallets), routing (internal infrastructure), the payment protocol (x402), and governance (as an AP2 collaborator). Stripe forms a mirror image through Tempo (settlement), Privy (wallets), Bridge (routing, acquired for $1.1 billion), MPP (protocol), and its compliance infrastructure.

Over the past 12 months, traditional giants have spent over $8 billion on acquisitions to fill gaps in their stack coverage. Capital One acquired Brex for $5.15 billion, Mastercard spent $1.8 billion on BVNK, and Stripe bought Bridge. These are infrastructure consolidation moves by companies that see machine payments as a natural expansion of their core business.

From Bot Activity to Agent Commerce

The machine economy has arrived. It just hasn't started doing commerce yet. But the signals are clear: AI Agents account for 37% of all Safe transactions on Gnosis Chain, peaking over 75%. Coinbase has deployed tens of thousands of fenced Agents. Over 104,000 Agents are registered across 15 or more directories and registries.

The shift from extractive bot activity to productive Agent commerce is underway. The payment infrastructure studied in this report is what makes this possible.

Regulation as a Constraint

MiCA, the GENIUS Act, and the EU AI Act will all reach enforcement stages within weeks of each other in mid-2026. None of them address autonomous machine-to-machine transactions. This is not a future problem; it's a current one, playing out on a real-time timeline with real capital at stake.

What Happens Next

The market is moving towards greater Agent autonomy, but we believe the pace will not be set by technology—that's largely ready. The pace will be set by the trust infrastructure that makes it safe. The fully permissionless vision is attractive in theory, but it assumes a level of AI reliability that doesn't exist yet. Until Agents stop hallucinating, they probably shouldn't have unsupervised access to user funds.

We find the bottom-up argument the most compelling framework for what happens next. Crypto rails have already default-won for micropayments. As transaction volumes grow and trust infrastructure matures, increasingly larger transaction amounts will migrate on-chain. The question isn't whether machine-native payments can scale, but how quickly the trust layer can catch up with the settlement layer.

This article is a summary of the report's core findings. The full report delves deeper into the data, including analysis of protocol architectures, insights from interviews with Coinbase and Tempo, economic modeling of transactions, and the regulatory landscape.