Author: Yi.Pineapple

LPs no longer buy dreams; GPs must sell products. This article will attempt to categorize current crypto fundraising products into three types: Primary, Liquid, and CeFi / DeFi Native Yield. The first part will focus on Primary: After VC blind pools lose their appeal, who remains at this table, and who must prove themselves anew? The answer is at the end; feel free to scroll down.

Note: This article aims to provide a landscape description of the entire crypto fundraising market. The first part mainly categorizes and explains the market status from a product perspective, while the next part will analyze it more from the LP's perspective. As the author is primarily in the Asian market, this article may have a regional bias.

Market Status

After losing the grand vision, most Crypto GPs who failed to earn excess returns this cycle must now ground themselves and launch a product with PMF (Product-Market Fit). They must either re-prove their ability to generate excess returns for LPs in niche markets or demonstrate their capacity to solve specific problems for LPs/partners to survive.

- For most GPs, the market has long transitioned from a phase of "buying a future vision" to one of "buying a specific product."

- LPs have lost patience and no longer want to gaze at the stars and the ocean; they want to see immediate, tangible, and relatively certain opportunities to make money.

- Crypto LPs have lost trust in the market and are no longer willing to easily believe the "next cycle" narrative (this has been discussed too much and won't be elaborated here). Moreover, many haven't made easy money this cycle; when money becomes harder to earn, investment actions tend to become more cautious and conservative.

- Most traditional LPs have also completed a round of learning, moving past the storytelling phase. The 2020/2021 bull market was the peak of market FOMO. Dollar funds were cheap (Treasury yield near 0), LPs were making relatively easy money (on the eve of the economic downturn), and Crypto was in an explosive growth phase (with numerous rags-to-riches stories and dreams to sell). Back then, many were willing to impulse buy into the dream even if they didn't fully understand crypto, or they entered strategically to learn.

- AI and declining labor costs have also changed GPs' niche. The cost for LPs to learn, hire, analyze data, trade, and make small direct investments is decreasing. The trend of LPs transforming into GPs is significant. GPs who only offer vague capabilities like "I understand crypto" will find their value increasingly precarious.

- In terms of storytelling, unless it's a strong US-based fund with a proven track record pitching visions in specific niches (like a16z leveraging its AI advantage to pitch crypto * AI, or Dragonfly pitching internet capital markets based on its investments in Ethena/Polymarket), opportunities remain. In Asia, this niche is already difficult, as both crypto projects and funds, to some extent, only get the chance to tell stories if they are "White Papers."

Product Landscape

This article divides crypto fundraising products into three main categories for discussion: Primary, Liquid, and CeFi / DeFi Native Yield (Note: This classification is not entirely precise, with some blurry areas between the three). (*This part covers Primary first)

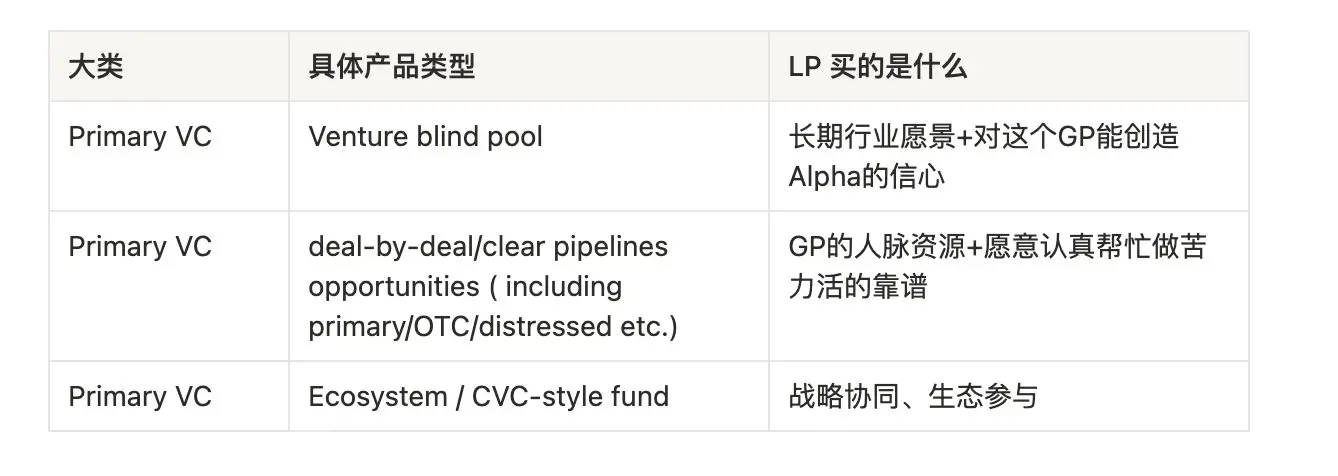

Primary VC:

In terms of transparency, they can roughly be divided into blind pools and those with clear pipelines.

In terms of liquidity, they can roughly be divided into primary and primary-secondary markets.

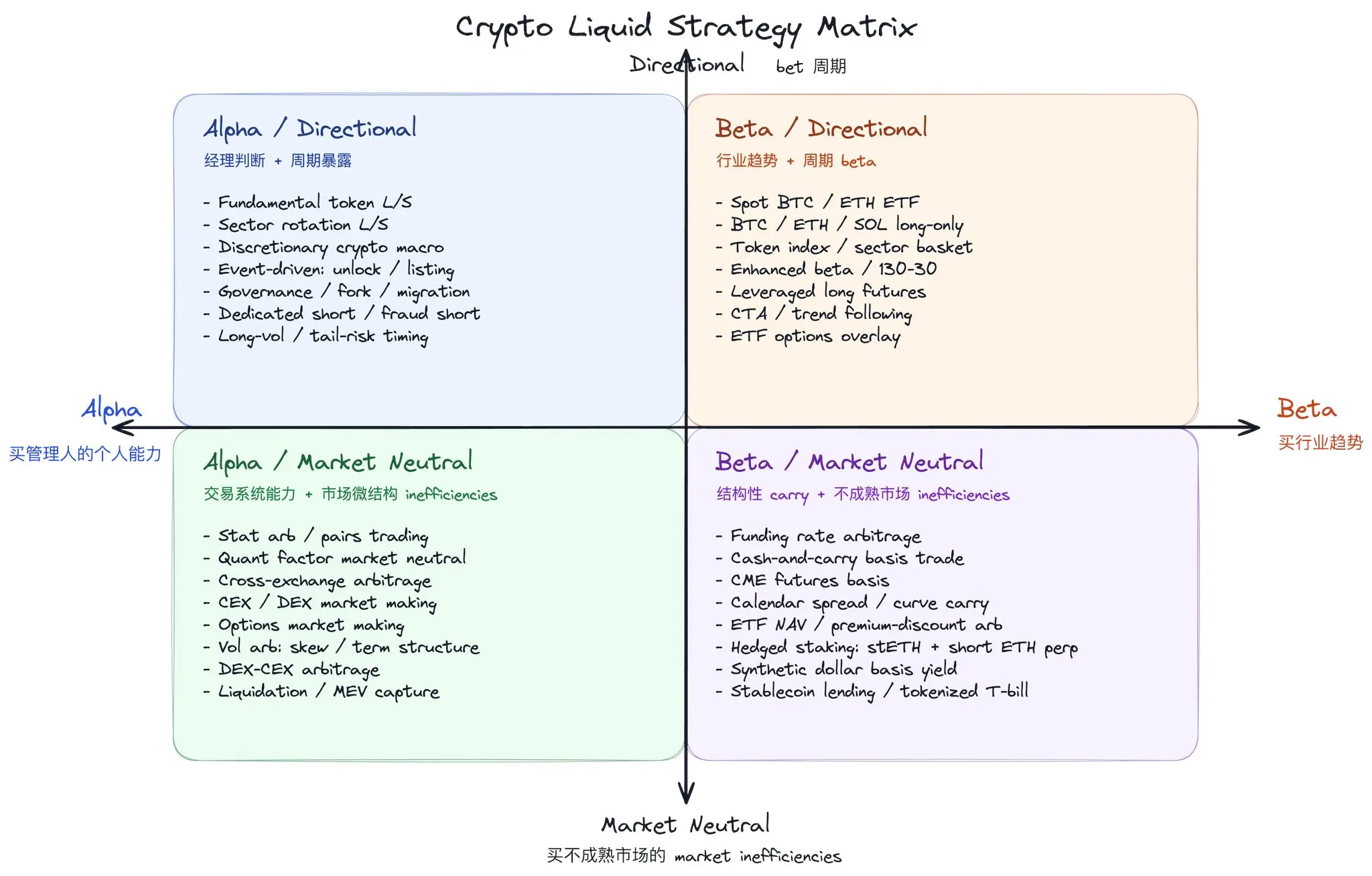

Liquid:

Divided by source of returns, roughly into alpha-focused (buying the GP's personal skill) and beta-focused (buying industry trends).

Divided by directionality, roughly into directional (buying cycle timing) and market neutral (buying market inefficiencies in immature markets).

There are many ways to categorize; this is just one idea.

CeFi/DeFi Native Yield:

Theoretically, CeFi/DeFi Native Yield could be seen as a source of returns within or spanning both the crypto primary and liquid markets. The main reason for separating it is that from a TradFi investor's perspective, they usually use traditional financial frameworks to understand crypto: for example, crypto VC can be seen as a sub-sector of VC, and staking/lending yield can be analogous to fixed income or cash management products.

However, crypto does have some mechanisms and playbooks not fully mirrored in traditional finance, such as farm-and-dump, points/airdrop farming, protocol incentives, and on-chain liquidity mining. These are more like crypto-native distribution, customer acquisition, and incentive mechanisms, warranting separate discussion.

Secondly, for many Crypto Native Investors, their initial entry point to understanding financial markets was not the traditional equity/bond market, but crypto-native scenarios like exchange wealth management products, staking, DeFi lending, providing liquidity, points/airdrop farming, and basis trades. Therefore, they might not first translate this yield into TradFi terms like fixed income, cash management, or alternative yield. Instead, they more naturally understand it from angles like protocol incentives, liquidity provision, token emission, on-chain risks, counterparty risk, and capital efficiency.

For Crypto Native LPs, accessing this yield doesn't require a GP, maybe just a reliable key account manager.

For TradFi LPs, some institutions are now packaging this yield into fund products to sell to them.

Primary Market

From the perspective of the entire primary market, crypto VC is just a sub-sector under the broad VC category. 2021 was a crazy year; whether crypto or non-crypto, the real returns from that vintage are poor. As a cruel fact, LPs have learnt their lessons and are tired of any product with ultra-long lock-ups (traditional VC often 10 years, crypto VC often 5-10 years). Because without hard locks, they at least have a chance to withdraw some money if circumstances change.

In some sense, crypto is worse off than traditional VC because the grand vision has collapsed. It is not a new industrial revolution, at most a revolution in financial infrastructure. This judgment is not to disparage crypto; financial infrastructure revolution is still important, but it's not as grand as many imagined in the last bull run. Worse, the market was too immature back then; many projects were funded without sufficient due diligence and legal protection. Many failures are a combination of investment failure and founder exit. Too many articles in the industry describe the current misery, so we won't elaborate here.

Investing in VC is like VC investing in startups: it's a power-law business, a lottery-like business. As long as someone is willing to buy lottery tickets, this table won't disappear.

Why LPs invested in crypto VC back then, and why these reasons have weakened now:

1. Invest to capture the beta of the industry

This reason was particularly true for TradFi LPs. It held early on because market choices were few. For outsiders, onboarding, buying tokens, going on-chain, using CEXs, and managing wallets were difficult. They feared losing private keys and CEXs running away. Investing in VC seemed like a more reliable access point.

But today, a traditional LP entering crypto has a full suite of choices: BTC ETF, ETH ETF, crypto ETPs, DATs, custody accounts, SMAs, structured products. More importantly, these products don't require learning on-chain operations; they trade like stocks.

According to CoinShares, global digital asset investment products AUM (ETF/ETP/trust/closed-end funds, etc.) reached about $156.9B in mid-May 2026. This number isn't total industry AUM, just a tally of listed or quotable products, but it shows: gaining crypto exposure no longer requires investing in a VC blind pool.

However, for long-term capital with clear mandates (e.g., endowments, etc.), this reason still applies. For them, positioning in an industry often involves a basket of assets, so there's still likely a 1~2% allocation to Crypto VC.

2. Invest for deal accessibility

This typically applied to crypto LPs and some TradFi LPs with strategic layout visions. Many such LPs didn't have the resources/time/capability to build their own investment teams, so they gave money to GPs hoping for good deal access.

But they later found this reason unstable. When the market was good, GPs themselves had insufficient allocation, and LPs struggled to get real access. When the market was bad, competition wasn't fierce; if you were willing to reach out, getting allocation wasn't that hard.

For traditional LPs, access had another meaning: they knew nothing initially but hoped to enter the ecosystem and gain insider information by investing in crypto-native GPs. It was a form of strategic investment when there was no clear strategic target. Now the situation has changed. Many traditional LPs have either left for hotter fields like AI, or have developed their own internal teams. AI and cheap analysts have narrowed the knowledge gap. New learners still exist, but they learn faster and have more paths. Investing in the primary market with ultra-long lock-ups is not necessarily the optimal choice for them anymore.

3. Invest for superior judgment

This is the trickiest part. In a rapidly evolving market, unless a GP can continuously self-iterate, the judgment premium disappears quickly. The rules change every cycle, but people don't change easily (is this another form of "old habits die hard").

We must face a harsh reality: Most GPs did not prove to LPs they had superior judgment in the last cycle.

For traditional LPs, part of the reason for investing in crypto-native GPs was to educate themselves and learn the industry through the GP's judgment. This typically applied to two types: companies wanting to strategically enter Web3 (like internet giants, etc.), and sophisticated TradFi investors (like traditional GPs or family offices) who wanted to later do their own direct Web3 investments. The learning phase is over. Only a few GPs who have truly proven superior judgment remain on their investment lists.

For crypto LPs, they found it better to lose money themselves than to bet on a GP's judgment. Losing money yourself at least has emotional value, and you don't pay management fees.

4. Invest for deal-making ability

From an investment return perspective, deal-making ability primarily manifests as whether it can achieve good final exits for projects. Ideally, it's best to help projects achieve healthy growth for good secondary market returns. Failing that, the ability to organize the next round of financing is also important (essentially, the difference between relying on retail or large investors to take over).

However, as a form of financial innovation, Crypto sometimes resembles a large-scale capital game. Sometimes, investment is just a form of interest exchange, ensuring aligned interests to make money together relatively safely.

5. Invest for reputation

For some large LPs, money invested in a single VC might only be 1% of their overall portfolio, insignificant. Sometimes they invest in a GP just to be cool (like investing in A16Z). But most GPs aren't in this category.

Who can still stay at the primary table

From a pure capital source perspective, the players most likely to remain at the primary table are:

Funds large enough to enter the mandate of endowments/other similar long-term patient capital. These institutions buy crypto VC as lottery tickets without short-term funding pressure.

FOs, companies, and HNW individuals investing proprietary capital in primary crypto investments. FOs/HNWs are more likely to run accelerator-like, very early-stage funds; companies are more likely to make direct strategic investments/acquisitions.

The few funds that struck gold/bought BTC this cycle and genuinely delivered excess returns to LPs. LPs believe they can win next time.

Funds with clear deal-making ability, possessing ecosystem resources to exchange interests with LPs.

For other players, if trust is lost, it might be better to restart mentally and rebuild trust. Re-prove the ability to generate excess returns for investors in a niche, or provide some specific service/value, then scale based on that.