Author:Chuk @Stablecoin Blueprint

Compiled by: Payment 201

Introduction: Not the 'Tokenization' You Think

The Depository Trust & Clearing Corporation (DTCC) has received a "no-action letter" from the U.S. Securities and Exchange Commission (SEC), allowing it to begin tokenizing securities infrastructure. This is a meaningful upgrade to the "plumbing" of the U.S. capital markets: DTCC holds $99 trillion in securities and supports annual trading volumes measured in "quadrillions."

However, the market's reaction to this announcement reveals an "expectation vs. reality gap": What is being tokenized are security entitlements, not the shares themselves, and this distinction dictates everything that follows.

Today's "security tokenization" narrative is not a single, unified future arriving all at once. In fact, two distinct models are emerging simultaneously: one is an internal modernization upgrade to the current "indirect holding system"; the other is redefining the very concept of "share ownership." (Note: For simplicity, this article does not distinguish between DTCC's subsidiary DTC and its parent company.)

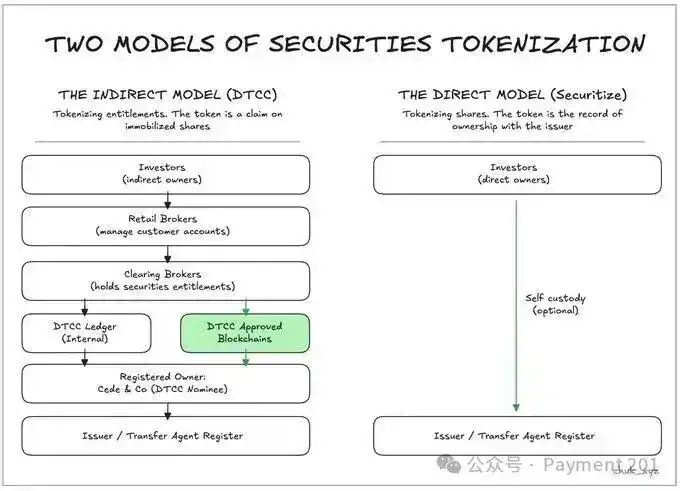

How Securities Ownership Actually Works Today

In the U.S. public markets, investors do not directly hold shares of a company. They exist within a chain of multiple layers of intermediaries. At the bottom layer is the issuer's shareholder registry, typically maintained by a transfer agent. For almost all public companies, only one name appears on this registry: Cede & Co. — DTCC's nominee. This means the issuer does not need to maintain records for millions of individual shareholders.

Above this is the DTCC, which holds shares in bulk in an "immobilized" manner.

DTCC's direct participants are called clearing brokers, who handle custody and settlement on behalf of retail brokers, who are the entities that interface directly with customers and receive trade orders. The DTCC records the number of shares each participant is "entitled to."

At the very top are the investors. They do not actually own specific shares; instead, they hold "security entitlements"—a legally protected claim on the underlying shares, a right against their broker, which in turn holds down through the clearing broker to the DTCC.

What DTCC is tokenizing are these security entitlements, not the underlying shares. This upgrade improves system operation but does not solve the limitations inherent in the multi-layered intermediary structure itself.

In other words, DTCC is tokenizing "claims"; the direct model tokenizes "the shares themselves." Both are called "tokenization," but the problems they solve are completely different.

Why This Upgrade?

The U.S. securities system is very robust, but its architecture still has some limitations.

-

Settlement relies on delayed, business-hours processing;

-

Corporate actions and reconciliation still run on batch messaging systems, not shared state;

-

Because ownership is a complex network of multiple layers of intermediaries, each with its own technology upgrade cycle, real-time processes cannot be supported unless every layer enables the capability, and DTCC is the key "gatekeeper" among them.

This design also "locks up" capital: the long settlement cycle requires tens of billions of dollars in margin to manage risk between trade execution and final settlement. These optimization designs originated from an era when "money moved slowly and was expensive." If the settlement cycle could be shortened, or if some participants could opt for "instant settlement," the scale of capital tied up could be significantly reduced, costs lowered, and competition increased.

Some of these benefits can be achieved by upgrading existing infrastructure; but others—especially those involving direct ownership and faster innovation cycles—require entirely new models.

Tokenizing the Existing System (The DTCC Model)

In the DTCC's path, the underlying securities remain "immobilized" and continue to be registered in the name of Cede & Co.

What changes is the载体 of the "record of entitlements": it no longer exists solely in proprietary ledger systems but has a digital twin on an "approved blockchain."

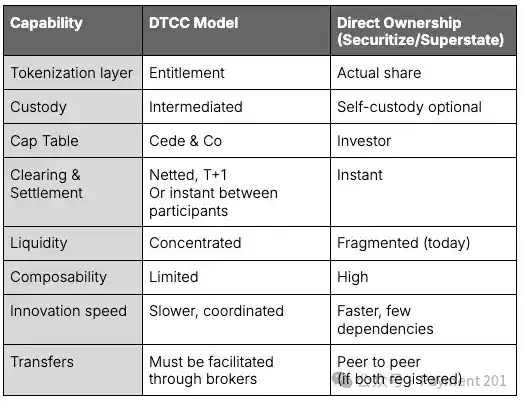

This is crucial because it enables modernization without disrupting the existing market structure: DTCC can introduce 24/7 fund flows between participants, reduce reconciliation burdens, and ultimately facilitate faster use of entitlement tokens in collateral liquidity and automated workflows, while still retaining the efficiencies of the centralized system, such as net settlement.

Multilateral netting can compress trillions of dollars in gross trading activity into hundreds of billions in final settlement, an efficiency that is a core advantage of the current market structure.

But these boundaries are "deliberately set": these tokens do not make the holder a direct shareholder. They remain permitted, revocable rights under the same legal framework. They cannot become freely composable collateral in DeFi, cannot bypass DTC participants, and do not change the issuer's shareholder records.

In short: it improves the system we have, but retains the intermediary structure and its advantages.

Tokenizing "Ownership Itself" (The Direct Holding Model)

The second model starts "outside the boundaries" of the DTCC model: it aims to tokenize not entitlements, but the shares themselves. Ownership is registered directly on the issuer's shareholder registry, maintained by the transfer agent. When the token is transferred, the shareholder record changes accordingly. Here, Cede & Co. is no longer in the chain of ownership.

This unlocks features that are structurally impossible in the DTCC model: self-custody, direct relationships between investors and issuers, peer-to-peer transfer, and composability with programmable and on-chain financial infrastructure (such as collateralization, lending, and innovative structures not yet invented).

This model is not theoretical. Galaxy Digital shareholders can already tokenize and hold shares on-chain through Superstate, appearing on the issuer's cap table. And in early 2026, Securitize will enable the same mechanism, with 24/7 trading through a regulated broker-dealer system.

However, the trade-offs are very real: without the indirect holding system, liquidity is fragmented, and netting efficiency disappears. Brokerage services (such as margin trading, securities lending) must be redesigned. Operational risk also shifts from intermediaries to the holders themselves.

But the autonomy offered by direct ownership allows investors to choose these trade-offs themselves, rather than having them imposed. Within the DTCC framework, this "choice" is nearly impossible, as any innovation regarding entitlements must go through multiple approval processes involving governance, operations, and regulation.

Overall, the DTCC model is more compatible and scalable; the direct holding model allows for more innovation around self-custody.

Why These Models Are Not Currently in Competition

The DTCC model and the direct holding model are not in competition; they solve different problems. The DTCC's path is an upgrade to the existing indirect holding system, preserving net settlement, liquidity concentration, and system stability. It targets institutions that require scale, settlement guarantees, and regulatory continuity.

The direct ownership model serves a different set of needs: self-custody, programmable assets, and on-chain composability. It targets investors and issuers who want new capabilities, not just greater efficiency. Although the direct holding model may one day reshape the entire market, achieving this will require years of technological, regulatory, and liquidity migration transition; it cannot happen overnight. The evolution of clearing rules, issuer behavior, participant readiness, and global interoperability moves slower than technological progress.

The realistic future is one of parallel coexistence: infrastructure modernization on one side, ownership innovation on the other. Currently, neither can replace the other.

What It Means for Market Participants

These two tokenization models have distinctly different impacts on the market ecosystem:

Retail Investors:

For retail investors, the DTCC upgrade is almost "invisible." Retail brokers already abstract away most friction for their clients (e.g., fractional shares, instant buying power, weekend trading), and these advantages will still be provided through brokers.

It is the direct holding model that will bring real change: self-custody, peer-to-peer transfer, instant settlement, and the potential to use stocks as on-chain collateral. Currently, stock trading is beginning to appear on platforms like Coinbase, Kraken, and wallets like Phantom, but most still rely on "wrapped representations." In the future, these tokens could become registered equity, not a synthetic layer.

Institutional Investors:

Institutions are the ones who benefit the most from DTCC tokenization. Their operations rely on collateral liquidity, securities lending, ETF processes, and multi-party reconciliation, and tokenized entitlements can significantly reduce burdens and increase speed in these areas.

The direct holding model is more attractive to some institutions, particularly trading firms seeking the advantages of programmable collateral and settlement. But due to liquidity fragmentation, broader institutional adoption will start at the edges.

Brokers & Clearing Houses:

Brokers are at the center of this change. In the DTCC model, their role is reinforced, but innovation also gravitates towards them: clearing houses that最早 adopt tokenized entitlements can gain a differentiated advantage, and vertically integrated companies can develop new products on top of this.

In the direct holding model, brokers do not disappear—they are reshaped. Licensing and compliance still exist, but new "on-chain native intermediaries" will emerge to serve users who value direct ownership features.

Conclusion: Investor Choice is the Real Winner

The future of tokenized securities lies not in which model "wins," but in how the two evolve and interact. The "entitlement tokenization" model will modernize the core of the public markets; the "direct ownership" model will expand from the edges, offering self-custody and programmable features.

As migration between the two models becomes smoother, we will see a broader market landscape: existing rails become faster and cheaper; new rails support new behaviors that the existing system cannot承载. Both paths will create winners and losers, but the existence of a direct ownership channel means: investors are the ultimate winners—they will get better infrastructure due to competition and have the right to choose freely between the two models.